Building Ordinance or Law Coverage – How does it work? Your house is damaged. The fire crew is gone, the tarp is up, the water is drying out, and you finally expect your insurance company to do what you paid them to do.

Then the estimate shows up.

It covers obvious damage. Burned framing. Wet drywall. Missing shingles. Maybe some flooring. But the adjuster leaves out the parts that decide whether you can rebuild legally. New electrical requirements. Demolition of the undamaged section the town says must come down. Mandatory elevation work. Wind protection upgrades. Accessibility requirements in the right setting. Suddenly the claim that looked manageable turns into a financial ambush.

That is why building ordinance or law coverage matters so much. It is also why insurance companies love keeping it confusing. If they can make you think your claim is only about visible damage, they can low-ball the code-related costs that make a real rebuild possible.

The Second Disaster Your Insurance Company Creates

A lot of homeowners think the disaster ends when the flames are out or the storm passes. It doesn’t. The second disaster starts when the carrier’s adjuster hands over a narrow estimate and acts like the missing items are your problem.

What homeowners hear from the adjuster

The language is almost always the same. “We owe for direct damage.” “That upgrade isn’t caused by the loss.” “That’s a code issue, not a covered issue.” “Your policy doesn’t pay to improve your house.”

That sounds reasonable until the inspector gets involved. The city or county doesn’t care what your carrier wants to pay. The inspector cares whether the rebuilt structure complies with current code. If it doesn’t, your permit stalls, your contractor can’t proceed, and you are stuck in the middle.

Why this feels so brutal

You’re already dealing with displacement, contractors, temporary living arrangements, and a damaged property that may be getting worse by the week. Then the insurer takes a technical coverage issue and turns it into an advantage.

They know ordinance or law language is frequently misunderstood on the first read. They know it’s often assumed that “replacement cost” means the house will be rebuilt the way the law now requires. It often doesn’t.

Practical rule: If the insurer’s estimate rebuilds the damaged area but ignores what the building department requires, the estimate is incomplete.

Frustrated homeowners get trapped in this scenario. They think they are arguing over price. They are not. They are arguing over scope, and scope controls the money.

The carrier wants to shrink the claim to the obvious damage. You need to force the claim to include the legal consequences of that damage. That means code-triggered demolition, code-triggered upgrades, and the cost of rebuilding in a way the jurisdiction will approve.

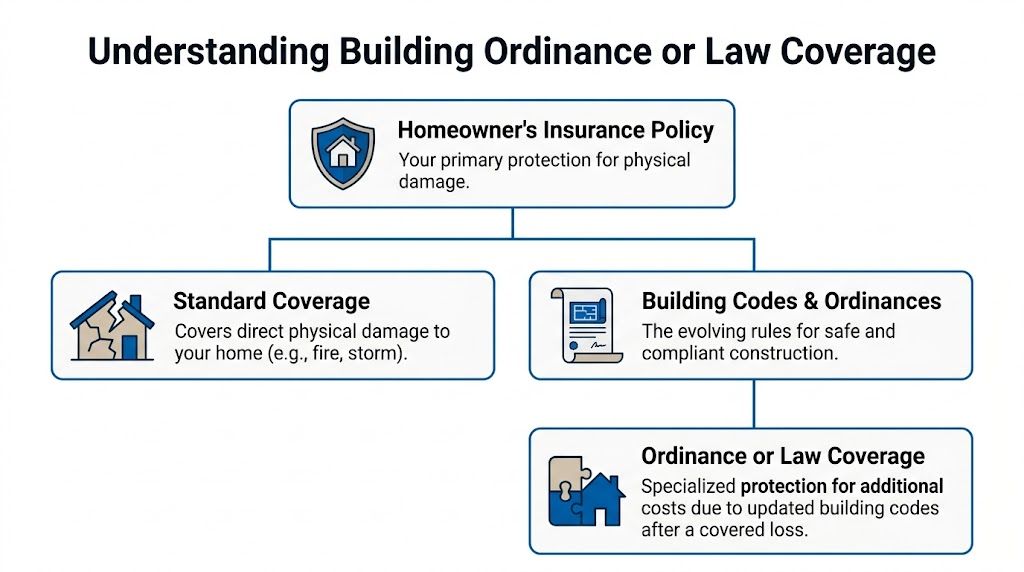

What Is Building Ordinance or Law Coverage

Think of your property policy this way. Standard coverage insures the physical house. Building ordinance or law coverage insures the consequences of the rules that govern how that house must be rebuilt after a covered loss.

The default limit is usually too small

In standard HO-3 policies common in North Carolina and Virginia, ordinance or law coverage is typically an additional coverage limited to 10% of Coverage A, and a $300,000 dwelling limit would provide $30,000 of this coverage. That often falls short when codes require a total rebuild after 50%-75% damage or require upgrades such as hurricane-resistant windows in North Carolina wind-borne debris regions, as explained in this North Carolina ordinance or law coverage overview.

That default limit is not a safety net. In many serious losses, it’s a trap.

The three parts you need to understand

Insurers bury this coverage in policy language and endorsements because confusion helps them. The easiest way to understand it is to break it into the three working parts.

| Coverage part | What it pays for | Why it matters in a dispute |

|---|---|---|

| Coverage A | Loss to the undamaged portion | If the law requires tearing down part of the structure that wasn’t physically damaged, this is the section that should respond |

| Coverage B | Demolition cost | Pays for tearing down the undamaged portion that must be removed because code requires it |

| Coverage C | Increased cost of construction | Pays the added cost to rebuild to current code rather than old standards |

Coverage A is where many fights begin

A homeowner sees a partial fire loss and assumes the claim is about the burned rooms. The building department may see something very different. If the law requires the whole structure to come down, the undamaged section has value, and your policy may need to pay for that lost value under Coverage A.

That is where carriers start narrowing the claim. They say the undamaged area wasn’t “damaged.” You answer that the covered loss triggered a legal requirement that destroyed its usable value.

Coverage B covers the mess nobody wants to pay for

Demolition costs add up fast. Contractors don’t tear down structurally connected portions of a house for free, and debris doesn’t disappear by itself. If the jurisdiction requires removal of the undamaged section, demolition becomes part of the covered rebuilding problem, not a side issue.

Coverage C is often the biggest money fight

This is the part that pays for bringing the structure into compliance with today’s rules. That can include storm-related code requirements, structural upgrades, safety systems, and other mandatory items the original build didn’t have.

The rebuild doesn’t stop at “replace what burned.” It stops when the building department signs off.

That’s the point many homeowners miss because insurers encourage them to miss it. Standard property coverage often responds to direct physical damage. Ordinance or law coverage responds to the extra cost created by code enforcement after that covered loss.

If your carrier is talking only about materials and labor to replace what was visibly damaged, but not the legal requirements attached to the permit, you’re probably looking at an underpaid claim.

Why Your Standard Policy Is a Financial Trap

Most homeowners don’t intentionally buy weak building ordinance or law coverage. They inherit it. It comes baked into the policy with a limit that looks fine until a serious loss exposes how thin it really is.

The trap springs when local code gets involved

Local building codes in North Carolina and Virginia frequently require a full rebuild when damage exceeds a 50%-75% threshold, which activates ordinance or law coverage. That is especially serious for older homes that don’t meet modern requirements such as deeper footers or impact-resistant glass in coastal North Carolina under NCGS § 143-138. Standard policies in NC and VA often default to 10% ordinance or law coverage, while Florida requires a 25% minimum, as discussed in this analysis of replacement cost and ordinance coverage limits.

The insurance company knows this. That is why I call it a financial trap.

A partial loss can become a total money problem

You think you have a half-house claim. The town tells you that you now have a whole-house code problem. The carrier still tries to adjust it like a half-house loss.

That gap is where families get crushed. The insurer wants to pay for damaged roofing, damaged framing, and damaged finishes. The jurisdiction may require a much broader rebuild that touches structural components, safety items, and undamaged areas connected to the repair.

If your home is older, the risk is worse. Older properties were built under different rules. Once a major loss opens the walls, roof, or systems, current code can reach deeper into the project than most owners expect.

Contractors see this problem every day

A solid contractor can tell you quickly when the insurer’s estimate won’t survive permit review. If you’re dealing with fire damage, it helps to compare the carrier’s scope against a contractor familiar with Fire Restoration work, because code issues and hidden damage often show up together. The permit set and the insurance estimate need to match reality, not the carrier’s preferred version of it.

Why carriers like low default limits

They don’t need to deny every ordinance-related cost to win. They only need to delay, narrow, and confuse long enough that you accept less than the full code-compliant rebuild requires.

Watch for these warning signs:

- The estimate ignores permit comments: If the building department is asking for items not listed by the carrier, the claim is behind.

- The adjuster talks only about direct physical damage: That usually means they are avoiding the ordinance side of the loss.

- You hear “upgrade” used as a dirty word: If the law requires it, it isn’t an elective remodel.

- The carrier never discusses sublimits or endorsements: That often means there is coverage language they don’t want examined too closely.

If your insurer is pricing a patch job and your municipality is demanding a legal rebuild, your problem isn’t contractor cost inflation. Your problem is claim under-scoping.

Real-World Battles Over Code Upgrades in NC and VA

The fights over building ordinance or law coverage don’t stay in the policy. They show up on real jobs, with real inspectors, and with homeowners who thought the hard part was surviving the damage.

A fire claim that turns into a whole-house dispute

A Raleigh-area homeowner suffers a kitchen fire. The carrier pays for cabinets, drywall, insulation, and part of the electrical work tied directly to the burned area. At first glance, that seems normal.

Then the local inspector reviews the permit scope. Once the damaged area is opened and repair work begins, older wiring in connected portions of the house becomes part of the compliance problem. The insurer’s response is predictable. They call the added work pre-existing, unrelated, or maintenance.

That position is convenient for them and brutal for the homeowner. The fire is what started the repair. The repair is what triggered inspection. The inspection is what triggered code enforcement. That chain matters.

A detailed code-based presentation makes the difference. The homeowner’s side has to separate what is elective from what the municipality requires for approval. If you need a practical overview of how these disputes develop, this guide on code upgrade coverage in property claims is worth reviewing before you answer the insurer in writing.

A coastal storm loss with hidden ordinance costs

Now take a Wilmington-area storm claim. The roof is heavily damaged, water gets in, and the carrier focuses on replacing roofing materials and interior finishes. That is only the opening round.

Coastal jurisdictions can require work tied to wind resistance, openings protection, and flood-related construction rules depending on the location and the scope of repair. The homeowner hears, “We paid for the roof.” The contractor hears, “We can’t close this permit without addressing code.”

Those are two very different conversations. One is about what the insurer wants to buy. The other is about what the law requires to rebuild.

The key issue is causation, not convenience

Carriers love arguing that the undamaged or previously noncompliant parts of the home are not their responsibility. Homeowners need to push the essential question back onto the table. Did the covered loss trigger the legal requirement that created the added expense?

That is the heart of the dispute in both fire and hurricane claims. Not whether the home was old. Not whether the owner would have upgraded eventually. The issue is whether the covered event set off the code compliance obligation.

When the loss triggers enforcement, the ordinance issue belongs inside the claim, not outside it.

The strongest disputes are built around documents, not outrage. Permit comments, red-tag notices, code citations, contractor narratives, engineer opinions, and a line-by-line estimate tied to required work all help lock the causation chain in place.

Fight an Insurer’s Tricks to Deny Your Claim

Insurance companies don’t improvise these disputes. They use a routine playbook. Once you recognize the tactics, you can stop reacting to them and start dismantling them.

The partial loss trap

Insurers exploit the Partial Loss Trap by refusing to pay for demolishing the undamaged portion of a property even when code triggered by a covered loss requires it. They define the covered loss narrowly and try to confine payment to the visibly damaged section. This is a major dispute point in NC and VA claims, especially when wind damage to one area triggers broader flood-mitigation or structural code requirements for the whole property, as discussed in this Property Insurance Coverage Law review of ordinance disputes.

That argument sounds technical, but it is really a money-saving move. If the carrier can isolate the loss to one area, it can avoid Coverage A and Coverage B issues tied to the undamaged portion.

Your counter is simple. The legal requirement to remove or upgrade the rest of the structure did not appear out of nowhere. The covered event triggered it.

The coverage limit mismatch

Another favorite move is letting you discover the shortfall late. The carrier knows your ordinance or law sublimit may not be enough, but it won’t volunteer that fact in a way that helps you. Instead, it acts as if the sublimit ends the conversation.

It doesn’t always end the dispute. First, the insurer still has to identify the correct coverage parts and apply them properly. Second, it has to evaluate whether every code-driven item was placed in the right bucket. Third, it cannot label required work as optional to reduce what counts toward coverage.

The fake remodel argument

This tactic shows up constantly. The adjuster says, “We’re not paying to improve your property.” That statement is misleading when the work is mandatory.

Use this distinction:

- Elective improvement: You choose it for appearance, convenience, or preference.

- Required code work: The municipality requires it before approving the rebuild.

- Loss-triggered compliance work: The covered damage and resulting repair brought the property into a code enforcement situation.

Those are not the same thing, and carriers blend them on purpose.

If your property was hit by wind or storm conditions, it helps to compare your loss scope against practical guidance on storm damage insurance coverage so you can spot where the carrier has omitted structural or code-related items that contractors and inspectors will not ignore.

What to gather before you argue

Do not send angry emails without documents. Build the file.

- Get the permit comments: These often show exactly what the jurisdiction requires.

- Request written code citations: Verbal statements from an inspector help, but written references help more.

- Demand the carrier’s full estimate and policy basis: You need to see not just what they omitted, but why they claim they omitted it.

- Create an itemized code-upgrade list: Break out each required item instead of sending one lump number.

- Protect the formal claim record: If the carrier demands a sworn statement, understand what it means before signing. This explanation of a sworn statement in proof of loss is useful when the insurer starts pushing paperwork fast.

Don’t let the insurance company define your rebuild as a cosmetic repair when the permit requires a legal reconstruction.

The language you should stop accepting

When an adjuster says “not covered,” ask which policy section they are relying on. When they say “pre-existing,” ask whether the loss triggered the code enforcement now being imposed. When they say “that falls under maintenance,” ask whether the municipality will approve the repair without it.

Force specifics. Vague denials help carriers. Precise questions help policyholders.

How a Public Adjuster Wins the Building Code Fight

A public adjuster changes the fight because the claim stops being a homeowner’s complaint and starts becoming a documented coverage position.

Homeowners usually come into this issue feeling cornered. The insurer speaks policy language. The building department speaks code language. The contractor speaks construction language. You are expected to translate all three while living through a property loss.

A good public adjuster does that translation and then converts it into an advantage.

What the adjuster for the policyholder actually does

For ordinance disputes, the work is very specific. The public adjuster audits the policy for sublimits, endorsements, and hidden restrictions. Then the adjuster builds a scope that separates direct damage from demolition obligations, undamaged-portion issues, and increased-cost-of-construction items.

In the commercial setting, the structure of the coverage becomes even clearer. For a $10 million commercial building with 50% damage, if code requires full demolition, Building Ordinance Coverage A pays for the undamaged half, Coverage B pays for demolition, and Coverage C pays for upgrades. Public adjusters secure these amounts by auditing sublimits that are often only 10-25%, documenting code violations through certified inspections, and pressing carriers to address upgrades that can cost 20-30% more than original construction, as outlined in this commercial ordinance coverage breakdown.

That same method applies to homeowners, even though the numbers are smaller. The dispute is still about classification, causation, and documentation.

A review that captures the difference

One client review shown above highlights what homeowners usually value most after a hard claim battle. Clear communication, persistence, and someone who doesn’t work for the insurance company. That matters because the carrier’s adjuster is there to protect the carrier’s interests, not yours.

If you want a plain-English overview of the role itself, this explanation of what a public adjuster does lays out the mechanics.

Here is a quick look at how the work changes the claim:

| Real Client, Real Results | What changed in the claim |

|---|---|

| Policy review | Hidden sublimits and ordinance wording get identified before the carrier controls the narrative |

| Code documentation | Required items are tied to written code or permit demands, not loose contractor opinions |

| Scope expansion | The claim grows from visible damage only to the full legally required rebuild scope |

| Negotiation pressure | The insurer has to answer detailed support instead of broad objections |

| Homeowner burden | Fewer direct fights with the carrier while the documentation process becomes organized |

There is also value in seeing the claims process discussed visually, especially if you are dealing with a carrier that keeps moving the goalposts.

One option for policyholders in NC and VA

For homeowners and business owners in North Carolina and Virginia, For The Public Adjusters, Inc. is one available option for reviewing the policy, documenting code-related damage, and negotiating directly with the carrier on property claims. The key is not the brand name. The key is having someone on your side who knows how to force ordinance or law issues into the claim file in a way the insurer can’t casually brush off.

The best time to bring in help is before you accept the carrier’s narrow scope as the final version of your loss.

Take Control of Your Claim Today

If your property loss involves building code issues, you cannot afford to treat them like side notes. They drive permit approval, demolition, reconstruction, and final cost. If the insurer leaves them out, the claim is not complete.

Start with the declarations page. Find the ordinance or law wording and the limit. If it looks small, missing, or unclear, stop assuming the carrier’s estimate tells the whole story.

Then do three things:

- Get the building department requirements in writing. Verbal comments disappear. Written requirements don’t.

- Do not relinquish your advantage too early. Final payments, releases, and rushed paperwork often help the insurer more than they help you.

- Get an independent review of scope and coverage. You need someone to compare the carrier’s estimate against the actual code-compliant rebuild.

This is not a paperwork technicality. It is often the difference between a legal rebuild and a project that stalls halfway because the insurer never paid for what the municipality requires.

If the insurance company is acting like ordinance or law issues are your private problem, push back. They are claim issues when a covered loss triggers them.

2. How do I interpret "Coverage A, B, C, and D" in my NC or VA policy to see if I have "Ordinance or Law" Coverage?

In standard HO-3 homeowners policies (the most common in North Carolina and Virginia), these are the core property coverages listed on your declarations page:

- Coverage A (Dwelling): Covers the main structure of your home (roof, walls, attached garage) against covered perils. This is the primary limit, based on your home's rebuild cost.

- Coverage B (Other Structures): Protects detached items like sheds, fences, or guest houses—typically 10% of Coverage A.

- Coverage C (Personal Property): Insures your belongings (furniture, clothes, electronics)—usually 50-70% of Coverage A.

- Coverage D (Loss of Use / Additional Living Expenses): Reimburses extra costs (hotel, meals) if a covered loss makes your home uninhabitable—often 20-30% of Coverage A, with no fixed time limit in most policies (lasts during reasonable repairs).

- Ordinance or Law coverage (also called Building Ordinance or Law) is not assigned a standard letter like Coverage A through F.

- In most HO-3 policies (common in North Carolina and Virginia), basic Ordinance or Law is often included as an additional coverage (typically 10% of Coverage A) and may appear on the declarations page as a separate line item, such as "Ordinance or Law" with its limit (e.g., percentage or dollar amount of Dwelling coverage).

- If increased (via endorsement), it shows explicitly on the declarations page under endorsements or additional coverages—not as Coverage E (which is Personal Liability).

Check your declarations page for a line labeled "Ordinance or Law," "Increased Ordinance or Law," or under "Additional Amounts of Insurance." Not listed? It may be minimal/basic—ask your agent to confirm or add more.

3. What is the "50% Rule" (Substantial Damage) in North Carolina and Virginia?

In many jurisdictions across NC and VA (especially in floodplains like the Outer Banks or Virginia Beach), if a structure is damaged by 50% or more of its market value, it is deemed "Substantially Damaged." Under local ordinances, a substantially damaged building cannot be repaired as-is; it must be brought into full compliance with current codes, which often includes elevating the entire structure. Without Ordinance or Law Coverage, your insurer may only pay for the repair cost, leaving you with a six-figure bill for elevation.

4. How do I handle an adjuster who says my code upgrade is a "voluntary improvement"?

The "Determination Letter" is your strongest weapon. Many adjusters will claim a code upgrade is optional. To solve this, contact your local building official (e.g., the Charlotte-Mecklenburg Building Development or the Richmond Building Inspector) and request a formal Code Determination Letter. If the official states in writing that a specific upgrade (like hard-wired smoke detectors or specific wind-rated windows in NC) is a mandatory requirement for a permit, the insurance company generally cannot deny the claim as "voluntary."

5. Does Ordinance or Law cover ADA compliance for commercial properties in Virginia?

Yes, but only if the loss triggers the requirement. Under the Virginia Uniform Statewide Building Code (USBC) and the ADA, certain repairs to "Primary Function" areas trigger a requirement to spend up to 20% of the repair cost on "Path of Travel" accessibility upgrades (ramps, wider doors). A sophisticated Public Adjuster will ensure that these statutory costs are included in your claim, even if the insurance company’s estimate completely ignores them.

6. Why is my claim being denied because the upgrade wasn't "Incurred" yet?

Insurance companies often use the "Incurred" clause as a stalling tactic, stating they won't pay until you have already paid the contractor. However, in both NC and VA, courts and the Department of Insurance (NCDOI) generally recognize that if a legal obligation to comply exists (via a permit requirement), the cost is "incurred." The Solution: Secure a signed contract with the code-compliant scope clearly line-itemed to prove the future expense is a legal certainty.

7. Does Ordinance or Law Coverage apply to "Grandfathered" features?

Grandfathered status is revoked the moment you suffer a major loss. Many older homes in historic districts like Old Town Alexandria or Winston-Salem are "out of code" but legal because they haven't been touched. Once a fire or storm occurs, the "Grandfathering" ends. Ordinance or Law Coverage is the only mechanism that pays to bridge the gap between your 1950s wiring and the 2023 National Electrical Code requirements currently enforced.

8. What are the common "Coastal Triggers" for Ordinance or Law Coverage in NC and VA?

If you own property on the coast, two specific codes frequently trigger these claims:

Wind-Borne Debris Regions (NCGS § 143-138): Certain areas in NC require impact-resistant glass or storm shutters.

Freeboard Requirements: Local ordinances in VA Beach or Norfolk often require building heights to be 1–3 feet above the base flood elevation. Ordinance or Law Coverage is what pays for that extra elevation height.

9. Can I use Ordinance or Law coverage to move to a different location?

Generally, no. Coverage for "Increased Cost of Construction" is usually limited to the existing location. However, if local ordinances (such as new setback laws) make it legally impossible to rebuild on your current lot, Coverage A (Undamaged Portion) and Additional Debris Removal (Demolition) can help provide the cash value needed to transition to a new site, subject to your policy limits.

10. How does the "Matching" law in NC/VA affect Ordinance or Law claims?

This is a high-level dispute area. In North Carolina, insurers are often required to provide a "reasonably uniform appearance." If a building code requires you to replace a damaged electrical panel with a larger one, and that new panel requires a different type of exterior meter box that doesn't "match" your siding, your Ordinance or Law coverage can be leveraged to pay for the resulting siding changes required by the code-mandated electrical move.

If your homeowner or commercial property claim in North Carolina or Virginia has been delayed, underpaid, or boxed into a low-ball scope that ignores code upgrades, contact For The Public Adjusters, Inc. for a no-cost review of your policy and claim. A second opinion can show whether the carrier left out demolition costs, undamaged-portion value, or increased construction costs you may be owed.