A sworn statement in proof of loss isn't just another piece of paperwork. It’s a formal, legally binding document your insurance company demands when they want you to declare—under oath—the final dollar amount of your property damage claim.

Receiving one is a major escalation and a sign of a claim dispute. It’s the moment your claim stops being a simple back-and-forth and the entire burden of proof gets shifted squarely onto your shoulders. It is a clear signal that your insurance company is preparing to low-ball or deny your claim.

Your Insurer Demanded a Sworn Statement. What Now?

When a letter from State Farm, Allstate, or any other carrier arrives demanding a Sworn Statement in Proof of Loss, you need to understand what's really happening. This is a clear signal they’re digging in their heels and getting ready to fight your claim.

This isn't standard operating procedure for every claim. It's a calculated move they make when they want to dispute what you're owed, search for reasons to deny you, or lock you into a low number before you even know the full extent of the damage. They are not on your side and are actively working to protect their profits.

Simply put, the insurance company is drawing a line in the sand. They're taking your claim out of the customer service department and moving it into a formal, legal arena where they hold all the power.

Your insurer is handing you a document designed to challenge your claim's validity. They are counting on the fact that most homeowners will make mistakes under pressure—mistakes that can cost them thousands and give the insurer a legal reason to deny the claim.

A Critical Legal Document, Not Just More Paperwork

That first phone call you made to report damage? This is nothing like that. The Sworn Statement in Proof of Loss carries the full weight of a legal affidavit. You are literally swearing, under penalty of perjury, that every single detail and dollar figure is 100% accurate.

Any mistake, forgotten item, or accidental inconsistency can be used against you as evidence of "misrepresentation." At worst, they'll call it fraud. Either way, it gives the insurer a powerful, built-in excuse to deny your entire claim. Understanding when this form might appear in something like the roof insurance claims process helps put its seriousness into perspective.

Your policy spells out your duties after a loss, and submitting this form is a big one. They will almost always give you a strict deadline, usually 60 days, to fill it out and send it back. Miss that date, and you've handed them one of the easiest, most legally sound ways to deny your claim on a technicality.

Proof of Loss vs. Initial Claim

It’s easy to get confused, but it’s critical to understand the difference between your first call to the insurance company and this high-stakes document.

| Aspect | Initial Claim Report | Sworn Statement in Proof of Loss |

|---|---|---|

| Legal Status | An informal notice to the insurer. | A formal, legally binding document signed under oath. |

| Purpose | To start the claim process and get an adjuster assigned. | To officially declare the total, itemized value of your loss for a claim dispute. |

| Level of Detail | A general description of the damage you can see. | A precise, line-item accounting of all damages and costs. |

| Consequence of Error | Usually correctable during the adjustment process. | Can lead to claim denial, accusations of fraud, or a lowball settlement. |

Because this document is so serious, you have to get it right the first time. There are no do-overs. You can learn more about navigating these complexities in our detailed guide on the Proof of Loss.

How Insurers Use Proof of Loss to Undervalue Your Claim

Let's be clear: your insurance company is a business. Its primary goal is protecting its bottom line, which often means paying you as little as possible. The sworn statement in proof of loss is one of the oldest and most effective tools they have to shortchange you.

When a carrier like Nationwide or USAA sends you this form, it’s not a friendly request for information. It’s a strategic move. They are making a calculated bet that you’re stressed, inexperienced with the claims process, and likely to make mistakes that will cost you thousands.

Exploiting Your Lack of Expertise

Insurance companies know you aren’t a contractor, an engineer, or a restoration expert. They demand a sworn statement because they’re banking on you to submit a claim value based only on the obvious damage, missing the expensive, hidden problems.

Once you sign that document under oath, they treat it like it's set in stone. Later, when your contractor discovers extensive mold inside a wall or hidden structural damage the adjuster conveniently overlooked, the insurer will just point to your own sworn statement. They'll say, "Too bad. You already swore this was the full amount of the loss." This is a classic low-ball tactic.

The Deadline Trap

This document is also a favorite delay tactic that they weaponize to create grounds for a flat-out denial. Your policy almost certainly has a strict deadline for returning the form, often just 60 days from when they request it.

This tight timeline is intentional. The insurance company is hoping for one of two outcomes, both of which benefit them:

- You miss the deadline completely, giving them an easy, technical reason to deny your entire claim.

- You rush to meet the deadline and submit a sloppy, incomplete document they can use against you.

It's a high-pressure trap, forcing you to choose between a rushed, flawed submission and a potential denial for being late.

Turning Your Words Against You

Every single number and statement you put on that proof of loss form will be put under a microscope. The carrier's adjusters are trained to hunt for any inconsistency, no matter how small, between the form and anything else you’ve said or submitted.

Did you accidentally list the wrong "cause of loss"? Forget a specific item? Miscalculate the depreciation on your damaged property? They will pounce on these mistakes to build a case for "misrepresentation," using your own words as an excuse to delay, underpay, or deny your claim.

This isn’t about an honest search for the facts; it’s about finding an excuse. The form becomes a tool of intimidation, designed to make you feel overwhelmed and pressure you into taking whatever lowball offer they slide across the table just to make it all stop. It's a calculated strategy to protect their profits at your expense.

Deconstructing the Sworn Statement in Proof of Loss Form

Think of the Sworn Statement in Proof of Loss as a weapon your insurance company hands you, daring you to use it. It looks official, even helpful, but it's loaded with legal jargon and carefully placed traps. They know that one wrong word, one accidental misstatement, is all they need to justify a denial or a ridiculously low offer.

Let's pull this document apart, line by line. I’ll show you exactly where the traps are and what the insurance company’s confusing language really means for your money.

Cause and Origin of the Loss

This one looks simple. It’s not. It’s a trick question. When they ask for the “cause of loss,” they’re baiting you into using a term that isn’t covered by your specific policy.

Here’s a classic example: You have water pouring into your living room from a burst pipe, so you write down “water damage.” But your policy might have an exclusion for general “water damage” from slow leaks, while specifically covering damage from a “sudden and accidental discharge from a plumbing system.” An adjuster from a company like Allstate will seize that opportunity. By using the "wrong" words, you’ve just handed them a perfectly legal reason to deny your claim.

You are not a forensic engineer, but the insurance company is demanding you—under oath—state the exact cause. It’s a setup from the start.

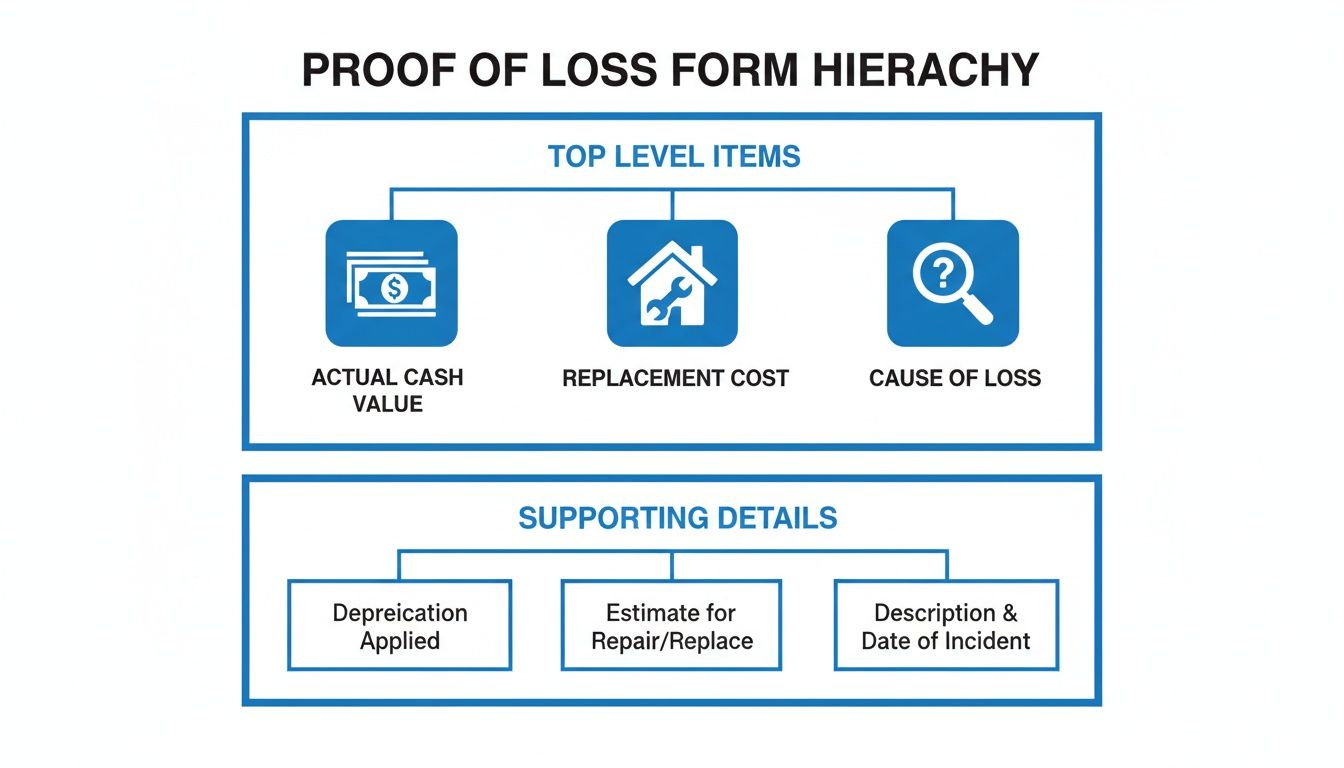

Actual Cash Value vs. Replacement Cost Value

This is where homeowners lose thousands, and it’s where insurance companies make a killing. Getting these two numbers right is absolutely critical, but your adjuster will do everything they can to confuse you.

Actual Cash Value (ACV): This is what your property is worth today, factoring in all the wear and tear (depreciation). Insurers push this number hard because it’s always lower. They’ll tell you your 10-year-old roof is only worth 25% of what it costs to replace, drastically cutting your initial check.

Replacement Cost Value (RCV): This is the real-world cost to actually repair or replace what was damaged, using new materials of similar quality. This is the number you need to be made whole again.

The form demands you list both. What happens all too often? The adjuster gives the homeowner their low-balled ACV number, the homeowner writes it down on the form, and they just unknowingly forfeit their right to recover the full replacement cost.

Statement of Interest

Who else has a financial stake in your property? For just about everyone, this means your mortgage company. It seems like a minor detail, but forgetting to list your lender can bring your entire claim to a dead stop.

If you have a mortgage, your insurance company won't—and can’t—issue a final settlement check without your bank’s name on it. Getting this wrong creates massive delays. And who benefits from delays? The insurance company, of course. They know that the more time that passes, the more desperate you become to accept whatever they’re offering.

Don’t be fooled. The Sworn Statement in Proof of Loss isn’t just a form; it’s a legal minefield. Every single line, from your policy number to the total amount you’re claiming, is another chance for them to find an inconsistency and cry misrepresentation. They will cross-reference every word with every email and phone call you’ve had. This isn’t a document you should fill out alone. Having an expert public adjuster prepare it isn’t a luxury—it’s the only way to protect yourself.

Costly Mistakes Homeowners Make on the Proof of Loss

Signing a flawed sworn statement in proof of loss isn't just a simple error—it can be a multi-thousand-dollar catastrophe. Let's be blunt: insurance companies are banking on you, under immense stress, to make critical mistakes on this document. These aren't just forgiven slip-ups; they are weaponized to justify a lowball settlement or deny your claim entirely.

Understanding the common pitfalls is your first step in fighting back. In this process, your insurer is not your friend, and every single line on that form is a potential trap.

Rushing to Submit Before a Full Assessment

This is the single most devastating mistake you can make. Your insurer puts a strict deadline on the form, usually 60 days, to create a sense of panic and pressure you into acting fast. Why? Because they know the full extent of your damages—like hidden structural issues, slow-leaking pipes behind a wall, or mold that hasn't bloomed yet—often takes time to surface.

Once you swear that your loss totals a specific amount, the insurance company will fight tooth and nail to hold you to that number, no matter what you discover later. Submitting a figure before a professional has done a complete, forensic investigation is like handing the insurer a winning lottery ticket.

Guessing at Costs Instead of Proving Them

Your insurance adjuster might casually suggest, "Just put down a number you think is fair." This is a classic, deliberate trap. A guess is not evidence. A number pulled out of thin air holds zero weight when it comes to a claim dispute.

Your sworn statement must be the final conclusion of a meticulous process, not the starting point. It has to be backed up by a mountain of evidence:

- Detailed Contractor Estimates: This means line-item scopes of work from reputable, licensed contractors, not a simple one-page quote.

- Expert Reports: You may need documentation from engineers, industrial hygienists, or other specialists to prove the full scope of the damage.

- Contents Inventory: A comprehensive, itemized list of every single damaged personal or business item, complete with documented values.

Without this proof, your number is just an opinion. And your insurer will be more than happy to counter it with their adjuster's much lower, self-serving "opinion."

This shows how everything is connected. To build a strong Proof of Loss, you need precise calculations for both the depreciated value (ACV) and the full repair cost (RCV), all tied directly to the specific cause of your loss.

Forgetting Secondary and Indirect Costs

After a disaster, it's easy to focus only on the obvious repairs—the ruined roof, the soaked drywall, the warped flooring. But in doing so, homeowners routinely leave thousands of dollars on the table by forgetting to include other covered expenses. Your insurer isn't going to point these out for you.

Here are some commonly forgotten costs that are a legitimate part of your claim:

- Debris removal and site cleanup

- Code upgrade requirements mandated by your city or county

- Temporary rent and living expenses (Additional Living Expenses or ALE)

- Damage to landscaping, fences, or outdoor structures

- Business interruption losses (for commercial policies)

These costs add up quickly and must be included in the final amount you swear to on the Proof of Loss form.

Contradicting Earlier Statements

From your very first phone call, the insurance company is building a file on you. They record calls and document every email and conversation. When they get your sworn statement, one of the first things they do is cross-reference it with everything you've said before, hunting for contradictions.

Did you tell the first adjuster the leak started on Tuesday, but the form says Monday? Did you forget to mention a pre-existing crack in the foundation that you discussed on a recorded call? They will seize on any inconsistency, no matter how small, to accuse you of misrepresentation—a serious charge that can put your entire claim in jeopardy.

This is often part of a larger strategy to corner you, which can escalate to a demand for an Examination Under Oath to lock you into your story under penalty of perjury. A public adjuster’s job is to ensure your claim has one unified, consistent, and accurate narrative from day one, closing the door on these traps before they’re even set.

How a Public Adjuster Wins the Proof of Loss Battle

Make no mistake: when your insurance company demands a sworn statement in proof of loss, they are escalating the claim into a full-blown fight. This isn’t a routine request. It’s a signal that they are digging in their heels, and it's the exact moment you need to bring in an expert of your own.

Hiring a public adjuster doesn't just level the playing field. It flips the entire game in your favor. We don't just fill out their form; we build an undeniable, evidence-backed case for every penny you're owed. This isn't about arguing—it's about presenting a conclusion so solid they can't possibly refute it.

We Find What They "Missed"

The insurance company's adjuster works for them. Their inspection is often a quick, surface-level walkthrough designed to find the cheapest way to close your claim. A public adjuster does the exact opposite. We launch a deep, forensic investigation of your property damage, using advanced tools to uncover everything their adjuster conveniently missed or deliberately ignored.

Our boots-on-the-ground investigation includes:

- Thermal Imaging Cameras: To expose hidden moisture trapped behind walls, under floors, and in ceilings—the kind that leads to devastating mold and rot.

- Moisture Meters: To get scientific proof of water saturation in building materials, replacing the carrier’s guesswork with hard data.

- Specialized Experts: When the damage is complex, we bring in structural engineers or industrial hygienists to document foundation issues, structural failures, or toxic contamination.

This isn’t just a walkthrough. It's a meticulous, top-to-bottom investigation to document the true scope of your loss.

A public adjuster’s job is to turn your claim from your word against theirs into a battle of facts. When we present your claim, it’s not based on opinion; it’s built on science, data, and irrefutable proof.

We Build an Ironclad Estimate in Their Language

After we’ve documented every last bit of damage, we build a professional, multi-page repair estimate. We don't use guesses or simple quotes. We construct our estimates using Xactimate—the very same software the major insurance carriers use to calculate their own claim values.

This is a critical strategic move. By speaking their language and using their own tool, we shut down their ability to argue over pricing, methods, or materials. We deliver a line-by-line breakdown of every single task and component needed to restore your property to its pre-loss condition. Our estimate isn't just a number; it's a complete repair protocol they can't dispute.

We Deliver a Conclusion, Not a Request

The sworn statement in proof of loss we prepare for you is the final punch. It’s a conclusion, not a guess. This one-page legal document is backed by a mountain of evidence, often hundreds of pages long, including:

- Comprehensive photo and video documentation

- Detailed expert reports and moisture maps

- The complete, line-itemized Xactimate estimate

- An exhaustive inventory of all damaged personal or business property

When the insurance company gets our package, they aren't looking at a form filled out by a stressed-out homeowner. They are facing a bulletproof claim assembled by an industry expert who knows their playbook inside and out. A skilled public adjuster often focuses on settling civil disputes out of court, forcing a fair resolution without the need for a long, drawn-out lawsuit.

This approach changes the entire dynamic. It forces the insurer to confront the documented reality of your loss, stripping them of the excuses they use to underpay or deny claims. You can learn more about the specific tactics we use to beat the insurance companies by reading our guide on what a public adjuster does.

Common Questions (And Traps) About Proof of Loss Forms

Getting a letter from your insurance company demanding a sworn statement in proof of loss sends most people into a panic. Suddenly, you’re staring at a legal document with a ticking clock, and it feels like your entire claim hangs in the balance. It does.

Let's cut through the noise and tackle the most common questions—and the insurance company traps that come with them.

What Happens If I Miss the 60-Day Deadline?

Missing the deadline is fatal to your claim. Period. Your policy is a contract, and if it says you have 60 days to submit the proof of loss, the insurance company will deny your entire claim on day 61 without a second thought.

They see a missed deadline as a clean, easy way out of paying what they owe. It’s a simple technicality they will absolutely use to protect their bottom line.

This isn't a soft deadline you can just ignore. But don't rush and submit a half-baked, inaccurate form just to meet it. If you're running out of time, call a public adjuster immediately. We can often file a formal notice of representation and request an extension, protecting your claim while we do the work to get the numbers right.

Can I Change My Proof of Loss After I Submit It?

Technically, maybe. Realistically, it’s a terrible idea and incredibly risky. You signed the document under oath, so any attempt to change it will be met with intense suspicion.

The carrier's first thought will be insurance fraud. Their second will be that you're trying to pull a fast one. They will grill you on why your story or your numbers suddenly changed, and they’ll use your original, lower-valued statement to lock you into that smaller amount. While you might be able to correct a simple typo, trying to increase the claim value after the fact almost always ends in disaster. This is exactly why it has to be done right the first time.

The Adjuster Told Me to "Just Put a Number Down." Should I?

Absolutely not. You are being walked into a trap. The insurance company's adjuster is not your friend or your advisor—they are a trained negotiator working to save their employer money.

When they casually tell you to "just write something down," they are trying to trick you into signing a legal document that commits you to a low, completely unsupported number. Once you sign it, they will hold that document up as your own sworn testimony to justify their lowball payment. It doesn't matter what your contractor discovers later. They will simply point to the number you swore to and close the file.

Never, ever use a number suggested by the insurance company's adjuster. The only number that should go on your proof of loss is one that comes from a detailed, independent investigation by an expert fighting for you.

Is a Proof of Loss for a Flood Claim Different?

Yes, and it’s a minefield. A claim with the National Flood Insurance Program (NFIP) isn't like a standard homeowners claim. It’s governed by rigid, unforgiving federal law, making the sworn statement in proof of loss one of the most dangerous documents you can sign.

The adjusters sent by FEMA or their "Write Your Own" (WYO) carriers are notorious for enforcing these rules without mercy and making the claim dispute process incredibly difficult.

- Zero Flexibility: The format is strict. Any deviation, no matter how small, can get your claim tossed out.

- Brutal Deadlines: Extensions are almost never granted. If you miss the deadline, your claim is dead on arrival.

- Bureaucratic Nightmare: Fighting a denial involves a complex and frustrating appeals process that is heavily stacked against the policyholder.

If you have an NFIP flood claim and they’ve demanded a proof of loss, you are in a high-stakes emergency. You need immediate help from a public adjuster with direct experience fighting the NFIP. Do not try to face this alone.

Navigating a sworn statement in proof of loss is stressful, especially when it feels like your insurer is setting you up to fail. Don't let them bully you into a lowball settlement. The team at For The Public Adjusters, Inc. knows these tactics inside and out. We take control, build your claim on solid evidence, and fight to get you the full and fair settlement you’re owed.

If you’ve received a proof of loss demand, contact us today for a free consultation and let’s talk about how to fight back.