A pipe bursts under the sink. The dishwasher line lets go while you’re at work. Water runs behind cabinets, under flooring, into baseboards, and maybe into rooms that still look “fine” to the naked eye. Then the insurance company sends someone out, takes a quick look, writes a number, and acts like the matter is straightforward.

It usually isn’t.

If you’re reading this, you’re probably already dealing with the second disaster. Not the water. The claim. The low estimate. The missing line items. The vague explanation. The feeling that the carrier’s adjuster saw far less damage than your contractor did. That instinct is often right. A water damage public adjuster exists for exactly this fight.

Table of Contents

- Why Your Insurance Company Is Not Your Friend

- Whose Adjuster Are They Really? Insurer vs Public

- How a Public Adjuster Takes Control of Your Claim

- Building an Unbeatable Water Damage Claim File

- Fighting Back on Flood Claims in North Carolina and Virginia

- Real Stories of Policyholders Who Fought Back and Won

- Take the First Step to Winning Your Claim Dispute

Why Your Insurance Company Is Not Your Friend

Most homeowners still believe the insurance company will “take care of it” if the damage is obvious enough. That belief causes a lot of underpaid water claims.

Water losses are too common and too expensive for carriers to treat casually. Industry reporting says water damage is the second most common home insurance claim, behind wind and hail, with an average payout of about $11,605. The same reporting says water damage and freezing made up nearly 28% of all home insurance claims from 2018 to 2022, with average severity of $13,954 per claim according to this water damage insurance claim summary.

That matters for one reason. When a claim category is frequent and costly, insurers scrutinize it hard. They question scope. They narrow causation. They separate “sudden damage” from “long-term seepage.” They approve what’s easy to see and push back on what takes work to prove.

What the conflict looks like in real life

A homeowner sees soaked flooring, swollen cabinets, stained drywall, and a musty odor. The carrier’s estimate may only include the most visible area. That’s how underpayment starts.

Common tactics include:

- Fast inspections: A brief walk-through can miss water migration into adjacent rooms and hidden assemblies.

- Tight scope writing: If it isn’t documented, they may leave it out.

- Mitigation pushback: Emergency dry-out costs often get questioned unless the paper trail is clean.

- Delay pressure: The longer the process drags, the more likely a homeowner accepts less just to move on.

Practical rule: If the insurance company controls the inspection, the scope, and the narrative, they control the number.

You don’t need to be cynical to see the problem. You just need to understand incentives. Their adjuster’s job is to close claims for the insurer. Your job is to prove the full loss. Those are not the same thing.

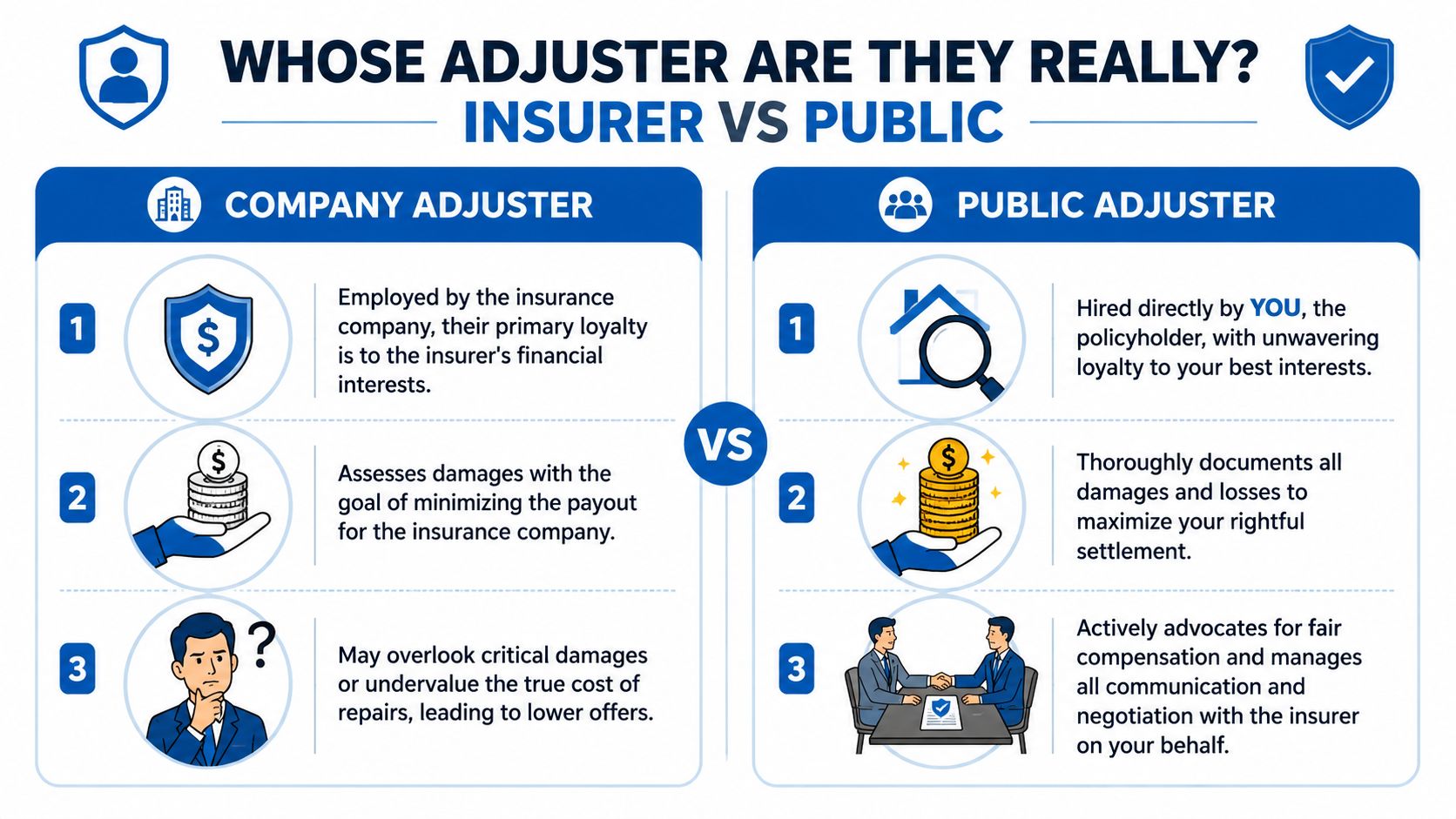

Whose Adjuster Are They Really? Insurer vs Public

The insurance industry loves confusion. “Company adjuster.” “Independent adjuster.” “Desk adjuster.” “Field adjuster.” The names sound official, and that’s the point. What matters is simpler. Who hired them, and whose interests do they serve?

The adjuster title game

A company adjuster works directly for the carrier. An independent adjuster sounds neutral, but usually isn’t. They’re typically hired by the insurance company to inspect and report on the insurance company’s behalf. A public adjuster works for the policyholder.

That difference changes everything.

If you want a fuller breakdown, read this guide on insurance adjuster vs public adjuster. The short version is this: the insurer’s side is evaluating your loss through a cost-control lens. A public adjuster evaluates it through a documentation and coverage lens.

Adjuster allegiance showdown

| Attribute | The Insurer’s Adjuster | Your Public Adjuster (For The Public Adjusters, Inc.) |

|---|---|---|

| Who pays them | The insurance company | You, the policyholder |

| Primary role | Evaluate the claim for the carrier | Advocate for the insured |

| Scope approach | Often limited to what is quickly observable | Builds the full scope, including concealed damage when supported |

| Communication style | Requests information from you | Handles communication for you |

| Negotiation position | Protects carrier interests | Pushes for full and fair payment |

| Loyalty | To the insurer that assigned the claim | To the policyholder who hired them |

Here’s the blunt truth. Friendly doesn’t mean neutral. Many homeowners mistake politeness for alignment. That mistake gets expensive.

The person sent by the carrier may be courteous, responsive, and professional. They still do not represent you.

A water damage public adjuster doesn’t just “help with paperwork.” That description is far too soft. A good one audits the carrier’s scope, challenges omissions, documents hidden damage, ties repairs back to the policy, and negotiates from evidence instead of frustration.

If your insurer’s estimate feels thin, it probably is. If your contractor says there’s more damage than the carrier allowed, that gap needs proof. If the carrier keeps asking for more information while refusing to revise the number, you’re already in a dispute whether they admit it or not.

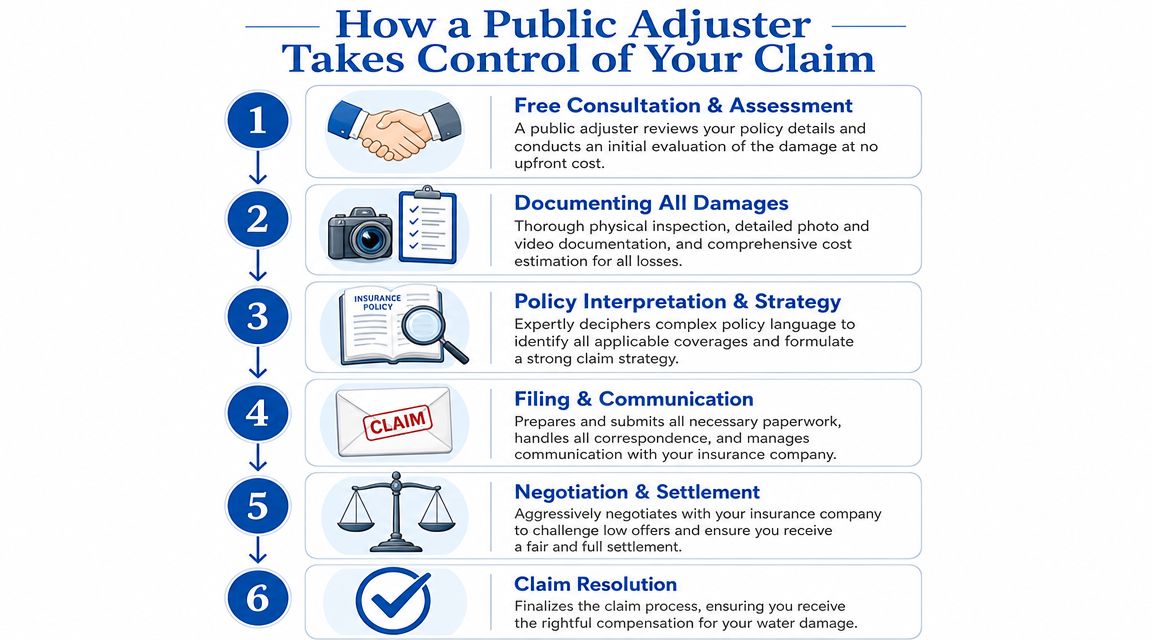

How a Public Adjuster Takes Control of Your Claim

Most homeowners call for help after they’re exhausted. The carrier is asking for more documents. The mitigation company wants payment. The contractor sees more damage than the insurer approved. Nobody seems to be talking the same language.

That’s when a water damage public adjuster becomes useful. Not as a spectator. As the person who takes control of the claim file.

What control actually looks like

First, the claim gets reviewed from the ground up. Not just the visible damage, and not just the insurer’s estimate. The policy language matters. Cause of loss matters. Exclusions matter. Endorsements matter. If you want a baseline for that role, this overview of what a public adjuster does is a good place to start.

Then comes the inspection. A proper water claim inspection is not a quick walk-through with a flashlight and a notepad. It means checking where water traveled, what materials were affected, what can be dried, what has lost integrity, and what must be removed to access trapped moisture or complete repairs correctly.

A seasoned adjuster will usually focus on things homeowners get punished for missing:

-

Point of origin

What failed, where it failed, and whether evidence of that failure was preserved. -

Path of migration

Water doesn’t stay where it lands. It moves under flooring, behind trim, into wall cavities, and sometimes into rooms that don’t show dramatic staining. -

Mitigation documentation

Emergency extraction, dehumidification, and dry-out costs need support, not guesses.

Here’s a useful walkthrough if you want to see the claim process in action:

Why this changes the outcome

The insurance company often works from an estimate-first mindset. A public adjuster works from an evidence-first mindset. That sounds like a subtle distinction. It isn’t.

An estimate-first approach asks, “What can we justify paying?” An evidence-first approach asks, “What was damaged, what does the policy cover, and what will proper repair require?” That’s how weak files become stronger files.

A good public adjuster also absorbs the administrative burden. That means carrier emails, document demands, estimate revisions, reinspection scheduling, and back-and-forth with contractors or mitigation vendors. You stop trying to decode claim jargon after work and start getting represented by someone who speaks it every day.

Building an Unbeatable Water Damage Claim File

Low-ball water claims usually don’t happen because the damage is minor. They happen because the file is weak.

A ceiling stain gets photographed, but the wet insulation above it doesn’t. The warped floor gets listed, but the moisture under the subfloor doesn’t. Cabinets are noted, but the baseplates behind the wall are never checked. That’s how insurers under-scope a claim without ever saying the words out loud.

Visible damage is not the whole loss

In a water loss, the defensible scope comes from diagnostics, not guesswork. Industry practice uses thermal imaging to identify temperature anomalies, but those findings need confirmation with direct-contact moisture meters and, when needed, invasive inspection, because infrared alone can produce false positives. That’s why a strong claim file pairs room-by-room photos with moisture maps, meter readings, and contractor notes to prove the full extent of damage, as explained in this discussion of documenting hidden water damage in a claim.

That technical work matters because hidden water can migrate beyond the visibly affected room. If the file proves moisture in subflooring, wall cavities, insulation, or structural components, the estimate changes. If the file doesn’t prove it, the carrier often leaves it out.

If your claim only shows what a phone camera can see, don’t be surprised when the insurer only pays for what a phone camera can see.

Some losses also involve drainage or line issues that need separate confirmation. When that question comes up, homeowners should understand CCTV drainage inspections because a pipe condition report can help clarify where the problem started and whether additional areas may have been affected.

The documents that carry a dispute

A strong water claim file usually includes several layers of proof, not one dramatic photo.

- Scene records: Timestamped photos before demolition, including affected finishes, contents, and transition areas.

- Moisture evidence: Meter readings, moisture maps, and notes identifying wet materials beyond the obvious damage.

- Mitigation support: Drying logs, extraction invoices, equipment records, and emergency service receipts.

- Repair rationale: Contractor notes explaining why removal, access, or replacement is necessary.

- Formal claim presentation: A detailed statement that ties damages, costs, and supporting records together. This guide to a proof of loss helps explain why that document can become a turning point in a dispute.

Insurers don’t pay because damage feels unfair. They pay when the file forces them to deal with evidence.

Fighting Back on Flood Claims in North Carolina and Virginia

A lot of homeowners say “flood” when they really mean water damage from a pipe break, appliance leak, or roof opening. Insurance companies know the difference, and you need to know it too.

Water claim or flood claim

Standard homeowners policies typically treat internal water events and rising surface water as different claim categories. A burst supply line under the sink is one thing. Water entering from rising ground water or storm surge is another.

That distinction can decide whether you’re dealing with a standard property carrier or a flood claim under the National Flood Insurance Program, often handled through a Write Your Own company. Once you’re in that federal flood world, the rules get tighter, the paperwork gets more rigid, and casual documentation won’t cut it.

Why NFIP disputes are tougher

NFIP claims can be frustrating because they’re highly procedural. The carrier or WYO administrator may focus heavily on documentation, line-item support, causation, and strict compliance with flood-claim requirements. Homeowners often assume they can handle the dispute the same way they would a normal homeowners water claim. That assumption causes problems.

In North Carolina and Virginia, this matters after coastal storms, heavy rain events, and overflow situations where the source of water becomes the central issue. If the damage came from rising surface water, the fight is not about a normal homeowners water loss. It is about flood coverage, federal rules, and a very different claim path.

When there’s confusion about whether the damage falls under homeowners coverage or NFIP coverage, get clarity fast. Don’t let the wrong category control the claim. And don’t let a carrier blur the distinction to limit what gets paid.

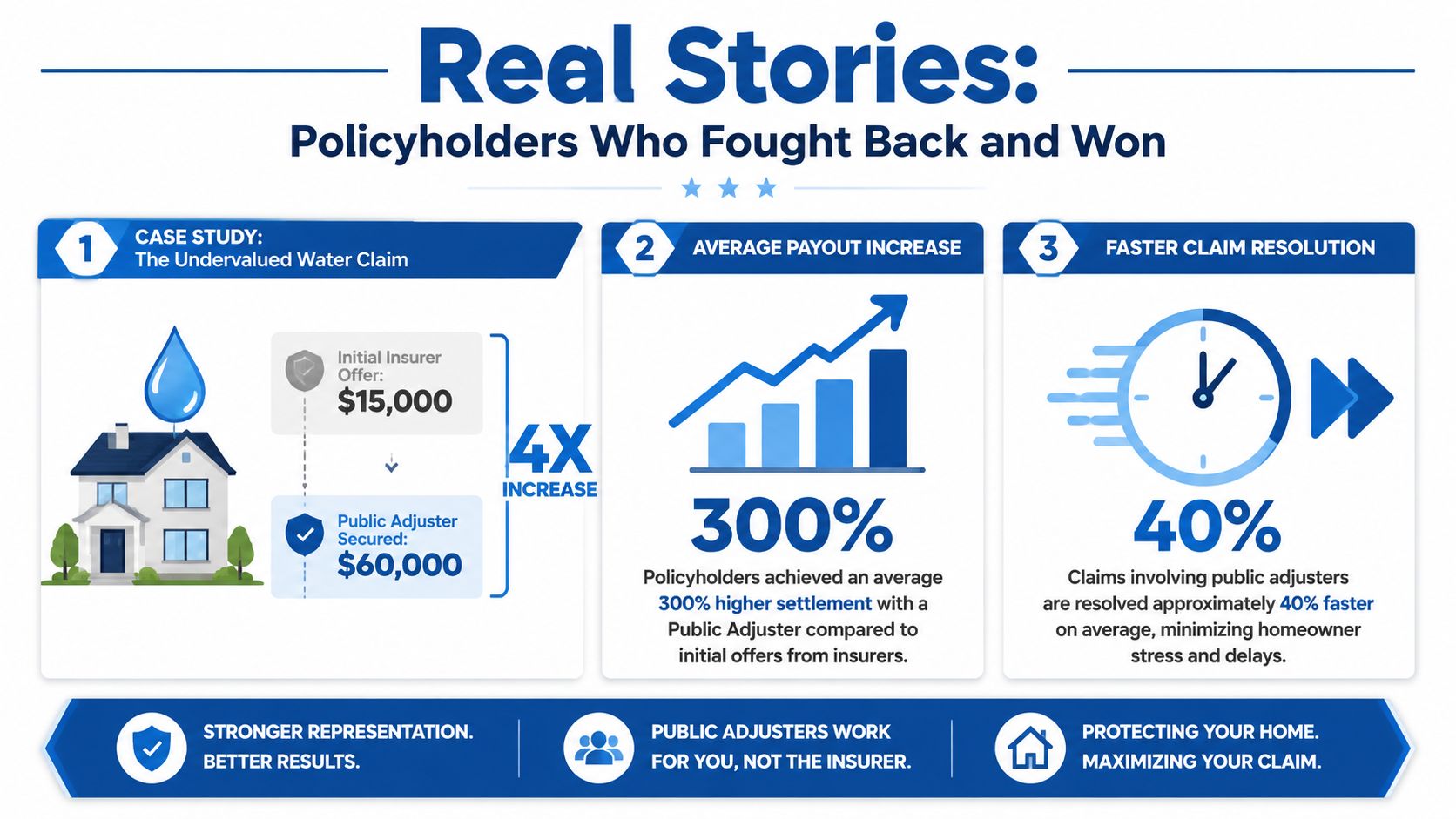

Real Stories of Policyholders Who Fought Back and Won

People want proof. Fair enough. But there’s a problem in this industry. A lot of firms publish flashy “success stories” loaded with big numbers, dramatic before-and-after claims, and vague references to lawsuits. Much of it is marketing first and evidence second.

That’s why you should be cautious here.

What winning usually looks like

A real water damage dispute often looks less cinematic and more technical. A homeowner gets an estimate that only covers the visibly damaged area. Their contractor finds wet materials outside that area. The carrier resists because the original inspection didn’t document it. The dispute turns on evidence, not outrage.

Then someone does the work properly. Moisture readings get taken. Hidden damage gets mapped. Mitigation records are organized. Contractor notes explain why access and replacement are necessary. The carrier reopens the scope or supplements the payment because the file got stronger.

That is what “winning” usually looks like. Not magic. Not slogans. Documentation that corners a weak estimate.

The best claim turnarounds don’t come from arguing louder. They come from proving more.

What to look for in real claim help

Be skeptical of any company that leans on giant payout claims without giving you a defensible reason those amounts changed. Water losses vary wildly based on source, duration, materials, mitigation timing, and policy terms. The number matters less than the method.

Look for these signs instead:

- Technical inspections: They talk about moisture mapping, not just photos.

- Policy analysis: They can explain coverage issues in plain English.

- Clean documentation: They know how to support mitigation invoices and repair scope.

- Negotiation discipline: They answer insurer objections with records, not chest-thumping.

- Actual client feedback: Reviews that mention communication, responsiveness, and claim handling are more useful than hype.

The same goes for legal examples. Carriers do get challenged, and policyholders do fight back, but legal outcomes depend on facts, policy language, and procedure. If someone waves around lawsuits without tying them to your kind of claim, that’s noise.

What you need is not a story that sounds heroic. You need a claim file that makes a low-ball position harder to defend.

North Carolina Water Damage Claim Case Study

A North Carolina homeowner contacted For The Public Adjusters, Inc. after a supply line leak caused water to spread from the kitchen into adjoining living areas. The insurance carrier’s first estimate focused mainly on visible cabinet damage and a small section of flooring near the leak source.

The problem was that the water had traveled farther than the initial inspection recognized. Moisture readings and a more detailed room-by-room review showed affected baseboards, flooring transitions, wall cavities, and materials that required additional access and removal before proper repairs could begin.

The carrier’s original scope left out several important items, including:

- Additional moisture mapping in connected rooms

- Removal and replacement of affected baseboards and trim

- Flooring repairs beyond the visibly wet area

- Cabinet detach and reset work needed for access

- Mitigation documentation tied to drying equipment and emergency labor

- Painting and finish work across continuous surfaces

The dispute was not about whether water damage existed. The dispute was whether the insurance company had acknowledged the full path of the water.

After the claim file was rebuilt with better documentation, photos, moisture evidence, contractor support, and a more complete repair scope, the carrier had to address damage that was missing from the original estimate. The case shows why water damage claims in North Carolina should never rely only on a quick visual inspection.

Customer Review After a Water Damage Claim Dispute

“Our insurance company made the water damage sound simple, but the first estimate did not come close to what our contractor said was needed. We had wet flooring, damaged cabinets, and moisture that moved into areas the adjuster barely looked at.

For The Public Adjusters helped us organize the photos, mitigation records, contractor notes, and missing repair items – lots of them. They explained the process clearly and dealt with the insurance company when we were tired of getting vague answers.

Once the claim was presented properly, the conversation changed. We finally felt like the full damage was being taken seriously instead of being minimized.”

— North Carolina Homeowner After a Water Damage Claim Dispute

Customer experiences like this are common in water damage claims because the most expensive parts of the loss are often the areas the carrier’s first estimate does not fully document.

Take the First Step to Winning Your Claim Dispute

If your insurance company is dragging its feet, under-scoping the damage, or acting like your dry-out and emergency costs are optional, stop waiting for them to “do the right thing.” Establish your position.

Water claims are time-sensitive. High moisture increases mold risk if drying is delayed, and a public adjuster’s role is to document pre-mitigation conditions and preserve receipts for emergency services because those mitigation expenses are typically part of the loss presentation, as explained in this guide on documenting water damage for an insurance claim.

That means your next move matters. Fast documentation helps. Better evidence helps more. If the insurer already has the upper hand in the file, you need someone who knows how to take it back.

Questions people ask right before they call

Can a public adjuster help if the carrier already made an offer?

Yes. In many disputes, the first offer is the beginning of the fight, not the end of it.

What if the claim was denied or partially denied?

That’s often when representation becomes most valuable. A denial letter is not the last word if the facts, scope, or policy interpretation can be challenged.

Is it too late if mitigation already started?

Not necessarily. The key issue is what evidence still exists, what records were kept, and whether the damage can still be documented correctly.

Do I need to keep every invoice and drying record?

Yes. Keep everything. Emergency mitigation costs often become a point of contention, and poor records make that argument harder.

You do not have to accept a shallow inspection, a thin estimate, or a payment that leaves part of the repair bill on your shoulders. A water damage public adjuster can step into the fight, tighten the evidence, and force a more honest conversation about what your claim is worth.

2. What specialized tools do PAs use to document "Hidden" water damage that insurance adjusters often overlook?

Insurance adjusters typically only scope the visible damage. Our expertise is finding the damage that extends deep into the structure, which dramatically increases the claim value. The core technology we rely on is thermal imaging and moisture mapping.

Thermal Imaging (Infrared Cameras): This technology detects temperature differences within walls, ceilings, and floors. Water-damaged areas often have a lower surface temperature due to evaporation, making them appear as distinct color differentials on the thermal image. This proves the extent of moisture migration that is completely invisible to the naked eye.

Moisture Meters: We use non-penetrating and penetrating moisture meters to create a Moisture Map. This map provides objective, quantifiable readings of water saturation levels within building materials (e.g., drywall, wood framing). This documentation is essential for justifying the full scope of necessary drying, demolition, and mold prevention protocols (IICRC S500 standards).

3. How do Public Adjusters maximize coverage when my policy has a $5,000 (or low) mold remediation sub-limit?

Most homeowners policies include a specific sub-limit for mold remediation, often capped at a low amount (e.g., $5,000 or $10,000). A professional approach is essential to avoid using that sub-limit prematurely.

The Allocation Strategy: Mold coverage generally falls into two buckets: a) Mold that resulted from a covered peril (e.g., a burst pipe) and b) Mold that is unrelated to a covered peril (e.g., from long-term humidity). A PA fights to have the costs related to tear-out and replacement of water-damaged materials (like sheetrock and wood) paid for under the standard Dwelling Coverage limit, which is much higher.

Defining Remediation: We argue that the mold sub-limit should only apply to specialized mold treatment and air scrubbing, not the removal and replacement of the structure itself.

Proving Timeframe: We secure reports from industrial hygienists to confirm the mold growth was directly related to the covered, sudden water event, not a long-term issue.

4. Does my homeowner's policy cover the cost to repair the broken pipe or the appliance that caused the water damage?

This is a critical distinction in water claims:

Damage is Covered: Standard homeowners insurance (HO-3) policies are designed to cover the resulting damage to the structure and contents caused by the sudden discharge of water (e.g., the ruined flooring, ceiling, and walls).

Source is Not Covered: Generally, the policy does not cover the cost to repair or replace the failed system itself—the broken pipe, the faulty hot water heater, or the washing machine. This is considered maintenance or wear and tear.

5. Why is my carrier saying my emergency "water mitigation" costs are unreasonably high?

Emergency mitigation (drying, water extraction, debris removal) is typically the first and most expensive step. Carriers frequently challenge these costs, claiming the scope or pricing was excessive.

PA Due Diligence: We establish that the policyholder has a contractual "duty to mitigate" the loss, meaning they must take reasonable steps to prevent further damage (like mold growth). Failure to do so can lead to a full claim denial.

The Xactimate Advantage: We ensure the mitigation contractor's invoices are created using Xactimate, the same standardized estimating software used by insurance carriers. We cross-reference the line-item codes to guarantee industry-standard pricing. If the carrier attempts to unilaterally reduce the hourly rate or drying equipment rentals, we formally dispute it with clear market data.

6. What is the difference between "Clean Water" (Category 1) and "Black Water" (Category 3), and how does it affect my claim value?

Water is categorized based on its source and contamination level (IICRC S500 standard). This categorization dramatically impacts the scope of demolition and the overall claim value.

| Water Category | Contamination Level | PA Claim Impact |

| Category 1 (Clean Water) | Source is clean (e.g., burst pipe, supply line). | Materials may be salvable. Drying and disinfection may be sufficient for non-porous materials. |

| Category 2 (Gray Water) | Some contaminants (e.g., dishwasher overflow, toilet overflow without feces). | Porous materials (carpet pad, drywall) are non-salvable. Requires full removal/disposal and advanced disinfection. |

| Category 3 (Black Water) | Highly contaminated (e.g., sewage backup, floodwater from the ground). | All porous materials must be removed and disposed of. Requires intensive structural decontamination, sometimes called sub-surface decontamination. |

7. If my claim is denied due to "Sump Pump Failure" or "Sewer Backup," can a Public Adjuster get it covered?

Damage caused by water entering the home from outside or below the foundation (e.g., sewer, drain, sump pump failure) is typically excluded from standard HO-3 policies.

The Endorsement Check: The first step is determining if the policyholder purchased a specific Water Backup and Sump Overflow Endorsement. If this endorsement exists, the PA ensures the carrier applies the coverage correctly, even if the limit is subject to a sub-limit (e.g., $10,000).

The "Cause" Dispute: If the water came from a clogged toilet drain within the home (above the main sewer line), we may argue that it was a sudden plumbing system failure covered by the main policy, not an excluded "sewer backup."

8. My insurance company is only offering Actual Cash Value (ACV). How does a PA secure the full Replacement Cost Value (RCV)?

Policies are either written as ACV (Replacement Cost minus Depreciation) or RCV (Full cost to replace the item). Most homeowners policies offer RCV coverage, but the carrier first pays the ACV amount.

The Depreciation Holdback: Carriers withhold the recoverable depreciation (the difference between ACV and RCV) until the policyholder provides proof that the repairs have been completed.

The PA's Role: We submit a finalized, expert-level scope and estimate (using Xactimate) to the carrier that details the true, pre-loss RCV. This ensures the initial ACV payment is maximized. More importantly, we stick with you during during your repair process and the final documentation (contractor invoices, lien waivers) to secure the final depreciation holdback check quickly and efficiently.

9. What is "Bad Faith" in a water damage claim, and what is the Public Adjuster's legal leverage?

Bad Faith occurs when an insurance carrier unreasonably delays, low-balls, or denies a legitimate claim without proper investigation or justification.

PA as the Shield: When a PA is retained, all communication and negotiations are handled by us. This formal representation immediately signals to the carrier that the policyholder is informed and prepared for litigation if necessary.

Leveraging Evidence: The PA's comprehensive claim package (thermal imaging, detailed Xactimate scope, microbial reports) leaves no room for the carrier to argue they lack sufficient information. A denial or low-ball offer against this evidence becomes much harder to defend as being made in "good faith."

10. Can a claim cover the cost of upgrading my plumbing system to prevent future water damage?

Generally, no. Policies do not pay for betterments, preventative maintenance, or upgrades (e.g., replacing old copper pipes with PEX).

Code Compliance Loophole: We check for Ordinance or Law coverage. If the water damage is extensive enough that local building codes now require the entire plumbing system to be brought up to current code during the repair, this coverage may apply, potentially paying for the upgrade of undamaged pipes adjacent to the repair area.

11. How does a PA ensure correct pricing for repairs in a volatile, post-disaster construction market?

Insurance estimates rely on a static pricing database (Xactimate). However, after a major area-wide disaster, costs for labor, materials, and specialized equipment (like dehumidifiers) spike due to high demand.

Surcharges and Market Conditions: A PA does not blindly accept the default Xactimate pricing. We apply justifiable surcharges, such as General Contractor Overhead and Profit (GCOP), and specialized Demand Surcharges to account for the actual, inflated costs contractors face in a busy market.

Non-Standard Materials: If the damaged tile or flooring is discontinued, a PA secures quotes for the closest Like Kind and Quality replacement, even if that replacement is significantly more expensive than the original material, forcing the carrier to indemnify the policyholder properly.

12. My water claim is for a rental property. How can a Public Adjuster secure coverage for lost rent?

If a rental property becomes uninhabitable due to a covered water loss, the policyholder can claim Fair Rental Value (FRV) or Loss of Rents coverage (often called Additional Living Expense - ALE or Loss of Use on a primary residence policy).

PA Documentation: We immediately collect the lease agreement, bank records proving rent payment history, and provide local rental market comparisons for similar properties.

The Uninhabitable Clock: The PA ensures the carrier pays for the lost rent for the full duration it takes to make the property habitable again, including the time required for structural drying, demolition, permitting, and reconstruction. This clock often runs much longer than the carrier initially estimates.

If you’re dealing with a denied, delayed, or low-ball property claim in North Carolina or Virginia, For The Public Adjusters, Inc. offers a no-cost claim review for homeowners and business owners. They represent policyholders, not insurance companies, and help inspect, document, and negotiate water, storm, fire, and flood-related property losses. If your carrier’s estimate doesn’t make sense, this is the time to get a second set of expert eyes on the file.