When your home or business is hit with devastating property damage, the single most important choice you’ll make is between the insurance adjuster vs public adjuster. It’s a decision that will absolutely define the outcome of your claim and your ability to rebuild.

Here’s the hard truth: the insurance company’s adjuster, whether from State Farm, Allstate, or another major carrier, is paid to protect the insurer’s profits. Their primary goal is to minimize what they pay you by using delay tactics, lowball offers, and confusing policy language. A public adjuster is a licensed expert you hire to fight for your best interests and maximize your settlement.

Your First Choice in a Property Claim Fight

The moment a fire, burst pipe, or storm damages your property, you’re thrown into a battle you didn’t ask for. The first call you get will likely be from your insurance company’s adjuster, and it’s critical to understand that this person is not on your side.

Whether they are a direct employee or an independent contractor hired by your insurer, their primary job is to serve the financial interests of the company that signs their checks.

This creates a massive conflict of interest right out of the gate. Insurance giants like State Farm and Allstate have entire systems built to control the narrative of your claim. They send their adjusters to inspect the damage through a lens that favors their bottom line, a practice that almost always leads to undervalued estimates, overlooked damages, and infuriating delays. They’re trained to twist your policy’s language in the company’s favor and pressure you into accepting a quick, lowball offer before you even know the full extent of your loss.

A public adjuster, on the other hand, has one job and one job only: a legal duty to you, the policyholder. You hire them to level the playing field and fight back. They will meticulously document every single detail of your loss, translate the dense policy jargon into plain English, and build an ironclad claim designed to get you the maximum compensation you are rightfully owed.

Understanding the benefits of hiring a public insurance adjuster is the first step toward taking back control.

Who Represents Whom?

The core difference all comes down to allegiance. Who does the adjuster work for? That one fact dictates every action, every recommendation, and every negotiation that follows.

This table breaks down the fundamental divide.

Key Differences Insurance Adjuster vs Public Adjuster

| Attribute | Insurance Company Adjuster | Public Adjuster |

|---|---|---|

| Who They Represent | The insurance company (e.g., State Farm, Allstate) | You, the policyholder |

| Primary Goal | Minimize the insurance company’s payout | Maximize your financial settlement |

| Who Pays Them | The insurance company (salary or fee-based) | You (a small percentage of the settlement) |

| Loyalty & Duty | Owed to the insurance company’s profits | Owed to you and your recovery |

This comparison makes it pretty clear. One is looking out for a corporation, the other is looking out for you.

An ethical insurance adjuster’s job is hard, as they must balance their employer’s interests with a duty to the public trust. However, company culture often pressures them to prioritize profits, leading to underpaid claims.

This fundamental divide is why the “insurance adjuster vs public adjuster” question is so critical. One path leads to protecting a corporation’s assets; the other leads to rebuilding your own.

Whose Side Is Your Adjuster Really On?

When you’re trying to figure out the insurance adjuster vs public adjuster puzzle, it all comes down to one simple, brutal question: Who signs their paycheck?

That single answer dictates every move they make, every suggestion they offer, and every tactic they use while handling your property damage claim. It’s the most critical factor determining whether you get a fair settlement or just a fraction of what your policy actually owes you.

An insurance company adjuster works for one master: the insurance company. It doesn’t matter if they’re a staff employee for a giant like Allstate or an “independent” contractor hired for the job. Their professional loyalty is to the insurer’s bottom line, period.

A Deep-Seated Conflict of Interest

Think about the career path of a company adjuster. It’s built on closing claims and keeping payouts as low as possible. Their bosses reward them for being “efficient,” which in their world, means settling your claim for the least amount of money in the shortest amount of time.

Let’s look at their day-to-day reality:

- Company Training: They are trained by the insurer to interpret your policy in a way that benefits the insurance company, not you.

- Proprietary Software: They use estimating software like Xactimate, which often uses standardized, low-ball pricing that doesn’t reflect the true cost of local labor and materials for your dwelling or business.

- Strict Protocols: They have to follow internal company rules and hit performance goals that are almost always tied to minimizing settlement amounts.

A company adjuster’s career advancement, and even their bonuses, are directly linked to how much money they save their employer. This creates a massive, unavoidable conflict of interest when they’re supposed to be impartially assessing your devastating loss.

A public adjuster plays by a completely different rulebook. They are licensed professionals that you, the policyholder, hire to represent your interests. Their legal and ethical duty is to you and you alone. They are your advocate in the fight, with zero ties to the insurance company that wants to shortchange you.

The Loyalty Gap in the Real World

Picture this: A pipe bursts, and your home suffers major water damage. The insurance company’s adjuster shows up, gives the soggy walls a quick look, and writes up an estimate to dry some drywall and replace a few baseboards. His job is to close this file and move on.

Now, imagine the same disaster, but this time you’ve hired a public adjuster. They don’t just do a visual check. They bring in moisture meters to find the water hiding behind the walls. They check for the beginnings of mold growth. They document the ruined insulation and structural wood that the company adjuster conveniently “overlooked.”

This isn’t just theory. That loyalty gap is the real-world difference between a check that covers a patch-up job and getting the actual funds you need to make your home whole again.

Your decision in the insurance adjuster vs public adjuster debate is a choice between hiring your adversary or hiring your ally.

How Financial Incentives Dictate Your Settlement

If you want to understand the fundamental difference in the insurance adjuster vs public adjuster fight, just follow the money. It’s that simple. How each adjuster gets paid directly shapes their motivation, and that motivation has a massive impact on the final check you get for your damaged property.

The adjuster sent by your insurance company is just an employee. They’re either on a salary or paid a flat fee by the insurer for each homeowner or business owner claim they handle. Their personal income has absolutely no connection to the size of your settlement.

Whether you get a check for $15,000 or $150,000, their paycheck doesn’t change one bit.

This payment model creates a powerful, built-in incentive to close your claim as fast as possible for the lowest amount the insurer can get away with. Their employer rewards them for closing files and saving the company money, not for making sure you’re truly made whole. It’s why they often pressure you to accept a quick, lowball offer—they just want to clear your file off their desk and move on to the next one.

The Power of Aligned Interests

A public adjuster’s financial model couldn’t be more different. We work on a contingency fee, which means we only earn a small, agreed-upon percentage of the final settlement we win for you. If you don’t get paid, we don’t get paid.

This structure creates a genuine partnership. A public adjuster is paid based on a percentage of the final settlement, which usually falls between 5% and 20%. In stark contrast, the insurance company’s adjuster is a salaried employee or a contractor who gets paid a fixed amount, creating a clear incentive to protect the insurer’s profits by minimizing your payout. You can learn more about how these payment structures influence claim outcomes on nwclaimsmanagement.com.

This financial alignment is everything. A public adjuster is motivated to dig deep, find all the hidden damage, and fight for every single dollar your policy owes you. We meticulously build a claim to maximize your payout because our success is tied directly to your success.

The difference in how we get paid exposes the massive conflict of interest baked into the insurance company’s model. Their adjuster serves the corporation’s goal of minimizing costs. The public adjuster is financially driven to secure the maximum possible recovery for you, the policyholder.

Your choice of who handles your claim determines whose financial interests are being protected.

The Real-World Impact on Your Final Payout

Let’s get down to what really matters: the money. The whole debate over an insurance adjuster vs a public adjuster isn’t just some technical argument—it has a direct, measurable impact on the check you get to rebuild your home or business.

This choice is the difference between a settlement that barely slaps a bandage on the problem and one that actually makes you whole again. The proof is in the results. Time and time again, policyholders who hire a public adjuster walk away with substantially larger payouts.

This isn’t by chance. It’s a direct result of who each adjuster works for. The insurance company’s guy often does a quick, surface-level walk-through, looking for the cheapest and fastest way to close your claim. They might gloss over hidden water damage behind a wall, completely ignore smoke contamination in your HVAC system, or use outdated, low-cost pricing for materials and labor.

A public adjuster, on the other hand, works for you. We launch our own exhaustive investigation. We don’t just look at the obvious damage; we dig deep to uncover the full, true extent of your loss.

Building an Undeniable Case for Your Claim

To beat the insurance company’s lowball tactics, a public adjuster builds an ironclad case backed by hard evidence and expert analysis. This flips the power dynamic completely. You stop begging for what you’re owed and start demanding it with proof in hand.

Here’s how a public adjuster can totally change the game for you:

- Expert Network: We bring in our own trusted network of engineers, contractors, and inventory specialists to provide detailed, third-party proof of your damages that the insurer can’t ignore.

- Detailed Documentation: Every last crack, stain, and damaged possession is meticulously documented with photos, videos, and professional, line-item estimates.

- Policy Expertise: We comb through your homeowner or business owner policy to find every single bit of coverage you’re entitled to. This often includes things most people miss, like code upgrade requirements or additional living expenses.

The insurer’s first offer is never their best offer. It’s a calculated opening move in a negotiation, and they are banking on you being too overwhelmed and inexperienced to fight back.

The numbers don’t lie. A landmark study out of Florida found that policyholders who hired public adjusters received settlements that were up to 747% larger than what the insurance company initially offered. Think about that. A lowball $10,000 offer could become a final settlement of nearly $85,000 with a real advocate on your side. You can dig into these powerful public adjuster statistics on forthepublicadjusters.com.

This massive financial impact isn’t just for one type of claim; it’s across the board. A denied roof claim gets turned into a full replacement when we prove the damage was caused by a covered storm. A business interruption claim that the insurer tried to brush off gets renegotiated to reflect the true financial hit you took.

Having a public adjuster in your corner isn’t just a nice-to-have—it’s essential if you want the full and fair settlement you actually deserve.

Navigating the Claims Process With an Advocate

A property damage claim can either be a bureaucratic nightmare or a managed process—and the person guiding you makes all the difference. The choice in the insurance adjuster vs public adjuster debate directly shapes your experience, your stress levels, and whether you can focus on getting your life back.

When you’re left to deal with the insurance company’s adjuster alone, the entire burden of proof falls squarely on your shoulders. Suddenly, you’re expected to be an expert in construction codes, inventory valuation, and complex insurance law. You have to document every nail and wire, argue policy provisions you don’t really understand, and chase the adjuster for updates while they deploy intentional delay tactics.

It’s an exhausting and emotionally draining ordeal. This process is often designed by major insurers to wear you down, hoping you’ll accept a lowball offer out of sheer frustration just to make it stop.

Shifting the Burden to a Professional

Hiring a public adjuster completely flips this dynamic. The entire burden shifts from your shoulders to a dedicated professional who advocates only for you. They become your single point of contact, managing the claim from the first notice of loss to the final check. You can learn more about the specifics of what a public adjuster is and how they fight on your behalf.

This shift lets you stop fighting a battle you were never meant to win and start rebuilding.

Here’s how the two experiences stack up:

The Process With an Insurance Adjuster:

- You are responsible for every phone call, email, and piece of paperwork.

- You must schedule and attend all inspections and meetings by yourself.

- You are pressured to accept their estimates, which are almost always too low.

- You are constantly chasing them for basic updates on your own claim.

The Process With a Public Adjuster:

- They handle 100% of the communication with your insurance company.

- They manage all documents, evidence, and critical deadlines for you.

- They bring in their own team of experts to build an undeniable claim.

- They provide you with regular, straightforward updates, letting you focus on your family or business.

The peace of mind that comes from having a professional advocate manage the endless paperwork, hostile negotiations, and frustrating delays is invaluable. It transforms the claims process from a lonely battle into a managed project with a clear path forward.

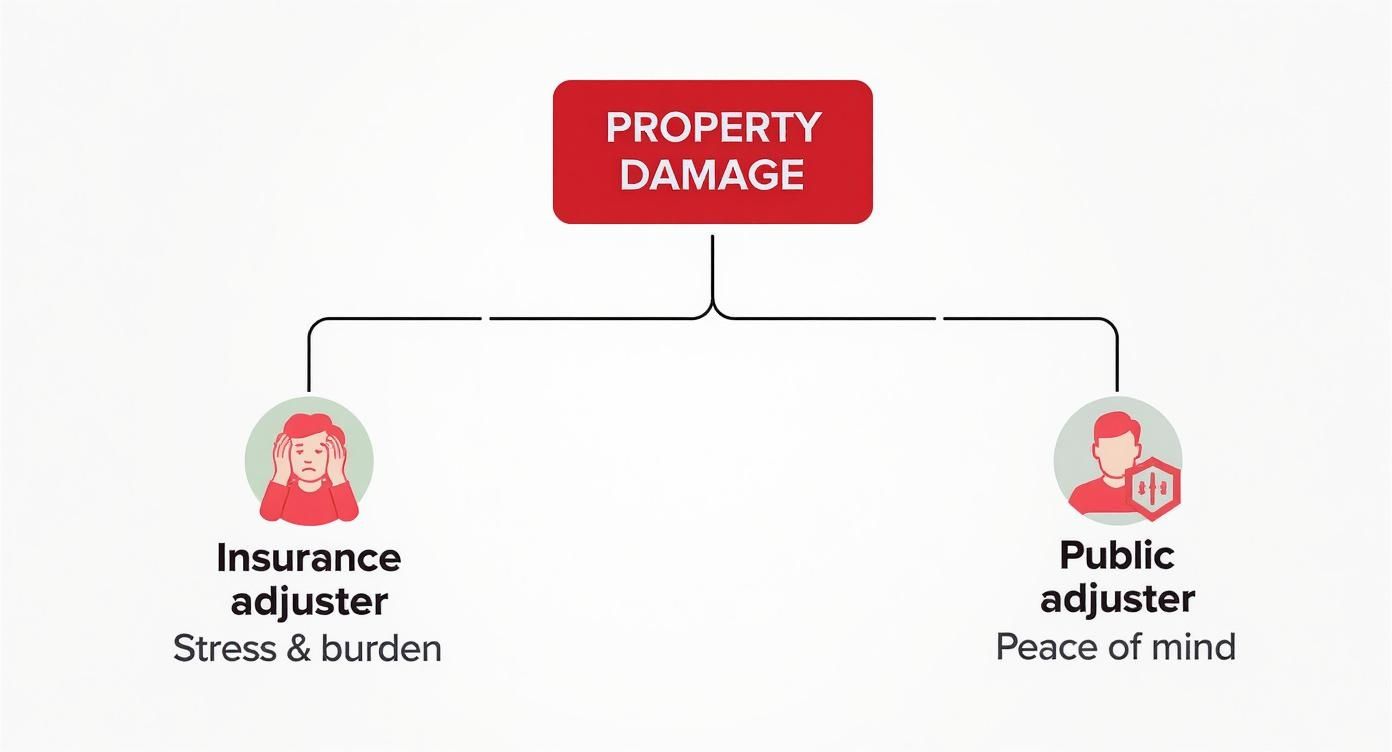

When to Hire a Public Adjuster for Your Claim

While a public adjuster can add value to almost any property damage claim, there are certain high-stakes situations where their expertise becomes absolutely essential. Knowing when to call in a professional can be the difference between a fair, fast recovery and a long, drawn-out battle that leaves you shortchanged.

The key is to recognize the red flags your insurance company might be throwing up and to be honest about the complexity of your own claim.

If your claim is complex, you need an advocate on your side. Think extensive damage from a major fire, widespread water damage from a burst pipe, or significant structural issues after a storm. The more moving parts there are, the more room your insurer has to underpay, delay, or deny parts of your dwelling or business claim.

Recognizing the Warning Signs

Some tactics from insurance companies should be seen as immediate signals that you need help. These moves are designed to control the process and pressure you into accepting less than what you’re truly owed.

- An Immediate Lowball Offer: If the adjuster from Allstate or State Farm shows up and quickly throws out a low settlement number, it’s not a good-faith estimate. It’s a strategic test to see if you’ll take the fast cash without questioning the real cost of your repairs.

- Unreasonable Delays: Constant excuses, blown deadlines, and radio silence are classic delay tactics. Insurance companies know that the longer they drag out the process, the more desperate you’ll get and the more likely you are to just give up and accept whatever they offer.

- Outright Denial of Your Claim: If your claim gets denied with a flimsy or confusing explanation, don’t for a second think that’s the final word. It’s often just a tactic to see if you’ll walk away without putting up a fight.

The decision tree below paints a clear picture of the two very different paths your claim can take, showing the stark contrast in stress and results.

This illustration makes it crystal clear: bringing in a public adjuster is about taking back control and getting some peace of mind during an incredibly stressful time.

When the Stakes Are Highest

For both homeowners and business owners, a large-loss event demands professional representation. We’re talking about situations like a collapsed roof, a major commercial fire, or significant water damage that shuts down your business operations. These are too critical to handle alone.

The financial stakes are massive, and you can bet the insurance company will fight tooth and nail to minimize its payout. In these moments, the insurance adjuster vs public adjuster dynamic becomes a direct conflict over your financial future.

If you feel overwhelmed, confused by your own policy, or just have a gut feeling that your insurer isn’t playing fair, it’s time to hire a public adjuster. Trust that instinct. You’re dealing with an opponent whose primary goal is to protect its own bottom line.

The numbers back this up. A Bankrate analysis found that homeowners who hired a public adjuster received settlements that were, on average, 19.4% higher. The typical settlement with a public adjuster’s help was around $22,266, compared to just $18,659 for those who went it alone—that’s a difference of over $3,600. This data just highlights the real-world value an expert brings to the table, especially when things get complicated.

If you’re still on the fence, our guide on whether you should hire a public adjuster can offer more clarity. Making the call to bring in a professional advocate is the most powerful move you can make to level the playing field and get the settlement you truly deserve.

Frequently Asked Questions

When you’re trying to pick up the pieces after a disaster, the last thing you need is confusion. The insurance adjuster vs public adjuster decision is a big one, so let’s clear up a few common questions.

Can I Hire a Public Adjuster After My Claim Has Been Denied?

Absolutely. That denial letter from your insurance company isn’t the end of the road—far from it. Think of it as their opening move in a negotiation.

Many homeowners and business owners bring in a public adjuster for this exact reason. A good public adjuster can reopen your denied claim, build a powerful case with new evidence, and force the insurance company to look at the facts, not just their bottom line.

Is It Worth Hiring a Public Adjuster for a Small Claim?

It really depends on how you define “small.” For a truly minor and simple dwelling claim where the insurance company’s offer feels right, you might be fine on your own.

But be careful. What looks like a small problem on the surface can often mask much bigger, hidden damage. If your gut tells you the insurer is lowballing you, or if the damage seems more complex than it appears, getting a professional opinion is a smart first step.

Most public adjusters won’t charge you a dime to review your claim. It’s a no-risk way to get an expert’s take on your situation and find out if you’re leaving money on the table.

How Much Does a Public Adjuster Cost?

Public adjusters don’t charge by the hour or ask for money upfront. They work on a contingency fee.

This means they only get paid if you get paid. The fee is a small, pre-agreed percentage of the final settlement they secure for you. This setup is a huge win for policyholders because:

- There are no upfront costs to get an expert on your side.

- They have a powerful financial incentive to maximize your claim payout.

- Their success is tied directly to your success.

This model flips the insurance adjuster vs public adjuster dynamic completely in your favor, ensuring your advocate is fighting for every penny you deserve.

Q2: Whose interests does a Public Adjuster truly represent during the property claim process?

A: A Public Adjuster represents the policyholder's interests only. They level the playing field by preparing, documenting, and negotiating the claim to secure the full and fair settlement amount the policyholder is entitled to.

Q3: What is the goal of the Insurance Company's Adjuster?

A: The goal of the insurance company's adjuster is to assess the damage and determine the lowest reasonable cost to indemnify the company's client (the policyholder) while protecting the insurer's financial bottom line.

Q4: Can a Public Adjuster get me a higher insurance settlement, even after factoring in their fee?

A: Yes. Studies often show that claims handled by Public Adjusters result in significantly higher settlements compared to policyholders who handle the claim themselves, which typically offsets the adjuster's fee and results in a larger net recovery for the policyholder.

Q5: How does a Public Adjuster get paid, and do I pay them upfront?

A: Public Adjusters typically work on a contingency fee basis, charging a small percentage (usually 5%–20%) of the final claim settlement amount. You generally pay nothing upfront; the fee is paid out of the new settlement proceeds.

Q6: When is the best time to hire a Public Adjuster for my property damage claim?

A: The earliest stage possible is best. Hiring a Public Adjuster at the beginning ensures proper documentation and strategy from day one, but they can be hired at any point: when a claim is denied, delayed, or severely underpaid by the insurance company.

Q8: Is an 'Independent Adjuster' the same as a Public Adjuster?

A: No. An 'Independent Adjuster' is a contractor hired and paid by the insurance company to handle claims on their behalf—they still represent the insurer's interests, not yours. A Public Adjuster is hired and paid by the policyholder.

Q9: How does a Public Adjuster handle the complex documentation and policy review?

A: A Public Adjuster handles the entire process: meticulously documenting all damages (including hidden losses), preparing detailed repair estimates (often using the same software as the insurer), and interpreting the policy language to ensure all coverages, including code upgrades and extended coverages, are applied correctly.

Q10: What types of claims do Public Adjusters typically handle?

A: Public Adjusters specialize in property damage claims for both residential and commercial policies, including losses from fire, water, wind, hail, hurricane, mold, collapse, theft, and business interruption.

When you’re in a fight with your insurance company, you can’t afford to go it alone. You need an expert who is 100% in your corner. For The Public Adjusters, Inc. provides licensed, professional advocacy to make sure policyholders in North Carolina and Virginia get the fair settlement they’re owed.

Contact us for a free, no-obligation review of your claim.

https://forthepublicadjusters.com

On July 27 2025 we had a bad rain Strom I had a sewer back up in my basement and destroyed everything so i call the insurance company and file a claim and they came out to see the damages I they send me a check for 12,750 but that only cover the amount for the clean so I call them back to ask for more money and they told me that they going to give me an additional 630.00 dollars more and that’s was my limited so I’m seeking for help if it’s not too late

Antonio, sorry to hear you are having such trouble with your claim. Who is your insurance company? What city and state is your damaged home located? Most states allow you to present new evidence between 1 to 3 years from the date of loss. So, it’s not too late for you to fight it.

Looking for help with sewerback up

A, what city and state is your claim damage in? Also, do you know what type of policy you have… Like HO3 or a DP policy? You can find this on the Declarations Page of your policy. It will say “Policy Forms” and list what type you have.

Insurance company under pay for damages

Hi Antonio, yes. It’s been found that most carriers are trying to only pay approximately 30% of what they owe.

My claim for a cat attack on my wife was refused by my insurance company because she was living with me at the time, but I later found out that my insurance company paid $6,000 dollars to a separate law firm to help deny my wife ANYTHING! This was only a year ago, can a public adjuster help me?

WOW, that sound like a traumatic event. I’m so sorry to hear about this and I hope she is doing okay. I don’t really think a PA could help. More than likely an attorney can though. Find an “insurance claim attorney” that will work on a contingency (no money up front. only paid if they win the case) basis.