When you file a property damage claim, you’re formally asking your insurance company for the money you’re owed to fix your home or business. It’s a right you have as a policyholder. But far too often, it’s the start of a fight you never saw coming, especially when your insurer seems more interested in protecting its bottom line than helping you recover.

Your Guide to Disputing a Property Damage Claim

Getting a denied or lowballed property damage claim is a slap in the face. It’s incredibly frustrating. You’ve paid your premiums on time for years, trusting that your insurance company would have your back. But now that you actually need them, major carriers like Allstate or State Farm can suddenly feel more like an opponent than a partner.

This guide is your playbook for fighting back. We’re going to pull back the curtain on the delay and denial tactics that are all too common in this industry. The goal is to shift your mindset from a passive, frustrated policyholder to an empowered advocate for your own recovery. You absolutely have the power to challenge an unfair settlement, and we’re here to give you the confidence and the strategy to do it.

Understanding the Dispute Process

When your insurer digs in its heels and refuses to pay what you’re rightfully owed, you’ve entered a dispute. This isn’t just a simple disagreement; it’s a formal process where the burden falls on you to prove the full, true extent of your loss and hold your insurance company accountable to the policy you paid for.

Success here comes down to being organized, persistent, and armed with rock-solid evidence. While every claim has its own unique twists and turns, the fundamental stages of a dispute are always the same.

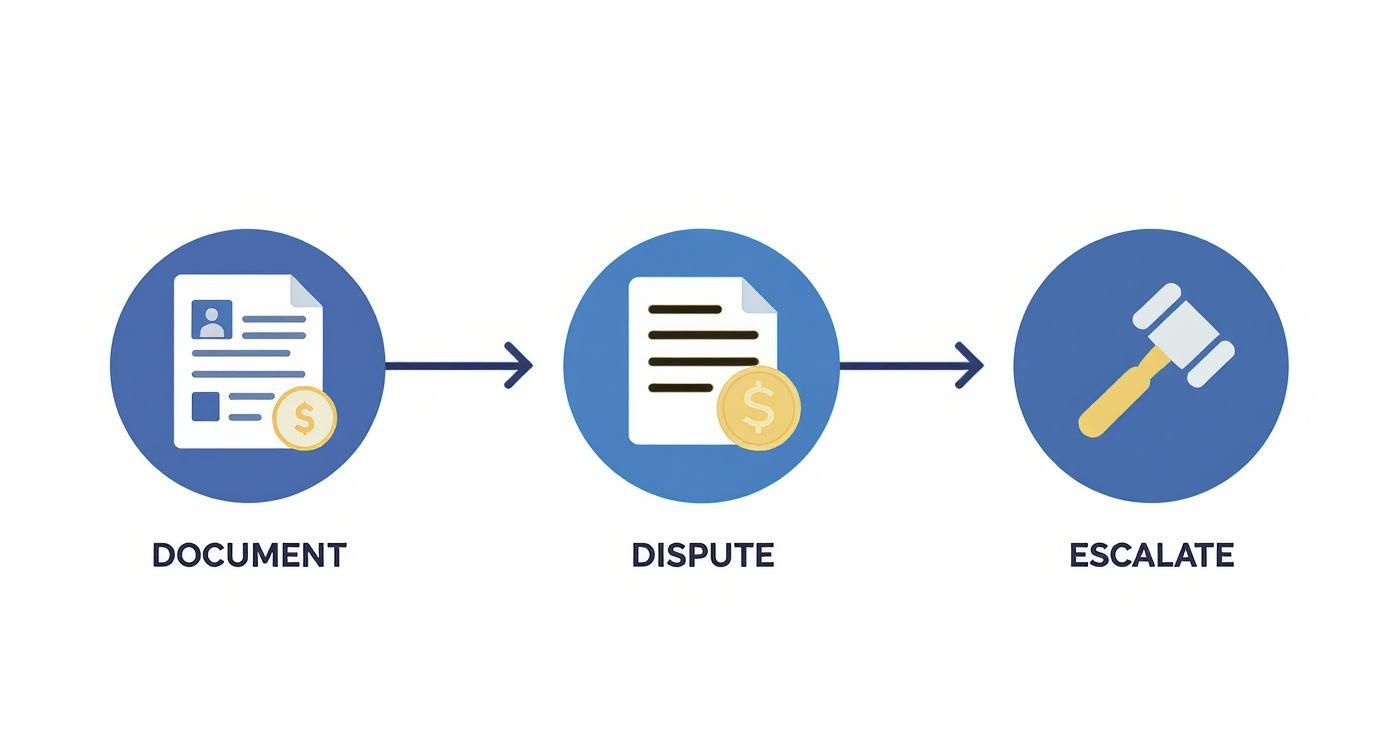

The infographic below breaks down the essential steps for fighting back against an unfair settlement offer.

Think of this as your road map. It shows the journey from gathering your initial proof all the way to formal escalation, highlighting the key moves you need to make to effectively challenge your insurer’s decision.

Why You Must Fight Back

Let’s be blunt: insurance companies are for-profit businesses. Their financial health depends on paying out as little as possible in claims. This isn’t a secret; it’s just business. When a major disaster hits, that pressure intensifies.

For example, recent years have seen global catastrophic losses hit $137 billion, with North America getting hit with nearly 80% of that from events like massive wildfires and brutal storms. The 2025 Los Angeles wildfires alone triggered $30 billion in residential claims, putting immense financial strain on insurance carriers. That pressure almost always trickles down to policyholders like you in the form of aggressive cost-cutting tactics.

When you get that lowball offer, understand it’s not just a starting point for negotiation. It’s a business strategy. Your insurer is making a calculated bet that you’ll be too worn out, too intimidated, or just too uninformed to fight for the full amount you are actually owed.

This guide will walk you through the stages of a dispute, from spotting bad faith tactics to knowing when to bring in expert help. But remember, the fight often begins long before a formal dispute. Properly documenting and presenting your initial claim is your first, best line of defense. For a deep dive on that crucial first step, check out our guide on how to file a property damage claim.

We’ll make sure you have a clear path forward to securing the fair and full settlement you deserve.

Why Your Insurance Company Is Not on Your Side

Here’s a hard truth you need to accept right now: your insurance company is not your friend. It doesn’t matter what the “good neighbor” slogans from State Farm or the “good hands” promises from Allstate say. At the end of the day, an insurer is a business, and its main goal is to make a profit for its shareholders. They are notorious for lowballing and delaying valid claims.

That’s not an opinion—it’s just their business model. You pay them premiums for a safety net. But the moment you file a property damage claim, you flip from being an asset to a liability on their spreadsheet. Every dollar they pay you is a dollar out of their profit column. This immediately puts you and your insurer on opposite sides of the table.

It’s a bit like a casino. The house always has an advantage because it created the game and wrote the rules. The insurance claims process is no different. It’s a system designed by the insurance industry, for the insurance industry. Their adjusters are trained to play by those rules to protect the company’s money.

The Insurer’s Playbook for Paying You Less

To keep their profits healthy, insurance companies have a well-worn playbook of tactics they use to drive down the value of your property damage claim. These moves are sneaky, effective, and designed to take advantage of the fact that you’re stressed, overwhelmed, and just want to get your life back to normal.

A classic move is to push you toward their “preferred” contractors. It sounds like they’re helping you out, but it’s often a trap. These contractors get a steady stream of business from the insurer, so they have a strong incentive to write low estimates that match what the insurance company wants to pay—not what it actually costs to do the job right. They might use second-rate materials or skip crucial steps, leaving you with a shoddy repair.

They’ll also try to dazzle you with official-looking estimates from software like Xactimate. The adjuster will hand you a detailed report and present it as gospel truth.

But that software is only as good as the information someone puts into it. An adjuster can easily fudge the numbers by using old labor rates, wrong material prices, or just “forgetting” to include line items for things like debris removal or painting. The result is a number that looks official but is deceptively low.

They’re banking on you being too intimidated by the professional-looking document to question it.

Twisting Your Policy Against You

Your insurance policy is a dense legal contract, and your carrier knows every loophole and vague phrase inside and out. They are experts at using that complexity to their advantage.

They’ll seize on any ambiguity to limit what they have to pay. For example, they might try to label water damage from a storm as “flood” damage (a common exclusion) or argue that your leaky roof is just from “wear and tear” instead of a covered event like a hailstorm. They live in these gray areas, and it forces you to prove them wrong—which is incredibly difficult if you don’t speak their language. The very “good hands” you thought you were in are the ones holding the rulebook and bending it in their favor.

How to Build an Airtight Case Against Your Insurer

When you get that lowball settlement offer, you need to understand one thing right away: the insurance company’s adjuster isn’t there to make you whole. They work for the insurer, and their job is to protect their employer’s bottom line by minimizing what they pay out.

To fight back, you have to become the chief investigator for your own claim. Your mission is to build a case so overwhelming, so packed with irrefutable proof, that their offer looks completely indefensible. This isn’t about snapping a few photos; it’s about building a mountain of evidence so high your insurer simply can’t ignore it.

Master Your Documentation

The absolute foundation of a strong claim is meticulous, almost obsessive, documentation. Think of every photo, every note, every receipt as another brick in the wall you’re building against their cost-cutting tactics.

Start with your camera, but shoot with a clear strategy. A quick walk-through video isn’t enough.

- Capture Everything: Start with wide shots of every single affected room, from every angle. Then, get in close. Show the detail—the warped floorboards, the soot staining the walls, the individual dents from hail on your siding.

- Document the Source: This is critical. Get clear, well-lit pictures of the burst pipe under the sink, the tree limb that punched through the roof, or the charred outlet where the fire started. This helps shut down any ridiculous argument that the damage was already there.

- Use Good Lighting: Open the blinds, turn on every light. If you’re in a dark space like an attic or crawlspace, use a powerful flashlight. A dark, blurry photo is about as useful as no photo at all.

This level of detail creates a visual story that an adjuster from a company like Allstate or State Farm will find very difficult to argue with.

Create an Unbreakable Timeline

Next, you need to document every single interaction you have with your insurance company. This creates an undeniable timeline that exposes any attempts to delay, mislead, or give you the runaround. Grab a notebook or start a digital log—today.

From the very first call to report the damage, you are taking notes. Log the date, the time, the full name of the person you spoke with, and a summary of the conversation. Save every email in a dedicated folder. This organized record is your best weapon against the “he said, she said” games some adjusters love to play.

If an adjuster gives you a key piece of information over the phone, follow it up immediately with a polite but firm email. Something as simple as, “Hi [Adjuster’s Name], I’m just writing to confirm our phone call today where you stated…” creates a written paper trail they can’t deny later.

Gather Your Own Independent Proof

Never, ever trust the insurance company’s numbers. Their estimate isn’t a fair assessment; it’s an opening offer designed to benefit them. To punch back, you need to bring in your own experts and evidence.

- Get Multiple Contractor Estimates: Call at least two or three trusted, local contractors to write up detailed, line-item estimates for the full scope of repairs. Steer clear of the insurer’s “preferred” vendors—they often have a cozy relationship with the insurance company and an incentive to keep their bids low.

- Create a Detailed Property Inventory: For any claim involving personal or business property, you have to create a list of every single item that was damaged or destroyed. You need the item description, brand, model number if you have it, its age, and what it would cost to buy a new one today. The more detail, the better.

With natural disasters getting more frequent and severe, insurers are under massive pressure to control their losses. A recent report showed that global insured losses from catastrophes hit $80 billion in just the first six months of the year, partly driven by massive wildfires. Explore more data on rising catastrophe losses and their impact on insurance.

When insurers are facing losses that big, you can bet they are going to scrutinize every claim with a microscope. Your independent proof isn’t just a good idea—it’s absolutely essential. The goal is to hand them a complete, evidence-backed package that leaves them no room to wiggle.

Countering Lowball Offers with A Negotiation Playbook

Getting that first settlement offer for your property damage claim can feel like a slap in the face. After everything you’ve been through, the number is insultingly low. It’s a deliberate move by carriers like State Farm and Allstate—a calculated test to see if you have any fight left in you. They’re betting you’re too tired and overwhelmed to push back.

Your job is to prove them wrong.

This isn’t just a friendly chat with the adjuster. Think of it as a business transaction where you have to defend the true cost of your loss. Their adjuster has software, a script, and one primary goal: minimize the payout. You need to come to the table with solid evidence, a firm resolve, and a clear game plan.

Crafting Your Dispute Letter

The first real move is to formally reject their offer with a powerful dispute letter. This isn’t the time for an angry email. It’s a professional, evidence-backed rebuttal that systematically picks apart their lowball estimate. Always send it via certified mail to create a paper trail.

In the letter, state clearly that you reject their settlement amount. Then, go line-by-line through their estimate and challenge the inaccuracies with the evidence you’ve gathered.

- Bring Your Own Estimates: Say something like, “Your estimate for the roof replacement is $8,500. However, I have attached two quotes from licensed local roofers for $14,200 and $15,100, which reflect the actual market cost for labor and materials here.”

- Point Out What They “Forgot”: Call out anything they conveniently left out. For example, “Your assessment fails to account for debris removal, city permit fees, and the specific primer required for the new drywall, all of which are necessary for a proper repair.”

- Use Your Policy Against Them: If you can, quote the exact language from your policy that covers the items they’re undervaluing. This shows them you’ve done your homework and you know your rights.

This letter puts the ball squarely back in their court. It forces them to justify their numbers against your real-world proof and changes the dynamic completely.

Decoding Your Insurer’s Estimate vs Reality

Insurance company estimates often look detailed, but they are designed to minimize costs at every turn. They rarely reflect what it actually takes to get the job done right by a qualified, local contractor.

| Damage Area | Typical Insurer Estimate Approach | Independent Contractor Quote Reality | Why It Matters |

|---|---|---|---|

| Roofing | Uses generic, low-grade material costs and minimal labor hours. | Prices high-quality, code-compliant materials and includes specialized labor. | Cheap materials fail faster. Rushed labor leads to leaks and bigger problems down the road. |

| Drywall | Budgets for simple “patch and paint” jobs, often ignoring water saturation. | Includes full removal of damaged sections, proper drying, and seamless finishing. | Painting over wet drywall traps moisture, leading to dangerous mold growth and structural rot. |

| Flooring | Offers to replace only the visibly damaged boards or squares. | Accounts for matching the entire continuous floor to avoid obvious patchwork. | A mismatched floor is a constant reminder of the damage and tanks your property value. |

| General Labor | Uses outdated, national average labor rates that don’t reflect local demand. | Bills based on current, local market rates for skilled, licensed tradespeople. | You get what you pay for. Lowball labor rates attract unqualified workers who cut corners. |

The gap between their estimate and reality isn’t an accident—it’s their business model. Your job is to close that gap with undeniable proof.

Shutting Down Common Adjuster Objections

During your conversations, the adjuster will pull from a playbook of common objections to get you to back down. If you’re ready for them, you can shut them down confidently and keep the negotiation focused on the facts of your property damage claim.

When an adjuster says, “Our software shows the repair should be cheaper,” they are relying on you not knowing that the software’s output is entirely controlled by their inputs. It’s a tool for justification, not an objective measure of cost.

Here’s how you handle their go-to lines with a calm, fact-based response.

Objection 1: “That looks like pre-existing wear and tear.”

- Your Response: “My documentation, including dated photos from before the storm, clearly shows the roof was in excellent condition. This damage is a direct result of the covered event, as confirmed in my independent contractor’s report.”

Objection 2: “Our software, Xactimate, says this is the going rate.”

- Your Response: “That software’s estimate doesn’t reflect the current local market for labor and materials. I’ve provided three detailed quotes from reputable local contractors that show the actual cost to complete these repairs to pre-loss condition.”

Objection 3: “We don’t cover that much material or labor.”

- Your Response: “According to my policy, you are required to cover the cost to return my property to its condition before the loss. The scope of work detailed by my contractor is what is necessary to do that correctly and up to local building codes.”

Staying professional but firm is everything. This isn’t personal; it’s a business dispute over facts and figures. For a deeper dive into these tactics, check out our guide on how to negotiate with an insurance adjuster. Your ultimate goal is to make it clear that you will not be worn down and you will not accept a penny less than what you’re owed.

When to Hire a Public Adjuster for Your Claim

There are moments in a property damage claim when, no matter how much evidence you’ve gathered or how well you argue your case, the insurance company just won’t budge. They refuse to pay what’s fair, and it’s easy to feel completely outgunned.

This is when you bring in a powerful ally: a public adjuster.

Unlike the company adjuster sent by State Farm or Allstate—who works for and is paid by the insurer—a public adjuster works exclusively for you, the policyholder. Their only duty, both legally and ethically, is to protect your interests and fight for the maximum settlement you’re entitled to.

Strategic Moments to Call for Backup

Look, you don’t need a public adjuster for every small, straightforward claim. But in certain high-stakes situations, bringing one in is a game-changing strategic move that can dramatically alter the outcome of your dispute.

Consider calling in a professional when you’re facing one of these scenarios:

- Large and Complex Claims: If a fire, hurricane, or major flood has caused catastrophic damage, the claim is going to be incredibly complicated. A public adjuster knows exactly how to document every detail, account for hidden damage, and translate the dense, confusing language of your policy.

- An Outright Denial: When an insurer flat-out denies your claim, they’re essentially daring you to fight back. A public adjuster will dissect that denial letter, expose the weak spots in the company’s argument, and build a rock-solid case to get that decision overturned.

- Lack of Time or Expertise: Let’s be honest, managing a major property damage claim is a full-time job. If you’re trying to juggle your actual job, your family, and the stress of recovery, a public adjuster can lift that entire weight off your shoulders. They handle every inspection, every phone call, and every negotiation.

How a Public Adjuster Levels the Playing Field

When you hire a public adjuster, you’re bringing in a pro who speaks the insurer’s language and knows their playbook inside and out. They immediately take control of the entire process, from re-inspecting the damage with a fresh, expert eye to aggressively negotiating a final, fair settlement.

A public adjuster works on a contingency fee basis. This means they get paid a small, agreed-upon percentage of your final settlement. The structure is simple: if you don’t get paid, they don’t get paid. Their only financial motivation is to get you the absolute highest payout possible.

This completely flips the power dynamic. The insurance company can no longer drag its feet or hide behind jargon to wear you down. Now, they have to deal with an expert who is every bit as knowledgeable as their own team—but is fighting for your side. You can learn more about the vital role of a public insurance adjuster in our detailed guide.

With storms and other disasters becoming more severe, the financial stakes are through the roof. Global insured property losses from natural catastrophes recently hit a modeled average of $152 billion a year—a staggering 25% jump from the previous year. You can discover more insights about these rising catastrophe losses on Verisk.com.

Insurers are under immense pressure to control those payouts, which often means getting tougher on policyholders. A public adjuster is your best defense against these industry-wide pressures.

Escalating Your Claim: When Negotiation Fails, It’s Time to Fight Back

So, what happens when you’ve laid out all your proof, argued every point, and the adjuster from a big carrier like State Farm or Allstate just won’t move? It feels like hitting a brick wall. But let me be clear: this is a stall tactic, not the end of the road. When negotiations break down, you have formal, powerful options to escalate your property damage claim.

It’s time to stop playing their game of delays and lowball offers. This is where you force the issue using the very mechanisms built into your policy and the legal system.

The Appraisal Clause: Your Policy’s Secret Weapon

Buried in the dense legal language of most insurance policies is a tool most policyholders don’t even know exists: the appraisal clause. This isn’t a lawsuit. Think of it as a binding arbitration process designed for one specific thing: settling disagreements over the cost of the damage. It doesn’t debate if the damage is covered, only how much it will take to fix it right.

Here’s how it works. You hire an independent, expert appraiser, and your insurance company hires one. Those two experts then agree on a neutral third-party expert, known as an umpire. Your appraiser and their appraiser present their cases, and if they can’t agree on a final number, the umpire breaks the tie. When any two of those three agree on the amount, that decision is binding. The insurance company has to pay.

This process yanks the decision-making power away from the stubborn company adjuster and puts it in the hands of impartial professionals. In many cases, it’s the quickest and most effective way to break a stalemate and force the insurer to pay what your claim is truly worth.

Knowing When You Need to Lawyer Up

Appraisal is a fantastic tool for disputes over price, but some fights go beyond dollars and cents. If your insurer isn’t just lowballing you but is actively acting in bad faith, it’s time to call an attorney. Bad faith isn’t just a low offer; it’s a pattern of dishonest, unethical, or deceptive behavior designed to cheat you out of a legitimate claim.

You should seriously consider hiring an attorney if your insurer is:

- Telling outright lies: The adjuster insists something isn’t covered, but a plain reading of your policy shows it is.

- Refusing to investigate properly: They deny the claim without even bothering to conduct a fair and thorough investigation into the facts.

- Creating unreasonable delays: They drag their feet for months with no good reason, just hoping you’ll get frustrated and give up.

- Using threats or intimidation: The adjuster hints that your policy might be canceled if you don’t accept their pathetic offer.

These aren’t negotiation tactics—they’re potentially illegal actions. An experienced insurance attorney can go after the company not just for the money you’re owed on the original claim, but for additional damages caused by their malicious behavior.

Frequently Asked Questions About Property Damage Claims

Going toe-to-toe with your insurance company over a property damage claim is exhausting, and it’s completely normal to have questions about what they can and can’t legally do. Let’s cut through the noise and get you some straight answers to the worries we hear about most.

Will My Insurer Cancel My Policy If I Dispute My Claim?

This is one of the biggest fears homeowners have, but you can put it to rest. It is illegal for an insurance company to cancel your policy just because you filed a claim or had the nerve to question their lowball offer.

That kind of retaliation is a classic example of bad faith. While they can choose not to renew your policy for other legitimate reasons down the road, they absolutely cannot drop you for fighting for the fair settlement you’re entitled to. You have every right to dispute their math, so focus on building a rock-solid case.

How Long Does The Insurance Company Have to Settle?

Most states have “prompt payment” laws on the books, which sound great in theory. They require insurers to handle claims in a “reasonable” amount of time. The problem? Big carriers like Allstate and State Farm are masters at exploiting how vague the word “reasonable” is. They drag their feet, hoping you’ll get so frustrated you just take whatever they’re offering.

Don’t just sit there and wait. If your claim is stalling, it’s time to take action. Send a formal, written demand for a status update via certified mail. In that letter, make sure you reference your state’s fair claims practices act. This does two things: it shows them you mean business and it creates an official paper trail you can use if you need to file a formal complaint later.

Can I Start Repairs Before The Claim Is Settled?

Hold off on any major work. The only repairs you should make are temporary, emergency fixes meant to stop the damage from getting worse. Think tarping a hole in your roof to keep the rain out or boarding up a shattered window to secure your property.

Do not, under any circumstances, start permanent repairs until you and your insurer have a final, signed settlement agreement. If you start rebuilding, the insurance company can argue that you accepted their lowball offer. Worse, you’ll be destroying the very evidence a public adjuster needs to inspect to prove the full scope of your property damage claim.

Always take photos of the damage before you do anything, and keep detailed receipts for every penny you spend on those emergency repairs. This makes it easy to get reimbursed for those costs without hurting your leverage for the much bigger negotiation to come.

Why is my insurance company offering me a low settlement for my property damage claim?

Insurance companies are for-profit businesses. They use lowball offers as a calculated business strategy to minimize payouts and protect their bottom line. Carriers often bet that policyholders will be too overwhelmed or uninformed to effectively fight for the full amount they are owed.

Should I use the "preferred contractor" recommended by my insurance company?

You should avoid using the insurer’s “preferred” contractor. These vendors often have a financial incentive to write low estimates that match the insurance company's desired payout, potentially leading to cheap materials or incomplete repairs. Always obtain at least two or three independent, detailed estimates from reputable local contractors of your choosing.

How can a policyholder effectively dispute a property damage claim using documentation?

An effective dispute requires creating an unbreakable timeline and a mountain of independent evidence. This includes:

- Meticulous, well-lit photos and videos of the damage.

- A written log of all dates, times, and names from every conversation with the adjuster.

- A complete, itemized inventory list of damaged personal property (brand, model, age, replacement cost).

You should always consider speaking with a professional public adjuster who has done this sort of thing on thousands of claims. Have all your claim questions answered at NO COST! We work for YOU... NOT your insurance company! Speak with a Public Adjuster at (919) 400-6440 or visit For The Public Adjusters website for more details.

What is the Appraisal Clause in my insurance policy, and how can I use it to fight a claim?

The Appraisal Clause is a formal dispute mechanism found in most policies used when you and the insurer disagree only on the cost (value) of the covered damage, not whether the damage is covered. It involves both parties hiring an independent appraiser, who then selects an umpire to settle the dispute. This process is generally faster and less expensive than a lawsuit. Contact an Independent Appraiser with all your questions at (919) 669-9111 or https://insuranceclaimsgroup.com.

When is the best time to hire a public adjuster for a property damage claim?

The best time to hire a public adjuster is immediately after you receive a denial or a lowball settlement offer, or even shortly after the loss is reported. A public adjuster works exclusively for the policyholder, taking control of the entire process—re-inspecting the damage, countering insurer tactics, and aggressively negotiating for the highest possible payout.

You should always consider speaking with a professional public adjuster who has done this sort of thing on thousands of claims. Have all your claim questions answered at NO COST! We work for YOU... NOT your insurance company! Speak with a Public Adjuster at (919) 400-6440 or visit For The Public Adjusters website for more details.

What common tactics do insurance companies use to undervalue a claim?

Insurers use several tactics, including:

- Manipulating estimating software (like Xactimate) by using old labor rates or omitting necessary repair line items.

- Twisting policy language to label a covered peril (like storm damage) as an exclusion (like "wear and tear").

- Encouraging unnecessary delays to wear down the policyholder's resolve.

What should be included in a formal dispute letter when rejecting a low settlement?

A formal dispute letter should be professional, evidence-backed, and sent via certified mail. It must:

- Clearly state your rejection of the settlement amount.

- Systematically go line-by-line, challenging inaccuracies in their estimate.

- Attach your independent contractor estimates and all supporting documentation (photos, inventory, timeline).

How do I counter an insurance estimate that relies solely on computerized pricing software?

You counter a software-generated estimate by providing real-world market data. Present multiple, detailed quotes from local, licensed contractors that reflect the actual, current costs for materials, labor, permit fees, and necessary remediation in your area. This evidence proves the insurer's low number does not represent the true cost to repair the damage correctly.

What options do I have if my insurer refuses to negotiate a fair settlement after a formal dispute?

If your personal negotiation has fallen on deaf ears, you should first consider speaking with a professional public adjuster. They can guide you onto whether you should consider the Insurance Appraisal Clause or if you grounds to file a bad faith lawsuit against the insurance company. This legal action asserts that the insurer breached its duty to act in good faith by wrongfully denying, lowballing, or unreasonably delaying a valid property damage claim. This is typically the final step, so being guided by an experienced insurance litigation attorney or public adjuster is your best bet.

Are you tired of fighting your insurance company alone? The team at For The Public Adjusters, Inc. advocates exclusively for policyholders, not insurance carriers. We have the expertise to counter their delay tactics and lowball offers to secure the full settlement you deserve. Get a no-cost claim review today and let us handle the fight for you. Learn more and get the help you need at https://forthepublicadjusters.com.