Yes — homeowners insurance often covers fallen trees, but coverage depends on why the tree fell and what it damaged. A storm rips through overnight. You wake up to a cracking sound, a slammed roofline, and rain dripping where your ceiling used to be dry. You call the insurance company expecting answers. Instead, you get a claim number, a vague promise that “someone will review it,” and the first hint that this won’t be simple.

That’s the moment most homeowners start asking, does homeowners insurance cover fallen trees? The better question is this: how will the insurer try to limit what it pays?

Because fallen tree claims rarely turn into clean, easy payouts. The carrier may agree the house was hit, then fight about the cause of the fall. It may accept roof damage, then slash debris removal. It may tell you the tree was “old,” the fence was “already worn,” or the cleanup isn’t covered because the trunk landed in the “wrong” place. If you’re already frustrated, you’re not overreacting. You’re seeing the claim fight start in real time.

Table of Contents

- The Crash The Call and The Coming Claim Fight

- Your Policy’s Fine Print Insurers Use to Deny Claims

- Fallen Tree Scenarios and The Inevitable Insurance Dispute

- How to Fight Back Against Common Denials and Low-Ball Tactics

- Special Claim Rules for NC and VA Hurricanes and Windstorms

- Your Secret Weapon A Public Adjuster from For The Public Adjusters Inc

- Take Control Your Next Steps to Secure a Fair Settlement

The Crash The Call and The Coming Claim Fight

The worst part isn’t always the tree. Sometimes it’s the conversation that comes right after.

A homeowner hears the limb break, sees the trunk laid across the roof, and assumes the policy will respond. The first adjuster call sounds calm enough. Then the language starts. “We need to determine the cause.” “We need to inspect for prior condition.” “Removal may be limited.” That’s when a lot of people realize the claim they thought was obvious is already being narrowed.

The insurance company doesn’t experience your loss the way you do. You see a wrecked roof, soaked insulation, a split fence, and a driveway full of debris. The carrier sees categories. Covered peril. Exclusion. Sub-limit. Depreciation. Access issue. Maintenance issue. Those labels decide whether you get paid fairly or get boxed into a partial denial.

The emotional trap after the storm

Most homeowners make one mistake early. They assume cooperation means protection.

It doesn’t. Be polite, but don’t be passive. If you let the insurer define the damage before you understand your own policy position, you’re already behind. Fallen tree claims move fast, especially when emergency crews need access and rain keeps entering the home. That urgency helps the insurer if you don’t document the scene before anything changes.

You don’t need to be hostile. You do need to be organized, skeptical, and ready to challenge a weak coverage position.

Why this claim turns into a dispute so often

Tree claims look straightforward from the street. They’re not. The fight usually centers on three points:

- Cause of the fall: The insurer may focus on whether wind or lightning caused it, or whether the tree was already failing.

- What was damaged: The carrier may separate covered structural damage from non-covered cleanup.

- Value of the loss: Even when coverage exists, the first estimate can leave out major repair and removal costs.

That’s why this topic isn’t just about whether a policy covers a tree. It’s about whether you’re prepared for the claim fight that follows.

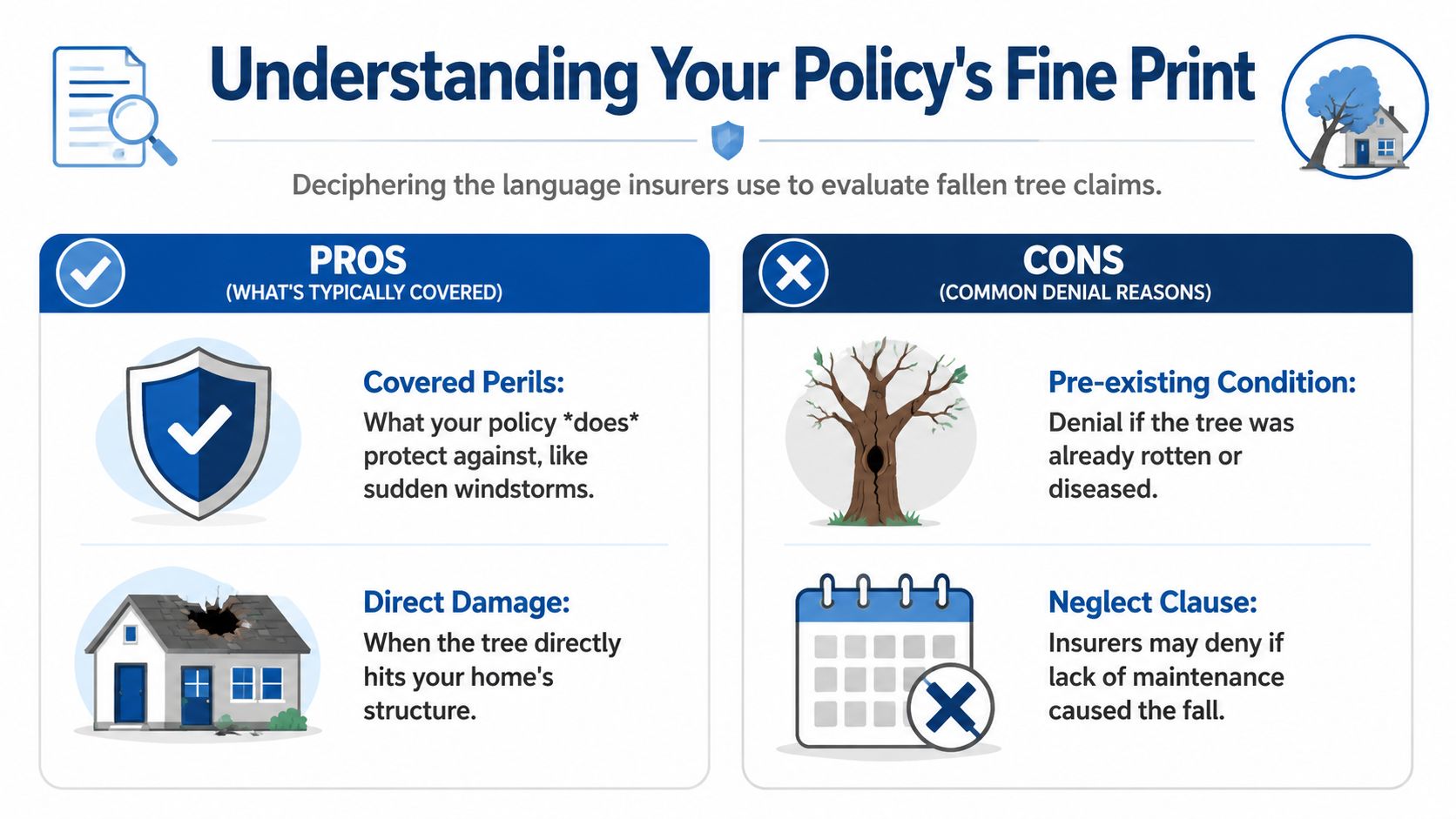

Your Policy’s Fine Print Insurers Use to Deny Claims

Claims get cut down by policy wording long before the insurer sends a formal denial letter.

The carrier will read your policy like a defense lawyer. You need to read it like someone protecting a six-figure asset. The fight usually starts with one question: was the tree loss caused by a covered peril, or can the insurer label it wear, rot, neglect, earth movement, or another exclusion?

The first fight is causation

A storm on the same night does not guarantee an easy approval.

Adjusters often look for any fact that lets them reframe a wind loss as a maintenance problem. They will point to decay, hollow sections, exposed roots, prior limb loss, a visible lean, or old photographs that suggest the tree was failing before the storm. Once they push the claim into that category, they have their excuse to deny all or part of it.

Watch what you say. Offhand comments hurt claims. If you tell the insurer you were “worried about that tree for a while,” expect that statement to show up later as proof of pre-existing damage or neglect.

The second fight is the damaged property

Insurers know homeowners often focus on the fallen tree. The policy usually focuses on what the tree struck.

That distinction matters. A tree on the roof, garage, shed, or fence creates a much stronger claim than a tree lying in the yard. Tree removal by itself is often not the covered event. Direct damage to covered property is.

So stop describing the loss in broad terms. Name every damaged item with precision. Roof decking. Shingles. Underlayment. Gutters. Fascia. Siding. Ceiling stains. Wet insulation. Flooring damaged by rain entering through the opening. Specific damage forces a specific response.

Best rule: Do not argue that a tree fell. Argue that covered property was physically damaged by a covered cause of loss.

The third fight is sub-limits and carve-outs

In this scenario, insurers subtly reduce the claim after admitting part of it.

They may accept the roof damage, then limit debris removal. They may pay to repair the structure, then cap what they owe for hauling away the tree. They may also separate landscaping, shrubs, and yard restoration into smaller buckets with their own restrictions. Homeowners hear “covered” and assume the whole bill is getting paid. That assumption costs money.

Read the declarations, exclusions, additional coverages, and special limits together. If you need a practical breakdown, use this guide on how to read an insurance policy.

Here is the blunt truth. The insurer already knows which line in the policy helps them pay less. Your job is to find it before they use it against you.

Fallen Tree Scenarios and The Inevitable Insurance Dispute

The fastest way to understand these claims is to stop thinking in generalities and look at the specific fact pattern. A tree claim is won or lost on details.

Homeowners insurance usually doesn’t pay for a fallen tree just because it’s in the yard. Coverage generally turns on whether the tree struck a covered structure or blocked access. Removal is commonly covered only if the tree lands on the home, detached garage, shed, fence, or similar insured structure. And if a tree damages a car, homeowners insurance generally doesn’t apply. Allstate’s guidance on tree-fall claims notes that auto insurance with broader protection is the usual source of recovery.

Where claims usually stand or fall

| Scenario | Expected Coverage | Common Insurer Pushback / Low-Ball Tactic |

|---|---|---|

| Tree crashes through the roof | Strongest path to coverage when the facts support a covered cause and direct structural damage | Carrier narrows scope to visible roof damage only and ignores interior water damage, insulation, ceiling damage, and temporary protection costs |

| Tree lands on detached garage or shed | Often treated similarly to other insured structures if the structure is covered under the policy | Insurer questions whether the structure qualifies, then underestimates repair scope or values it cheaply |

| Tree crushes a fence | Coverage may exist if the fence is an insured structure under the policy | Heavy depreciation, arguments that sections were old, and offers based on patchwork instead of proper replacement |

| Tree blocks the driveway but misses structures | Possible limited coverage in some situations, but this is a common dispute area | Carrier says no covered structural damage means no removal payment, or it narrowly interprets access obstruction |

| Tree falls in the yard and hits nothing | Commonly denied for removal | Adjuster treats the whole event as outside coverage and closes the issue quickly |

| Neighbor’s tree falls onto your house | Your own property claim often becomes the first battlefield | Carrier delays while hinting this is a neighbor problem, even though your own policy may still be the immediate path to recovery |

| Tree damages exterior items near the home | Depends on what was hit and how the policy classifies it | Insurer classifies the item in the least favorable way and applies smaller limits or exclusion language |

How to read the insurer’s position

Watch what the adjuster emphasizes. If they ask repeated questions about whether the tree was healthy, they may be building a maintenance denial. If they focus on what the trunk touched and what it didn’t, they may be trying to split covered structural damage from non-covered cleanup.

If the fence is involved, expect depreciation arguments. If the driveway is blocked, expect a narrow reading of access language. If the trunk is in the yard, expect a fast “not covered” answer unless there’s a clear policy basis to challenge it.

Use this checklist when reviewing the first estimate:

- Missing line items: Look for tarping, emergency mitigation, interior drying, insulation, ceiling repairs, and haul-away.

- Bad categorization: Make sure damage to a shed, fence, or detached garage wasn’t ignored because the adjuster focused only on the main dwelling.

- Artificial separation: If the insurer covers the opening in the roof but not the water damage beneath it, that’s a red flag.

- Weak inspection: A quick walkaround from the driveway is not a real damage evaluation.

A low offer doesn’t always arrive stamped “final.” Sometimes it shows up disguised as an incomplete scope.

North Carolina Case Study: Tree Through Roof After Windstorm

After a severe windstorm in North Carolina, a homeowner woke up to a massive pine tree split across the roofline of their two-story home. Rainwater entered through the opening overnight, soaking attic insulation, ceiling drywall, recessed lighting, and hardwood flooring below.

The insurance carrier initially accepted part of the claim but attempted to limit the payout to basic roof repairs and partial tree removal. The first estimate failed to include:

- Wet insulation replacement

- Interior moisture remediation

- Electrical inspection around affected fixtures

- Full debris hauling and crane access

- Hidden framing damage beneath the impact zone

- Additional interior painting and flooring repairs

The homeowner was told much of the damage appeared “pre-existing” or unrelated to the storm event. The insurer also attempted to apply heavy depreciation to several exterior components.

What began as a partial approval quickly turned into a scope and valuation dispute.

After the damage was documented more thoroughly and the missing repairs were challenged, the claim scope expanded significantly beyond the carrier’s original estimate.

This is exactly why fallen tree claims in North Carolina require careful documentation from the beginning. The biggest losses are often not the visible tree impact itself, but the secondary structural and water damage that insurers initially overlook or underpay.

North Carolina Homeowner Review After a Tree Damage Claim

“After a windstorm dropped a large oak tree onto our house we honestly thought the insurance company would take care of everything fairly. Instead, the first estimate barely covered the visible roof damage and ignored the water damage spreading inside the house.

We were overwhelmed, exhausted, and getting vague answers every time we asked questions. For The Public Adjusters stepped in, documented the full scope of damage, challenged the carrier’s inspection, and helped us understand what the policy actually covered.

The difference was night and day. Once the claim was properly presented, the insurance company expanded the scope significantly. We finally felt like someone was fighting for us instead of trying to close the file quickly.”

— John Vauss Raleigh, NC

Reviews like this are common after major tree losses because homeowners often discover the real dispute is not whether damage exists — it’s whether the insurance company is acknowledging the full extent of it.

Homeowners who rely only on the carrier’s first inspection often never realize how much damage was omitted from the original scope.

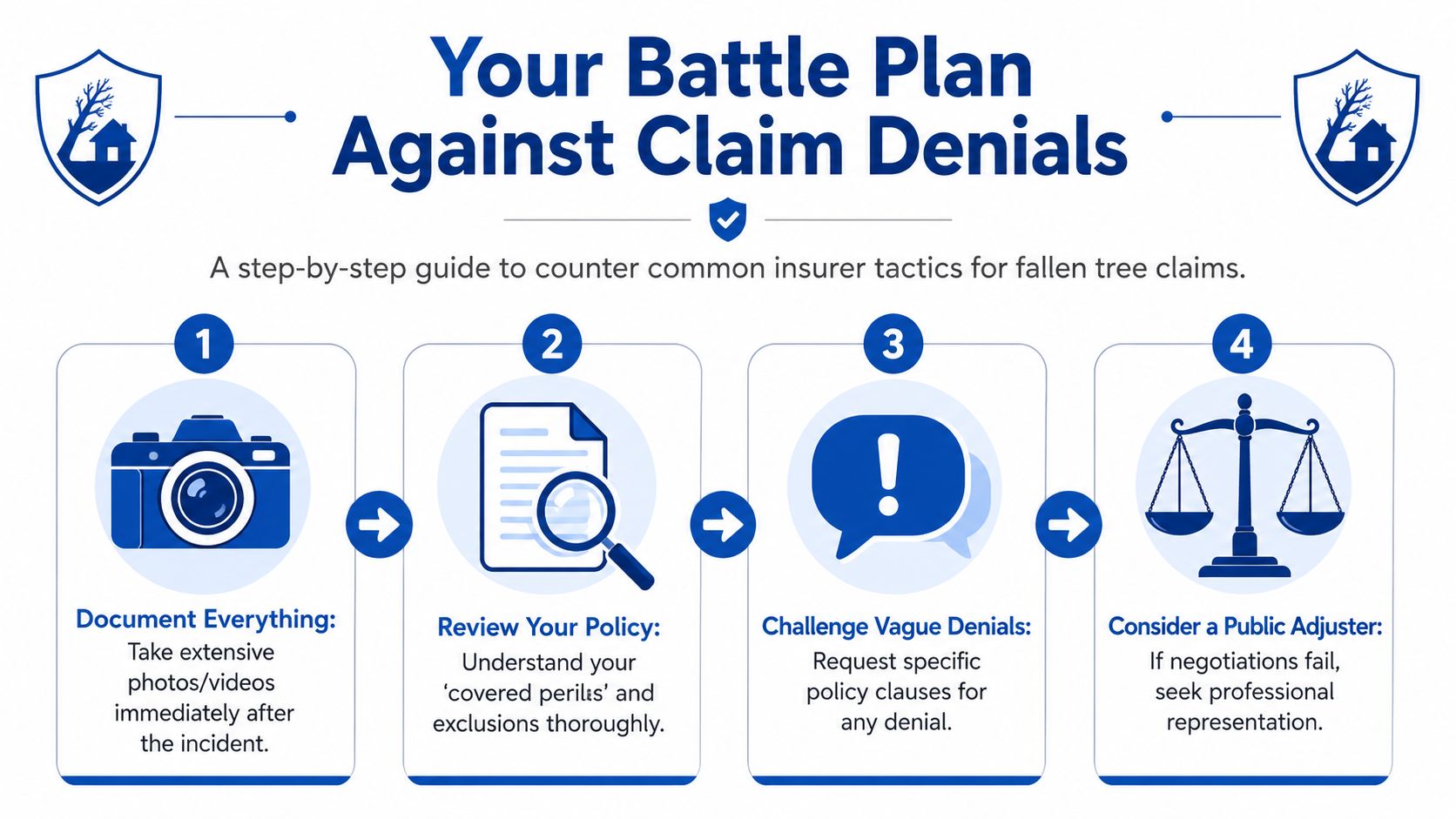

How to Fight Back Against Common Denials and Low-Ball Tactics

Homeowners either take control or get pushed into a bad result. The carrier has a script. You need one too.

Homeowners insurance generally covers fallen-tree damage only when the tree fall was caused by a covered peril such as windstorm, lightning, snow or ice, or vandalism, and the tree then strikes an insured structure. If the fall is traced to rot, age, neglect, or other maintenance failure, coverage is commonly denied because the loss is attributed to an excluded or unmaintained condition rather than a fortuitous peril, according to Progressive’s explanation of fallen tree coverage.

When the carrier blames rot or neglect

This is the denial homeowners hate most because it often feels unfair. The storm was real. The timing is obvious. Yet the insurer says the tree failed because it was compromised before the weather event.

Don’t answer that with outrage alone. Answer it with evidence.

Get the insurer to commit in writing to its actual position. Is it saying rot caused the fall? Is it saying the tree was dead? Is it saying poor maintenance was the dominant cause? Those are different arguments, and vague denial language helps the carrier more than it helps you.

Then gather your own proof:

- Photographs from the day of loss: Wide shots, close-ups of the root ball, trunk split, roof impact, and debris pattern.

- Weather documentation: Not for invented wind speeds or unsupported data points. For timing and event context.

- Arborist input: If the cause is disputed, an independent arborist can be more useful than arguing with the field adjuster.

- Repair and removal estimates: One carrier estimate is not gospel.

If the denial says “wear and tear,” “rot,” or “neglect,” make the insurer tie that claim to a specific policy exclusion and a specific factual basis.

When the estimate ignores real removal costs

Tree losses often require more than chainsaws and a pickup truck. They may involve roof access, rigging, crane coordination, debris sorting, overhead hazards, and protection of the remaining structure.

A common low-ball tactic is to write for basic cleanup while ignoring the complexity of safe removal. Another is to write only for what’s visibly on the roof and skip the hidden damage below the impact point. If the tree punched through and water followed, the claim is not just “remove tree and patch shingles.”

Build your counter the right way:

- Separate removal from repair. Ask contractors to break out emergency stabilization, tree removal, roof work, and interior repair.

- Demand line-item detail. Lump-sum bids are easier for insurers to dismiss.

- Photograph after temporary mitigation too. Once crews move debris, the carrier may later act like the damage looked minor all along.

- Track every communication. Date, time, who said what, and what they promised.

What to say when the denial is vague

A lot of insurers hide behind soft language. “Based on our investigation.” “It appears.” “Coverage may not apply.” That wording is strategic. It sounds official while avoiding a clean position you can attack.

Push back with direct questions:

- Identify the clause: Ask for the exact policy language being relied on.

- Identify the facts: Ask what evidence supports the conclusion.

- Identify what was inspected: Was the roof walked, was the attic entered, was the tree evaluated by a qualified expert?

- Identify what remains open: Don’t let the carrier act like the whole claim is closed if only one category was denied.

If you’re at that stage, this guide on how to dispute a claim will help you organize the challenge.

A strong dispute is calm, specific, and documented. Anger is understandable. Precision is more effective.

Special Claim Rules for NC and VA Hurricanes and Windstorms

In North Carolina and Virginia, tree claims after major storms carry extra complications. The weather event doesn’t just damage property. It also changes how deductibles, causation disputes, and neighbor liability arguments play out.

Named storm deductibles change the math

Many homeowners don’t realize this until the estimate arrives. A hurricane or named storm loss may trigger a different deductible than an ordinary wind event. That means your out-of-pocket cost can be much higher than you expected, even when coverage exists.

This catches people off guard after a tree claim because the damage looks obvious and severe, but the net payout still feels disappointing. Then the insurer compounds the problem by trimming scope, limiting debris removal, or disputing related water intrusion. The result is a covered claim that still feels underpaid.

What should you do? Ask early, in writing, which deductible the carrier is applying and why. Don’t assume the adjuster’s verbal explanation is complete.

Neighbor tree disputes are messy for a reason

Homeowners often think a neighbor’s tree automatically means the neighbor’s insurance should pay. That’s not how these disputes usually begin.

If a storm knocks a tree from the next yard onto your house, your own property claim may still be the first path to recovery. Liability arguments against the neighbor usually depend on proof that the tree was hazardous and that the owner knew or should have known it. Without that proof, carriers often frame the event as storm damage rather than negligence.

The fact that the tree came from next door doesn’t automatically move the claim next door.

For NC and VA homeowners, that matters because storm claims move fast and repair pressure is immediate. You can’t sit still waiting for a neighbor dispute to solve itself while your roof is open and water is entering. Preserve photos, note any visible prior condition if it exists, and keep your focus on your property damage first.

Windstorm claims need disciplined documentation

The best claims in hurricane-prone areas are documented before the insurer starts narrowing the story.

Use a simple order of operations:

- First, secure safety: Keep people clear of unstable limbs, electrical risks, and compromised roof areas.

- Next, preserve the scene: Photograph impact points before major debris is removed if conditions allow.

- Then, document storm-linked damage throughout the property: Not just where the trunk landed, but also interior staining, cracked framing, shifted gutters, and detached structures.

- Finally, challenge partial inspections: A carrier that only inspects the obvious impact site may miss the full windstorm loss.

Storm-prone states reward homeowners who document aggressively and question every shortcut.

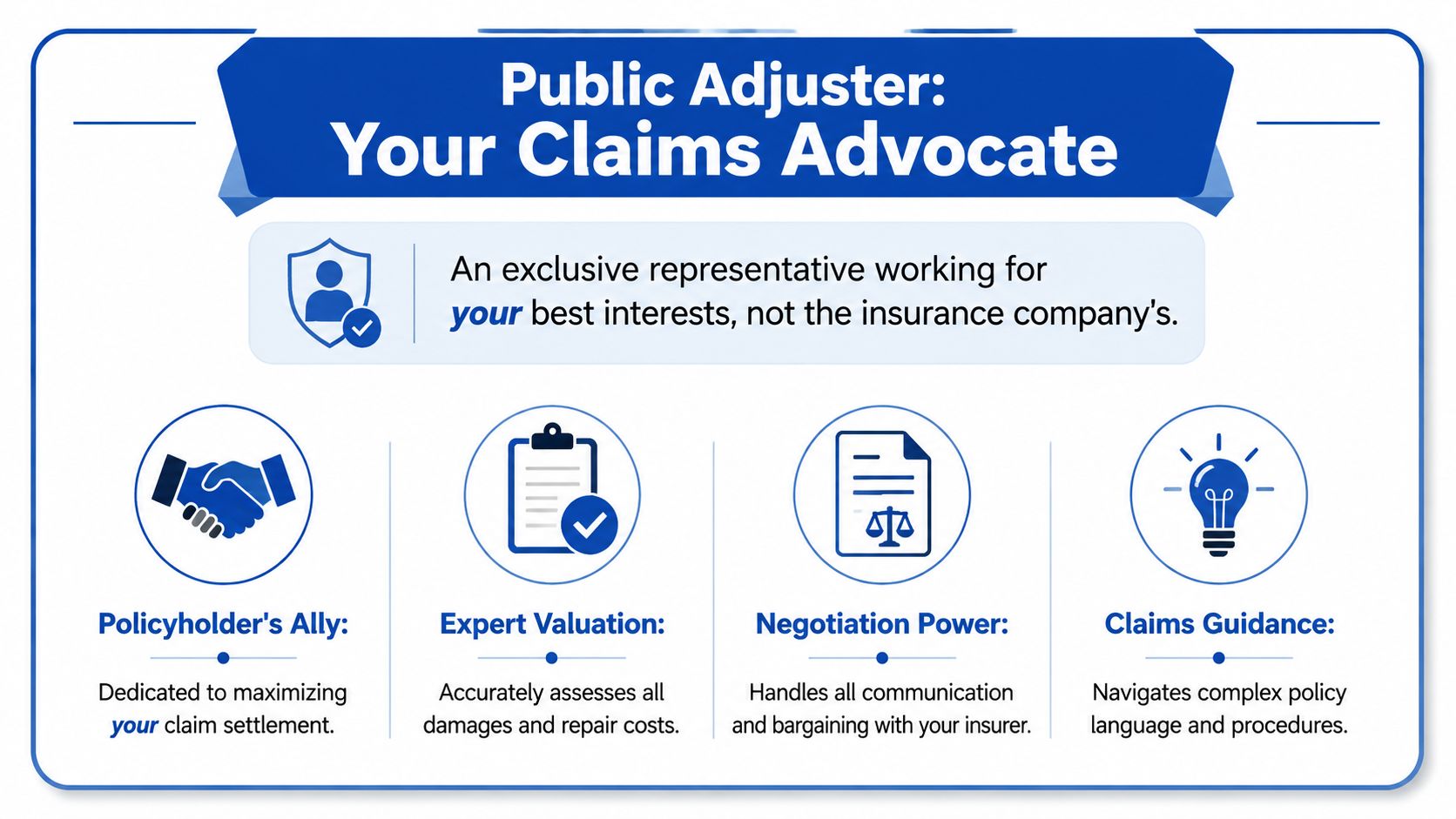

Your Secret Weapon A Public Adjuster from For The Public Adjusters Inc

At some point, many homeowners realize they’re not arguing about a tree anymore. They’re arguing about policy interpretation, construction scope, causation, depreciation, access, and documentation. That’s when claim representation stops being a luxury and starts being practical.

The dispute is often sharpest where consumers least expect it. Insurers’ own guidance shows that cleanup and removal can be capped or unavailable if there’s no covered structural damage, which makes the distinction between tree impact and simple debris a major dispute point in storm-prone markets like NC and VA, as summarized in GEICO’s discussion of tree removal coverage.

Why these claims need an advocate

The insurance company already has adjusters, vendors, systems, and experience on its side. The homeowner usually has one damaged property, one policy they haven’t read in full, and a lot of pressure to make decisions fast.

That imbalance matters in a fallen tree claim because the scope can evolve. A roof hit may also involve attic insulation, wet drywall, framing damage, flooring damage from water entry, and detached structure issues. If nobody is building the full story for the policyholder, the carrier’s smaller story often wins by default.

A good public adjuster works for the policyholder, not the insurer. If you need a clear explanation of that role, read what a public adjuster is.

What strong claim representation actually does

Strong representation is not just “making calls.” It’s technical.

A serious public adjuster will inspect the property carefully, document damage beyond the obvious impact point, review policy language, organize supporting estimates, and push back when the insurer uses broad denial language or a thin scope. They help separate what’s excluded from what’s merely being under-evaluated.

That matters after storms because tree losses rarely happen in isolation. Roof systems, exterior components, and water pathways all interact. Homeowners also need to think ahead. For example, if your property includes vulnerable exterior features, storm prep matters long before the next claim. Resources on safeguarding screen enclosures from storms can help reduce future damage to attached outdoor structures and surrounding improvements.

Here’s what effective representation usually looks like in practice:

- Damage scoping with discipline: The inspection follows the path of impact and the path of water, not just the most visible break.

- Estimate review with skepticism: If the carrier’s scope feels thin, it probably is. Missing trades and missing line items are common.

- Policy-based negotiation: The argument isn’t “please pay more.” It’s “this damage falls within the contract, and your scope or valuation is incomplete.”

- Communication control: Homeowners stop carrying the burden of every insurer call, vague update, and shifting explanation.

A good claim file is built, not hoped for.

That’s the fundamental value. It turns a chaotic event into a documented position the insurer has to answer.

Take Control Your Next Steps to Secure a Fair Settlement

If you’re dealing with this right now, don’t wait for the carrier to define the claim for you. That’s the fastest way to get boxed into a partial payout.

The right mindset is simple. The insurance company’s first position is not the final word. It’s an opening move.

What to do right now

Start with the steps that help ensure a favorable outcome:

- Photograph before major changes: Get wide and close shots of the tree, roofline, debris field, interior water, detached structures, and any blocked access.

- Protect the property: Reasonable temporary measures matter, but document the condition before and after.

- Read the actual denial or estimate: Don’t rely on phone summaries. The written language matters.

- Get independent estimates: One estimate from the insurer is not enough if the damage is complex.

- Keep a claim log: Track names, dates, promises, and inspection details.

If the insurer says the tree was rotten, ask for proof. If it says removal isn’t covered, ask which policy language applies. If it pays for the roof opening but not the interior damage beneath it, challenge the separation.

Mistakes that cost homeowners money

A few errors show up over and over:

- Accepting the first number too quickly: Fast money feels good when your house is exposed. It can also lock in a bad scope.

- Throwing away evidence: Once debris is gone and repairs begin, weak documentation becomes your problem.

- Talking loosely about prior condition: Casual comments about an aging tree can get repurposed against you.

- Assuming the adjuster saw everything: Many inspections are shorter and narrower than homeowners realize.

- Treating a partial approval like a fair settlement: A claim can be “accepted” and still be badly underpaid.

Your job is not to make the insurer comfortable. Your job is to protect your property and insist on a fair reading of the policy.

If you’ve been asking does homeowners insurance cover fallen trees, the honest answer is this: sometimes yes, often partially, and frequently only after a fight. Coverage depends on cause, impact, structure, and policy wording. Payment depends on how well the loss is documented and how forcefully weak claim positions are challenged.

If your fallen tree claim has been denied, delayed, or low-balled, For The Public Adjusters, Inc. can help you level the playing field. Their team represents policyholders across North Carolina and Virginia, reviews property damage claims at no cost, and helps homeowners challenge weak inspections, incomplete scopes, and unfair settlement offers. If the insurance company is giving you vague answers or a number that doesn’t come close to the actual damage, get a professional claim review before you accept less than you’re owed.