When your property gets hit with major damage, the last thing you want to do is fight with your insurance company. It’s an overwhelming process. This is where a public insurance adjuster comes in. They are state-licensed professionals who work exclusively for you, the policyholder—not for the insurance company. Think of them as your personal advocate in the claims process.

Your Expert Advocate in an Insurance Claim

Let’s say a major fire or water leak damages your home. The first person your insurance company sends out is their own adjuster. While they might seem helpful, their job is to protect their employer’s financial interests, not yours. Right away, the odds are stacked against you. You’re trying to deal with the chaos of a disaster while also trying to make sense of dense policy language and document every single loss.

A public insurance adjuster steps into this situation to balance the scales. They take over the entire claims process, acting as your dedicated strategist from beginning to end.

Leveling the Playing Field

Their role goes way beyond just filling out forms. A public adjuster brings certified expertise to the table to protect your financial recovery. They handle the nitty-gritty details with a fine-toothed comb.

Here’s what they do for you:

- Deep-Dive Policy Review: They’ll tear apart your insurance policy to find every ounce of coverage you’re entitled to—even the hidden clauses you’d likely miss.

- Meticulous Damage Documentation: Using professional tools and experience, they create a detailed, comprehensive list of everything you’ve lost, from the foundation to your personal belongings.

- Manage All Communication: They take over all the back-and-forth with the insurance company. No more stressful phone calls or endless emails for you.

A public adjuster has one mission: to make sure you get the full and fair settlement you are owed under your policy. They are the perfect counter to the conflict of interest that arises when an insurance company is asked to investigate its own financial obligation to you.

By building a rock-solid, evidence-based claim, they negotiate for the true cost of getting your life back to normal. This kind of professional representation is your best defense against common insurance company tactics like delays, denials, and lowball offers.

Knowing how public adjusters work can give you the confidence to pursue a better outcome. Their help turns a stressful, confusing ordeal into a managed process, letting you focus on rebuilding while they fight to get you the money you need.

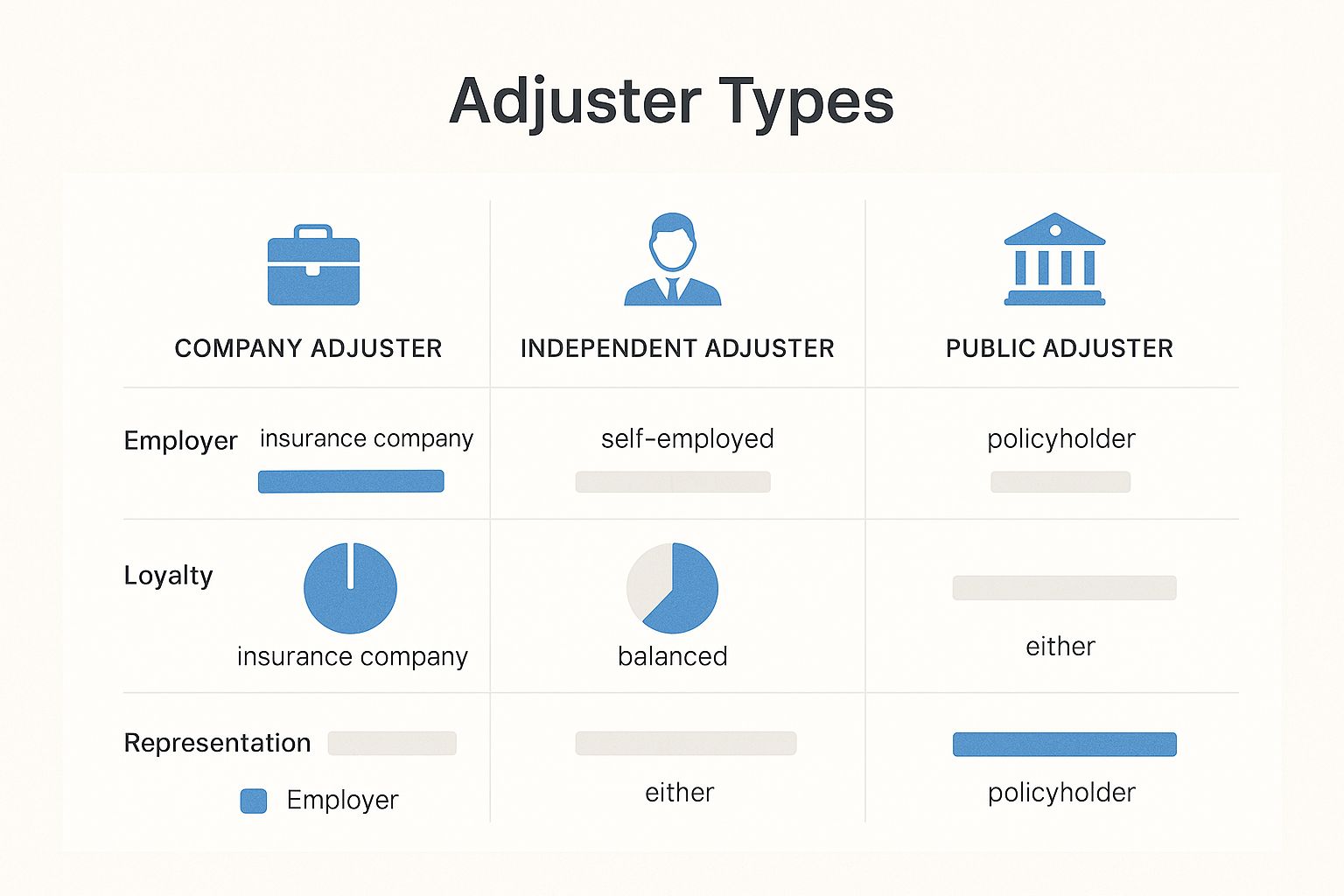

Understanding the Different Types of Adjusters

When you file an insurance claim, you’ll quickly hear the word “adjuster.” But here’s something most people don’t realize: not all adjusters are on your side. Knowing who’s who is absolutely critical to protecting your interests after a loss.

There are three main types, and each one has a very different boss.

Company and Independent Adjusters: Who Do They Really Work For?

The first person you’ll probably meet from your insurance company is the company adjuster. They are a direct employee of the insurer, and their loyalty lies with the company that signs their paychecks. Their job is to assess the damage from their employer’s point of view, which often means limiting the payout.

Then there’s the independent adjuster. The name can be a bit misleading. These are contractors, not employees, but they are still hired and paid by insurance companies. Insurers often call them in to help when they’re swamped with claims, like after a big storm hits. Even though they’re “independent,” they still work for the insurance company, not for you.

To make this crystal clear, let’s break down who each adjuster represents.

Company Adjuster vs Independent Adjuster vs Public Adjuster

| Adjuster Type | Who They Represent | Primary Goal |

|---|---|---|

| Company Adjuster | The insurance company (as an employee) | Protect the insurer’s financial interests and limit the claim payout. |

| Independent Adjuster | The insurance company (as a contractor) | Fulfill their contract with the insurer, whose goals they must align with. |

| Public Adjuster | You, the policyholder | Maximize your settlement and ensure you receive fair compensation. |

As you can see, the lines of loyalty are very clearly drawn. Only one of these professionals has a legal and ethical duty to you.

The Public Adjuster: Your Advocate in the Claims Process

This brings us to the public insurance adjuster. A public adjuster is a state-licensed professional who works exclusively for you, the policyholder. They have zero ties to the insurance company.

Their one and only job is to get you the fair and full settlement you’re entitled to under your policy.

This infographic gives a great visual breakdown of how the loyalty and representation differ among the three types.

The key distinction is that a public adjuster has a fiduciary duty to you and you alone. They level the playing field.

The insurance company has its experts—the company and independent adjusters—working to protect its bottom line. A public adjuster is your expert, dedicated to protecting your bottom line. They handle everything from documenting the damage to negotiating with the insurer, making sure your voice is heard and your rights are protected.

Hiring a public adjuster is about ensuring you have an expert on your team with the same level of knowledge as the professionals on the insurance company’s side. They are your dedicated advocate in a complex process.

When Should You Hire a Public Adjuster?

Knowing the right moment to call for backup can completely change the outcome of your insurance claim. A public adjuster probably isn’t necessary for every little thing—a minor leak or a few missing shingles, for example. But when the stakes are high, their expertise is invaluable.

Think of it this way: you might fix a dripping faucet yourself, but you’d call a plumber for a burst pipe that’s flooding your house. A public adjuster is that emergency expert for serious property damage.

If your home or business has taken a major hit, you should be thinking about getting professional help right away. The sooner you bring them into the picture, the better. They can manage the process from the very beginning and help you avoid common mistakes that could cost you thousands down the road.

Clear Signals It’s Time to Call an Expert

Some situations are giant red flags telling you it’s time to get an advocate in your corner. If you wait too long, you’re putting yourself at a real disadvantage against the insurance company’s team of seasoned professionals.

You should seriously consider hiring a public adjuster if you’re facing any of these issues:

- Large or Complicated Claims: We’re talking about damage from a fire, hurricane, major flood, or a tornado. These events are messy, often involving structural damage, smoke and water issues, and a mountain of personal property to inventory. It’s a lot to handle, and it requires an expert’s touch to document everything correctly.

- An Unfairly Low Settlement Offer: If the first offer from your insurance company feels like a slap in the face and won’t even begin to cover the cost of repairs, that’s a big warning sign. It often means their adjuster missed crucial details or is deliberately undervaluing your loss.

- Significant Delays or Radio Silence: Is your insurer dragging its feet? Not returning calls? Throwing up one bureaucratic roadblock after another? These are often tactics meant to frustrate you into giving up. An expert can cut through that red tape.

- A Denied Claim: A claim denial is rarely the final word. A good public adjuster can dissect the denial letter, find the evidence to challenge it, and reopen the claim to fight for the settlement you deserve.

Hiring a public adjuster isn’t admitting defeat; it’s a strategic move to level the playing field. It shows the insurance company that you’re serious about getting the full and fair settlement you’re entitled to.

At the end of the day, if you feel overwhelmed, confused by the dense language in your policy, or just completely outgunned by the insurance company, bringing in a professional is the smartest thing you can do to protect your financial recovery.

Here’s the rewritten section, designed to sound completely human-written and natural.

So, What’s This Going to Cost Me?

It’s one of the first questions on every homeowner’s mind: “How much does a public insurance adjuster charge?” When you’re already staring down the barrel of repair bills and displacement costs, the last thing you want is another expense.

The good news is, that’s not how it works. Reputable public adjusters operate on what’s called a contingency fee.

Put simply, you don’t pay them a single penny out of your own pocket. Instead, their fee is just a small, agreed-upon percentage of the final insurance settlement they win for you. If they can’t get you a settlement, you owe them nothing. It’s as simple as that.

A Partnership Where Everyone Wins

This payment model is fantastic because it puts your adjuster on your side of the table, 100%. Their success is directly tied to your success—the more money they get for you, the more they earn.

Think of it as a performance-based partnership. They are completely invested in getting you the absolute best outcome possible.

Typically, this fee is a small percentage of the claim, often somewhere in the 10-15% range. That might sound like a lot, but their knack for uncovering hidden damages, understanding dense policy language, and negotiating with the insurance company almost always leads to a much larger final settlement than you could ever secure on your own.

When an adjuster works on contingency, they’re putting their own time and resources on the line for you. Their paycheck depends entirely on the results they deliver, which makes hiring one a powerful investment in your own financial recovery.

While a staff adjuster might earn an average salary around $75,770 a year, a public adjuster’s income is directly tied to how well they serve their clients. It’s a powerful incentive to fight for every dollar you need to rebuild. You can dig a little deeper into adjuster income and fee structures on adjusterpro.com.

At the end of the day, that small percentage you pay your public adjuster is usually just a fraction of the extra money they find for you. It’s one of the smartest financial moves you can make after a disaster.

How a Public Adjuster Maximizes Your Claim

So, what’s the secret sauce? How does a public adjuster actually get you a bigger settlement? It’s not about magic tricks or aggressive tactics. It’s a methodical process that combines deep policy knowledge with painstakingly detailed documentation.

They don’t just argue for more money; they build an ironclad, evidence-backed case for what your claim is truly worth.

It all starts with your insurance policy. A good public adjuster will comb through every single page, line by line. They’re hunting for all the coverages you’re entitled to, especially the obscure clauses and endorsements that policyholders (and even the insurance company’s adjuster) often miss. This deep dive frequently uncovers hidden value right from the get-go.

From there, they pivot to creating an exhaustive inventory of your loss. This isn’t just a quick walkthrough with a smartphone camera. It’s a forensic-level investigation of the damage.

Building a Bulletproof Case

A public adjuster’s real strength lies in how meticulously they document every single detail. They use specialized tools and industry-standard software to build a complete and undeniable picture of what it will cost to put your life back together.

This detailed approach involves a few key steps:

- A Detailed Scope of Work: They create a professional-grade repair estimate that specifies the exact materials, labor, and steps needed. Nothing is left to guesswork.

- Evidence Gathering: They go beyond what’s visible, using tools like thermal imaging cameras and moisture meters to find hidden damage behind walls or under floors.

- Expert Valuation: From the cost of lumber to the replacement value of your personal belongings, they price everything accurately. This prevents the insurer from lowballing the value of your property.

A public adjuster transforms your claim from a simple request into a professional, evidence-based demand. They handle all communication with the insurance company, presenting a powerful argument that is difficult for the insurer to dispute.

By taking over the entire process, they relieve you of the stress of dealing with endless phone calls and mountains of complicated paperwork. Their negotiation expertise is one of the biggest benefits of hiring a public insurance adjuster, making sure the final check reflects the true extent of your loss—not just the insurer’s opening offer.

Why Insurance Claims Feel So Complicated These Days

Filing an insurance claim isn’t what it used to be. The landscape has shifted dramatically, and what was once a straightforward process has become incredibly complex for the average homeowner.

Insurance carriers now lean heavily on sophisticated software, data analytics, and rigid review processes to control what they pay out. For a policyholder just trying to get back on their feet after a disaster, it can feel like you’re up against a system designed to work against you.

On top of that, we’re seeing more severe weather events, and the costs for building materials and labor have shot through the roof. This means claims are not only more frequent but also much more expensive, a perfect storm that can turn a stressful event into a full-blown financial crisis.

Why You Need a Pro in Your Corner

This is where a public insurance adjuster becomes your most valuable ally. Think of them as a professional guide who knows every twist and turn of the modern claims maze. Their entire job is to counter the complex systems insurance companies use to minimize settlements.

The insurance market itself is fiercely competitive. While that might sound good for consumers, it often pressures carriers to tighten their belts and scrutinize claims even more closely to protect their profits. You can read more about how these market shifts impact claims on ajg.com.

A public adjuster levels the playing field. They make sure your claim is evaluated based on its true, documented merits—not just the insurance company’s initial, often low, assessment. It’s about getting a fair shot in a system that has grown increasingly difficult.

Hiring an advocate gives you the expertise to build a solid, evidence-backed claim. It’s a common question policyholders ask: can a public adjuster obtain higher compensation for a claim? The answer lies in their skill at meticulously documenting every detail of your loss and negotiating from a position of strength, ensuring you receive the full settlement you’re entitled to.

Got Questions? We’ve Got Answers

Even after learning what a public adjuster does, you probably still have a few questions rolling around in your head. That’s completely normal. Bringing in a professional is a big decision, and you should feel confident before you make a move.

Let’s tackle some of the most common questions we hear from homeowners.

Is It Too Late to Hire an Adjuster if I Already Filed My Claim?

Not at all. You can bring a public adjuster on board at any stage of the game. In fact, many people don’t realize they need help until they’re staring at a frustratingly low settlement offer or their claim has gone silent for weeks.

A good adjuster can jump right in, reopen a denied or underpaid claim, and start a fresh, comprehensive assessment of the damage. They’ll then go back to the insurance company to negotiate for a supplemental payment. It’s almost never too late to get an expert in your corner.

Are Public Adjusters and Attorneys the Same Thing?

That’s a great question, but no, their roles are quite distinct. Think of a public adjuster as your property damage and policy expert. They specialize in documenting the physical loss, digging into the fine print of your policy, and fighting for the maximum financial settlement you’re entitled to.

An attorney steps in when things get legal. You’d hire a lawyer if you need to sue your insurance company for acting in bad faith or breaching your contract. For the vast majority of property damage claims, a public adjuster is the right first call.

A public adjuster handles the what and how much of your property damage claim. An attorney handles the legal fight if the insurance company breaks the law or violates your rights.

How Can I Find a Good Public Adjuster?

Finding the right professional is crucial. Start by verifying they are licensed to practice in your state—that’s non-negotiable. Look for someone with a solid track record and real, verifiable testimonials from past clients.

You can also check for memberships in professional organizations like the National Association of Public Insurance Adjusters (NAPIA). Most importantly, talk to a few different adjusters. You need to find someone you trust and can communicate with easily, especially when you’re already stressed out.

If you’re facing a complex claim in North Carolina or Virginia, you don’t have to handle it alone. The team at For The Public Adjusters, Inc. offers no-cost claim reviews to help you understand your situation and secure the settlement you deserve. Learn more and get the expert help you need by visiting us online.

Article created using Outrank