The moment you discover damage to your home or business is a gut-punch. Whether it’s from a storm, a fire, or a burst pipe, the chaos can feel paralyzing. But your actions in these first 48 hours are absolutely critical. This insurance claim state farm guide will give a process you can follow.

What you do right now lays the groundwork for your entire State Farm insurance claim. It’s about securing the scene, stopping the damage from getting worse, and getting the ball rolling with the insurer the right way.

What to Do Immediately After insurance Claim State Farm Property Damage

That first look at significant property damage is jarring. It’s easy to get overwhelmed. But remember, your insurance policy is a contract, and it requires you to take specific, responsible actions to protect your property from more harm. Documenting every step you take from this point forward is the first block in building a strong claim.

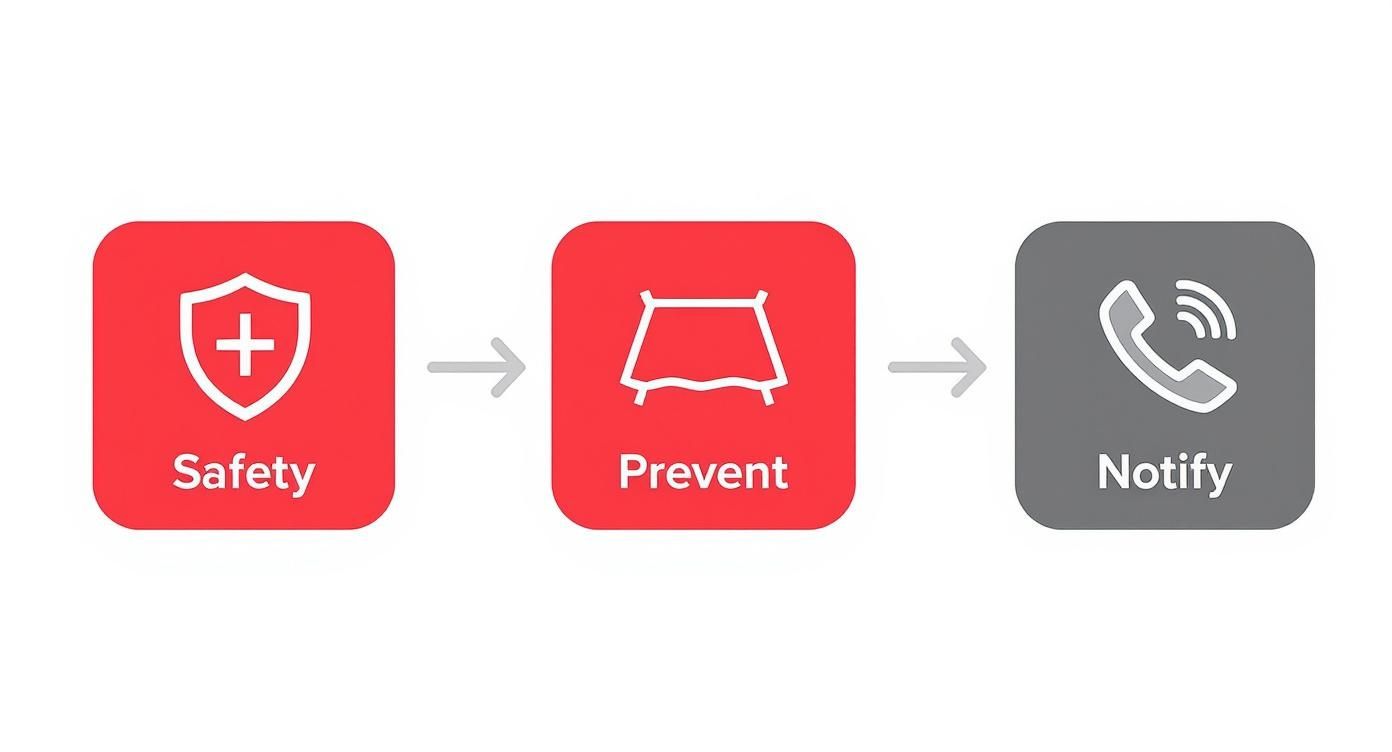

This quick visual breaks down the three most important things you need to do right away.

It’s a simple, powerful sequence: your safety comes first, then stop the bleeding, and only then do you call the insurance company.

To help you stay focused during a stressful time, here’s a quick checklist of the essential first steps.

Immediate Actions Checklist for Your State Farm Claim

| Action Item | Why It’s Critical | Example |

|---|---|---|

| Ensure Safety | Your life and health are priceless. | If you smell gas, see downed power lines, or the structure feels unstable, evacuate immediately and call 911. |

| Mitigate Damage | Your policy requires you to prevent further harm. Failing to do so can jeopardize your claim. | Tarping a damaged roof to stop rain from getting in, or boarding up a broken window. |

| Document Everything | Photos and videos are undeniable proof of the initial damage before any cleanup or repairs. | Take hundreds of photos and videos from every angle, both wide shots and close-ups of the damage. |

| Contact State Farm | Prompt notification is a policy requirement and officially starts the claim process. | Call the State Farm claims number or use their app to report the loss. |

| Keep All Receipts | Expenses for temporary repairs and mitigation are often reimbursable. | Save the receipt from Home Depot for the tarp and plywood, and the invoice from the water extraction company. |

Following this checklist ensures you’re protecting both your property and your rights under the policy from the very beginning.

Prioritize Safety Above All Else

Before you even glance at your insurance policy, your absolute first priority is the safety of everyone on the property. Things like structural damage, live wires, or contaminated floodwater can be incredibly dangerous.

If you have any doubt—you smell gas, see fallen power lines, or the building looks unstable—get out immediately. Do not go back inside until a professional, like a firefighter or a utility crew, gives the all-clear. Nothing is more important than your personal safety.

Prevent Further Damage

Your State Farm policy, like virtually all property insurance policies, contains a “duty to mitigate” clause. In plain English, this means you’re required to take reasonable steps to keep the damage from spreading. If you don’t, State Farm could argue that any subsequent damage isn’t their responsibility.

This isn’t about starting a full-scale renovation. We’re talking about emergency, temporary fixes.

- For water damage: Shut off the main water valve if it’s safe. After a storm, you might need a pro to start pulling out water and setting up industrial fans.

- For roof damage: Get a tarp over the hole. This prevents rain from pouring in and ruining everything inside.

- For broken windows or doors: Board them up. This keeps the weather out and secures your property from theft.

Document every single thing you do. Take pictures before you put the tarp on and after. Keep every receipt for supplies and every invoice from emergency contractors. These costs are almost always covered as part of your claim.

Notify State Farm Promptly

Once the property is safe and secured, it’s time to call State Farm. Your policy requires you to provide “prompt notice” of the loss. When you make that first call or file online, just stick to the basics.

You don’t need a complete damage inventory on this first call. The goal is simply to open the claim. Give them your policy number, a very brief and factual description of the incident, and your best contact info.

Avoid guessing about the cause or the full extent of the damage. Keep it factual and simple. For example, instead of saying, “I think the whole roof is a total loss,” just say, “A large tree limb fell on the garage and put a hole in the roof.”

This sets a professional, no-nonsense tone and officially gets your claim into their system.

How to Document Your Property Damage Claim

Once the initial shock from the damage wears off, your mindset has to shift immediately. You are now in the business of proving your loss. I can’t stress this enough: the success of your insurance claim state farm will rise or fall based on how well you document everything. A few quick snaps with your phone isn’t going to cut it. You need to build an ironclad case so there’s nothing for them to argue about.

Start thinking like a detective compiling a case file. Every single photo, video, receipt, and note is a piece of evidence. The more meticulous and organized you are, the more power you’ll have when it’s time to talk turkey with the State Farm adjuster.

Go Beyond Basic Photos

Your camera is your best friend right now, but how you use it makes all the difference. Your goal is to tell the complete story of what happened, from the 30,000-foot view all the way down to the tiny details.

- Start Wide, Then Go Deep: Kick things off with overview shots of every single affected room. This establishes the scene. From there, zoom in on the specific damage—the warped floorboards, the sagging and stained ceiling, the cracks spidering up a wall, the soot clinging to your furniture.

- Label Everything: Don’t even think about relying on your memory. It will fail you. As you take pictures, make a simple log or use a photo app to add captions. For instance: “Living Room – East Wall – Water Stain from Roof Leak – 10/26/2024.” That kind of clarity is priceless weeks or months down the road.

- Show Scale and Context: This is a pro move. Place a ruler or a tape measure next to a crack or a water stain to give it scale. Make sure you also snap pictures of the manufacturer’s label or serial number on any damaged appliances or electronics.

This kind of methodical approach stops an adjuster from trying to minimize the damage. You’re not just showing them a stain; you’re showing them a 14-inch water stain that proves significant, undeniable saturation.

Harness the Power of Video Walkthroughs

A narrated video walkthrough is probably the most powerful piece of evidence you can create. It breathes life into those static photos and, more importantly, it lets you control the story of your claim.

Just hit record and walk through your property, moving from room to room. Talk out loud, pointing out the damage as the camera sees it. For example, you might say, “Coming into the kitchen now, you can see the water has completely delaminated the base of these cabinets. The floor is buckled clear across the room and into the hallway.”

That commentary adds a whole other layer of detail that pictures just can’t match. It connects the dots for the adjuster and turns your claim from a file number into a personal, compelling account of your loss.

Create a Detailed Inventory of Damaged Items

If your personal belongings or business inventory were damaged, you’ve got to create a comprehensive list of every single item. I know this is the part everyone dreads—it’s tedious and time-consuming, but it is absolutely mandatory if you want a fair settlement for your contents.

Pro Tip: Do not throw anything away. I don’t care how ruined it looks. Don’t discard a single item until it has been inspected and documented by the adjuster. If you toss things early, the insurance company has a perfect excuse to deny that part of your claim, saying they couldn’t verify the loss.

Your inventory needs to be organized. For every item, you need:

- Item Description: Be specific. Not just “TV,” but “Samsung 55-inch 4K Smart TV.”

- Brand and Model Number: If you can find it.

- Original Purchase Price: Dig for old receipts or credit card statements. If you can’t find them, look up similar items online.

- Age and Condition: Be honest about how old it was and what shape it was in before the loss.

- Link to Replacement: This is huge. Find a link to a new, comparable item online to prove what it costs to replace it today.

Document Every Single Expense

Remember, your claim is more than just the building and your stuff. It also covers any money you have to spend because of the damage. This is especially true for Additional Living Expenses (ALE) if you’re forced out of your home or Business Interruption (BI) if your commercial operation is shut down.

Get a folder and keep every single receipt for things like:

- Temporary repairs (tarps, boarding up windows, etc.)

- Hotel bills or short-term rent

- Meals out (if your kitchen is out of commission)

- Laundry services (if your machines are damaged)

These expenses add up fast and are a key part of a full insurance claim state farm. No receipts, no proof, no reimbursement. It’s that simple. This level of detail is also critical as major insurers face more scrutiny. For example, State Farm, as the largest homeowners insurer in the U.S., has even faced legal action from the Illinois Attorney General over its refusal to share key data. You can learn more about the importance of insurer transparency on SFChronicle.com.

Working With The State Farm Adjuster

Once you’ve filed your claim, the next person you’ll deal with is the State Farm adjuster. This is the person who holds the purse strings. They evaluate the damage and write the first check, so how you manage this relationship can make or break your claim’s outcome.

It’s crucial to remember who they work for. The adjuster’s primary job is to close your claim based on State Farm’s rules and your policy’s fine print. They’re not your advocate. While most are professional, their loyalty is to their employer, not to getting you the maximum payout.

Understanding Who You Are Dealing With

State Farm has a few different types of adjusters they might send out, and knowing which one you’ve got can give you some useful context.

- Staff Adjusters: These are full-time State Farm employees. They live and breathe the company’s internal procedures for everything from a kitchen fire to a flooded basement.

- Independent Adjusters: When a big event like a hurricane hits, State Farm gets swamped. They bring in independent, third-party adjusters to handle the overflow. They work for State Farm on a contract basis but aren’t on the payroll.

- Catastrophe (CAT) Adjusters: These are the storm chasers, either staff or independent, who parachute into disaster zones. They’re pros at managing a ton of claims in high-stress situations.

At the end of the day, it doesn’t matter what their title is. Their job is the same: inspect your property, read your policy, and create an estimate for the repairs. That estimate becomes their opening offer.

Preparing For The On-Site Inspection

The adjuster’s visit is your prime time to make your case. Don’t be a passive bystander; you need to be an active participant who’s fully prepared.

Before they even pull into your driveway, have all your ducks in a row. Get a folder and organize your photo and video evidence, your detailed inventory of everything that was damaged, and copies of receipts for any temporary repairs you had to make.

When the adjuster arrives, you lead the tour. Walk them through the damage, pointing out every detail you’ve documented. Show them your “before” pictures to drive the point home.

Here’s a pro tip: Listen more than you talk. Answer their questions with facts, not feelings or guesses. Never admit fault or speculate. Instead of saying, “I guess the storm was just too much for my old roof,” you say, “The storm winds damaged this part of the roof here.”

Your goal is to be seen as helpful and cooperative, but you are also there to control the narrative with solid proof. Let your documentation do the talking.

Managing Communications And Following Up

After that first meeting, shift every important conversation to writing. A phone call is fine for a quick “what’s the status?” check-in, but anything about the scope of work, repair costs, or settlement numbers needs to be in an email. This creates a paper trail that you can rely on.

If you do have a phone call where the adjuster makes a promise or gives you key information, send a follow-up email immediately. Something simple like: “Hi [Adjuster’s Name], just wanted to recap our call from this morning. You confirmed that the damaged hardwood floors are covered for full replacement. If I misunderstood, please let me know. Thanks!”

This one simple habit prevents “he said, she said” arguments later. It turns a verbal agreement into a documented fact, which is priceless if a dispute pops up.

Responding To The Initial Estimate

Sooner or later, the adjuster will send you their damage estimate, often called a Scope of Loss. Do not—I repeat, do not—treat this as the final word. It’s just their opening bid in a negotiation.

Go through it with a fine-tooth comb. Look for common mistakes and lowball tactics:

- Missed Items: Did they include the cost of priming and painting the new drywall? What about the baseboards?

- Incorrect Measurements: Double-check their square footage. It’s amazing how often these numbers are off.

- Low-Quality Materials: Did they price out cheap carpet to replace your high-end hardwood?

- Outdated Labor Rates: Are their labor costs based on what contractors actually charge in your town right now?

If you find problems, you need to push back with your own evidence. Get detailed quotes from trusted local contractors to counter their low numbers. This is a business deal. Come prepared. For a much deeper look into the art of the deal, check out our guide on how to negotiate with an insurance adjuster. Being firm, professional, and armed with facts is how you turn an undervalued estimate into a fair settlement for your insurance claim state farm.

How to Dispute a Low Settlement Offer

Getting that settlement letter from State Farm only to see a number that doesn’t even come close to what you need—or worse, an outright denial—is a gut punch. It feels final. But it’s not.

That first offer is just that: an offer. It’s the start of a negotiation, not the end of the road. You have every right to challenge it, and if you approach it correctly, you can successfully dispute an unfair decision on your insurance claim state farm.

The trick is to figure out why they lowballed or denied your claim. From there, you can build a methodical, evidence-based case to tear their reasoning apart. This isn’t about yelling on the phone; it’s about making a business case for why your policy says you’re owed more.

Why Did They Underpay or Deny the Claim?

State Farm’s adjusters don’t just pick a number out of a hat. Their low offer is usually rooted in a specific interpretation of your policy or how they’ve assessed the damage. Getting inside their logic is the first step to beating it.

Here are the most common reasons we see for disputes:

- Disputes Over Cause of Loss: The classic “wear and tear” argument. The adjuster might claim the damage was from a long-term issue your policy doesn’t cover, not the sudden storm that just blew through.

- Aggressive Depreciation: This one is huge. They might apply an unreasonably high depreciation rate to your damaged property, which dramatically slashes the Actual Cash Value (ACV) check you get upfront.

- Pointing to Policy Exclusions: Adjusters love to dig into the fine print and find an exclusion for things like mold or specific types of water damage to justify a denial. In fact, some internal insurance protocols for things like water damage have even been challenged in court as being designed to systematically deny valid claims.

- An Incomplete Scope of Work: This happens all the time. The adjuster’s estimate simply misses things—like forgetting to include the cost of priming and painting the new drywall or overlooking the need for specialized equipment to do the job right.

These reasons are frustratingly common, but they are absolutely beatable.

To help you get started, here’s a quick look at how you should initially react to these common roadblocks.

Common Claim Disputes and Your First Response

| Dispute Reason | What It Means | Your First Action |

|---|---|---|

| Cause of Loss Disagreement | They’re blaming “wear and tear” or another uncovered event. | Review your policy’s “covered perils” section and provide your own expert report (e.g., from a roofer) stating the true cause. |

| Excessive Depreciation | They’re devaluing your property too much, lowering your payment. | Request their full depreciation schedule and challenge unreasonable life expectancies for items. Provide receipts or photos to prove the original condition. |

| Policy Exclusion Applied | They claim a specific part of your policy excludes the damage. | Ask them to cite the exact policy language they are using. Often, their interpretation is overly broad. Consult a professional. |

| Incomplete Scope of Work | Their repair estimate leaves out necessary steps or materials. | Get detailed, line-item estimates from at least two reputable local contractors. Use these to show what’s missing from their scope. |

This table covers the initial pushback. Your next move is to make it official.

Writing a Formal Dispute Letter

Your first real move is to put your disagreement in writing. A formal dispute letter (or a well-documented email) is a critical piece of the paper trail. It shows State Farm you’re serious and forces them to respond on the record.

Keep it professional, factual, and organized. Leave the anger and emotion out of it; that won’t help. The goal is to present your case so clearly that they have no choice but to reconsider.

Make sure your letter includes:

- Your Claim Vitals: Start with your name, address, policy number, and claim number right at the top.

- The Money Discrepancy: State the amount State Farm offered and the amount you believe you are owed, based on your own estimates.

- A Point-by-Point Rebuttal: Go through the adjuster’s estimate and explain exactly where you disagree. Don’t just say it’s wrong; explain why. For instance, “Your estimate accounts for replacing the damaged hardwood, but it omits the necessary cost to sand and refinish the entire continuous floor to ensure a uniform match, as required by industry standards.”

- Your Evidence Packet: Attach everything. Include your photos, videos, personal property inventory list, and—most importantly—at least two detailed estimates from local, reputable contractors.

A strong dispute letter, backed by solid proof from independent experts, changes the conversation. It’s no longer their opinion versus yours; it’s their opinion versus documented, real-world facts.

Using the Appraisal Clause in Your Policy

If your letter doesn’t get you a fair revision, check your policy for a powerful but often-missed tool: the appraisal clause. This is a formal process built into most policies specifically to resolve disputes over the amount of loss.

Now, it’s critical to know what appraisal can and can’t do. It’s not for arguing about whether something is covered in the first place. It is only for when you and State Farm agree something is covered but can’t agree on the price to fix or replace it.

Here’s the typical process:

- You hire your own independent, competent appraiser.

- State Farm hires one.

- The two appraisers meet and try to hammer out an agreed-upon amount.

- If they can’t agree, they select a neutral third-party “umpire” who listens to both sides and makes a final, binding decision on the price.

Invoking appraisal can be a fantastic way to break a stalemate. One word of caution: be mindful of legal deadlines. In some states, the statute of limitations for filing a lawsuit can keep ticking even while you’re in the middle of appraisal.

Special Rules for NFIP Flood Claims

If your damage is from a flood and you have a National Flood Insurance Program (NFIP) policy, throw the standard playbook out the window. The rules are different and incredibly strict because these policies are federally regulated.

With an NFIP claim, you must file a formal “Proof of Loss” form within a specific window, usually 60 days from the flood date (unless FEMA grants an extension). If you disagree with their decision, you can either file an appeal directly with FEMA or file a lawsuit in U.S. District Court. The deadlines are absolute, so you have to move fast.

Challenging an insurance company takes patience and persistence. To dive deeper into strategies for when your claim gets flat-out rejected, check out our guide on how to appeal a denied insurance claim. Taking the right steps from the start can make all the difference.

Deciding to Hire a Public Adjuster

Trying to manage a major State Farm claim on your own can quickly feel like a second full-time job—one you never wanted and certainly didn’t apply for. While you can probably handle a small, straightforward claim yourself, there are times when the stakes are just too high and the process too complicated.

That’s where a public adjuster comes in. This is the point where bringing in a professional advocate isn’t giving up; it’s a smart, strategic move to protect your interests.

A public adjuster is a state-licensed insurance pro who works only for you, the policyholder. They’re not the adjuster State Farm sends out—that person works for the insurance company. A public adjuster’s one and only job is to make sure you get every single dollar you’re entitled to under your policy. They take over the entire headache, from documenting the loss and calculating its true value to going toe-to-toe with State Farm.

When to Seriously Consider a Public Adjuster

Look, not every little claim needs a public adjuster. But if your situation falls into one of these buckets, getting an expert in your corner can be the difference between a lowball offer and a fair settlement.

It’s time to call in a pro when:

- The Damage is Severe or Complex: We’re talking about a major house fire, catastrophic hurricane damage, or anything involving serious structural problems. Valuing these kinds of losses is a beast, and a public adjuster knows how to find and document damage the insurance company’s adjuster might miss.

- You Suspect Bad Faith: Is State Farm dragging its feet? Ignoring your calls? Making you jump through ridiculous hoops? Those are huge red flags. A public adjuster recognizes these delay-and-deny tactics and knows exactly how to fight back.

- You Just Don’t Have the Time or Energy: Let’s be real. Juggling a massive claim is exhausting, especially when you’re trying to run a business or just put your life back together. Handing it off to a professional lets you focus on what really matters.

A lot of policyholders aren’t sure if their claim is “big enough” to need help. That’s why we offer free, no-strings-attached claim reviews. The first step to a fair recovery is simply understanding where you stand and what your options are.

How Public Adjusters Are Paid

This is probably the first question everyone has, and it’s simple. Public adjusters work on a contingency fee basis.

What does that mean? They get paid a small, pre-agreed percentage of the final settlement they win for you. There are no upfront fees. They don’t get paid unless you get paid.

This setup puts you on the same team. Their success is tied directly to your success, so they’re motivated to fight for the maximum possible settlement.

Vetting and Choosing the Right Professional

Once you decide to get help, picking the right public adjuster is critical. You need someone with a license, real experience, and a solid reputation.

Here’s what to look for:

- State Licensure: Make sure they are actively licensed in your state (like North Carolina or Virginia). You can and should verify this on your state’s Department of Insurance website.

- Local Experience: An adjuster who knows local building codes, labor rates, and material costs will build a far more accurate and defensible estimate. Out-of-state storm chasers often get this wrong.

- Solid Reviews and References: See what past clients have to say. Check online reviews and don’t be afraid to ask for references from people who had claims similar to yours.

Be wary of anyone using high-pressure sales tactics or showing up at your door uninvited right after a disaster. A true professional offers expert guidance and gives you the space to make your own decision. To dig deeper into this, check out our guide on whether you should hire a public adjuster to see if it’s the right move for you.

Common Questions We Hear All the Time

When your property is damaged, your head is spinning with questions. It’s completely normal. We’ve been in this business a long time, and we’ve heard them all. Here are the straight-up answers to some of the most common questions homeowners and business owners ask about their insurance claim state farm.

How Long Is This State Farm Claim Going to Take?

Honestly, it depends. There’s no single timeline. A simple claim for a few blown-off shingles might wrap up in a couple of weeks. But if you’re dealing with a catastrophic fire or major hurricane damage, you’re looking at a marathon, not a sprint—it can easily take many months to get everything settled.

The two things that move the needle most are your documentation and your communication. The more organized and detailed you are from the very beginning, the fewer reasons you give the adjuster to drag their feet.

What’s This “Depreciation” on My Estimate, and How Does It Hit My Wallet?

Depreciation is just the insurance world’s way of saying your stuff gets less valuable over time due to age and use. How this affects your payout comes down to the kind of policy you have.

- An Actual Cash Value (ACV) policy pays you for what your damaged property was worth the second before the loss happened. It’s the replacement cost minus all that wear and tear.

- A Replacement Cost Value (RCV) policy is much better. State Farm will usually cut you a first check for the ACV. Then, once you actually go out, buy the new item, and show them the receipt, you can claim the depreciation they held back. That second payment is called recoverable depreciation.

Can I Start Fixing Things Before the State Farm Adjuster Shows Up?

You can—and you should—make immediate, “temporary repairs“ to stop the damage from getting worse. This is what insurers call your “duty to mitigate damages.” It means putting a tarp over that hole in the roof, boarding up a busted window, or calling a water extraction company to start drying things out.

But hold off on any permanent repairs. Don’t start tearing out walls or hiring a roofer to do the full replacement until after the adjuster has done their inspection and you have an agreed-upon plan. Make sure you photograph everything before you touch it and keep every single receipt for those temporary fixes; those costs should be part of your claim.

I Got a “Reservation of Rights” Letter. What Does That Mean?

When you get a “reservation of rights” letter in the mail, pay close attention. It’s State Farm’s formal way of telling you that while they’re going to investigate your claim, they are also reserving the right to deny it later on. This usually happens when they spot something that makes them question if your policy actually covers this specific type of damage.

It might be a standard procedure, but it’s also a big red flag. It tells you the insurance company is already looking for a way out. This is the moment when your documentation and communication need to be absolutely flawless.

This letter gives State Farm the legal cover to investigate without admitting they owe you a dime, even after they’ve spent time and money on your claim.

Q2: Does State Farm try to use their preferred contractor network to lowball my claim?

A: Yes. State Farm's preferred contractors may be financially incentivized to write estimates that align with the insurer's low valuation, potentially leading to cheaper materials or the omission of necessary repairs. Always get multiple independent estimates.

Q3: What is the first step I should take when State Farm sends me a formal claim denial letter?

A: Do not panic. The first step is to formally hire an independent Public Adjuster to review the denial letter, perform a fresh inspection, and prepare a documented, technical rebuttal based on policy language and engineering reports.

Q4: What specific policy types does State Farm offer, and how do they affect the claims process?

A: State Farm offers several policy types (e.g., HO-3, HO-5). The HO-5 (Comprehensive) may offer the best protection, covering all perils except those specifically excluded. Your Public Adjuster ensures the correct policy form's rules are applied to your claim.

Q5: How does State Farm's internal estimating software affect my final claim payout?

A: State Farm, like other insurers, relies on software (like Xactimate) that can be manipulated by their adjuster to use low labor rates, omit line items for code upgrades, or fail to account for local market costs, resulting in a significantly low initial offer.

Q6: How can a Public Adjuster prove to State Farm that my damage was "sudden and accidental" and not neglect?

A: A Public Adjuster counters the "neglect" argument by retaining forensic engineers or plumbing experts whose reports conclusively state the failure (e.g., burst pipe) was sudden and not the result of long-term poor maintenance.

Q7: What documentation is necessary to fight State Farm's undervaluing of my personal property (contents) loss?

A: You must maintain a detailed, itemized inventory list (brand, model, age, replacement cost) and provide a professional, line-by-line comparison of your valuation versus State Farm's low valuation, usually prepared by a Public Adjuster.

Q8: Should I use State Farm's photo documentation, or should I take my own evidence?

A: Always take your own meticulous, date-stamped, high-resolution photo and video evidence before any cleanup begins. The evidence you gather is solely for your benefit, whereas the insurer's photos are for their file.

Q9: How do I fight a State Farm claim denial if they rely solely on a single adjuster's opinion?

A: You fight this by obtaining an independent, expert opinion from a licensed structural engineer, contractor, or Public Adjuster, whose report will introduce contradictory evidence and expert analysis into the claim file.

Q10: Can State Farm force me to use Actual Cash Value (ACV) instead of Replacement Cost Value (RCV) for my contents?

A: State Farm typically pays the lower Actual Cash Value (ACV) initially. However, to get the full Replacement Cost Value (RCV) payout, you must purchase and submit proof of replacement within a specified time frame, a process your Public Adjuster manages.

Q11: What formal dispute mechanisms can I use to fight State Farm besides a lawsuit?

A: You can use the Appraisal Clause (if the dispute is only over the cost of damage) or file a formal complaint with your State Department of Insurance if State Farm exhibits unreasonable delay or bad faith claim handling tactics.

Q12: Does hiring a Public Adjuster mean I am suing State Farm?

A: No. Hiring a Public Adjuster means you are hiring a claims expert to negotiate and manage the dispute for you, avoiding the time and expense of litigation. A lawsuit is only necessary if negotiation and all other formal remedies fail.

Q13: How can I stop State Farm from dragging out the claim process through unnecessary delays?

A: Your Public Adjuster holds State Farm accountable by tracking all communication, citing state Fair Claims Settlement Practices Act timelines, and submitting all documentation via certified mail to maintain an undeniable, documented paper trail.

Q14: What is the Appraisal Clause, and is it a good tool for fighting State Farm?

A: The Appraisal Clause is a formal alternative dispute resolution process used when State Farm agrees the loss is covered but disagrees on the amount of the loss. It involves both parties hiring an appraiser and is often a faster route to resolution than litigation.

Q15: How does State Farm handle my claim if I have a mortgage on my damaged property?

A: State Farm often includes your mortgage lender's name on the settlement check. Your Public Adjuster helps you manage the process of getting the lender to endorse and release the funds so repairs can begin, which is often a significant point of delay.

Q16: Can a Public Adjuster get me more money for my claim than State Farm’s initial offer?

A: Yes, Public Adjusters consistently obtain settlements that are significantly higher than the initial lowball offer by ensuring the insurer pays for all structural damage, code upgrades, and full coverage for Additional Living Expenses (ALE) required by the policy.

Q17: What actions by State Farm would constitute a potential "bad faith" insurance claim?

A: Potential bad faith actions include unreasonable delays in processing your claim, refusing to provide a clear explanation for a denial, or failing to conduct a proper and timely investigation of the loss.

Q18: Does State Farm's handling of a previous claim affect how they treat my new one?

A: Yes. If State Farm has a history of denying or underpaying your previous claims, your Public Adjuster will leverage that pattern of behavior to argue for a fairer settlement and highlight potential bad faith concerns.

Q19: Can State Farm withhold payment for code upgrade costs (e.g., matching shingles) that are legally required?

A: State Farm is generally obligated to pay for code upgrades required to bring the damaged portion of your property up to current local ordinances, provided you have the necessary Ordinance or Law policy endorsement. Your Public Adjuster ensures this coverage is included in the claim.

Q20: Why is hiring a Public Adjuster considered the most effective way to fight a State Farm claim?

A: A Public Adjuster is the most effective way because they level the playing field by having the expertise to interpret the policy, the authority to submit an independent, documented estimate, and the experience to counter State Farm's internal claim defense strategies.

You can also report your displeasure of the way State Farm is handling your claim by reporting them to your state’s Department of insurance via, National Association of Insurance Commissioners (NAIC): Use the official state tool via the NAIC Consumer Information Source to locate your specific state regulatory division.

Trying to manage a major property damage claim on your own can feel like a second full-time job. If you’re stuck with a complicated claim, fighting a lowball settlement offer, or just need a professional advocate in your corner, the team at For The Public Adjusters, Inc. is here to help. We provide a no-cost claim review so you can understand your real options and fight for the fair settlement you deserve. Learn more and get the help you need today.

To report a new State Farm homeowners claim by phone, call 1-800-SF-CLAIM (1-800-732-5246), which is available 24 hours a day, seven days a week — including holidays. Have your policy number ready before you dial, because the representative will ask for it immediately, and fumbling to find it while you’re already stressed just slows everything down.

One thing most policyholders don’t realize is that calling that number connects you directly to State Farm’s intake team, whose job is to open the claim file — not to protect your interests or maximize your settlement. That’s a meaningful distinction. If the damage is significant or the cause of loss is anything other than completely straightforward, consider speaking with a public adjuster before or shortly after making that first call, so you go in knowing exactly what to say and what not to volunteer.