When people find out that public adjusters exist, after a bit of research they will ask themselves, “Should I hire a public adjuster?” When you’re dealing with a serious property damage claim, the decision to hire a public adjuster really comes down to a single question: Do you want an expert fighting in your corner?

A public adjuster is a state-licensed professional who advocates exclusively for you, the policyholder. Their job is to make sure you get a fair and full settlement from your insurance company, not a penny less.

What a Public Adjuster Actually Does for You

Think of an insurance claim like a high-stakes negotiation. Your insurance company has its own expert—the company adjuster—whose main job is to protect the insurer’s bottom line. Right away, the deck is stacked against you. A public adjuster is the pro you bring in to level that playing field.

They take over the entire claims process, lifting that massive weight of stress and confusion right off your shoulders. And it’s about a lot more than just filling out forms.

Your Advocate and Strategist

First things first, a public adjuster conducts their own deep-dive investigation into the damage. They’re trained to spot the things a company adjuster might conveniently overlook, like hidden water damage inside a wall or the subtle signs of smoke contamination that can linger for years. Their mission is to document the true scope of your loss.

They also handle the heavy lifting of the claim itself:

- Decoding Your Policy: They’ll tear through the fine print of your insurance contract, finding every bit of coverage you’re entitled to. This often includes things you’d never think of, like additional living expenses or money for code-compliance upgrades.

- Meticulous Documentation: They build an undeniable, evidence-backed case for your claim, complete with detailed estimates and inventories that leave no room for the insurance company to argue.

- Handling All Communication: All those phone calls, emails, and back-and-forth negotiations? They handle it all, so you don’t have to.

By representing your interests and yours alone, a public adjuster makes sure your claim is valued based on the real-world cost to make you whole again—not just the insurance company’s initial lowball offer.

Ultimately, a public adjuster is your strategist, your negotiator, and your advocate from start to finish. To get a closer look at how they work, you can learn more about what a public adjuster does for policyholders in our detailed guide.

When Do You Need to Call in a Public Adjuster?

Not every claim needs a public adjuster. A small leak under the sink? You can probably handle that yourself. But when does a simple claim turn into a high-stakes battle you can’t afford to lose? Knowing that tipping point is everything.

Think of it like this: you can handle a minor fender-bender with the other driver’s insurance company on your own. But if you’re in a multi-car pileup with serious injuries, you’re calling a lawyer. A public adjuster is that exact same kind of expert—but for property damage.

For Large and Complex Damage Claims

The most clear-cut time to hire a public adjuster is after a catastrophe. We’re talking about a house fire, a major hurricane, or a burst pipe that floods your entire first floor. These aren’t just claims; they’re logistical nightmares. The sheer amount of paperwork and documentation can bury a homeowner.

A big loss involves so much more than what you can see with your own eyes. A good public adjuster knows exactly where to look for the hidden costs the insurance company’s guy might “forget”:

- Smoke and Soot Contamination: After a fire is put out, tiny toxic particles get into everything—your HVAC system, your clothes, your furniture. Things that look fine are often a total loss.

- Hidden Water Damage: The water used to fight a fire or the rain from a hurricane doesn’t just disappear. It soaks into drywall, insulation, and subflooring, setting the stage for dangerous mold and structural rot.

- Code Compliance Upgrades: When you rebuild, you can’t just put things back the way they were. Your city will require you to bring things like electrical and plumbing up to today’s building codes. Your policy should cover these mandatory—and expensive—upgrades.

A major loss isn’t a simple insurance claim. It’s a forensic investigation. Every single detail has to be documented and proven to rebuild your life, and that takes an expert.

When Your Claim Gets Denied or Lowballed

Here’s the other big red flag: your insurer denies your claim or sends you a settlement offer that’s just plain insulting. That’s the moment you know you’re not on the same team. Their priority is their bottom line, not yours.

This is where a public adjuster becomes your most powerful weapon. They don’t just ask nicely for more money. They reopen the claim, conduct their own top-to-bottom investigation, and build a new, evidence-packed claim that the insurance company can’t ignore. They speak the same language as the insurer and know how to dismantle a weak denial or a lowball offer, forcing them back to the negotiating table on your terms.

The Real Financial Impact of Hiring an Expert

It’s easy to look at a public adjuster’s fee as just another expense. But that’s the wrong way to think about it. The fee is really an investment in your financial recovery, and the return on that investment can be massive.

It’s easy to look at a public adjuster’s fee as just another expense. But that’s the wrong way to think about it. The fee is really an investment in your financial recovery, and the return on that investment can be massive.

Think of it this way: a skilled public adjuster knows exactly where to look for hidden damages and how to interpret the fine print in your policy—the kind of stuff most homeowners would never even notice.

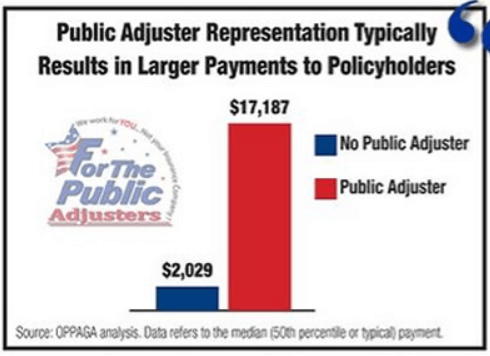

The numbers don’t lie. A landmark report from the Office of Program Policy Analysis and Government Accountability looked at over 76,000 claims. It found that when policyholders used a public adjuster, catastrophe payouts were an incredible 747% higher. For non-catastrophe claims, settlements were still 574% higher on average. You can read the report about how public adjusters boost settlements here.

“An expert’s negotiation can turn a lowball offer into a settlement that fully covers your losses.”

This isn’t just theory; it plays out in real-world claim scenarios every day.

As you can see, having a pro in your corner makes a huge difference, especially with large, denied, or stalled claims.

Turning Fees Into Net Gains

Even after you account for their fee, homeowners almost always walk away with significantly more money than they would have by going it alone.

Here’s how they do it:

- Deep Damage Audit: They uncover structural, smoke, and water issues that aren’t obvious to the untrained eye.

- Policy Expertise: They dig through your policy to find coverage for things like code upgrade requirements that can add tens of thousands to your claim.

- Skilled Negotiation: They know how to counter an insurer’s lowball offer with hard evidence, pushing for a settlement that reflects the true value of your loss.

We dive deeper into these points in our article on the benefits of hiring a public insurance adjuster.

Let’s run a quick example. Imagine your insurance company offers you an initial settlement of $50,000. It might seem like a decent amount, but you’re not sure if it’s fair.

You bring in a public adjuster who re-evaluates everything and negotiates the settlement up to $150,000.

After their 10% fee ($15,000), you pocket $135,000. That’s an extra $85,000 in your hands that you wouldn’t have had otherwise. The fee didn’t cost you money; it made you money.

Estimating Your Investment Return

So, what does that investment look like? Most public adjusters work on a contingency fee basis, which means they only get paid if you get paid.

Typically, their fee ranges from 5-20% of the final settlement amount. The exact percentage often depends on the size and complexity of your claim.

Let’s say your adjuster secures a $200,000 settlement. Here’s what your net payout could look like based on different fee structures:

- With a 5% fee: You keep $190,000.

- With a 10% fee: You keep $180,000.

- With a 20% fee: You keep $160,000.

Even in the highest-fee scenario, you’re walking away with $160,000 instead of the initial $50,000 offer.

When you look at it that way, it’s clear that the fee is a small price to pay for the expertise and advocacy that leads to a much, much larger recovery. A public adjuster’s fee isn’t a cost—it’s an investment in getting what you’re owed.

Understanding How Public Adjusters Get Paid

One question that comes up again and again is, “How much does a public adjuster cost?” Surprisingly, the fee structure is one of the biggest perks of hiring one.

Public adjusters work on a contingency fee basis. That means:

- You pay nothing out of pocket unless they win your claim.

- Their payment is a fixed percentage of the settlement they secure.

- If they don’t boost your payout, they don’t get paid, period.

This setup aligns their interests with yours. The better they negotiate on your behalf, the better their own return.

What Is A Typical Fee Structure

Public adjusters are upfront about their rates. The norm falls between 5% and 20% of the final settlement, with 10% being the most common. In many states, regulators even cap these percentages—especially after major disasters—to protect homeowners.

For a deeper dive into how these fees stack up, check out public adjuster fee structures at lopriore.com.

Their fee comes out of the settlement money they recover for you, not from your own savings. That keeps everyone focused on the same goal: maximizing your payout.

It’s also why a contingency model beats an “Assignment of Benefits” every time. To see why handing over your claim can backfire, read our guide on what an Assignment of Benefits is. With a contingency plan, your adjuster only succeeds if you do, making them a genuine partner in getting you the funds you deserve.

Let’s look at a quick example.

Here’s a side-by-side comparison of a hypothetical $100,000 damage claim:

Hypothetical Claim Settlement With vs Without a Public Adjuster

| Scenario | Initial Insurer Offer | PA-Negotiated Settlement | Public Adjuster Fee (10%) | Net to Homeowner |

|---|---|---|---|---|

| Without Public Adjuster | $60,000 | $60,000 | $0 | $60,000 |

| With Public Adjuster | $60,000 | $100,000 | $10,000 | $90,000 |

Even after the 10% fee, the homeowner nets $90,000—a 50% increase over handling the claim alone. That extra negotiating power can make all the difference when you’re rebuilding after a major loss.

How to Find and Vet a Reputable Public Adjuster

Once you’ve decided to bring in a public adjuster, the next step is the most important one: finding the right professional. This isn’t a decision to take lightly. Not all adjusters are created equal, and your choice here will directly impact the outcome of your claim.

Think of it like hiring a contractor to rebuild your home. You wouldn’t just hire the first person who knocks on your door. You’d want someone with a proven track record, a solid reputation, and total transparency.

Your search should always start with the basics. Any public adjuster you consider must be licensed, bonded, and insured in your state. This is non-negotiable. It’s your primary protection against fraud or incompetence. A reputable adjuster will have their license number ready to share, and you can usually verify it right on your state’s Department of Insurance website.

But a license is just the starting line. You need to dig deeper into their actual experience.

Key Vetting Checklist

As you start talking to potential adjusters, use this checklist to separate the pros from the rest:

- Relevant Experience: Have they actually handled claims just like yours? Someone who’s an expert in fire claims might not be your best bet for a complicated hurricane claim. Ask them to walk you through past cases that mirror your exact situation.

- Strong References: Don’t be shy about asking for a list of past clients, especially homeowners who have recently gone through the process. Talking to them gives you priceless insight into an adjuster’s communication, professionalism, and, most importantly, their results.

- Professional Affiliations: Are they part of any professional groups? Membership in an organization like the National Association of Public Insurance Adjusters (NAPIA) is a good sign. It shows they’re committed to ethical standards and staying on top of their game.

A great public adjuster won’t just tell you they can get results; they will show you. They should be able to provide clear evidence of their past successes and connect you with satisfied clients.

Critical Questions to Ask

Treat your first conversation like an interview—because that’s exactly what it is. You’re hiring a key member of your recovery team. Their answers to these questions will tell you everything you need to know.

- What is your exact fee structure and when is it paid? They should work on a contingency fee basis. If they ask for any money upfront, walk away.

- How will you communicate updates with me? You need to set clear expectations from day one. Will they call, email, or text? How often should you expect to hear from them?

- Who will be my primary point of contact? You want to know if you’ll be working directly with the experienced adjuster you’re talking to or if your case will be handed off to someone else in the firm.

Finally, trust your gut and watch for red flags. Be incredibly wary of anyone using high-pressure sales tactics, showing up at your door uninvited after a disaster, or demanding a large upfront payment. A true professional gives you the space and information you need to make a confident decision on your own time.

Common Questions About Public Adjusters

When you’re staring down a serious property damage claim, a few questions always bubble to the surface. Getting straight answers is the only way to feel good about your next move, so let’s get right into the most common ones.

Company Adjuster vs. Public Adjuster

So, what’s the real difference between the adjuster your insurance company sends out and a public adjuster you hire yourself? It all boils down to one word: loyalty.

The company adjuster is an employee of your insurance provider. Their job, first and foremost, is to protect the insurance company’s bottom line. They are legally and professionally bound to their employer’s interests, not yours.

A public adjuster, on the other hand, is a state-licensed advocate who works for you. Their only mission is to get you the best possible settlement allowed under your policy. One works for them; the other works for you. Simple as that.

This fundamental conflict of interest is the single biggest reason homeowners decide to bring in their own expert. You’re leveling the playing field with someone whose goals are perfectly aligned with yours.

Can You Hire an Adjuster After a Claim Denial?

Absolutely. A claim denial isn’t the final word—think of it as the insurance company’s opening offer in a negotiation. So many denials happen because of shaky evidence or a very narrow reading of the policy, which is exactly where a public adjuster shines.

Once you hire them, they get to work immediately:

- They demand your entire claim file from the insurance company.

- They launch their own independent, top-to-bottom investigation of the damage.

- They comb through your policy to find every bit of coverage the first adjuster might have overlooked.

- They package it all into a bulletproof new claim, armed with solid evidence, and formally reopen the fight.

Hiring a public adjuster gives you a powerful second chance to secure the payout you’re actually entitled to.

What if You Already Have a Settlement Offer?

It’s definitely not too late, especially if that offer feels low. If your gut is telling you the check they’re offering won’t even begin to cover the cost of repairs, that’s the perfect time to call in a professional.

A public adjuster will dissect the insurer’s offer and pit it against their own highly detailed damage estimate. If they find gaps—and they almost always do—they can reopen negotiations to fight for a supplemental payment. Their expertise helps them spot hidden costs the company adjuster might have conveniently ignored, ensuring the final number is what you truly need to recover.

Trying to navigate an insurance claim can feel like a full-time job you never wanted, but you don’t have to go it alone. The team at For The Public Adjusters, Inc. is here to provide the expert guidance and fierce advocacy you need to get a fair settlement. If you’re dealing with a difficult claim, reach out for a no-cost consultation. Learn more at forthepublicadjusters.com