The broad evidence rule is a legal standard that came out of the 1928 New York case McAnarney v. Newark Fire Insurance Co. and tells the decision-maker to consider “every fact and circumstance” that logically bears on value, not just replacement cost minus depreciation. For homeowners and business owners fighting a low Actual Cash Value offer, that rule matters because it gives you a real way to challenge a formula the insurance company may be using to push your claim down.

You're probably here because the carrier gave you an ACV number that feels detached from reality. The house was worth more than that. The building materials were better than that. The equipment was more useful than that. But the desk adjuster or field adjuster reduced everything to a depreciation spreadsheet and acted like the number was objective.

It often isn't.

When a property claim turns into a valuation fight, the broad evidence rule can shift the whole dispute. Instead of letting the insurer say, “Here's our formula,” you force the conversation toward, “Here is all the evidence that shows what the property was worth at the time of loss.” That's a very different fight, and it's usually a much stronger one for the policyholder who's prepared.

Table of Contents

- Your Claim Was Low-Balled Now What

- What Is the Broad Evidence Rule

- A Weapon Against Low-Ball ACV Offers

- The Broad Evidence Rule in Action with Examples

- How State Rules Impact Your Claim in NC and VA

- Your Battle Plan for Using the Broad Evidence Rule

- Claim Help to Fight Back and Get Paid Fairly

Your Claim Was Low-Balled Now What

A homeowner suffers a fire loss in the kitchen and part of the living area. The carrier's adjuster inspects, writes an estimate, applies steep depreciation to cabinets, flooring, trim, and built-ins, then sends over an ACV figure that doesn't come close to what it will take to recover. The policyholder looks at the number and thinks a common thought: “There's no way this is fair.”

That reaction is usually right.

The first mistake people make is assuming the insurance company's ACV number must be legitimate because it came from software, a report, or an adjuster with a title. But a low-ball offer often comes from a narrow method. The carrier starts with replacement cost, subtracts depreciation aggressively, and presents the result as if it's the only proper answer.

Why that offer feels wrong

It feels wrong because real property value isn't that simple. A house isn't just a line item in a spreadsheet. A business asset isn't just “old equipment.” The condition before loss, the usefulness of the property, the local market, the quality of construction, and the desirability of the asset all matter.

The insurer wants the valuation debate to stay mechanical. You want it to become factual.

That's where the broad evidence rule becomes useful. It gives you a framework to argue that the carrier can't lock the claim into one rigid formula if other evidence points to a higher and more accurate value.

What you should do immediately

If your ACV offer looks stripped down, don't argue in generalities. Start collecting proof.

- Request the valuation basis: Ask the insurer to identify exactly how it calculated ACV and what depreciation assumptions it applied.

- Pin down the disputed items: Find out whether the problem is condition, age, pricing, market value, or omitted features.

- Start building your own file: Photos, receipts, contractor opinions, maintenance records, appraisals, and comparable property information can all matter.

- Stop treating the insurer's number as the starting truth: It's only one position in a dispute.

A low ACV offer is not the end of the claim. It's the start of a valuation fight.

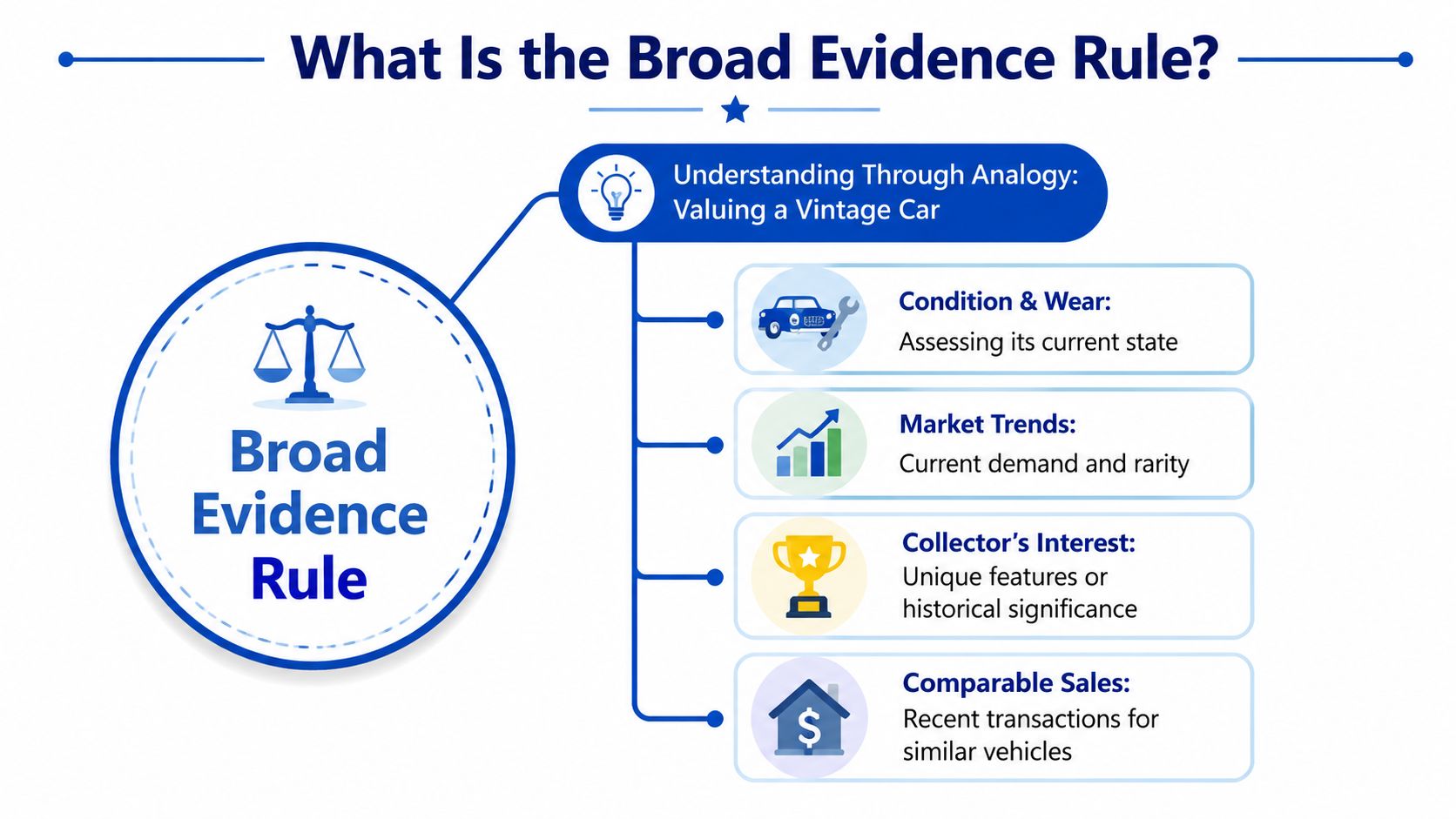

What Is the Broad Evidence Rule

The easiest way to understand what the broad evidence rule is is to stop thinking like an insurance spreadsheet and start thinking like a real buyer. If you were valuing a vintage car, you wouldn't use only original price minus wear. You'd look at condition, rarity, market demand, maintenance, upgrades, and what similar vehicles sell for.

Property claims work the same way when the broad evidence rule applies.

Why a single formula fails

A house can have older components and still carry strong real-world value. A commercial building can be dated on paper and still be highly functional, well-maintained, and attractive in its market. A replacement-cost-minus-depreciation formula may catch part of that picture, but it often misses the rest.

That's why the broad evidence rule matters. It allows the decision-maker to weigh multiple value indicators at once instead of treating depreciation as the whole story.

Some of the evidence that can matter includes:

- Market value: What similar property supports in the local market

- Replacement cost: What it would cost to repair or replace with like kind and quality

- Depreciation: Age and wear, but only as one factor

- Original cost and quality: What was installed and how it compared to ordinary materials

- Condition and maintenance: Whether the property was neglected or well-kept

- Location and use: How the property functioned before the loss and what utility it had

If you need a clear primer on ACV before tackling the dispute itself, review this breakdown of Actual Cash Value in insurance.

Where the rule came from

The rule didn't come from a blog, a claims memo, or an adjuster's opinion. It traces back to the 1928 New York Court of Appeals decision in McAnarney v. Newark Fire Insurance Co., which became the foundational case for modern ACV disputes. In that case, the court said the fact-finder should consider “every fact and circumstance” logically bearing on value rather than relying only on replacement cost less depreciation, as discussed in this analysis of total-loss damage and McAnarney.

Practical rule: If the insurer is valuing your loss through one narrow lens, but the law allows many lenses, your job is to force the full picture into the record.

That's the power here. The broad evidence rule doesn't guarantee a bigger settlement. It gives you the legal footing to prove why the insurer's shortcut is incomplete.

A Weapon Against Low-Ball ACV Offers

Insurance companies like clean formulas because formulas are easy to defend and easy to repeat. The problem is that easy for the insurer often means unfair for the policyholder.

What insurers often do

In an ACV dispute, the carrier often leans on one simple path. Start with replacement cost. Apply depreciation. Issue payment. If the insured complains, the adjuster points to age and wear and acts like the discussion is over.

That approach is convenient, but it can flatten important facts. It can ignore superior materials, unusually strong pre-loss condition, local demand, functional utility, and the fact that some property doesn't fit neatly inside a generic depreciation model.

Here's the cleaner comparison:

| Approach | What it focuses on | What it tends to miss |

|---|---|---|

| Rigid ACV formula | Replacement cost less depreciation | Market support, utility, condition, local value factors |

| Broad evidence rule | All relevant evidence bearing on value | Nothing is automatically excluded if it logically affects value |

How the rule changes the fight

The broad evidence rule is not fringe. It is described as the majority approach to determining ACV and is used by courts in nearly half of U.S. states, where the fact-finder considers all evidence that would logically help estimate the loss rather than one fixed formula, according to J.S. Held's discussion of indemnity and ACV calculations.

That matters because it changes the burden of the argument. Instead of debating whether the insurer depreciated your property too hard within its own formula, you attack the premise. You argue that the valuation method itself is incomplete.

If you're still sorting out how ACV differs from replacement cost coverage, this comparison of Actual Cash Value vs. Replacement Cost helps frame why insurers prefer the ACV side of the debate.

A low ACV offer often survives because the policyholder argues over the number. Strong disputes attack the method behind the number.

That's the tactical shift. Once the claim becomes an evidence fight instead of a formula fight, the insurer loses some control. The file starts to include appraisals, contractor opinions, market data, maintenance records, pre-loss photos, and other facts that are much harder to brush aside.

The Broad Evidence Rule in Action with Examples

Theory is useful. A claim file is better. The broad evidence rule becomes powerful when you can see how it works on actual property.

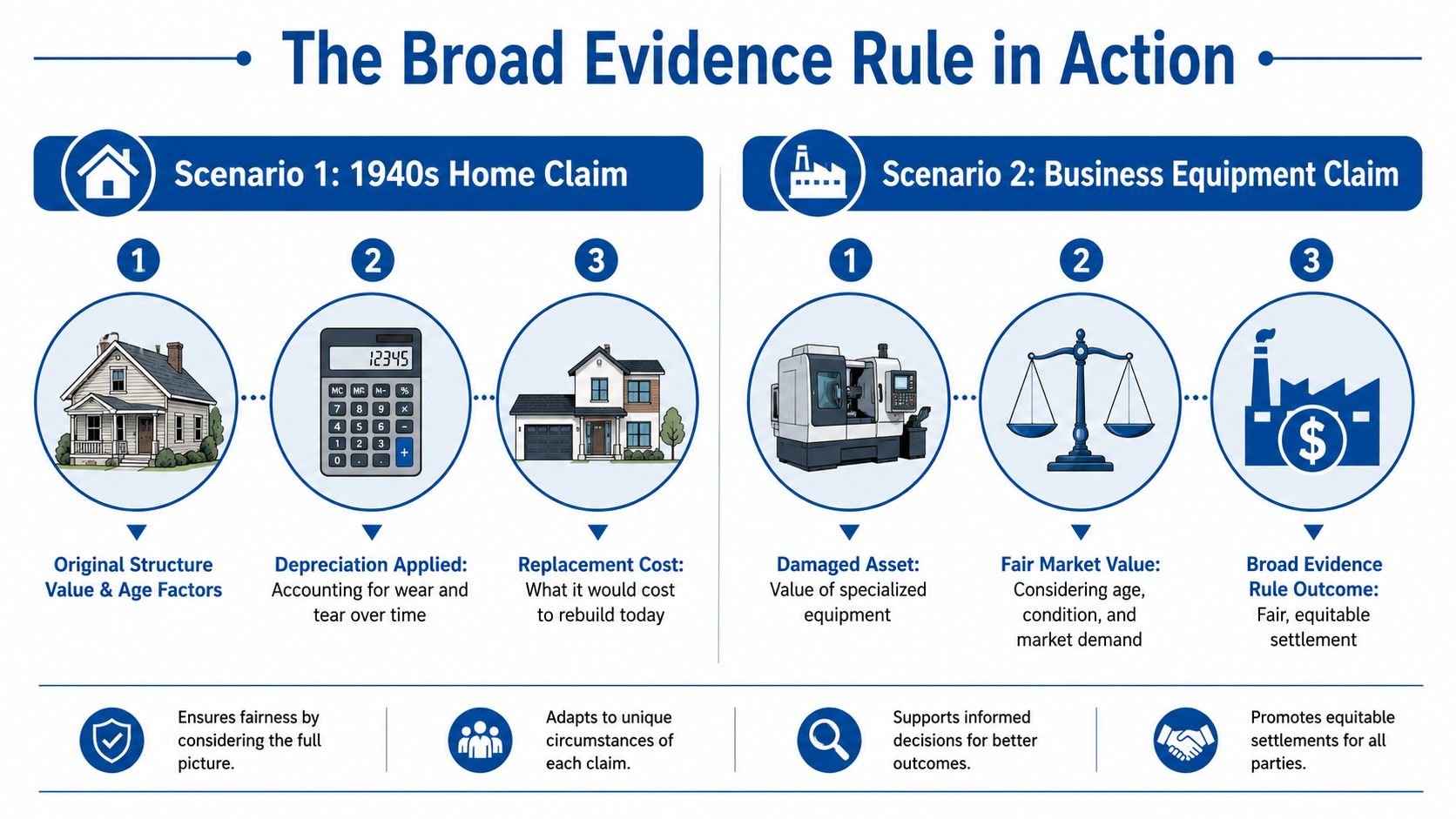

A historic home claim

A homeowner owns a house built in the 1940s. Fire damages several rooms. The insurer calculates ACV by pricing modern replacement materials, then applying depreciation based heavily on age. That produces a number that treats the house like any aging structure with old finishes.

But that isn't what the property was.

This home had plaster walls, original hardwood floors, custom millwork, and a level of workmanship that doesn't line up neatly with basic modern tract construction. The house also sat in an area where buyers specifically wanted older homes with original character. A blunt depreciation model ignored all of that.

A stronger broad-evidence argument would include:

- Pre-loss photographs: Showing the condition of finishes, trim, flooring, and built-ins

- Contractor opinions: Explaining the difference between replacing standard materials and matching older craftsmanship

- Market comparables: Supporting the desirability of similar homes in that neighborhood

- Maintenance records: Proving the property wasn't neglected

- Appraisal support: Giving context for quality, condition, and market appeal

The point isn't that every old house deserves a high ACV. The point is that age alone doesn't decide the question.

A business equipment claim

Now take a commercial bakery. A key oven is damaged. The insurer looks at age, applies depreciation, and says the equipment was old, so the ACV must be low. That might sound reasonable until you examine how the bakery operated.

The oven had been maintained, calibrated, and adapted for the business's production needs. It was central to output. It may have had features or modifications that made a generic used-equipment comparison weak or meaningless. A depreciated book-style value can miss functional reality.

A better claim presentation would gather evidence such as:

- Service and maintenance history: Showing the equipment was still productive and reliable

- Photos and operating records: Demonstrating actual pre-loss use and condition

- Replacement research: Identifying what a functionally equivalent unit would require

- Vendor input: Explaining custom features, installation demands, or scarcity

- Business-use evidence: Showing why this particular asset had real value to ongoing operations

The broad evidence rule works best when you stop describing property as old and start proving what it was worth in the real world.

These examples matter because homeowners and business owners often underestimate how much proof they already have, or how much additional proof they can gather once they know what the valuation fight is really about.

How State Rules Impact Your Claim in NC and VA

Not every state handles ACV the same way. That's one reason policyholders get blindsided. They assume there must be one national rule. There isn't.

North Carolina and Virginia are not identical

The broad evidence rule has historically remained less than majority rule, but it is still significant. One industry source says it is applied judicially in nearly half of the states, and another estimates that approximately 20 states had addressed the issue by adopting the rule in some form, as explained in this overview of the broad evidence rule trend in loss valuation.

That means two things. First, this is not some obscure doctrine. Second, you can't assume your state treats ACV exactly like another.

For North Carolina policyholders, that legal environment can be favorable when the claim facts support a broader valuation analysis. For Virginia policyholders, the practical question often becomes how local law, policy language, and claim facts line up in a specific dispute. Either way, broad-evidence arguments need to be built carefully and tied to the jurisdiction that controls the claim.

Why local strategy matters

A weak claim dispute sounds like this: “I think the offer is too low.”

A strong one sounds like this: “Your valuation ignores condition, market support, utility, and other evidence that matters under the governing framework.”

If you're trying to push back against an underpaid loss, start with a focused strategy for how to dispute a property insurance claim. General frustration won't move the file. Jurisdiction-aware evidence sometimes will.

- Policy language matters: Some disputes turn on whether ACV is defined or left open to interpretation.

- State law matters: Courts don't all treat valuation the same way.

- Claim facts matter: The better your proof, the more useful the broad evidence argument becomes.

This is why local claim handling isn't a detail. It's part of the valuation itself.

Your Battle Plan for Using the Broad Evidence Rule

Most policyholders lose ground early because they let the insurer define the claim before they build their own record. Don't do that. If ACV is disputed, your file needs to become a valuation package, not a complaint file.

Build your file before the insurer defines it for you

Start by forcing transparency. Ask for the full estimate, depreciation details, pricing support, photographs, and any valuation notes used to support the ACV number. If the carrier's calculation is weak, gaps will show up fast.

Then build outward.

Get the pre-loss story on paper

Write down the condition of the property before the loss. Include updates, maintenance, upgrades, special materials, business use, and anything unusual that gave the property added value.Gather visual proof

Photos and video taken before the damage can be decisive. Listing photos, renovation photos, leasing materials, inventory images, and social media posts can all help show condition and quality.Bring in outside experts when needed

A contractor can explain why the insurer's material assumptions are wrong. An appraiser can provide market context. On roof losses, a certified roof inspection can help establish condition, storm impact, and whether the carrier is minimizing damage.

Hard truth: If your evidence is thin, the flexibility of the broad evidence rule can work for the insurer too.

Evidence that moves an ACV dispute

Not all documents carry the same weight. Focus on evidence that speaks directly to value.

Repair and replacement estimates

These help show what like kind and quality means for your property, not a stripped-down substitute.Receipts and upgrade records

If you paid for better flooring, custom cabinets, specialty finishes, or business improvements, prove it.Market support

For homes, that may mean comparable sales or appraisal information. For businesses, it may mean vendor statements, equipment market information, or functional-equivalent replacement research.Maintenance and service records

These can undercut the insurer's favorite argument that the property was old and worn out.

One more point. Don't wait for the insurer to “reconsider” out of fairness. Claims move when evidence shifts the advantage. The broad evidence rule gives you the framework, but the paperwork gives it teeth.

Claim Help to Fight Back and Get Paid Fairly

The broad evidence rule can help policyholders. It can also become a mess if the insurer uses its flexibility better than you do. That's the part often overlooked.

Why this rule can help or hurt

The rule allows decision-makers to weigh “every fact and circumstance” affecting value, but that same flexibility can make results less predictable and harder to challenge. It has also been described as one of the hardest valuation standards to apply consistently, as noted in Investopedia's discussion of the broad evidence rule.

That means you cannot treat this doctrine like a magic phrase. Saying “broad evidence rule” won't fix a bad claim file. The rule only helps when you use it to present better proof than the insurer has presented.

Common mistakes include:

- Letting depreciation dominate the claim: Age matters, but it should not be the whole case.

- Failing to prove condition: If you don't document pre-loss quality and maintenance, the carrier will fill in the blanks its own way.

- Ignoring local market context: A house or building doesn't exist in a vacuum.

- Arguing emotionally instead of factually: Anger is understandable, but evidence wins valuation disputes.

What to do next if your offer is wrong

If your homeowner, dwelling, or business owner claim has been underpaid, denied, or dragged out, stop waiting for the insurer to correct itself. Review the estimate line by line. Demand support for the ACV calculation. Gather evidence that speaks to condition, utility, market value, and replacement reality.

Then push the dispute where it belongs. Not into a generic complaint about fairness, but into a documented challenge to an incomplete valuation method.

The broad evidence rule is powerful because it breaks the insurer's favorite shortcut. It tells the decision-maker to look at the whole picture. That's exactly what a frustrated policyholder needs when the insurance company is pretending the whole picture doesn't matter.

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your homeowner or commercial property claim has been low-balled, delayed, or denied, For The Public Adjusters, Inc. can help you challenge the carrier's valuation and document the full scope of your loss. They represent policyholders, not insurance companies, and they handle the hard part of the fight so you're not left arguing with an adjuster on your own.