You opened the claim because your house or building took real damage. Water spread behind baseboards. Wind tore up roofing. Fire left smoke, soot, and contamination where the carrier only wants to talk about what’s visible from the doorway. Then the insurance company sent an adjuster, gave you a number that doesn’t come close to putting the property back together, and acted like the file was basically done.

That’s the moment a lot of policyholders realize the process isn’t built around fairness. It’s built around control. The carrier controls the inspection, the scope, the estimate, the pace, and too often the story about what your damage is supposedly worth. If you’re searching for the benefits of hiring an independent claims adjuster, what you’re really asking is simpler: how do you stop getting pushed around and start fighting back?

Table of Contents

- Your Claim Was Low-Balled or Denied Now What

- The Adjuster Conflict of Interest You Must Understand

- How Public Adjusters Maximize Your Claim Payout

- Accelerate Your Settlement and End the Headaches

- Analyzing the Cost Versus the Financial Return

- How to Choose a Reputable Public Adjuster

- Special Claim Considerations for NC and VA Residents

- Take Control of Your Claim Dispute

Your Claim Was Low-Balled or Denied Now What

Start with this truth. A low-ball offer is not a final truth about your damage. It’s the insurance company’s position.

If your fire, water, wind, hail, hurricane, or storm claim came back short, stop arguing from memory and frustration alone. Get organized. Pull the policy. Save every email. Photograph every damaged area again. Keep receipts, mitigation invoices, contractor findings, and any reports that identify hidden damage or code-related repair needs.

Then change your mindset. You are no longer “checking on a claim.” You are building a dispute file.

Your next moves need to be deliberate

Here’s the order I recommend:

- Read the estimate line by line. Don’t focus only on the total. Look for missing rooms, omitted materials, and repairs that were downgraded instead of replaced.

- Compare the estimate to the actual condition of the property. If cabinets were detached but drywall behind them was wet, that matters. If smoke moved through the HVAC system, that matters.

- Document what was overlooked. Photos, moisture findings, contractor notes, and a written timeline all help.

- Bring in your own advocate. A public adjuster works for you, not the carrier, and that changes the whole fight.

Practical rule: If the insurance company’s number doesn’t rebuild the property to pre-loss condition under the policy, don’t accept it just because it arrived on official letterhead.

If you need a plain-English resource on how policyholders win fair settlements from adjusters, that guide is useful because it shows why documentation and negotiation matter after the first offer misses the mark.

A denied claim needs the same discipline. Read the denial language carefully. Carriers often rely on narrow interpretations, incomplete inspections, or sloppy cause-of-loss analysis. Don’t respond with outrage alone. Respond with evidence, policy language, and a professional claim presentation that forces a real review.

The Adjuster Conflict of Interest You Must Understand

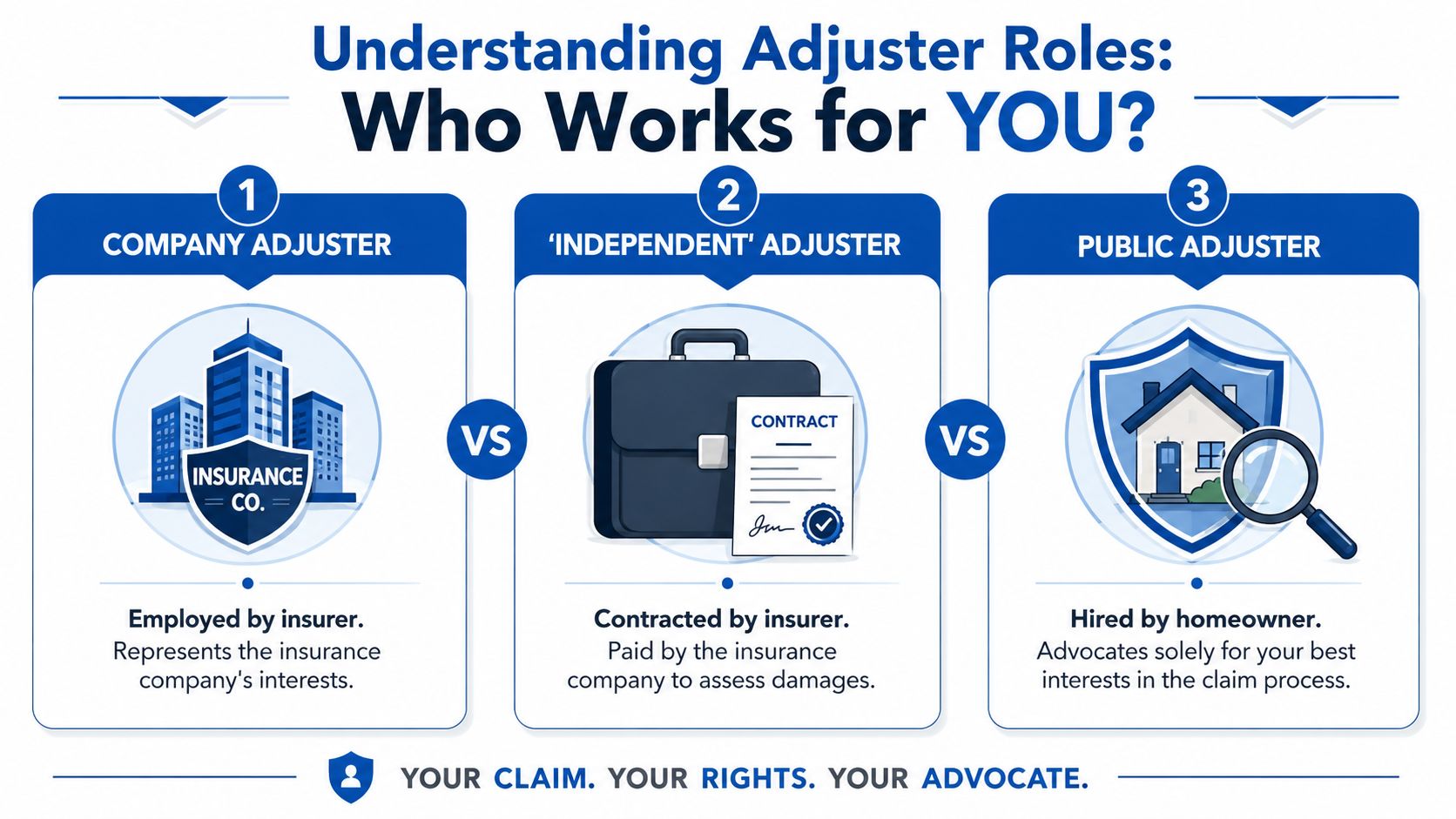

Most policyholders make one bad assumption at the start. They think an adjuster is just an adjuster.

That’s wrong. The title sounds similar, but the loyalty is completely different.

Three adjusters, three loyalties

A company adjuster is an employee of the insurance carrier. That person handles claims for the insurer and follows the insurer’s systems, procedures, and claim goals.

An independent adjuster sounds neutral, but the name fools people. An independent insurance adjuster is hired by the insurer on a contract basis to represent the insurance company’s interest in the settlement of a claim, and that adjuster owes a duty solely to the insurance company, not the policyholder or homeowner, as discussed in the Shlank v. explanation from Biller Law Group.

A public adjuster is the only adjuster in this group hired by the policyholder. That’s your side of the table.

If you want a deeper breakdown of the differences, this comparison of insurance adjuster vs public adjuster is worth reading because it strips away the marketing language and gets to the loyalty issue fast.

Who does your adjuster really work for

| Adjuster Type | Who Hires Them | Who They Represent | Primary Goal |

|---|---|---|---|

| Company Adjuster | Insurance company | Insurance company | Resolve the claim for the carrier |

| Independent Adjuster | Insurance company | Insurance company | Assess loss for the carrier on a contract basis |

| Public Adjuster | Policyholder | Policyholder | Document, present, and negotiate the claim for the insured |

That table should reshape how you handle every conversation going forward.

When the carrier says, “We sent an independent adjuster,” don’t hear “neutral expert.” Hear “outside contractor for the insurance company.” The paycheck tells you where the loyalty sits. So does the legal duty.

The insurer’s adjuster may be courteous, responsive, and experienced. None of that changes who they work for.

This is why the benefits of hiring an independent claims adjuster, as people often search it, are really the benefits of hiring a public adjuster for your own property claim. You need someone who can challenge scope omissions, pricing shortcuts, depreciation disputes, and coverage interpretations without worrying about pleasing the carrier that assigns work.

On homeowner claims, dwelling claims, and business owner property claims, that conflict matters from day one. It shapes what gets photographed, what gets measured, what gets omitted, and what gets paid.

How Public Adjusters Maximize Your Claim Payout

The biggest jump in claim value usually doesn’t come from slick negotiating. It comes from a better scope.

A public adjuster increases value by finding what was missed, tying it back to the policy, and presenting it in a format the carrier can’t brush aside. According to Investopedia’s explanation of independent insurance adjusters, hiring an independent public claims adjuster directly increases claim settlement values by 30–50% on average, and it addresses a documented gap where 22% of home claims are underpaid due to incomplete initial assessments.

That tracks with what happens every day on water, fire, and storm losses. The first inspection often captures the obvious. The second, more aggressive review captures the expensive part.

The money is in the scope

Take a water loss in a kitchen or bathroom. The carrier’s adjuster may write for visible drywall cuts, paint, and a few baseboards. A stronger claim review asks harder questions.

- What’s behind the wall? Water doesn’t stop where the stain stops.

- What about adjacent rooms? Moisture migrates.

- Were cabinets, insulation, flooring layers, or subfloor affected?

- Is there microbial growth or trapped moisture that changes the repair plan?

Public adjusters with IICRC-related knowledge on fire and water losses know how to inspect beyond the obvious. They work with moisture findings, scope details, mitigation records, and repair sequencing. That’s how hidden damage becomes documented damage.

If you’re trying to understand how contractors and policyholders build a stronger property claim record, this Restore Heroes Phoenix claim guide is useful background because it shows why early documentation and repair logic matter even before the dispute gets serious.

What a stronger documentation file looks like

A public adjuster’s file is usually stronger in four ways:

-

Policy interpretation

The adjuster reads what the policy owes, not just what the field estimate included. -

Detailed room-by-room scoping

Missing line items are where low-ball offers hide. -

Damage documentation tied to cause

If the loss caused the damage, the file needs to show that clearly. -

Negotiation backed by evidence

Carriers change position faster when the disagreement is documented, organized, and hard to dismiss.

A quick visual example helps:

This is why I tell people not to obsess over whether the company adjuster was “nice.” Nice doesn’t rebuild a house. Complete scoping does. Accurate estimating does. Pressure backed by evidence does.

Accelerate Your Settlement and End the Headaches

A bad property claim eats your time first, then your patience.

You call for updates. You leave voicemails. A new desk adjuster appears. The estimate gets revised, then stalled. A supplement is “under review.” The contractor says the carrier is missing obvious repairs. Meanwhile, your home is torn up or your business property can’t fully recover because the claim hasn’t moved.

What delays look like when you handle the claim yourself

Self-represented policyholders usually get buried in tasks they didn’t expect:

- Carrier communication loops that produce plenty of talk and very little movement

- Document requests that arrive in pieces instead of one clean list

- Estimate disputes over line items, pricing, and whether damage is related

- Scheduling drag when inspections, re-inspections, and reviews stretch out

None of that is accidental in effect, even if it’s presented as routine. Delay weakens policyholders. People get tired. They need money. They accept less just to move on.

What changes when a public adjuster takes over

A good public adjuster acts like a claim manager, not just a negotiator. They organize the file, submit the supporting material in a usable format, keep the carrier focused, and push the process toward decision points instead of endless drift.

According to Metro Public Adjustment’s discussion of the benefits of hiring an independent insurance adjuster, public adjusters eliminate time-to-resolution delays by 40–60% compared to self-represented claimants by using efficient documentation workflows and direct carrier communication channels that bypass common bottlenecks.

When the claim file gets cleaner, the excuses usually get weaker.

That speed matters on homeowner and business owner property claims. Faster settlement means repairs can start sooner. Contractors can work from a realistic scope. Business owners can stop living in limbo. Homeowners can stop chasing the claim every evening after work.

The benefits of hiring an independent claims adjuster aren’t just financial. They’re operational. You hand the paperwork fight, the follow-up burden, and the estimate war to someone who does this for a living.

Analyzing the Cost Versus the Financial Return

The most common objection is simple. “Why should I pay someone a percentage of my claim?”

Fair question. But it’s usually the wrong way to look at it.

Why the fee model matters

Public adjusters are commonly paid on a contingency basis. That means they get paid if money is recovered. Their compensation rises with the settlement, so their incentive is aligned with yours. On a $100,000 damage claim, a public adjuster’s fee is typically 10% to 30%, and their expertise often results in a higher total payout that exceeds that fee, leaving the homeowner with a greater net recovery, as described in this Reddit insurance discussion on hiring a public insurance adjuster.

That structure matters because the job isn’t just “making phone calls.” It’s measuring damage correctly, assembling support, interpreting the policy, rebutting weak positions, and negotiating from a documented claim file. If the adjuster fails, they don’t get rewarded for effort alone.

In some states, there are also specific rules. For example, Texas allows public adjusters to charge up to 10 percent of the total amount paid on a claim, and consumers have 72 hours after signing to cancel without penalty, according to the Texas Department of Insurance public adjuster guidance. The exact rules depend on the state, so read the contract before you sign.

A review that reflects what many clients feel

Here’s the sentiment I hear from clients all the time:

“I hated the idea of paying a fee until I saw how much the insurance company had left out. Once the claim was properly documented, the difference more than justified the cost.”

That reaction is common because most low-ball estimates don’t fail by a little. They fail in the scope, the sequencing, and the omissions. The fee only hurts if you assume the carrier’s original number was close to fair. In many disputed property claims, it isn’t.

If the claim is small and straightforward, hiring help may not make sense. If the claim is large, technical, delayed, underpaid, or denied, paying for professional representation is often the cheaper mistake than going alone.

How to Choose a Reputable Public Adjuster

Not every public adjuster is worth hiring. Some know how to sign files. Fewer know how to win tough ones.

Credentials are not optional

Claims adjustment is skilled work. The Kaplan Financial salary overview for claims adjusters notes that the median annual wage for claims adjusters, appraisers, examiners, and investigators in the U.S. was $76,790 in May 2024, with top adjusters earning over $100,000, which tells you something important. Real claim expertise has value, especially on technical property losses.

When you’re choosing a public adjuster for a homeowner, dwelling, or business owner property claim, look for this:

-

State license first

Verify the adjuster is properly licensed where your property sits. Don’t skip this. -

IICRC-related training for fire and water losses

On these claims, technical knowledge matters. Hidden moisture, smoke migration, and contamination issues don’t document themselves. -

Experience with your type of loss

Storm roof disputes, major water losses, fire claims, and commercial property claims all have different pressure points. -

A clear contract

Fee percentage, scope of representation, and cancellation rights should be understandable before you sign.

If you want a practical consumer guide, this article on should I hire a public adjuster is a useful checkpoint before making the decision.

Questions to ask before you sign

Don’t ask only “How much do you charge?” Ask better questions.

- Who will inspect my property and prepare the scope?

- How do you document hidden water, fire, or storm damage?

- Have you handled claims like mine before?

- What happens if the insurer denies part of the damage?

- How often will I get updates?

Hire the adjuster who can explain the claim strategy clearly, not the one who makes the biggest promise fastest.

A reputable public adjuster should sound organized, specific, and grounded in the property damage itself. If the conversation feels vague, move on.

Special Claim Considerations for NC and VA Residents

North Carolina and Virginia policyholders deal with a specific kind of mess after major storms. Wind damage, roof damage, interior water intrusion, and flood issues can hit the same property at once, and the claim often turns into an argument about what caused what.

Hurricane claims get messy fast

After hurricanes, insurers increasingly use independent adjusters to handle high claim volume in storm-prone regions like NC and VA, often prioritizing speed over accuracy, which leads to underpayments for homeowners, according to Pacesetter Claims on what an independent adjuster is.

That matters because rushed inspections miss things. Roof systems get under-scoped. Interior water paths get minimized. Matching issues, moisture migration, and business property impacts get treated like side notes.

If your property is headed toward repairs, choosing the right contractor matters almost as much as choosing the right claim advocate. This guide on North Carolina general contractor selection is worth reviewing before you commit to the rebuild side of the job.

For local claim help, many property owners start by looking for a public adjuster near me because regional storm patterns and carrier behavior do matter.

Flood claims are a different fight

Flood claims are not normal homeowners claims. They usually involve FEMA and NFIP flood coverage, and the adjusters may come through the NFIP or a Write Your Own company (WYO). That changes the rules, the paperwork, and the dispute process.

If your loss involves flood, get help from a public adjuster who understands NFIP claim handling. Don’t assume your standard homeowners policy will respond the same way. It won’t. These claims are technical, strict, and easy for policyholders to mishandle if they trust the first version of events coming from the assigned adjuster.

Take Control of Your Claim Dispute

You don’t have to accept a low-ball offer, a rushed inspection, or a denial that doesn’t hold up under scrutiny. On homeowner, dwelling, and business owner property claims, the key advantage comes from having someone in the fight whose job is to protect your side, not the carrier’s file.

A public adjuster levels the field. That’s the point. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

For homeowners and business owners dealing with fire, water, wind, hail, hurricane, tornado, theft, or vandalism damage, For The Public Adjusters, Inc. helps policyholders challenge underpayments, delays, and denials with no-cost claim reviews, detailed documentation, and direct negotiation support built around one mission: protecting the insured, not the insurance company.