You did what your policy required. You reported the damage, made yourself available, answered questions, and waited for the carrier adjuster to “review” everything. Then the letter came. Denied. Delayed. Or worse, approved for an amount so low it doesn’t come close to repairing your home or commercial building.

That’s where most policyholders get stuck. They assume the insurance company’s decision is final. It isn’t. If you need to dispute a claim in North Carolina or Virginia, you need to stop treating the insurer like a helpful partner and start treating this like a document fight. That’s what it is.

Big carriers know pressure works. They count on confusion, fatigue, and deadlines. They low-ball storm claims, argue over causation, hide behind vague policy wording, and drag out communication until the insured starts negotiating against themselves. If that’s happening to you, you’re not overreacting. You’re seeing the playbook.

Table of Contents

- Your Claim Was Denied – Now the Real Fight Begins

- Building Your Case – The Evidence Insurers Can’t Ignore

- The Formal Appeal – Writing a Demand Letter That Gets Results

- When to Call for Backup – Public Adjusters vs Attorneys

- Escalation Tactics When the Insurer Still Won’t Budge

- FAQ Your Top Questions on Disputing a Claim

Your Claim Was Denied – Now the Real Fight Begins

You open the letter and see a wall of policy language. Wear and tear. Exclusion. Limited coverage. No storm-created opening. Insufficient documentation. Partial payment. Different words, same message: the carrier wants to pay less.

That denial or low-ball offer isn’t the end of the claim. It’s the point where the file stops being routine and turns adversarial. State Farm, Allstate, and other big carriers know claimants often won’t push back hard enough. They know many homeowners are exhausted, displaced, or trying to keep a business running while arguing over line items and coverage wording.

Here’s what I’ve seen over and over. A storm hits. The insured reports roof, interior, or water damage. The carrier sends its adjuster. The inspection is rushed, key areas get missed, and the estimate comes back thin. Then the policyholder gets told the damage is old, cosmetic, excluded, or below deductible. If roof damage is part of your dispute, this guide to denied roof claims for homeowners is a useful outside reference because it breaks down the kinds of denial language carriers keep recycling.

The first denial letter is often drafted to discourage you, not to close the matter fairly.

Anger is justified, but anger alone won’t win. A phone call where you vent at the desk adjuster won’t move the file. Neither will a vague email saying you “disagree.” To dispute a claim effectively, you need proof, structure, and pressure. You need to answer every excuse with documentation the insurer can’t brush aside.

That changes the fight. Once you build a file that shows what was damaged, what the policy says, what the carrier ignored, and where their numbers fall apart, the insurer loses room to hide.

Building Your Case – The Evidence Insurers Can’t Ignore

Insurers win disputed claims by controlling the file. They document their version first, frame the cause their way, and wait for you to argue from memory. That is the delay, deny, and defend playbook.

Your job is to take control of the record.

Build a dispute file the carrier cannot shrug off

A complaint is not evidence. A tight file is.

Start one folder, digital and paper if possible, and keep every claim document in it from this point on. If your insurer stalls, changes adjusters, or starts rewriting what was said on prior calls, your file becomes your protection.

Include these items:

- A communication log with dates, times, names, phone numbers, email addresses, and a short note of what each person said

- Every estimate, coverage letter, reservation of rights letter, and payment breakdown from the carrier

- Your photos and video, sorted by room, slope, elevation, and date

- Receipts and mitigation invoices for tarping, drying, board-up, temporary repairs, pack-out, or emergency labor

- A damage timeline from the date of loss through each inspection, request, and insurer response

- Reports or written findings from roofers, contractors, engineers, mitigation companies, or other qualified experts

Keep it clean. Keep it organized. Keep it current.

In North Carolina and Virginia, that discipline matters more than policyholders realize. Carriers know many people will miss deadlines, lose paperwork, or submit half-finished support. They use those gaps to argue noncompliance, reduce scope, or claim they still do not have enough information to act.

Document the property like you are preparing for a fight

Take new photos even if you already sent some.

Insurer inspections often miss transition areas, secondary damage, attic evidence, underlayment issues, moisture spread, detached structures, and code-triggering conditions. You need wide shots that show location, close-ups that show damage detail, and date-stamped images that tie everything together. For roof losses, this homeowner’s guide to roof damage claims is a useful outside reference on what to photograph and preserve.

For interior water or storm claims, do not stop at the obvious stain. Photograph:

- ceiling and wall transitions

- baseboards and trim

- flooring edges and buckling

- insulation, decking, attic surfaces, or crawlspace conditions

- moisture meter readings if available

- temporary repairs and mitigation setup

If damage changes over time, document that too. Staining spreads. Swelling gets worse. Materials separate. A carrier that calls damage “minor” on day one will often have a harder time defending that position once the progression is documented.

Read the policy for pressure points

Many policyholders look at the deductible and the coverage limits, then stop. That is not enough. Read the full policy like the carrier’s denial depends on a few buried sentences, because it usually does.

Focus on these sections:

- Loss settlement language, especially actual cash value versus replacement cost

- Duties after loss, including notice, protection of property, records, inspection access, and sworn proof requirements

- Exclusions and exceptions, especially for wear and tear, repeated seepage, surface water, rot, and ensuing loss

- Endorsements that change the base form

- Appraisal provisions if the fight is mainly over price and scope, not coverage

Insurers often quote one clause and ignore the sentence right after it. Do not let them get away with that. If they rely on an exclusion, check for an exception. If they cite wear and tear, compare that claim to the physical evidence. If they say the damage is old, make them explain how old damage suddenly produced new interior staining right after a storm.

One rule matters here. Quote the policy exactly. Then match that language to the facts.

If you are dealing with sworn statement requirements or deadline-sensitive submissions, read this proof of loss guide for policyholders. Paperwork errors give carriers an opening they do not deserve.

Get outside support that exposes the low estimate

Carrier estimates often look polished. Plenty of them are still wrong.

A neat PDF does not prove the scope is complete. I have seen insurer estimates omit full roof sections, detachments, code items, overhead and profit, moisture work, insulation, paint across continuous surfaces, and tear-out needed to reach hidden damage. The formatting looks professional. The numbers still do not buy proper repairs.

Get outside support from people who know property damage and will put their findings in writing. Ask for specifics. Vague opinions do not move claim files.

What helps most:

-

Detailed repair scopes

Get line-item descriptions, material quantities, affected areas, and labor needed. Lump-sum bids give carriers room to dodge. -

Causation opinions tied to physical evidence

If the insurer says “wear and tear” or “not storm related,” your expert needs to explain why the observed damage pattern points to the reported loss. -

Moisture and hidden damage support

Water claims rarely end where the stain stops. Support for drywall, insulation, trim, flooring, subfloor, and microbial risk can change the value of the claim fast. -

Code and access requirements

If local code, matching issues, steep access, detach and reset work, or safety setup affect the repair, document it clearly. Carriers cut these items all the time.

Use state-specific pressure in NC and VA

North Carolina and Virginia policyholders should build the file with regulators and escalation in mind from the start.

In North Carolina, unfair claim settlement conduct can become part of the pressure if the carrier ignores facts, drags its feet, or refuses to explain its position clearly. In Virginia, the paper trail also matters because a vague objection gets ignored, but a documented pattern of delay, inconsistent positions, and unsupported scope cuts is harder to defend.

That means every request should be in writing when possible. Every missing line item should be identified. Every unsupported insurer conclusion should be challenged with documents, photos, and policy language. Do not ask the carrier to “take another look” in general terms. Tell them what they missed, where the support is, and what must be revised.

Practical rule: If the insurer makes a claim about cause, scope, price, or policy language, answer it with a document, a photo, a report, or the exact policy text.

Here’s a helpful explainer before the video below. You are not trying to drown the insurer in paperwork. You are building a file that makes continued underpayment look deliberate.

Strong evidence changes the power balance. Carriers do not pay more because a policyholder is frustrated. They pay more when their excuses stop matching the record.

The Formal Appeal – Writing a Demand Letter That Gets Results

You reported the loss, sent the photos, answered the questions, and waited. Then the carrier sent a denial, a thin partial payment, or an estimate so stripped down it barely covers cleanup. That is the insurer playbook in action. Delay the file, deny part of the damage, defend the shortfall. Your demand letter is where you stop reacting and start pinning them to the record.

Treat this letter like an evidence-backed business demand. It should be clear enough that a desk adjuster, supervisor, regulator, public adjuster, or lawyer can read it and understand two things fast. What the carrier got wrong, and what it must do to fix it.

What your letter must include

A strong demand letter usually includes:

-

Claim identifiers at the top

List the claim number, policy number, property address, date of loss, and assigned adjuster or examiner. -

A precise statement of the dispute

Identify the exact problem. Full denial, partial denial, missing rooms, low pricing, withheld depreciation, code items omitted, or unsupported causation position. -

A tight timeline

Show the key dates in order. Loss date, report date, inspections, requests for information, your responses, the carrier decision, and any periods of silence. -

Policy language that supports payment

Quote the actual policy wording that applies to the disputed issue. Coverage grant, loss settlement, replacement cost, ordinance or law, duties after loss, or exclusions the carrier is misreading. -

A focused evidence summary

Point to the documents that matter. Photos, contractor estimates, expert reports, invoices, drying logs, moisture readings, code citations, and a line-by-line comparison if the carrier estimate leaves out obvious damage. -

A specific demand

State the dollar amount owed if you have it. If the amount is still being finalized, state exactly what must be re-inspected, revised, or paid. -

A written response deadline

Give a firm date and require the response in writing.

Write it for the supervisor who gets copied later

Do not write a letter that sounds like you are begging for another look. Write one that shows the carrier’s position does not match the facts, the policy, or its own file.

That means specifics. If the insurer says the damage is wear and tear, quote that reason exactly and answer it with photos, a contractor report, prior maintenance records, or the carrier’s own inspection notes. If the carrier cut scope, identify the missing line items and the room or building component tied to each one. If the payment is short, say where the estimate is deficient and attach the support.

A simple format works well:

| Item | What to include |

|---|---|

| Carrier position | Quote the denial, limitation, or scope cut exactly |

| Why it is wrong | Match facts to policy language |

| Supporting proof | Identify estimate, photos, report, invoice, or code item |

| Action demanded | Reinspect, revise estimate, reverse denial, or issue payment |

In North Carolina, use the timeline aggressively. Reasonable communication and a reasonable explanation matter. If the carrier ignored your proof, changed positions without support, or sat on the file, say so plainly. Do not lecture. Document it.

In Virginia, the same rule wins. Vague complaints get parked. A clean demand letter with dates, policy language, and proof forces the adjuster to either address the dispute or expose that the file is being mishandled.

If you want a clear breakdown of who argues scope and valuation for policyholders during this stage, read the difference between an insurance adjuster and a public adjuster. It helps you decide whether to keep pressing alone or bring in professional help before the carrier hardens its position.

What to leave out

Bad demand letters give insurers room to stall. Cut anything that does not help prove coverage, scope, causation, or value.

-

Emotional blow-by-blow stories

Frustration is real, but long narratives bury the strongest points. -

Accusations you cannot prove

Do not throw around fraud or bad faith labels unless the record supports them. -

Loose admissions

Offhand comments like “some of it may have been old” can get pasted into the denial file. -

Random attachments

Send documents that support your position. Leave out clutter. -

Casual delivery

Email is fine if you can preserve the sent message, attachments, and any read receipt or portal confirmation. Keep a complete copy of everything.

A good demand letter changes the pressure. It tells the insurer you know the difference between a real dispute and a manufactured one, and you are building a record that can stand up in North Carolina or Virginia if the carrier keeps playing delay, deny, and defend.

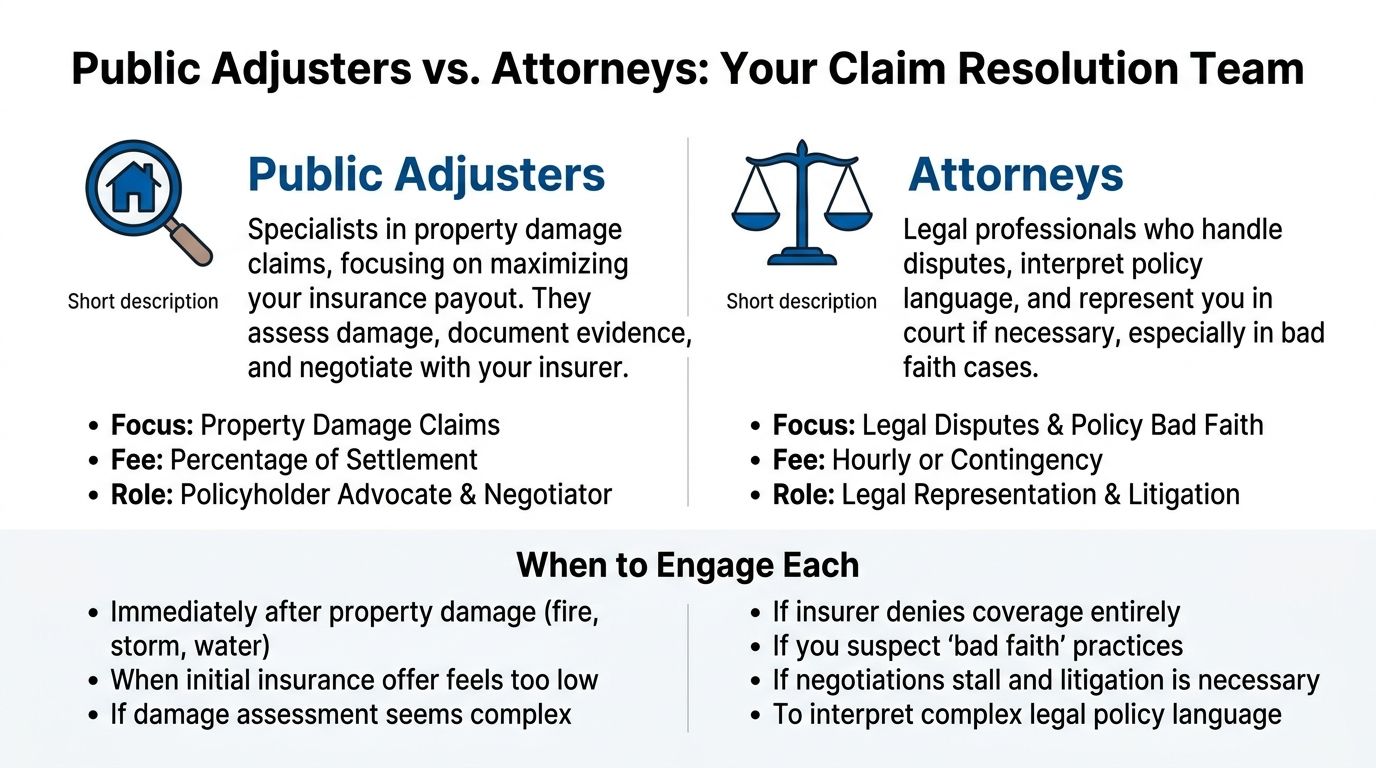

When to Call for Backup – Public Adjusters vs Attorneys

You submit photos, estimates, receipts, and a clean demand letter. The carrier answers with a new adjuster, a narrower scope, and another request for time. That is the point where many policyholders in North Carolina and Virginia lose months trying to out-wait a company that already chose its playbook. Delay, deny, defend.

The right response is to bring in the right professional, early enough to change the file before the insurer hardens its position.

They do different jobs

A public adjuster handles the property claim itself. They inspect the damage, build the scope, price the loss, organize proof, challenge bad causation calls, and negotiate with the carrier.

An attorney handles the legal fight. They step in when the dispute turns on policy language, legal deadlines, bad faith exposure, regulatory pressure, or litigation.

That line matters. A lot of policyholders hire a lawyer when the file still needs damage work, not court work. Others keep arguing scope on their own long after the carrier has shown it will not pay fairly without pressure.

Use this rule:

- If the core dispute is what was damaged, what caused it, and what it costs to repair, start with a public adjuster.

- If the core dispute is coverage law, bad faith conduct, suit deadlines, or a carrier that is openly preparing to defend in court, call an attorney.

Public adjusters and attorneys are not substitutes. In difficult files, they often work in sequence or side by side.

Choosing Your Advocate Public Adjuster vs Attorney

| Factor | Public Adjuster | Attorney |

|---|---|---|

| Primary focus | Property damage claims, scope, estimates, documentation | Legal disputes, policy interpretation, bad faith, lawsuits |

| Typical role | Policyholder advocate and negotiator | Legal representative and litigator |

| Best time to hire | Underpayment, denial support, reinspection, appraisal, complex damage valuation | Lawsuit posture, formal legal dispute, bad faith allegations |

| Evidence work | Heavy involvement in inspections, estimates, claim presentation | Uses evidence, but often after valuation record is built |

| Payment structure | Often tied to recovery structure permitted in the engagement | Often hourly or contingency, depending on matter |

If you need a clearer role-by-role breakdown, read this guide on the difference between an insurance adjuster and a public adjuster.

When a public adjuster is the smarter first move

Call a public adjuster if the insurer is using claims handling tactics to grind you down instead of dealing with the actual loss.

That usually looks like this:

- The estimate misses obvious work such as overhead items, code-related repairs, full-room finishes, moisture-related damage, or demolition needed to reach hidden damage.

- The carrier twists causation into wear and tear, maintenance, settling, or pre-existing damage without a solid inspection record.

- You keep getting passed around to new desk adjusters or outside vendors and nobody takes ownership of the file.

- The insurer is slow-walking the claim with repeated requests, partial answers, or inspections that never lead to a fair number.

- The amount of loss is the core dispute and the file needs a serious valuation record before appraisal or further escalation.

Policyholders in NC and VA make a costly mistake. They assume delay means the insurer is still considering the claim in good faith. Usually, delay means the carrier is testing whether you can build a stronger file than they can defend.

A good public adjuster changes that math.

When you need an attorney

Bring in an attorney when the case has moved past claim presentation and into legal exposure.

That includes:

- Coverage denials that turn on policy interpretation

- Threats of litigation or a clear litigation posture from the carrier

- Possible bad faith or unfair claims handling issues

- Approaching suit limitation deadlines or other legal deadlines

- A need for formal legal demands, regulatory strategy, or court action

In North Carolina and Virginia, deadlines and legal posture matter. Wait too long, and you hand the insurer another advantage. If you are near a limitation period, stop trying to salvage the file alone and get legal advice fast.

The practical call

If the insurer is underpaying, stripping scope, disputing causation, or dragging out the adjustment, a public adjuster is usually the right first call.

If the insurer has planted its flag on a legal denial, ignored strong evidence for too long, or forced the dispute into a legal corner, an attorney needs to protect your position.

For example, a property-focused advocate can inspect, document, prepare estimates, and negotiate directly with the carrier. That’s the lane firms such as For The Public Adjusters, Inc. work in for residential and commercial property losses in North Carolina and Virginia.

The experience of actual clients matters too, especially when you’re deciding whether to bring in help after months of stalling.

North Carolina Case Study: Disputing an Underpaid Storm Claim

After a severe storm in North Carolina, a homeowner reported roof damage, interior water staining, and damage to several rooms below the impact area. The carrier opened the claim, sent an adjuster, and issued a partial payment that barely addressed the visible exterior damage. The estimate looked official, but it left out the real cost of restoring the property.

The first carrier scope missed several important items, including:

- Interior drywall and paint repairs in affected rooms

- Wet insulation removal and replacement

- Moisture-related damage around trim and flooring

- Additional roof components needed for a proper repair

- Emergency mitigation and temporary protection costs

- Overhead, access, and labor required to complete the work correctly

The insurer suggested that some of the damage was pre-existing and that other items were outside the approved scope. From the homeowner’s perspective, the claim had technically been “approved,” but the payment was nowhere near enough to complete the repairs.

The real dispute was not whether a storm happened. The real dispute was whether the insurance company had acknowledged the full scope of covered damage.

Once the file was reorganized with photos, repair estimates, moisture documentation, and a clearer line-by-line challenge to the carrier’s estimate, the dispute became much harder for the insurer to dismiss. The missing items were tied directly to the reported loss, and the carrier was forced to answer specific scope and valuation problems instead of relying on vague explanations.

This is why policyholders in North Carolina should not treat a partial payment as proof that the claim was handled correctly. A claim can be open, accepted, and still badly underpaid.

North Carolina Policyholder Review After a Disputed Claim

“We thought the insurance company was going to handle our storm damage fairly because they accepted part of the claim. Then we saw the estimate and realized it did not come close to covering the actual repairs. Every time we asked questions, we got vague answers about exclusions, prior damage, and what the adjuster thought was reasonable.

For The Public Adjusters helped us understand the difference between a payment and a fair settlement. They reviewed the estimate, documented what was missing, organized the photos and contractor information, and pushed back on the carrier’s low scope.

The biggest relief was having someone who knew how to speak the insurance company’s language and challenge the file with facts instead of frustration. We finally felt like the claim was being taken seriously.”

— Jim s. Cary, NC

A review like this reflects what many policyholders experience after a denial, delay, or low-ball offer. The problem is not always that the insurer refuses to pay anything. Sometimes the problem is that the insurer pays only the smallest version of the loss and waits to see whether the policyholder knows how to fight back.

If the insurer has turned your claim into a grind, stop waiting for voluntary fairness. Put a professional between you and the carrier’s playbook.

Escalation Tactics When the Insurer Still Won’t Budge

Some carriers ignore a strong rebuttal letter because they’re testing whether you have another move. You do.

Use the appraisal clause when value is the fight

If the claim is really about the amount of loss, not whether a covered event happened at all, appraisal can be one of the most effective pressure points in a property claim. Many policyholders never use it because the insurer never volunteers it.

Appraisal is not the same as a lawsuit. It is a policy-based dispute process for valuation disagreements. It can force movement when the desk adjuster keeps circling the same low number.

Before invoking appraisal:

- Read the clause carefully in your policy.

- Confirm the dispute is valuation-driven, not purely a coverage denial.

- Make sure your estimate is complete, because weak numbers stay weak in appraisal.

- Get guidance on the role of the appraiser so you don’t step into the process blind.

If you’re trying to understand that role better, review this explanation of an insurance appraiser. Many insureds wait too long to consider appraisal and spend months re-arguing a number the carrier already decided to defend.

File the regulatory complaint and tighten the pressure

If the carrier is not communicating properly, keeps changing explanations, or fails to address evidence you submitted, a complaint to the appropriate insurance regulator can help tighten the file. It won’t solve every dispute, but it creates another layer of accountability and forces the carrier to respond more formally.

That matters when the insurer has been playing loose with timelines, explanations, or claim handling.

A complaint should be concise. Attach your timeline, identify the disputed conduct, and include the key correspondence. Don’t dump your entire file without context. Make it easy for the regulator to see the pattern.

Watch for procedural traps

A lot of bad claim outcomes are not about the merits of the damage. They happen because the insurer turns procedure into a weapon. Technical denials based on missed deadlines, incomplete forms, or other procedural issues are a real problem, and this discussion of insurance coverage disputes and technical denials describes how carriers use those rules to slow the process and pressure policyholders into lower settlements.

That means you need to be obsessive about the basics:

- Check every deadline for proof of loss, document submission, inspection access, and appeal response.

- Confirm receipt of everything you submit.

- Answer the actual request made by the insurer, not the version you assume they meant.

- Keep copies of signed forms and attachments in one dispute folder.

Here’s the hard truth. Carriers love procedural mistakes because they let the insurer avoid the central question: what is the covered damage worth? Don’t give them that opening.

If the insurer still won’t move after appraisal, regulatory pressure, and a fully documented rebuttal, then it may be time to get legal counsel involved and evaluate litigation, mediation, or other formal remedies. At that stage, your earlier documentation becomes the foundation of the entire case.

FAQ Your Top Questions on Disputing a Claim

Can I be dropped for disputing a claim

You open the denial letter, push back, and then a new fear hits. If I fight this, will the insurer cancel me next.

That fear keeps a lot of policyholders quiet. Carriers know it. Silence is useful to them.

Here is the practical answer. You have every right to dispute a bad claim decision. In North Carolina and Virginia, the bigger danger is accepting a low payment or wrongful denial and paying the repair bill yourself. Stay professional, keep everything in writing, and force the carrier to respond to the facts. Don’t hand them an excuse by missing deadlines or going off-message.

Do public adjusters charge upfront

Usually, no.

Many public adjusters work on a contingent fee set by the contract and limited by state rules, which means the fee is tied to what they recover for you. That is very different from paying hourly from day one. Read the agreement line by line before you sign. Ask three direct questions: What percentage is the fee, does it apply only to new money recovered, and what happens if you end the contract early.

If the adjuster gets vague, walk away.

How long should I keep fighting

Keep fighting while the claim file supports your position and the clock has not run out.

Insurers use delay, deny, and defend because it works. People get tired. Contractors want answers. Families want normal life back. Business owners need the doors open. The carrier knows pressure breaks people faster than bad facts do.

In North Carolina, claims handling rules exist for a reason, and as noted earlier, they can help expose slow responses, weak investigations, and unfair settlement conduct. In Virginia, the same basic principle applies. A carrier that knows you understand deadlines, documentation, and escalation options is harder for them to ignore.

What if my claim is for a business property

Commercial claims are where insurers find extra room to cut scope, question pricing, and drag out decisions.

A business property file can involve building damage, inventory, equipment, tenant improvements, code upgrades, and income loss issues all at once. One missing record can turn into weeks of delay. One vague estimate can give the insurer room to discount the entire loss. If this is a commercial claim, treat the dispute like a case file, not a conversation.

What about FEMA and NFIP flood claims

Flood claims are a different animal.

If your loss falls under FEMA or NFIP flood coverage, expect strict forms, strict deadlines, and very little flexibility. These claims can collapse over paperwork mistakes that would never matter in a standard homeowners claim. A bad proof of loss, a missed deadline, or incomplete support can kill recovery fast.

Get help early if the flood claim is denied, underpaid, or stalled. Waiting usually makes it worse.

Should I still dispute a claim if the insurer paid something

Yes.

Partial payment is one of the oldest moves in the insurer playbook. It creates the impression that the claim was handled fairly, even when major line items were cut, damage was missed, or parts of the loss were pushed into exclusions. If the money does not cover proper repair or replacement under the policy, the dispute is still alive.

A check is not the final word. The policy is.

If you need homeowners, dwelling, or commercial property claim help in North Carolina or Virginia has been denied, delayed, or low-balled, For The Public Adjusters, Inc. offers policyholder-side help with inspections, documentation, estimate review, and negotiation. If you’re tired of the carrier’s runaround, get the file reviewed before another deadline slips by.