Actual Cash Value (ACV) and Replacement Cost Value (RCV) are two different ways insurance companies calculate what they will pay after a loss.

Actual Cash Value (ACV) is the current value of your property after depreciation is applied for age, wear, and condition. In simple terms, it reflects what the item was worth immediately before the damage occurred.

Replacement Cost Value (RCV) is the cost to repair or replace your damaged property with a new item of similar kind and quality at today’s prices, without deducting for depreciation.

This is the fight behind actual cash value vs replacement cost. One valuation method helps restore the property. The other gives the insurance company room to cut your claim down with depreciation, delay, and technicalities. Here’s how the two compare in a claim:

1. Actual Cash Value (ACV)

Definition: Replacement Cost minus Depreciation.

How it works:

If a 5-year-old couch is destroyed, ACV coverage pays what that used couch was worth at the time of the loss—not what it costs to buy a new one today.

Pros:

- Lower insurance premiums

-

Less expensive coverage overall

Cons:

-

Payouts are often much lower than the actual replacement cost

-

You may have significant out-of-pocket expenses to replace damaged items

2. Replacement Cost Value (RCV)

Definition: The amount needed to repair or replace damaged property with materials or items of like kind and quality at current market prices.

How it works:

If that same 5-year-old couch is destroyed, RCV coverage pays what it would cost to purchase a brand-new comparable couch today.

Pros:

-

Better financial protection

-

Helps restore your home and belongings without large personal expenses

Cons:

-

Higher monthly insurance premiums

Real-World Example: A 5-Year-Old TV

Imagine you purchased a television five years ago for $1,500.

-

Today, its depreciated value is only $500

-

A comparable new television now costs $1,200

With ACV coverage:

You would receive approximately $500 (minus your deductible). You would need to pay the remaining $700 out of pocket to replace the TV.

With RCV coverage:

You would receive approximately $1,200 (minus your deductible), allowing you to replace the television with a new equivalent model.

How RCV Claims Are Typically Paid

Many insurance companies pay RCV claims in two stages:

-

The insurer first issues the Actual Cash Value (ACV) payment upfront.

-

After you repair or replace the damaged item and provide receipts, the insurer releases the remaining amount, commonly referred to as recoverable depreciation.

This process allows the insurance company to confirm the repairs or replacements were completed before paying the full replacement cost.

The storm passed. The fire department left. The mitigation crew tore out the wet drywall or the burned debris. Then the insurance company sent its number, and the number didn’t come close.

At that point, most homeowners and business owners in North Carolina and Virginia realize the true conflict is beginning. The carrier adjuster speaks as if the policy is simple math. It isn’t. It’s about bargaining power. They use terms like actual cash value and replacement cost to make a low offer sound legitimate, even when the check won’t put the property back the way it was.

If you are facing a settlement that fails to cover your roof, interior repairs, belongings, or business property, your confusion does not stem from a personal oversight. This uncertainty exists because policy language is structured with that complexity in mind. Carriers like State Farm and Allstate recognize that policyholders rarely study valuation clauses until after a loss occurs. By that point, the insurer already holds the advantage.

Table of Contents

- Introduction The Low-Ball Offer That Starts the Real Fight

- The Two Valuation Methods Insurers Use Against You

- ACV vs RC The Financial Impact on Your Claim

- How Insurers Use Depreciation to Deny and Diminish Claims

- Decoding Your Policy Fine Print That Can Cost You Thousands

- Real-World Battles Case Studies in Fighting Valuation Disputes

- Your Battle Plan Disputing Undervalued Claims and Getting Paid

- Frequently Asked Questions About ACV and RCV Claim Disputes

- Can I upgrade my policy from ACV to RCV

- My roofer says the roof must be replaced, but the insurer is paying ACV because of age

- My replacement cost policy still paid me on an ACV basis first. Is that allowed

- My business policy mentions functional replacement cost. What is that

- Should I accept the first offer if I need money quickly

Introduction The Low-Ball Offer That Starts the Real Fight

You paid premiums for years. Then a windstorm tears up your roof, or a pipe bursts and ruins floors, cabinets, drywall, and contents. The insurance company inspects, disappears for a while, and sends a figure that feels insulting.

That low number usually isn’t random. It often starts with actual cash value, not the amount it takes to rebuild or replace with materials of like kind and quality. The carrier deducts for age, wear, condition, and whatever else it can fit under “depreciation.” Suddenly the check looks less like protection and more like a partial contribution.

I’ve seen this pattern over and over. The policyholder thinks, “There has to be some mistake.” The insurer acts like the offer is objective. It usually isn’t. It’s a positioning move. They want you tired, rushed, and uncertain enough to cash the check and move on.

Practical rule: If the insurance number won’t restore the property or replace what was lost, treat the first offer as the start of negotiation, not the finish line.

The ugly truth is simple. Insurers love ambiguity when it cuts their payout. The fight over actual cash value vs replacement cost is one of the most common ways they underpay homeowners, dwelling owners, and business owners after fire, water, wind, hail, and storm losses.

The Two Valuation Methods Insurers Use Against You

Insurers present ACV and RCV as routine claim terms. They are payout tools, and the carrier chooses the one that saves it money whenever the policy language gives it room.

Replacement cost is the standard policyholders expect

Replacement Cost Value, usually called RCV or RC, is the cost to repair or replace damaged property today with materials of like kind and quality, without subtracting depreciation. That is the figure homeowners and business owners usually expect after paying premiums year after year.

If a storm tears up a roof, replacement cost is what a comparable roof costs now. If water destroys cabinets, flooring, or fixtures, replacement cost is what those items cost now in your market, not what they were worth after years of use.

Carriers still find ways to squeeze this coverage. Many policies let them issue an initial payment on an ACV basis and hold back the rest until repairs are completed and documented. In North Carolina and Virginia, that holdback turns into a pressure tactic fast. The insurer knows many policyholders do not have the cash to front repairs while waiting for money already owed under the policy.

Actual cash value is where underpayment starts

Actual Cash Value, or ACV, usually means replacement cost minus depreciation. That simple formula gives the insurer room to argue over age, condition, useful life, prior wear, and whether an item should be valued as old instead of serviceable.

This is the core of the fight over actual cash value vs replacement cost.

On paper, ACV sounds reasonable. In a live claim, it is often the carrier’s first and favorite discount. A roof that was fully functional the day before the storm gets priced like it was halfway to the dump. Flooring that matched the home gets treated like used material with little value. Business property gets hit the same way. Fixtures, equipment, and inventory can be discounted until the payout no longer comes close to what replacement costs.

That gap is not an accident. It is how insurers shift part of the loss back onto you.

The policy rarely values every category the same way

Many policyholders assume replacement cost applies across the board, but it often does not. The dwelling may have replacement cost, while contents are paid on an ACV basis. A commercial policy may value the building one way and business personal property another. Roof endorsements, cosmetic damage limitations, scheduled property terms, and loss settlement provisions can strip out replacement benefits.

That is why you need to read the loss settlement language, not the marketing summary.

Start with these questions:

- Which property is paid at ACV only: Roof surfaces, contents, flooring, fixtures, equipment, and inventory are common trouble spots.

- Which benefits are recoverable only after repairs: If depreciation is held back, find out exactly what documents, deadlines, and repair steps the carrier will demand before releasing it.

- Which endorsements cut down replacement coverage: Roof payment schedules, actual cash value endorsements, and special limits often do the damage.

- Which definitions give the insurer wiggle room: Terms like depreciation, like kind and quality, actual cash value, and comparable material matter more than policyholders are led to believe.

If you are in NC or VA, do not let the adjuster keep this discussion vague. Ask where the policy grants ACV treatment, where it grants replacement cost, and where the company claims a right to withhold depreciation. Make them point to the exact policy language. If they cannot do that cleanly, push back hard.

The carrier already mapped out the cheapest reading of your policy. Your job is to force them to justify every deduction in writing.

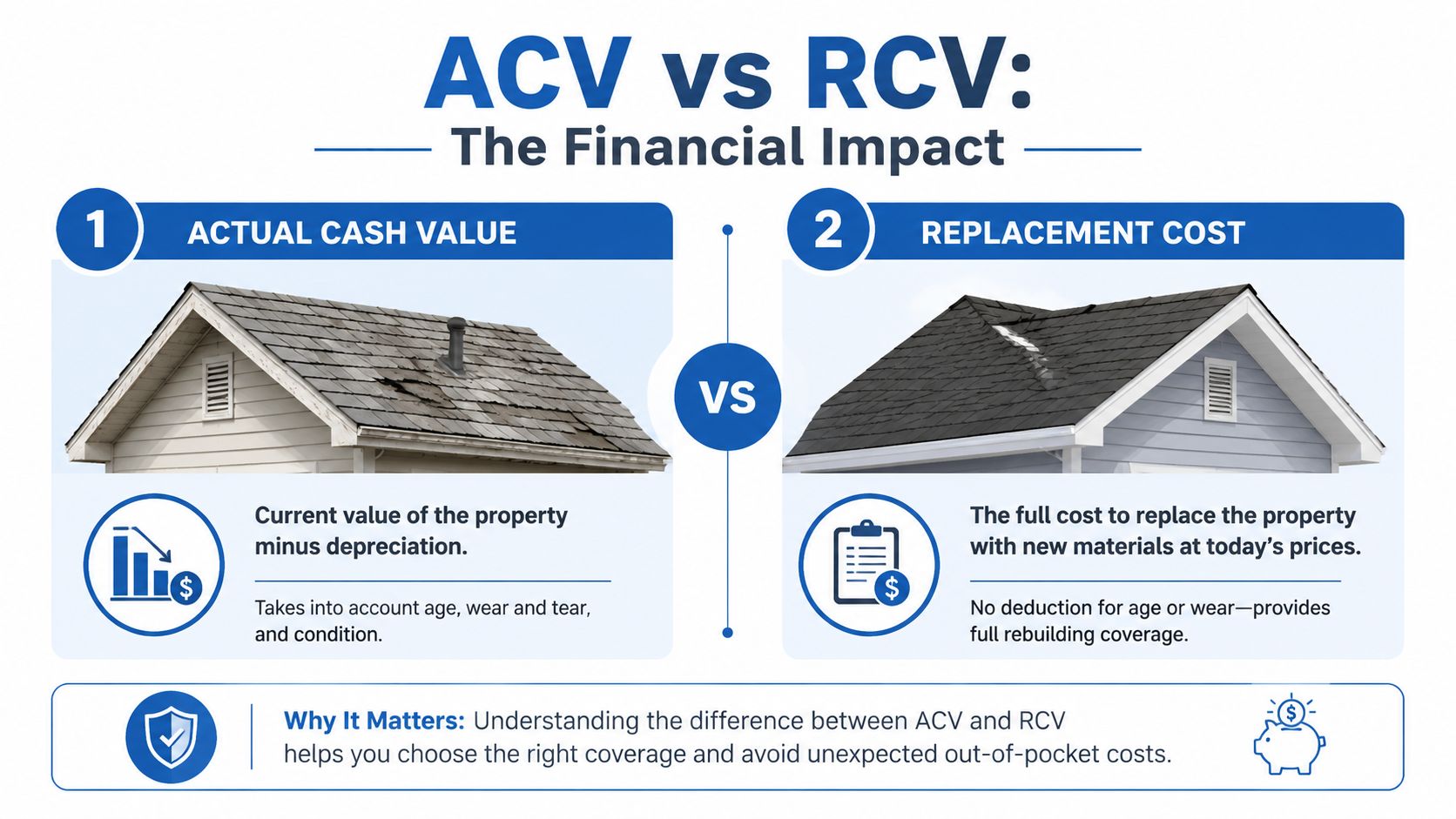

ACV vs RC The Financial Impact on Your Claim

A storm rips shingles off your roof in Raleigh or Richmond. The contractor says the roof has to be replaced. You expect insurance to cover a roof replacement. Then the carrier sends an ACV check that barely covers a portion of the job and acts like the gap is your problem.

That gap is the whole fight.

| Issue | Actual Cash Value | Replacement Cost |

|---|---|---|

| How payout is valued | Current value after depreciation | Current cost to replace with like kind and quality |

| Effect of age and wear | Used to cut payment | Not deducted from the final replacement benefit if you meet the policy conditions |

| Out-of-pocket exposure | Usually much higher | Usually lower if limits and terms are adequate |

| What insurers prefer | Easier to underpay and defend | Harder to suppress when the policy supports full replacement |

| What policyholders need | Money that often falls short | Money that more closely matches real repair costs |

Why ACV creates a real cash crisis

ACV shifts part of the loss back onto you. The carrier prices the claim as if old materials should be worth less, but your contractor charges today’s price for labor and materials. That mismatch is how families and business owners get trapped.

Roof claims make the problem obvious. An older roof may still be functioning before the storm, but once it is damaged, nobody installs half-used shingles at a discount. The insurer knows that. It still uses age and condition to drag the payment down, then waits to see whether you can come up with the difference.

That is why cheap coverage becomes expensive coverage the day you file a claim.

Replacement cost is better, but carriers still use it against you

Policyholders hear “replacement cost” and assume they will get full payment up front. That is rarely how the claim is handled. Many carriers pay ACV first, hold back depreciation, and release the rest only after repairs, invoices, photos, inspections, and deadline compliance.

That delay gives the insurer an advantage. If you cannot front the money, cannot get a contractor started, or miss one paperwork requirement, the carrier keeps money that should have gone to the claim. If you need help understanding how carriers build that holdback, read our guide on depreciation on insurance claims.

In NC and VA, this turns into a practical problem fast. Mortgage companies, contractors, and mitigation vendors do not wait for the adjuster to get around to releasing withheld funds.

The roof example policyholders live through

Say your roof is near the back half of its service life. A storm hits. The contractor says full replacement is required. The insurer agrees the roof is damaged but values it on an ACV basis or starts with ACV and withholds a large chunk as depreciation. Now you are staring at a check that does not buy the roof you need.

That is where carriers press their advantage. They know many policyholders do not know the expected service life of their roofing material, the significance of maintenance records, or how condition affects depreciation arguments. Before a loss ever happens, choosing long-lasting roofing shingles can affect how hard an insurer pushes age-based deductions later. After the loss, your job is to force the carrier to justify every deduction with facts, not broad assumptions.

What this means for your claim strategy

Do not treat ACV versus replacement cost as a technical policy debate. Treat it as a money fight.

If the insurer pays ACV only, calculate the shortfall against actual repair estimates immediately. If the insurer owes replacement cost but withholds depreciation, pin down every condition for release in writing. In NC and VA, demand a written explanation of the valuation method, the depreciation taken, and the exact policy language the carrier relies on.

A low ACV number is often the opening offer, not the correct one.

How Insurers Use Depreciation to Deny and Diminish Claims

Depreciation is where carriers do some of their best underpaying. They present it like a fixed formula. In the field, it’s often a judgment call dressed up as accounting.

The formula is simple. The manipulation happens inside it

A common formula is ACV = RCV × (1 – Depreciation Rate). That formula appears in Home First Agency’s discussion of replacement cost versus actual cash value. On paper, that looks straightforward.

What isn’t straightforward is how the insurer decides the depreciation rate. That’s where low-ball tactics live. The adjuster or desk reviewer can inflate age assumptions, downgrade condition, ignore maintenance, or apply broad depreciation across items that should be valued more carefully.

The same source gives a blunt example. A water-damaged HVAC system with a $12,000 RCV could be depreciated by 40% to an ACV of $7,200. It also states that ACV policies result in 35-60% under-recovery on personal property, with an average gap of $5,000-$15,000 per claim.

That should tell you everything about why carriers lean hard on ACV. It works.

The roof fight is rarely just about the roof

Roof claims are one of the most common depreciation battlegrounds in NC and VA. The carrier focuses on age because age is easy to weaponize. They’ll act like an older roof has little value left, even when the actual issue is whether a covered event damaged it so badly that replacement is required.

That’s why homeowners need outside documentation. Roofing material life isn’t a one-size-fits-all assumption. Climate, installation quality, ventilation, maintenance, and shingle type matter. If you want a practical overview of material longevity before you challenge the insurer’s assumptions, this guide on choosing long-lasting roofing shingles is useful context.

When you compare that kind of real-world roofing information to the insurer’s generic depreciation chart, you start to see the game. The carrier wants a shortcut. Your claim deserves an actual evaluation.

Where adjusters push hardest

Watch for these pressure points:

- Condition downgrades: The carrier may treat property as poorly maintained without solid support, which increases depreciation.

- Useful life assumptions: Adjusters often rely on internal schedules that don’t reflect the specific item, installation, or care history.

- Category-level depreciation: Instead of valuing items individually, they apply broad reductions to entire classes of property.

- Hidden damage minimization: If they miss the full scope, the replacement number starts too low before depreciation is even applied.

If you want to understand how these deductions show up line by line, review this explanation of depreciation on insurance claims. It helps decode what the carrier is doing when the settlement breakdown doesn’t make sense.

Depreciation should reflect real condition and real remaining usefulness. It should not be a blunt instrument to force you into a cheap settlement.

Why contents claims get hit especially hard

Insurers frequently apply depreciation to belongings because many policyholders lack receipts for every possession, model numbers for every appliance, or age records for every piece of furniture, tool, or electronic device. That lack of documentation becomes a significant advantage for the carrier.

The insurer says it needs proof. Then it uses your missing paperwork to assign lower values, older ages, and rough-condition assumptions. By the time you see the spreadsheet, the total has already been gutted.

Decoding Your Policy Fine Print That Can Cost You Thousands

Most policyholders don’t lose valuation fights because they’re careless. They lose because the policy splits coverage in ways that aren’t obvious until after a loss.

Start with the loss settlement section

To understand how your claim should be valued, go straight to the Loss Settlement, Valuation, Property Covered, and Endorsements sections. Don’t stop at the declarations page. The declarations page may tell you limits, but the ambush is usually in the form language and endorsements.

In North Carolina, the North Carolina Department of Insurance explains that HO-3 forms typically provide RCV for the dwelling but default to ACV for contents unless a specific endorsement is added. That single distinction catches a lot of people off guard after fire, water, and storm losses.

If your house is replacement cost but your contents are ACV, the insurer can pay one way on the structure and another way on everything inside it. That’s how families end up able to repair walls and ceilings but unable to replace what was damaged inside.

The holdback trap in replacement cost claims

Even if your policy includes replacement cost, don’t assume the carrier will pay it all at once. The North Carolina Department of Insurance also notes that for RCV claims, insurers make an initial ACV payment, and the policyholder can only claim the recoverable depreciation after submitting proof of repair or replacement. The same source states that public adjusters report an average 30% uplift in settlements by enforcing these RCV clauses against insurer low-ball tactics.

Insurers stall at this stage. They ask for more invoices, more photos, more proof, more forms, and more time. If you miss a deadline, don’t understand the requirement, or can’t fund repairs up front, the carrier keeps money that should have been released.

If your policy has recoverable depreciation, unpaid depreciation is not “extra.” It is part of the claim you still have to force the insurer to honor.

Endorsements that quietly reduce roof and contents claims

These are the clauses I’d check closely in NC and VA property policies:

- Roof surface endorsements: These may switch older roofs to ACV settlement.

- Actual cash value endorsements on personal property: Easy to miss until the inventory is priced out.

- Special limits and sublimits: These can reduce recovery even when the valuation method looks favorable.

- Replacement cost conditions: Some policies require repair or replacement within a certain framework before full benefits are owed.

If you want a plain-language explanation of how endorsement language can change what gets paid, this article on a replacement cost endorsement is worth reviewing.

Business owners have the same problem with more moving parts

Commercial property claims add another layer. The building, tenant improvements, fixtures, inventory, equipment, and business personal property may each have separate valuation rules. A business owner who assumes “replacement cost” applies across the board can get blindsided when the carrier values critical property on an ACV basis or hides limitations in endorsements.

That’s why the policy itself matters more than what the adjuster says over the phone.

Real-World Battles Case Studies in Fighting Valuation Disputes

A low ACV offer feels personal because it lands when you’re already dealing with contractors, cleanup, displacement, or business interruption. But the pattern is familiar. The carrier sends a thin estimate, depreciates aggressively, and hopes the insured won’t challenge the scope or valuation.

A contents claim that looked settled until it was examined line by line

One common fight goes like this. A house suffers major interior damage from fire or water. The insurer agrees there was a covered loss, then prices the personal property with old ages, rough-condition assumptions, and stripped-down descriptions. Electronics become “used electronics.” Furniture becomes “miscellaneous household goods.” Tools, clothing, kitchen items, office equipment, and décor get chopped down by depreciation.

The policyholder sees a total number that might look large on paper, but it won’t replace what was lost. That’s the key. Claim disputes are won by comparing the carrier’s spreadsheet to the actual cost of replacement, item by item, room by room.

Proof that policyholders aren’t imagining the problem

This review screenshot matters because it reflects what people deal with when the insurer’s valuation doesn’t match the actual loss.

That frustration is real. So is the relief when someone finally reads the policy, checks the estimate, and pushes back with documentation instead of excuses.

What winning usually looks like

Winning doesn’t always mean one dramatic moment. More often it looks like sustained pressure:

- A new scope is prepared because the carrier missed damage.

- Depreciation is challenged where the insurer used lazy assumptions.

- Replacement cost language is enforced where the policy supports it.

- Holdbacks are pursued until recoverable depreciation is released.

- Every vague category on the contents list gets converted into specific property with actual replacement support.

That’s how valuation disputes are turned around. Not with outrage alone, but with better evidence and tighter reading of the policy than the insurance company expected from you.

The carrier counts on policyholders being overwhelmed. Detailed documentation changes the balance of power.

Court fights happen because carriers overreach

Courts have sided with policyholders in property insurance disputes when insurers stretched valuation language too far or applied it unfairly. I’m not naming a case here because accuracy matters, and I won’t throw in citations I can’t verify from the approved record. But the larger point stands. Insurers do lose these fights when policyholders challenge weak interpretations instead of accepting them as final.

If your settlement feels detached from actual repair and replacement reality, trust that instinct. That’s often where the dispute starts.

Your Battle Plan Disputing Undervalued Claims and Getting Paid

You open the estimate and the number is nowhere near what it will take to rebuild, replace, or restock. That is the point. Carriers use the gap between actual cash value and replacement cost to pressure policyholders into taking less, especially when the file is messy, the policy is dense, and the insured is tired.

In North Carolina and Virginia, you beat that tactic by making the dispute specific. Do not argue in general terms. Force the insurer to defend each bad number, each missing line item, and each unsupported depreciation decision.

Step one is to dispute the numbers in writing

Phone calls do not protect you. A written dispute does.

Your letter or email should identify the exact problems in the carrier’s valuation:

- Wrong valuation method: Show where the insurer paid ACV even though the policy allows replacement cost, or where it applied ACV to items that need closer review under the policy wording.

- Excessive depreciation: Demand the age, condition, useful life, and method used to calculate depreciation. If they cannot show their math, push back hard.

- Incomplete scope: List every omitted room, trade, material, finish, fixture, and content item.

- Improper holdback handling: If repairs are complete or replacement is underway, demand release of recoverable depreciation based on the policy requirements.

Be blunt. Be organized. Ask for a revised estimate and a written explanation of every disputed item.

Build a file that can beat theirs

Insurers win low-ball disputes when the policyholder keeps reacting to the carrier’s paperwork instead of building a stronger record. Fix that fast.

Get contractor estimates, roofer reports, mitigation invoices, photos, video, receipts, product links, and a detailed contents inventory. In roofing, flooring, cabinetry, and commercial buildouts, specifics matter. Brand, grade, dimensions, finish, and code-related requirements can move the claim value by thousands.

If the policy has an appraisal clause and the valuation fight is heading there, learn the process before the carrier frames it for you. This guide to the insurance appraisal process and the role of an insurance appraiser will help you decide whether appraisal fits your claim.

Keep pressing until they answer the hard questions

A carrier that underpaid once usually does not fix it because you sent one strong letter. It may dodge the biggest issue, repeat the same estimate, or hide behind vague phrases like “standard depreciation” or “policy limitations apply.”

Do not let that slide.

Ask for the exact policy language they are relying on. Ask who prepared the estimate. Ask why materials were downgraded, why labor was reduced, and why line items were omitted. In NC and VA claims, that paper trail matters. If the file later goes to appraisal, complaint review, or litigation counsel, a clean record of your objections can expose how the underpayment happened.

A short explainer can help frame the process:

Bring in help before the claim gets boxed in

Some fights are too large or too technical to handle alone. If the loss is substantial, the depreciation is inflated, the estimate is missing major scope, or the adjuster keeps stalling, get professional help early.

A contractor can address repair scope. A contents specialist can document personal property. A public adjuster can read the policy, inspect the loss, challenge the valuation method, document the damages, and negotiate with the carrier from a position of strength.

The insurer already has trained people working to limit the payout. You need someone pushing the other way.

Frequently Asked Questions About ACV and RCV Claim Disputes

Can I upgrade my policy from ACV to RCV

Yes, but only before a loss. After damage happens, you’re stuck with the policy language that was in force on the date of loss.

If your current policy uses ACV for important parts of the property, ask your agent for the exact endorsement options that convert those areas to replacement cost. Don’t settle for a vague answer. Ask what applies to the dwelling, roof, contents, and business personal property separately.

My roofer says the roof must be replaced, but the insurer is paying ACV because of age

That’s a common dispute. The carrier uses age to reduce value. Your side needs to focus on damage, repairability, policy language, and what like kind and quality requires.

Use a detailed roofer report, photos, slope and elevation breakdowns, and any code-related replacement issues that affect the repair scope. Also check whether a roof endorsement changed settlement terms without you realizing it. A lot of these fights are won by proving the carrier oversimplified both the damage and the policy.

My replacement cost policy still paid me on an ACV basis first. Is that allowed

Often, yes. Many replacement cost claims are paid in stages. The insurer issues an initial payment based on ACV, then releases recoverable depreciation after proper proof of repair or replacement is submitted.

The key issue is whether the carrier is following the policy fairly or using paperwork and delay to avoid paying the holdback. If repairs are documented and the insurer still drags its feet, the dispute shifts from valuation to enforcement.

My business policy mentions functional replacement cost. What is that

Functional replacement cost usually means the insurer may pay to replace damaged property with a functional equivalent rather than an exact replica. For older buildings or unusual materials, that can reduce what the carrier owes compared with standard replacement cost.

Business owners need to read that language closely. “Functional” sounds reasonable until the insurer uses it to justify cheaper materials, altered finishes, or reduced restoration expectations.

Should I accept the first offer if I need money quickly

Usually not without review. Cash pressure is real, but accepting a low number can make a bad claim worse.

If you need funds urgently, focus on getting the claim evaluated properly fast. A weak initial settlement can cost much more than the short-term relief it provides.

2. How do carrier adjusters manipulate "Useful Life" expectations to artificially inflate ACV depreciation?

The Trap: When calculating ACV, company adjusters utilize proprietary estimating platforms like Xactimate or Symbility. They assign arbitrary "useful life" metrics to components like roofing, cabinetry, and flooring to force a lower upfront check.

The Math: If a kitchen cabinet set has a replacement cost of $20,000, and the adjuster claims it has a 20-year useful life and is 15 years old, they will apply a 75% depreciation rate:

$$\text{Depreciation} = \left( \frac{15}{20} \right) \times \$20,000 = \$15,000$$$$ACV = \$20,000 - \$15,000 = \$5,000$$The Solve: Challenge the adjuster's pre-loss condition assumptions. If your cabinets or roof were exceptionally maintained, updated, or modified, they do not follow standard linear depreciation tables. Document historical maintenance to force the adjuster to reduce the depreciation percentage, increasing your initial ACV payout.

3. Why is the "Two-Check" system a dangerous financial hurdle for policyholders in NC and VA?

Direct Answer: An RCV policy does not pay out the full replacement cost immediately. It operates as a reimbursement mechanism split into two distinct payments.

The Structural Reality:

Check 1 (The ACV Check): The carrier issues an initial check for the ACV amount (RCV minus depreciation and your deductible).

Check 2 (Recoverable Depreciation): The remaining balance—the withheld depreciation—is only released after you prove that the repairs are fully completed and you have incurred the actual costs.

The Trap: If you lack the cash flow or a contractor willing to start work based only on the small ACV check, you may find yourself stuck. If you do not perform the physical repairs, you completely forfeit the right to claim Check 2.

4. Can an insurer legally depreciate labor costs on an ACV calculation in North Carolina versus Virginia?

The Statutory Reality: This is one of the most critical legal distinctions between the two states.

In North Carolina: Per the landmark case Accardi v. Hartford Underwriters Ins. Co., insurance carriers are permitted to depreciate the cost of labor when calculating ACV. The state supreme court ruled that "property" represents a whole unit, meaning labor cannot be separated from materials when evaluating depreciation.

In Virginia: The legal framework treats labor depreciation with far higher scrutiny. While many carriers still attempt to bury labor depreciation inside global Xactimate line items (such as tearing off a roof or painting a wall), consumer advocates argue that labor does not lose value with age.

The Solve: Carefully audit the PDF breakdown of the adjuster's estimate. If you are in Virginia, challenge any line item where an intangible service (like labor or cleaning) has a depreciation percentage attached to it.

5. How does the brand-new 2026 Virginia law (HB 808) protect policyholders from arbitrary adjuster reductions to RCV estimates?

The Legislative Edge: Enacted during the 2026 legislative session, Virginia House Bill 808 directly amends Code of Virginia § 38.2-510 (Unfair Claim Settlement Practices), targeting a common carrier tactic where desk adjusters slash field estimates without justification.

The Mandate: Effective July 1, 2026, if an insurer reduces a property loss estimate by $3,000 or more, they must provide the policyholder with a meticulous, line-by-line written explanation for every reduction. Furthermore, the carrier must document the exact identity of the specific individual who ordered or made the cut, and retain all previous versions of the estimate file.

The Application: If a carrier adjuster slashes your contractor’s RCV estimate by thousands to force a lower ACV or RCV settlement, demand the formal HB 808 compliance addendum. This forces transparency and stops anonymous desk adjusters from making arbitrary claim cuts.

6. What is the "Actual Replacement" trap, and how can it cause an RCV claim denial?

Direct Answer: Most RCV contracts contain explicit "Strict Performance" clauses stating that the insurer is not liable for any structural loss on an RCV basis until the damaged property is actually repaired or replaced.

The Trap: If your home suffers a major loss and you decide to take the insurance money to buy a different house, clear the land, or downsize, the carrier will refuse to pay the withheld depreciation. You are capped at the ACV amount.

The Solve: If you choose to replace the property by buying an existing alternative home rather than rebuilding, you must negotiate an alternative replacement allocation. If you buy a replacement home that costs less than the RCV of your damaged home, the carrier will reduce their total payout to match what you actually spent.

7. How does North Carolina's "Broad Evidence Rule" prevent unfair ACV calculations on older or unique structures?

Direct Answer: It prevents the insurance company from using a single, rigid software metric to artificially deflate your property's value.

The Case Law Strategy: North Carolina is a Broad Evidence Rule state (Surratt v. Grain Dealers Mutual Insurance Co.). This rule establishes that adjusters cannot solely rely on arbitrary replacement-cost-minus-depreciation formulas to find ACV if it defies economic logic.

The Application: If your property contains historic architectural features, antique framing, or custom craftsmanship in cities like Wilmington or New Bern, a standard Xactimate depreciation matrix will yield a wildly inaccurate ACV. Under the Broad Evidence Rule, the valuation must factor in real estate market values, expert contractor assessments, age, condition, and localized utility value to establish a fair ACV settlement.

8. What is the "Matching" crisis, and how do NC and VA laws differ when RCV cannot buy matching materials?

The Operational Issue: A storm damages a portion of your siding or roof. The original material is completely discontinued. RCV requires "like kind and quality," but a partial repair will leave your asset looking mismatched and severely damaged in terms of curb value.

In Virginia: Under administrative rule 14VAC5-400-80, insurers must provide a "reasonable uniformity" standard. If an item cannot be matched within a continuous area, the carrier must often pay to replace the undamaged portions (such as the entire roof or all four sides of siding) to preserve visual uniformity.

In North Carolina: There is no explicit matching statute. However, public adjusters successfully counter this by citing the fundamental principle of Indemnity. A mismatched, checkerboard patch creates an immediate Diminution of Value on the open market, meaning the ACV/RCV calculation has failed to return the policyholder to their pre-loss financial position.

9. Why can a routine "Inflation Guard" endorsement still leave you facing a massive coinsurance penalty under an RCV policy?

Direct Answer: Because inflation guards are automatic percentage increases (typically 2% to 4% annually) that rarely match localized spike-inflation in construction material and labor costs.

The Danger: If a commercial building or custom home in booming areas like Northern Virginia or the Raleigh-Durham Triangle has a policy with a 90% coinsurance clause, the "Should Carry" value is calculated on the exact day of the loss, not when the policy was written.

The Risk: If construction costs in your zip code surged by 15% due to regional supply shortages, but your inflation guard only clicked up by 3%, your total limit will fall short of the 90% threshold. The carrier will apply a Coinsurance Penalty, slashing both your upfront ACV check and your ultimate RCV recovery proportionally.

10. How can a policyholder use the Appraisal Clause to break an ACV or depreciation deadlock with a carrier adjuster?

Direct Answer: When a carrier refuses to alter an unfair depreciation factor or disputes the real-world RCV of local contractors, the policyholder can bypass the adjuster completely by invoking the policy's Appraisal Clause.

The Remedy: Appraisal is a form of alternative dispute resolution built into almost all NC and VA property policies.

The Process: You select an independent appraiser, the insurance company selects their own, and a neutral Umpire is chosen. The team evaluates the physical property files and localized construction costs. A binding award signed by any two of the three parties establishes the final, immutable RCV and ACV figures, entirely stripping the file from the original adjuster's hands.

11. What is the time limit to recover withheld depreciation in NC and VA, and can it be extended?

The Statutory Reality: Under standard policy language, you typically have 180 days (6 months) from the date of the loss or the initial ACV payment to notify the insurer of your intent to claim the remaining replacement cost.

The Virginia Exception: Under Va. Code § 38.2-2119(B), the six-month clock to assert an RCV claim for the difference between ACV and full replacement cost can be calculated from the last date you received an ACV payment or from a court order establishing your right to coverage.

The Solve: Never assume a carrier will grant an extension out of goodwill. If supply chain slowdowns or contractor backlogs in Wake County or Fairfax County prevent you from finishing the work within 180 days, you must submit a formal, written request for an extension before the deadline passes. Cite specific regional delays to preserve your right to Recoverable Depreciation.

Settlement Mechanics Matrix: ACV vs. RCV vs. Functional RCV

| Operational Metric | Actual Cash Value (ACV) | Replacement Cost Value (RCV) | Functional Replacement Cost |

| Deduction for Depreciation? | Yes (Deducted upfront and unrecoverable). | Temporarily (Deducted upfront, released upon proof of repair). | No (But materials are downgraded to cheaper modern equivalents). |

| Material Quality Requirement | Same age/wear equivalent value. | Exact like kind and quality at today's retail market rates. | Functionally equivalent material (e.g., drywall replacing plaster). |

| Upfront Payment Base | $$RCV - \text{Depreciation} - \text{Deductible}$$ | $$RCV - \text{Depreciation} - \text{Deductible}$$ | Cost of modern functional equivalent minus deductible. |

| Strict Time Frame Limits? | No performance limits required. | Strict 180-Day Notice parameters apply in NC/VA. |

If your homeowners, dwelling, or business owner claim was low-balled with actual cash value, delayed through recoverable depreciation games, or underpaid because the carrier twisted the policy language, talk to For The Public Adjusters, Inc.. They represent policyholders in North Carolina and Virginia, not insurance companies, and can review the estimate, the policy, and the valuation dispute so you know what to challenge next.