What Is Coinsurance Penalty? – Coinsurance is a penalty clause in property insurance that cuts your claim when you carried less coverage than your policy required. Under a common 80% coinsurance requirement, a $100,000 loss can be reduced to $75,000 before the deductible if you insured $600,000 on a property that required $800,000 in coverage.

In the commercial and high-value residential property insurance markets of North Carolina and Virginia, the coinsurance penalty is one of the most financially devastating traps a policyholder can face. Driven to the forefront by dramatic spikes in construction and material costs over recent years, many property owners are discovering they are dangerously underinsured only after a major storm, fire, or pipe burst occurs.

Understanding how carriers utilize coinsurance clauses to shift risk back onto you is critical to protecting your asset and surviving the claim adjustment process. That’s the part insurance companies rarely explain clearly when they sell the policy. They’re happy to collect premiums for years, then after a fire, hurricane, hailstorm, or water loss, they suddenly point to a buried clause and say your settlement is being reduced because you were “underinsured.” It sounds technical. It isn’t. It’s a weapon.

If you’re searching what is coinsurance, you’re probably not doing it for fun. You’re doing it because the carrier’s number doesn’t make sense, the company adjuster is talking in circles, and the check on the table won’t rebuild your home or put your business back together. You need the plain truth, the math, and a plan to fight back.

Table of Contents

- Your Insurer’s Secret Weapon The Coinsurance Clause

- The Math They Use to Low-Ball Your Claim

- Real-World Fights How Coinsurance Slashes Payouts

- Coinsurance Penalties vs Deductibles A Double Hit

- Coinsurance Claim Disputes in North Carolina and Virginia

- Your Battle Plan Fight Back Against Coinsurance Penalties

Your Insurer’s Secret Weapon The Coinsurance Clause

The ugly part of a property claim often starts after the adjuster leaves. You’ve got torn roofing, soaked drywall, smoke damage, or a half-burned structure in front of you. Then the estimate arrives and it’s nowhere near enough.

The carrier blames “coinsurance.” They make it sound like a neutral accounting adjustment. It isn’t. In property insurance, coinsurance is the clause they use to punish underinsurance and slash a valid claim payment.

What coinsurance really means in property claims

According to the property coinsurance formula explained by CoverLink, the calculation is: loss recovery = (amount of loss) × (limit of insurance purchased ÷ required insurance value) − deductible. That required insurance value is typically 80% of replacement value, and that threshold is designed to penalize policyholders who insured for less.

That single formula gives the insurer room to fight on the numbers that matter most. They can argue about the replacement value of the building, the amount of insurance that should have been carried, the scope of damage, and whether your limit was high enough at the time of loss. If they drive those numbers in their favor, your payout drops.

Practical rule: If the company says “coinsurance applies,” don’t argue from emotion. Demand the replacement value they used, the coinsurance percentage in the policy, the limit they say you carried, and the exact calculation line by line.

Most homeowners and business owners never spot this problem when they buy the policy. They assume the dwelling limit or building limit is “what I’m covered for.” Then a loss hits and they learn that carrying a limit isn’t enough if the insurer later claims it fell below the required percentage of replacement cost. That’s why reading the forms matters, especially the loss settlement and valuation provisions. If you need help decoding the language, start with this guide on how to read an insurance policy.

Why carriers lean on this clause

Insurance companies love complexity because complexity keeps policyholders quiet. A deductible is easy to understand. A coinsurance penalty buried in policy language is not. That confusion benefits carriers like State Farm and Allstate when they want to defend a low payment.

Coinsurance also gives them a clean excuse. They don’t have to say, “We’re trying to save money.” They say, “Your policy requires this.” That sounds final even when their valuation is weak, their estimate is incomplete, or their own underwriting history helped create the problem.

Here’s my opinion after seeing these disputes over and over. If a carrier sold coverage on a building and collected premiums year after year, then turns around after a disaster and claims the structure was worth far more than the insured ever understood, that deserves scrutiny. A lot of scrutiny.

- Policy language matters: The clause has to be read with the declarations, valuation terms, endorsements, and any agreed value provisions.

- Valuation drives the penalty: If the insurer inflates replacement cost, they can force a penalty that shouldn’t apply.

- Documentation changes the balance of power: Contractor estimates, rebuild data, photos, inventories, and prior policy records can all expose a bad coinsurance position.

Coinsurance isn’t a partnership. It’s not “shared responsibility” in the way people think about health coverage. In property claims, it’s a penalty mechanism, and insurers use it when they think the policyholder won’t push back.

The Math They Use to Low-Ball Your Claim

If you can’t do the math, you can’t spot the trap. That’s why carriers hide behind spreadsheets, estimate platforms, and vague explanations from desk adjusters. They want the calculation to feel too technical to challenge.

The calculation itself is simple. The fight is over the inputs.

The formula in plain English

Think of property coinsurance this way:

- The policy sets a required coverage level, often tied to a percentage of replacement value.

- The insurer compares what you carried against what they say you should have carried.

- They apply that ratio to the loss.

- Then they subtract the deductible.

That means the carrier can cut you twice. First with the penalty ratio. Then with the deductible after the reduced amount is calculated.

Here’s how the pieces work in plain English:

- Insurance carried: The building limit or applicable limit listed in your policy.

- Insurance required: The amount the policy says you needed, often based on the property’s replacement value multiplied by the coinsurance percentage.

- Loss amount: The covered damage before the deductible.

- Deductible: Your policy’s share after the penalty math is done.

Don’t let the adjuster rush past the “insurance required” number. That’s usually where the fight lives.

A simple penalty table

| Line Item | Example Calculation |

|---|---|

| Insurance Carried | Coverage limit the policyholder bought |

| Insurance Required | Replacement value multiplied by the policy’s coinsurance requirement |

| Ratio Used by Insurer | Insurance Carried ÷ Insurance Required |

| Loss Amount | Covered damage before deductible |

| Payout Before Deductible | Loss Amount multiplied by the ratio |

| Final Check | Payout before deductible, then deductible subtracted |

This is why two policyholders with the same storm damage can get very different checks. The company isn’t only adjusting the loss. It’s also auditing whether it can apply a penalty.

A few practical questions force the issue fast:

- What replacement value did you use? Ask for the full basis, not a summary.

- What coinsurance percentage applies? It should be tied to the actual form and endorsement.

- Did you include all applicable coverages and endorsements? Some carriers “forget” provisions that help the policyholder.

- Did you calculate on replacement cost or actual cash value? The policy language matters.

If the insurer won’t show the math cleanly, that’s not a good sign. A valid adjustment should be easy to explain. When the desk adjuster keeps repeating conclusions without showing the calculation, they’re counting on you to give up.

Real-World Fights How Coinsurance Slashes Payouts

Numbers become real when they land on your kitchen table as a short check. That’s when people realize coinsurance isn’t just a definition. It’s the difference between rebuilding and draining savings.

The hotel example every policyholder should know

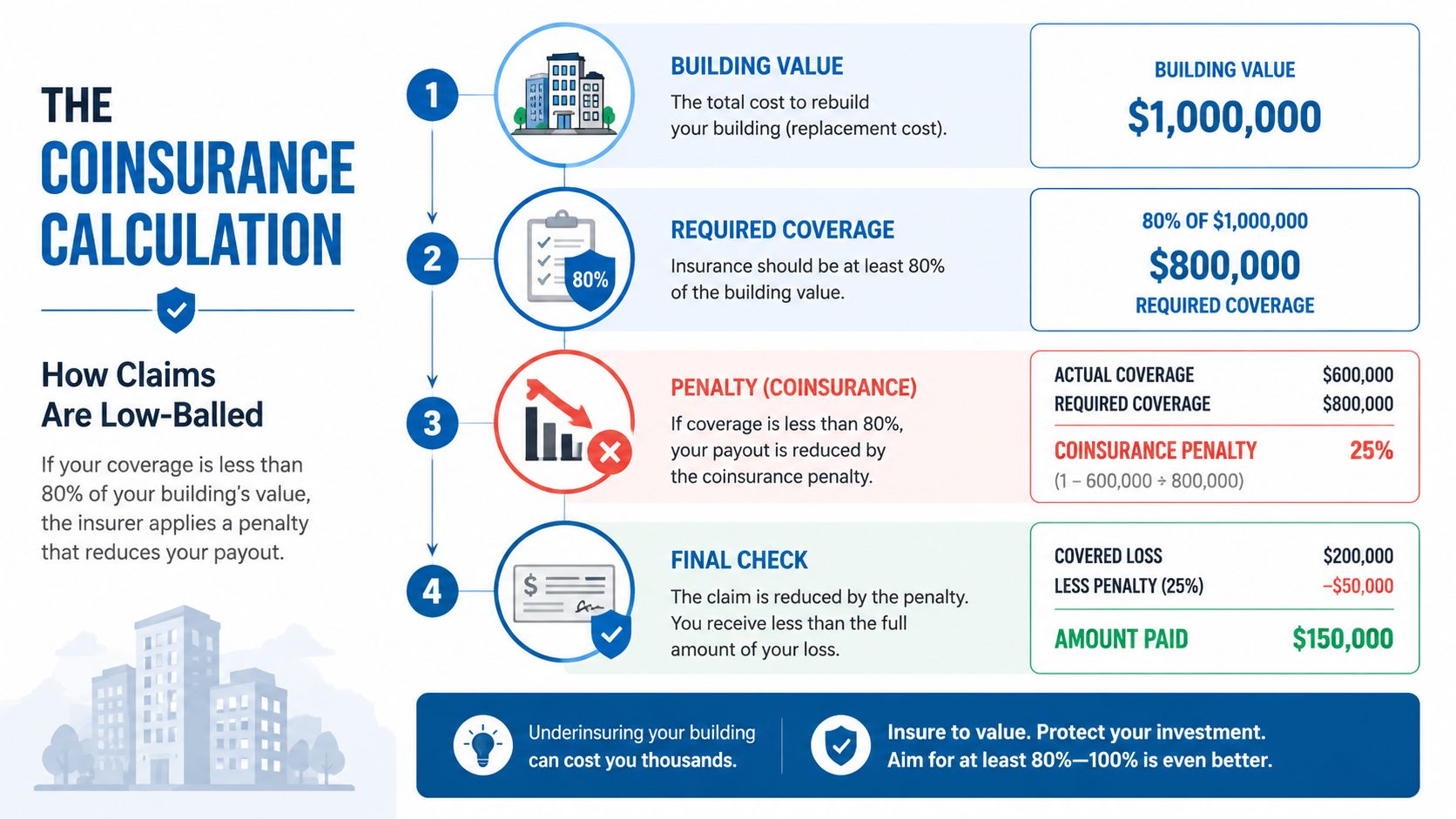

A classic example shows exactly how harsh this clause can be. In the Atlas Hotel coinsurance example from Adjusters International, the hotel had a building valued at $1 million with an 80% coinsurance clause, but carried only $600,000 in insurance. The required insurance was $800,000. After a $100,000 fire loss, the payout was ($600,000 ÷ $800,000) × $100,000 = $75,000, leaving the owner $25,000 short.

That wasn’t a total loss. That’s what shocks people. The owner didn’t lose the whole building. The penalty hit on a partial loss.

That’s how carriers use this clause in practice. You can have a legitimate covered loss to part of the structure, and they still reduce payment because they say your total insurance limit was too low compared with the building’s value.

A partial loss doesn’t protect you from a coinsurance penalty. In many cases, that’s exactly when the insurer uses it.

Why small coverage gaps become big repair bills

Policyholders often think underinsurance only matters if the building is destroyed. That assumption costs people real money. Coinsurance changes the economics of even modest claims because the shortfall gets spread proportionally across the loss.

Here’s where people get burned:

- Rising rebuild costs: Your limit may have looked reasonable when the policy renewed, then material and labor pricing changed.

- Old estimates: The insurer relied on outdated valuation assumptions when selling or renewing the policy.

- Incomplete schedules: Outbuildings, improvements, tenant improvements, or business property weren’t valued correctly.

- Carrier math games: The insurer applies a larger replacement value after the loss than anyone discussed before the loss.

Commercial owners get hit especially hard because building, contents, and business personal property values are often more complex. Homeowners aren’t safe either. A fire in one area of the home can trigger a penalty tied to the whole dwelling value, not just the damaged room.

The worst part is the timing. The penalty shows up when you’re already paying for temporary repairs, cleanup, mitigation, or lost use of the property. That’s why a coinsurance dispute is never “just” an accounting issue. It becomes a cash-flow crisis fast.

When a carrier applies this penalty, don’t focus only on the final number. Break apart the assumptions behind it. If the value is wrong, the ratio is wrong. If the ratio is wrong, the whole payment falls apart.

Coinsurance Penalties vs Deductibles A Double Hit

A storm tears through your property. You expect to pay your deductible and move on to repairs. Then the insurer cuts the claim again under a coinsurance clause and acts like that second hit is normal. It is not normal to policyholders. It is normal to carriers that want to shrink payouts.

A deductible is the amount you agreed to absorb. A coinsurance penalty is money the insurer withholds because it claims your limit was too low. Those are two separate cuts, and the carrier often applies them in the order that hurts you most.

The usual play is simple. The insurer reduces the loss first with a coinsurance penalty. Then it subtracts the deductible from that already-reduced figure. The result is a smaller check than many owners ever saw coming.

Property owners get trapped here because the word “coinsurance” sounds harmless. In health insurance, it often means a shared percentage of covered costs after the deductible. In property insurance, it is a claim-reduction tool tied to alleged underinsurance. Same word. Very different result. That confusion helps the carrier.

Here is the side-by-side reality:

| Issue | Deductible | Property coinsurance penalty |

|---|---|---|

| What it is | Your fixed share of a covered loss | A reduction based on alleged underinsurance |

| When it applies | On covered claims under the policy terms | When the insurer says you failed to carry the required limit |

| How it affects payment | Subtracted from the covered amount | Cuts the covered amount before the deductible is taken |

| Can it be hidden in the adjustment | Rarely | Often |

That order matters.

If a carrier owes $100,000 on a covered loss, applies a 20% coinsurance penalty, and then subtracts a $5,000 deductible, the payment drops to $75,000. The policyholder does not lose only the deductible. The policyholder loses the penalty first, then loses the deductible on top of it.

That is why so many owners feel ambushed. They planned for a deductible. They did not plan for the insurer to revalue the building after the loss, declare the policy underinsured, and slash the payment before the deductible even enters the math.

Do not let the adjuster blur those charges together. Ask three direct questions in writing: Was a coinsurance penalty applied? What valuation did you use to trigger it? Where does the policy allow you to take the penalty before the deductible? If the answers are vague, you likely have a dispute worth pressing. Start with this guide on how to dispute an underpaid insurance claim and build your paper trail fast.

The deductible is the price of entry. The coinsurance penalty is the squeeze play. Treat it that way.

Coinsurance Claim Disputes in North Carolina and Virginia

North Carolina and Virginia property owners live with storm risk, wind losses, fire losses, hail claims, and rebuild cost swings. That makes coinsurance disputes especially dangerous here. The clause doesn’t stay buried when a major weather event hits. Carriers start using it.

Why NC and VA property owners get trapped

After Hurricane Florence caused $22 billion in damages in North Carolina in 2018, many commercial property owners learned the hard way that underinsured buildings could receive only partial claim payments because of coinsurance penalties. That amplified losses when owners needed funds most.

That pattern isn’t limited to commercial buildings. Homeowners run into the same problem after major storm seasons because replacement costs don’t stay still. Roofing, framing, drywall, electrical work, code upgrades, and labor pressures can push rebuilding costs above what the policyholder expected. Then the insurer arrives after the loss with a bigger valuation than the one everyone lived with before the loss.

That’s where a dispute starts. Not every coinsurance penalty is valid. Some are based on shaky valuation models, incomplete inspections, or a one-sided reading of the policy.

What local policyholders should do when the carrier applies a penalty

This kind of fight requires documentation, not pleading. If your insurer applies coinsurance in NC or VA, demand:

- The valuation basis: Ask for the estimate, software output, scope, and assumptions behind the replacement cost number.

- The exact policy support: Require the company to identify the form, endorsement, and percentage they rely on.

- The full payment calculation: You want every line item, not a summary letter.

- The claim file trail: Notes, prior estimates, and underwriting history can matter.

For disputes already underway, this guide on how to dispute a property insurance claim is a useful place to organize the challenge.

Local policyholders also need to stop assuming the company adjuster is a neutral referee. The insurer’s adjuster works for the insurer. Their job is to protect the carrier’s position, and if that means leaning hard on coinsurance language, that’s exactly what they’ll do.

This is one reason outside representation matters in storm-prone states. A public adjuster can test the building valuation, compare scope against actual damage, review endorsements, and push back when the penalty is built on bad assumptions.

A lot of people feel isolated during a dispute like this. They’re not. Other policyholders have already gone through the same fight.

One customer review posted on CustomerLobby for For The Public Adjusters, Inc. reflects the same theme policyholders repeat all the time: the insurance company’s number wasn’t enough, the process was frustrating, and experienced claim advocacy changed the outcome. That doesn’t mean every case is identical. It means you’re not crazy for questioning a low payment.

Your Battle Plan Fight Back Against Coinsurance Penalties

Anger helps for about five minutes. After that, you need a strategy. Coinsurance disputes are winnable when you attack the right points and stop letting the carrier define the conversation.

Property policies do not have the kind of out-of-pocket maximums people associate with health insurance. As explained in Healthcare.gov’s coinsurance glossary, a property coinsurance penalty can reduce your claim payout without any cap, and once your policy limit is hit, you’re fully exposed. The same source says the NAIC reported in 2025 that 60% of homeowners still misunderstand this risk, which helps explain why so many claims end in underpayment.

What to challenge immediately

Start with the insurer’s valuation, not their conclusion. If they claim you were underinsured, they’re relying on a replacement cost number. That number is often vulnerable.

Use this checklist:

-

Get the full estimate

Ask for the carrier’s complete replacement cost estimate, not just the declarations page and not just a summary letter. You need line items, measurements, assumptions, and any depreciation or pricing basis.

-

Compare scope to real conditions

Walk the property with your contractor, restoration professional, or estimator. If the insurer missed code-related items, specialty materials, built-ins, roofing components, trim details, or necessary demolition, their replacement value may be distorted.

-

Pull prior policy and renewal records

Look at prior declarations, underwriting inspections, and communications about building value. If the carrier accepted the risk at a lower valuation for years and never flagged an issue, that history can matter in the dispute.

-

Read the endorsements

Some policies contain agreed value provisions, endorsements, or valuation language that changes how coinsurance applies. Never let the insurer quote one clause in isolation.

Bad carrier math only works if you accept the building value without proof.

You should also organize photos, contractor bids, invoices, maintenance records, appraisals if relevant, and any pre-loss documentation showing the condition and features of the property. This isn’t about drowning the insurer in paper. It’s about forcing them to deal with facts.

When to stop arguing and bring in help

There’s a point where direct back-and-forth with the company adjuster stops being productive. You’ll know it when every email sounds the same, every call ends with “our position stands,” and nobody at the carrier answers the actual valuation questions.

That’s when you bring in professionals who work for you. A public adjuster can analyze the policy, build a competing loss estimate, challenge the replacement cost assumptions, and negotiate directly with the carrier. In some disputes, legal support also becomes necessary, especially when the carrier delays, stonewalls, or misapplies policy language. Firms that need front-end client communication support sometimes look to resources like Hire legal intake specialist to keep claim-related legal matters organized, especially when high-volume dispute intake starts overwhelming the office.

If you need a structured next step, review this guide on how to appeal an insurance claim decision. Then decide whether the dispute has already reached the point where outside representation makes more sense than more arguments with the insurer.

For policyholders in NC and VA, For The Public Adjusters, Inc. handles property-loss evaluation, documentation, and negotiation for homeowners and business owners dealing with underpaid, delayed, or disputed claims. That kind of work matters when the conflict is over building value, policy interpretation, and whether the coinsurance penalty should apply at all.

Here’s the hard truth. Insurance companies count on fatigue. They know you’re trying to repair property, manage contractors, protect your family or business, and keep life moving. They use delay, complexity, and policy jargon because worn-out policyholders settle cheap.

Don’t do that.

- Challenge the value: If the replacement cost is wrong, the penalty may be wrong.

- Challenge the scope: Missed damage and omitted repairs can poison the whole calculation.

- Challenge the policy reading: One clause never tells the whole story.

- Escalate when needed: Public adjusters, contractors, consultants, and attorneys each have a role depending on how far the carrier pushes the dispute.

The insurer’s first coinsurance position is not the final word unless you let it be.

If you came here asking what is coinsurance, the honest answer is this: in property claims, it’s one of the most effective tools insurers use to shrink payments after a disaster. Once you understand that, you can fight it the right way.

2. How is a coinsurance penalty calculated during a partial loss claim?

The carrier divides the amount of insurance you actually purchased by the amount you should have purchased, applies that percentage to the total loss amount, and subtracts your deductible.

The Forensic Example:

True Replacement Value of Building: $1,000,000

Coinsurance Requirement: 80% (Amount you should carry: $800,000)

Amount Actually Carried: $400,000 (You only carried 50% of what you "should" have)

Your Partial Wind/Hail Loss: $100,000

The Math: $\frac{\$400,000}{\$800,000} = 0.50 \times \$100,000 = \$50,000$ payout (before deductible).

The Result: You lose $50,000 of your claim payout due to the penalty, despite the total loss being well below your $400,000 policy limit.

3. Why are property owners in NC and VA hitting coinsurance penalties more frequently now?

Rapid macroeconomic inflation and exploding local construction markets (such as the Triangle area in NC and Northern Virginia) have caused real-world replacement costs to drastically outpace historic policy limits.

Many policies are renewed year after year with standard 2% to 4% inflation guards. However, actual construction labor and material costs in markets like Raleigh or Richmond have surged far beyond those numbers over the last several years. If your building was valued accurately in 2022, it is highly likely underinsured today, triggering an automatic coinsurance penalty upon inspection.

4. What is the "Value at the Time of Loss" trap used by adjusters?

The adjuster determines the property's replacement cost value on the exact day the damage occurred, not the value when the policy was written or when the premium was paid.

This is where carriers frequently deny full payouts. The field adjuster will run a retroactive valuation using software like Xactimate or Marshall & Swift, maximizing the estimated building value to artificially inflate the "Should Carried" denominator. If they can inflate your building’s pre-loss valuation, they successfully trigger the penalty and slash your claim payout.

5. How does North Carolina General Statute § 58-3-15 protect policyholders?

NCGS § 58-3-15 dictates that no insurance company may issue a policy containing a coinsurance clause unless the policy explicitly and transparently details the requirement.

The statute mandates that if there is a difference in the insurance premium rate with versus without the coinsurance clause, the carrier must furnish those rate options to the insured upon request. If a carrier or broker fails to provide clear disclosures regarding the operational reality of the penalty at your policy's inception, you may have grounds for an errors and omissions (E&O) claim against the agent.

6. Can an insurance company apply both a coinsurance penalty and labor depreciation in NC or VA?

No, they cannot double-dip on the same line items to reduce your payout.

Under North Carolina case law (Accardi v. Hartford), carriers are permitted to depreciate labor when calculating Actual Cash Value (ACV). However, if a carrier applies a coinsurance penalty, they are adjusting the loss based on an insurance-to-value deficit. If an adjuster applies a massive depreciation percentage to materials and labor and then hits you with a coinsurance penalty on top of that depreciated number, they are violating standard policy loss-settlement provisions.

7. How does the "Broad Evidence Rule" help defeat a coinsurance penalty in North Carolina?

It prevents the insurance company from using a single, rigid software metric to artificially inflate your property's value to trigger a penalty.

North Carolina follows the Broad Evidence Rule (Surratt v. Grain Dealers Mutual Insurance Co.). This rule states that to find the true value of a property, the appraiser or adjuster must consider every logical factor, including market value, replacement cost, age, condition, and location. If the carrier’s adjuster uses an inflated, generic software estimation to claim you failed coinsurance, you can counter with real estate market comps and localized contractor assessments to drive the property valuation down, satisfying the coinsurance threshold.

8. Does a coinsurance penalty apply if my building suffers a total loss?

No. Coinsurance penalties technically disappear or become irrelevant in a true, 100% total loss scenario.

If your building burns entirely to the ground, the carrier will simply pay out the face value limit of the policy (e.g., $500,000). While you won’t face a percentage "penalty" reduction on that amount, you will still suffer a massive financial loss because your policy limit was fundamentally inadequate to rebuild the structure.

9. What is the difference between an 80%, 90%, and 100% coinsurance requirement?

The percentage indicates the proportion of the property's total value you must maintain in active policy limits to keep the policy's replacement cost coverage fully intact.

| Coinsurance % | True Rebuild Cost | Minimum Policy Limit Required | What Happens Below Limit |

| 80% Coinsurance | $1,000,000 | $800,000 | Proportional penalty on all partial claims. |

| 90% Coinsurance | $1,000,000 | $900,000 | Higher premium discount; stricter penalty margin. |

| 100% Coinsurance | $1,000,000 | $1,000,000 | Common in "Blanket Policies" or builder's risk; zero margin for underinsurance. |

10. How can a policyholder permanently eliminate the risk of a coinsurance penalty?

You must secure an Agreed Value Endorsement (sometimes called an Agreed Amount Endorsement) on your policy.

This endorsement suspends the coinsurance clause entirely. You and the carrier agree on the value of the property at the beginning of the policy year. As long as you maintain that specific agreed limit, the carrier cannot invoke a coinsurance penalty at the time of a claim, no matter how much local construction costs have fluctuated.

11. What should a policyholder do if an adjuster applies an unfair coinsurance penalty?

Immediately dispute the carrier's pre-loss building valuation and invoke the policy's Appraisal Clause.

Coinsurance penalties are entirely dependent on a disagreement over the value of the property and the amount of the loss. Because this is a valuation dispute rather than a coverage denial, it is a prime candidate for the Appraisal process. By hiring an independent appraiser who understands the NC/VA construction landscape, you can force a realistic valuation of the building, bypass the carrier's desk adjuster, and have a neutral umpire rule the penalty invalid.

If your insurer is using coinsurance to cut a fire, wind, hail, water, or hurricane claim in North Carolina or Virginia, get a second set of eyes before you accept the payment. For The Public Adjusters, Inc. works for policyholders, not insurance companies, and can review the policy, inspect the damage, and challenge low-ball claim math that leaves you short when it’s time to rebuild.