You opened the letter expecting money to repair your house or business. Instead, the carrier sent a denial, a partial payment, or an estimate so thin it barely covers cleanup. That shock is real. So is the anger.

If you're searching for how to appeal insurance claim decisions after fire, water, wind, hail, hurricane, or storm damage, start with this: the insurer's first answer is often just its first position. It is not the final word unless you let it be. Carriers know many policyholders are exhausted, busy, and unfamiliar with policy language. They use that.

Your Claim Was Denied or Low-Balled Now the Real Fight Begins

State Farm, Allstate, and the rest of the big carriers don't get the benefit of the doubt from me. I've seen too many delayed inspections, selective photos, narrow scopes, and estimates built to save the company money instead of restoring the property correctly.

When your claim gets denied or underpaid, you're not in a partnership anymore. You're in a dispute.

Why carriers expect you to quit

Insurance companies count on confusion. They count on people missing deadlines, accepting vague explanations, or assuming the adjuster's estimate must be correct because it came from the insurance company.

That assumption costs people money.

A useful parallel comes from a different insurance setting. In ACA Marketplace plans, insurers denied nearly 19% of in-network claims, yet consumers appealed fewer than 1% of those denials, showing how often policyholders accept a bad decision without a fight and leave money on the table that could be recovered through a formal appeal, according to MoneyGeek's review of ACA claim denial rates.

Property claims work differently, but the behavior pattern is familiar. People get discouraged. Carriers know it.

What a low-ball offer usually means

A low offer doesn't always mean the adjuster missed everything by accident. It often means the inspection was incomplete, the pricing was lean, the drying or mitigation scope was minimized, overhead and profit were ignored, line items were omitted, or the carrier framed part of the damage as wear, maintenance, pre-existing, or excluded loss.

That's why you can't treat the first estimate like gospel.

Use this quick reality check:

| Situation | What it usually means |

|---|---|

| Full denial | The carrier is taking a coverage position you need to challenge directly |

| Tiny payment | The carrier acknowledged some damage but is minimizing scope or price |

| Repeated requests for the same documents | Delay tactic, poor file handling, or both |

| Verbal promises without written follow-up | You have no protection unless it's documented |

Practical rule: A denial letter is not the end of the claim. It's the start of the paper fight.

Stop reacting and start countering

If you're frustrated, good. Use it. But don't waste it on angry phone calls alone.

Do three things immediately:

- Preserve every document: Keep letters, emails, estimates, photos, receipts, and text messages.

- Get the policy out: Not the declarations page only. The full policy with endorsements.

- Create a claim timeline: Date of loss, first notice, inspections, payments, denials, follow-ups.

That timeline matters because carrier delay is often half the game. If they can drag you out, they increase the odds you'll accept less.

You're not asking for a favor. You're demanding benefits under a contract you paid for.

Before You Appeal Understand Why They Denied You

Read the denial letter like you're looking for weaknesses, not truth. Most policyholders read it once, get angry, and jump straight to arguing. That's a mistake.

The letter tells you the insurer's defense. Your job is to break it apart.

Read the denial letter line by line

Start with the exact wording. Not the adjuster's summary on the phone. Not what you think they meant. The actual language in the letter.

Look for these pressure points:

- Specific exclusion cited: Did they identify the exact policy wording, or are they speaking in generalities?

- Condition allegedly violated: Late notice, failure to protect property, lack of cooperation, vacancy, wear and tear, repeated seepage, surface water, flood, or pre-existing damage.

- Causation language: Are they blaming excluded causes like flood instead of covered causes like wind-driven opening or sudden discharge?

- Scope manipulation: Did they accept part of the damage but ignore related areas?

If the denial refers to an engineer, consultant, or preferred vendor, flag it. That outside report often drives the whole decision.

Demand the complete claim file

A smart appeal is built from the carrier's own paperwork as much as your own. One of the most overlooked tactics is demanding the complete claim file, because it can expose weak spots such as a biased report or missing documentation you already sent, a strategy highlighted in this discussion of appealing denied insurance decisions.

Ask for the full file in writing. Be direct.

Request:

- Adjuster notes

- All photographs and video

- Recorded statements and transcripts

- Expert reports

- Internal estimates and revisions

- Reservation of rights letters

- Email communications tied to the claim

- Logs showing when documents were received

If the insurer resists, that tells you something too.

Demand the file early. If their report ignores evidence, or if the file is missing materials you already provided, you've found leverage.

What to look for inside the file

Bad carrier work surfaces at this point.

You may find:

- Selective photography: They photographed the least severe area and skipped the worst rooms.

- Changed narrative: Early notes acknowledge storm-created openings or sudden water damage, later reports back away from it.

- Missing submissions: Your contractor estimate, mitigation invoice, mold protocol, or repair photos never made it into the reviewed file.

- Biased experts: Their consultant used language that sounds certain while avoiding inconvenient damage indicators.

- Internal inconsistencies: One document says "sudden loss," another labels it "long-term seepage."

A lot of this gets harder for consumers to spot because carriers now use automated systems and software-assisted workflows. If you want a plain-English primer on how technology shapes modern carrier decision-making, this breakdown of AI in insurance claims processing is worth reading. It helps explain why fast denials and templated responses are so common.

Match the denial to the policy

Don't argue in general terms like "this isn't fair." Fairness doesn't move a claim. Policy language does.

Build a simple two-column worksheet:

| Carrier says | Your response should show |

|---|---|

| Damage is excluded | The cited exclusion doesn't apply, or an exception restores coverage |

| Damage is old | Photos, invoices, or witness history show a sudden event |

| Damage is below deductible | Their scope or pricing omitted covered work |

| You failed to comply | Your emails, calls, inspections, and document submissions prove cooperation |

Most homeowners lose momentum because they fight the carrier's conclusion instead of attacking the foundation under it. Focus on the foundation.

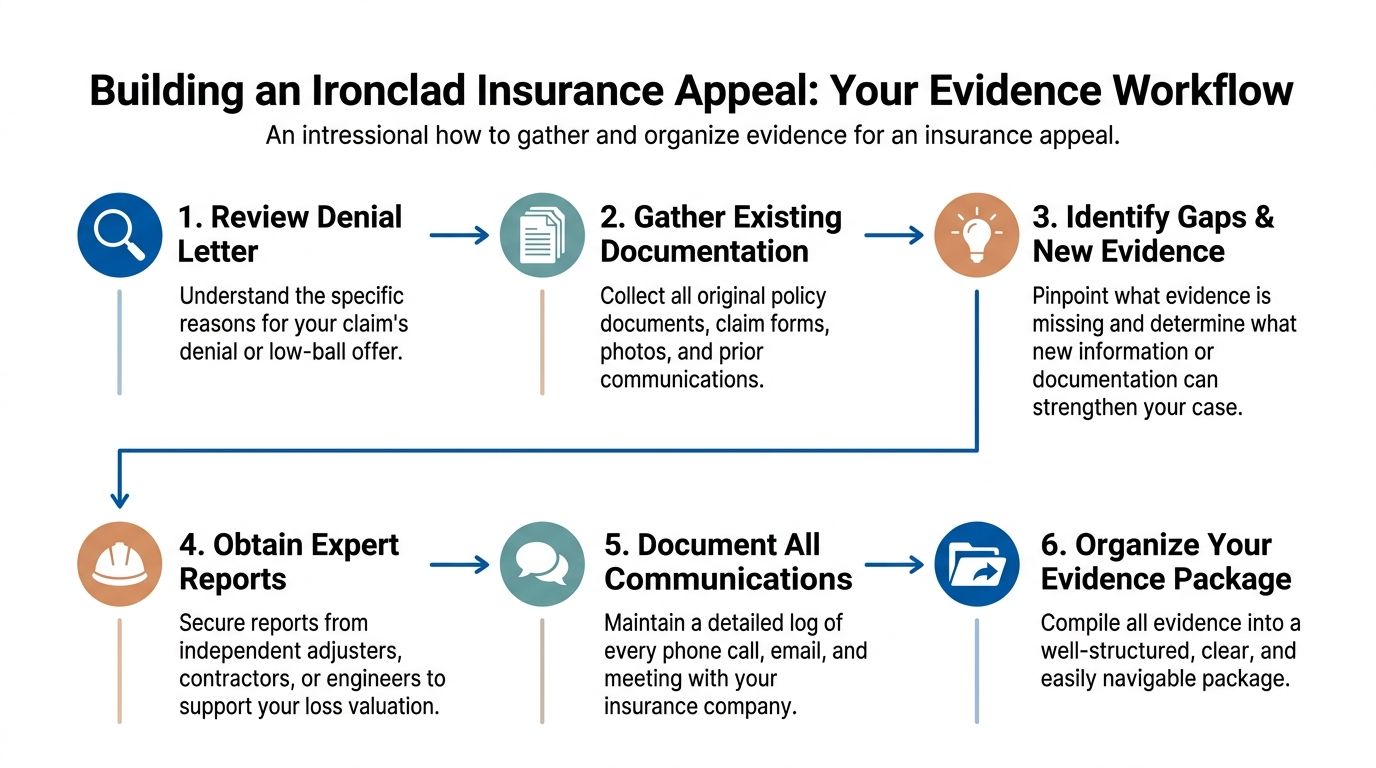

How to Build an Ironclad Case for Your Insurance Appeal

An appeal with no new proof is just a complaint in nicer formatting. If you want the carrier to reverse course, you need a file so organized and so specific that a supervisor, outside reviewer, or regulator can see the holes in the denial fast.

That means evidence. Clean, labeled, dated evidence.

Build the file like you're preparing for a serious dispute

Don't dump a stack of random PDFs on the insurer. Assemble a package.

Use this order:

- Appeal letter

- Claim timeline

- Relevant policy pages

- Your photos and video

- Independent estimates

- Expert reports if needed

- Receipts and emergency mitigation records

- Communication log

- A short damages summary

The appeal process follows a real methodology. A well-documented appeal with independent estimates, photos, and policy excerpts can overturn an insurer's decision, and while fewer than 1% of claims are appealed, those that reach external review can see 40-60% success rates, according to the methodology outlined by AHIMA.

That doesn't mean every case wins. It means sloppy appeals lose opportunities that strong appeals preserve.

Your independent evidence matters more than your opinion

Homeowners often tell me, "I know the adjuster missed damage." They usually did. But knowing it isn't enough. You need proof in a format the claim system can't ignore.

Get your own documentation:

- Contractor estimates: From local contractors who work for you, not for the carrier.

- Moisture or damage mapping: Helpful in water losses where the adjuster minimized spread.

- Detailed photos: Wide shots, close-ups, elevations, ceilings, trim, flooring transitions, attic or crawlspace if relevant.

- Content lists: Especially for smoke, soot, or water-damaged business property.

- Code-related observations: If repairs trigger code work, document that issue clearly.

If the claim involves a sworn statement of what was lost and what it should cost to repair or replace, review how a proof of loss works in a property claim and make sure your submission is consistent with the rest of your package.

A real-world pattern I see all the time

A homeowner gets a fire or major water loss. The insurance company sends its adjuster and maybe one preferred vendor. The carrier writes a narrow estimate. It leaves out hidden damage, detached and reset items, manipulation of cabinetry, paint continuity, smoke migration, moisture spread, or proper contents handling.

Then the homeowner gets told the estimate is "based on what was observed."

That's the trap. The insurer only values what it chooses to observe.

A stronger appeal file flips that.

An independent inspection can document areas the carrier brushed past. A line-by-line estimate can identify omitted work. Policy excerpts can tie those repairs back to covered loss. Once the evidence is organized, the issue stops being "the homeowner disagrees" and becomes "the insurer's scope is incomplete."

What a strong appeal packet includes

| Item | Why it matters |

|---|---|

| Photos taken over time | Show progression, spread, and areas the carrier skipped |

| Independent repair estimate | Challenges the insurer's pricing and scope |

| Policy excerpts | Forces the dispute back to contract language |

| Mitigation invoices | Prove emergency response and seriousness of loss |

| Written rebuttal to insurer report | Exposes unsupported conclusions |

Your appeal should make it easy for the next reviewer to reverse the first reviewer.

One option when the claim gets technical

Some cases need more than contractor input. Complex fire, smoke, water, wind, and commercial claims often require a public adjuster who can inspect, scope, estimate, and negotiate from the policyholder side. For The Public Adjusters, Inc. handles that kind of property-claim documentation and negotiation for homeowners and businesses in North Carolina and Virginia.

The point isn't to send in more paperwork. The point is to send in better paperwork.

Advanced Claim Dispute Tactics Your Insurer Hates

Most policyholders only hear about the path the insurance company wants them to use. That's convenient for the carrier, not for you.

Two tactics change the pressure in a claim dispute fast. First, knowing whether you need appraisal or a coverage appeal. Second, creating a record the carrier can't casually brush aside when it stalls, stonewalls, or keeps shifting explanations.

Appraisal is not the same as an appeal

A lot of homeowners hear "invoke appraisal" and think it solves everything. It doesn't.

A common mistake is confusing the appraisal clause with a coverage appeal. Appraisal is for disputing the amount of loss, not whether the loss is covered at all. Using appraisal for a full denial can badly delay the claim, especially in North Carolina and Virginia storm cases involving wind versus flood disputes, as explained in this appeals guidance.

Here's the practical version:

| If your dispute is about | Likely path |

|---|---|

| Whether the policy covers the loss at all | Appeal, complaint, or legal action |

| How much it costs to repair covered damage | Appraisal may be appropriate |

| Both coverage and amount | Resolve coverage position first, then evaluate appraisal |

If the insurer says, "We don't owe because this peril is excluded," appraisal usually won't fix that. If the insurer says, "We agree it's covered but your repairs cost less," appraisal may help.

Pick the wrong path and you burn time.

Use pressure tools the carrier doesn't control

When the insurer delays, repeats document requests, or demands another statement after you've already cooperated, stop treating every request as neutral. Some are legitimate. Some are pressure.

If the company schedules an examination under oath, read up on what that process means and how to prepare before you walk in unguarded. This overview of an examination under oath in property insurance claims is a good starting point.

Use these counter-moves:

- Put every dispute in writing: Phone calls disappear. Letters don't.

- Ask direct coverage questions: Request the exact policy basis for every denied item.

- Demand written clarification: If they change reasons, make them own the change on paper.

- Separate covered from disputed items: Don't let the carrier hide an underpayment issue inside a vague denial.

If the insurer won't explain its position clearly in writing, that's usually because the position gets weaker once it's pinned down.

A short explainer can help if you're trying to understand how insurers frame claim disputes and why documentation matters so much.

File complaints strategically, not emotionally

A Department of Insurance complaint isn't magic. It also isn't useless.

Use it when the carrier ignores evidence, drags its feet, refuses to explain coverage positions, or mishandles communications. Keep the complaint focused on conduct, dates, documents, and inconsistent claim handling. Don't turn it into a rant.

Your complaint should include:

- A timeline of events

- Copies of key letters and emails

- The denial or underpayment explanation

- A concise statement of what the insurer did wrong

- What action you want taken

Regulators won't rebuild your estimate for you. But a complaint can force the carrier to answer in writing and escalate the matter beyond the field adjuster who boxed your claim in the first place.

The carrier hates scrutiny. Use that.

Real Stories Real Results Beating the Insurance Company

People fight harder when they know someone else got through it. That's not theory. That's momentum.

I don't blame homeowners or business owners for feeling boxed in after a denial or a low offer. Carriers design the process to wear people down. The answer is proof and persistence.

A public review from a real client

This screenshot points to a real review location tied to the Raleigh office.

Reviews matter because they show what happens after the panic stage. Somebody starts out overwhelmed, the carrier controls the process, and then the balance changes once the claim is documented correctly and pushed the right way.

What winning usually looks like in the real world

Most successful disputes don't look dramatic from the outside. They look methodical.

A business owner suffers a serious property loss. The insurer's estimate comes in light. Large sections of interior work are missing. Contents handling is thin. Cleanup and build-back don't align. The adjuster treats the first draft as if it's complete.

Then the file gets rebuilt.

Independent photos. A proper scope. A sharper estimate. A written rebuttal tied to policy language. A demand for missing categories. A tighter timeline of the carrier's conduct. Suddenly the same claim looks very different because the insurer can't hide behind a vague number anymore.

That's how many low-ball claims change direction. Not because the insurer had a change of heart. Because the policyholder stopped arguing emotionally and started proving the loss item by item.

The lesson most people learn too late

You can be right and still lose if your file is weak.

You can also start in a bad position and recover if your evidence is organized, your deadlines are protected, and your dispute is framed correctly.

A few practical truths:

- The carrier's estimate is not neutral

- The first denial reason may not be the only reason they'll use

- Written records beat phone conversations

- Independent documentation provides an advantage

The people who recover more are usually the people who stop treating the insurer's first answer like a final answer.

If your claim feels stuck, you're not at the end. You're at the point where strategy starts to matter more than optimism.

Don't Accept No Take Control of Your Claim

A denied or underpaid property claim is not a verdict. It's a position taken by a company trying to protect its own money.

Your response has to be stronger than frustration. It has to be organized.

For complex claims, a multi-level pursuit strategy matters. An organized appeal can increase overturn rates by up to 60%, while internal appeals can succeed 20-40% of the time and external reviews can succeed up to 60%, according to this appeal escalation framework. Property claims have their own rules, but the lesson is clear. Escalation works better when the file is prepared properly.

Your next move should be concrete

Don't wait for the adjuster to "circle back." Do this instead:

- Request the full claim file

- Match the denial to the policy wording

- Get independent estimates and photos

- Put your dispute in writing

- Escalate when the carrier stalls

If the loss involves contamination, trauma cleanup, or specialty remediation issues that can complicate documentation, resources that explain how to navigate claims with confidence can help you understand what should be documented before the insurer narrows the claim.

And if you still think you're supposed to handle this alone, rethink that. You're up against a carrier that has adjusters, supervisors, consultants, software, and counsel built into its process. You need someone on your side who understands scope, estimating, policy language, and negotiation. If you need a plain-English overview, start with what a public adjuster does for property policyholders.

The insurance company already has representation. You should too.

If your homeowner or commercial property claim has been denied, delayed, or low-balled in North Carolina or Virginia, contact For The Public Adjusters, Inc. for a no-cost claim review. They represent policyholders, not insurance companies, and can help assess the loss, review the policy, document damages, and push back against underpayment tactics.