You paid premiums. You reported real damage. The carrier didn't deny the claim outright, which almost makes it worse, because instead they approved it and sent a check that doesn't come close to what it takes to repair the property.

That's where many homeowners and business owners get blindsided. The adjuster says the loss is covered, then points to a policy clause that often isn't explained clearly: the coinsurance rule. Suddenly the insurer says you didn't carry enough coverage for the property's value, so they're reducing payment. To the policyholder, it feels like bait and switch. In a lot of claim disputes, that's exactly how it plays out.

If you searched what is Coinsurance Rule, you're probably not curious in an abstract way. You're trying to figure out why the insurance company cut your payout and what you can do about it. Good. That's the right question, because coinsurance is one of the easiest ways for a carrier to turn an approved property claim into a low-ball fight.

Table of Contents

- Your Claim Was Approved But the Payout Is a Low-Ball Joke

- What Is the Coinsurance Rule and How Insurers Use It

- The Coinsurance Formula Insurers Use to Cut Your Payout

- Coinsurance Penalty Examples from Home and Business Claims

- How to Fight a Coinsurance Penalty and Dispute the Claim

- Avoid the Coinsurance Trap and Know When to Hire Help

Your Claim Was Approved But the Payout Is a Low-Ball Joke

A lot of property owners hit the same wall. There's a fire in the kitchen, storm damage to the roof, or a major water loss that tears through drywall, flooring, cabinets, or business space. The insurer inspects, says the claim is covered, then sends a payment that looks detached from reality.

The first reaction is usually confusion. The second is anger. Both are justified.

What happened? In many disputes, the carrier claims the building was underinsured compared to what it says the property was worth at the time of loss. Then it applies the coinsurance clause to shrink the payment. The insurer keeps the conversation technical on purpose. It throws around phrases like “insurance to value,” “required limit,” and “proportional reduction” because that language hides the simple truth: they're using policy math to pay less.

Why policyholders feel ambushed

Policyholders don't buy a homeowners policy or a commercial property policy expecting a trap door in the middle of a covered loss. They expect this: covered damage gets paid, minus the deductible, up to the policy limit. That's how common sense works.

Coinsurance changes that. It lets the carrier argue that even though the loss is covered, and even though premiums were accepted, the payment should still be reduced because the amount of insurance carried wasn't high enough compared to the insurer's valuation of the property.

The fight usually isn't just about damage. It's about value, timing, and whether the insurer is using an inflated replacement figure to justify a reduced check.

That's why a coinsurance dispute feels so personal. You did what policyholders are told to do. You bought insurance. You reported the loss. You cooperated. Then the carrier used a clause most agents barely explain to hold back money needed to rebuild.

Why you shouldn't just cash the check and move on

If the carrier applied coinsurance, you need to slow down and review the basis for that reduction. Don't assume the insurer's math is right. Don't assume its building valuation is accurate. And don't assume the adjuster's first explanation is complete.

A low-ball payment dressed up as a coinsurance penalty is still a low-ball payment.

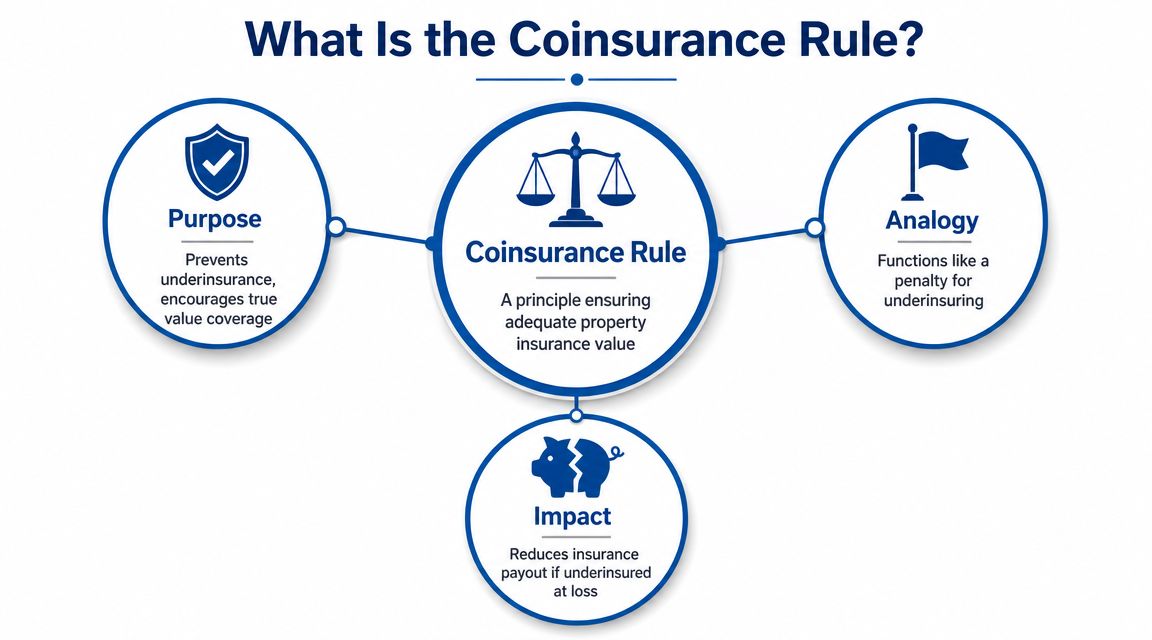

What Is the Coinsurance Rule and How Insurers Use It

Your building suffers a covered loss. The carrier agrees the claim is covered. Then the check arrives short, and the adjuster points to a clause you probably never saw explained clearly. That clause is the coinsurance rule.

The coinsurance rule is a property policy requirement that says you must insure the building to a stated percentage of its value. If the carrier says you insured it below that threshold, it cuts the payment on a partial loss. The clause gives insurers a clean-sounding excuse to pay less without denying the claim outright.

Why this clause exists at all

Insurers defend coinsurance as a pricing tool. Their position is simple. If a property is underinsured, the premium collected was too low for the amount of risk they believe they took on.

That explanation leaves out the part policyholders live through. After a loss, the clause becomes a claim-cutting device. The carrier gets to argue about what the property was worth, what amount of insurance should have been carried, and whether your limit was high enough. If the insurer can drive that value number up, your payment goes down.

That is why coinsurance disputes are usually valuation fights wearing policy language as a disguise.

Property coinsurance and health coinsurance are different

The same word causes a lot of confusion. In health insurance, coinsurance usually means the patient's share of a medical bill after the deductible. In property insurance, coinsurance is a coverage requirement tied to building value, as explained in Insureon's glossary entry on coinsurance.

If you are dealing with a house, apartment building, office, store, or warehouse claim, the dispute is about insured value and replacement cost. It is not a bill-splitting rule. It is a valuation rule that carriers use to reduce property claim payments.

That valuation fight gets even worse when the policy and estimate use different standards. If the carrier is mixing replacement cost numbers, depreciation, or outdated building figures, review the difference between actual cash value and replacement cost coverage before accepting the reduction.

How insurers use the rule against policyholders

The pattern is predictable.

First, the carrier adopts its own building value, often after the loss, when prices for labor and materials are already being debated. Next, it applies the coinsurance percentage in the policy to that value. Then it compares that required amount to the limit you carried and uses the gap to justify a smaller check.

Adjusters often present that result as automatic and final. It is neither.

A coinsurance penalty can be wrong because the insurer overstated replacement cost, used the wrong valuation date, ignored excluded costs, misstated square footage, missed code upgrade issues, or applied the clause to a category of loss where it does not belong. Policyholders lose these disputes when they argue feelings. They win them by attacking the valuation, the policy wording, and the insurer's calculation line by line.

Coinsurance is one of the insurer's favorite underpayment tools because it sounds technical, looks objective, and shifts attention away from whether the claim was valued fairly.

Treat any coinsurance reduction like a challenge, not a fact. If the carrier used the clause to shrink your payment, ask for the full valuation worksheet, the policy language it relied on, and the exact figures behind the penalty. That is where bad math and low-ball assumptions usually show up.

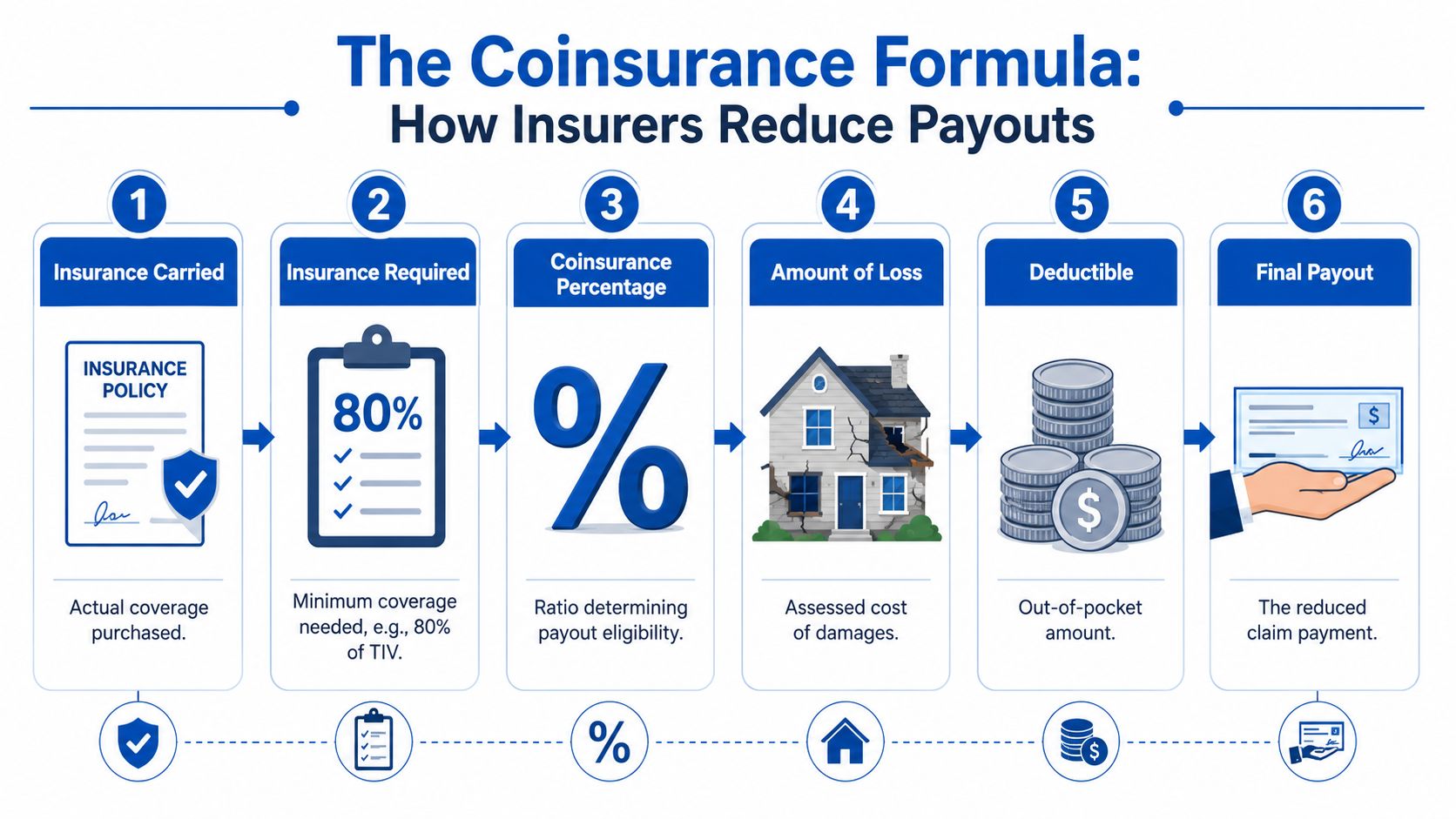

The Coinsurance Formula Insurers Use to Cut Your Payout

A lot of policyholders get blindsided here. The carrier says the loss is covered, then hides behind a formula to justify a smaller check.

Here is the formula insurers use:

(Insurance carried ÷ Insurance required) × Loss − Deductible = Payment

On paper, it looks neutral. In practice, it gives the insurer multiple places to cut your payment, especially if it inflates the value it says your property should have been insured for.

The formula in plain English

Break it into parts.

- Insurance carried means the building limit you bought.

- Insurance required means the amount the policy says you needed to carry to avoid a penalty. That figure is usually based on the property's total insurable value multiplied by the coinsurance percentage.

- Loss means the covered amount of damage under review.

- Deductible comes off after the coinsurance ratio is applied.

The pressure point is the "insurance required" number. If the insurer pushes the property value higher, the required amount rises with it. Your ratio gets worse. Your payment drops.

That is why experienced policyholders do not argue with the formula first. They attack the numbers fed into it.

A simple example

Use a clean example.

If a building's total insurable value is $100,000 and the policy has an 80% coinsurance requirement, the owner needed $80,000 in coverage to avoid a penalty on a partial loss, as explained in WSRB's coinsurance primer.

| Item | Amount |

|---|---|

| Total insurable value | $100,000 |

| Coinsurance requirement | 80% |

| Minimum insurance required | $80,000 |

If the owner carried less than that amount, the insurer reduces the payment by the same proportion. That is the whole trick. The claim can be covered, the damage can be real, and the check can still come in short because the carrier says you were underinsured.

Where to challenge the insurer's math

In this scenario, policyholders either recover money or leave it on the table.

Start with the valuation inputs, not the final payment figure. Ask for the estimate, worksheet, valuation report, and the exact policy wording the adjuster relied on. Then check each point line by line.

Use these questions:

- What value did the insurer assign to the building, and why? Demand the basis for that number.

- Did the carrier include costs that do not belong in insurable value? Land value, unsupported upgrades, and wrong components can distort the calculation.

- What valuation method applies under the policy? Replacement cost and actual cash value disputes often get stacked together. Review the difference between actual cash value and replacement cost before accepting both reductions.

- Did the insurer use the correct coinsurance percentage and form? Endorsements and special provisions can change the result.

Practical rule: If the carrier applies a coinsurance penalty, demand the valuation support before you debate the payment amount.

Insurers want this formula to look automatic. It is not. It is only as good as the assumptions behind it, and those assumptions are often where the underpayment starts.

Coinsurance Penalty Examples from Home and Business Claims

Your claim is approved. The carrier accepts the loss, then slices the payment down by saying the property should have been insured for more. That is how the coinsurance penalty blindsides people.

It hits hardest on partial losses because the insurer gets two chances to cut the check. First, it argues over repair scope and pricing. Then it applies the coinsurance clause to the reduced number and treats the result like simple math instead of a dispute about value.

Independent commercial property guidance from NAIOP's discussion of coinsurance and partial-loss underinsurance shows the basic setup. A building valued at $1 million with a 90% coinsurance requirement needs $900,000 in coverage to avoid a proportional reduction. If the insured bought less, the carrier pays only the fraction created by the purchased limit divided by the required limit.

Home partial-loss example

A kitchen fire damages part of the house. The insurer agrees the loss is covered. Then the adjuster claims the home was underinsured because the dwelling limit did not keep up with what the carrier now says the structure would cost to rebuild.

That is the trap.

A homeowner may start with a repair estimate that is already too low. Then the insurer applies a coinsurance reduction on top of it. Then the deductible comes off. By the time the check arrives, the payment can be nowhere near what it takes to do the work.

A simple version looks like this:

- The carrier says the home should have been insured to a higher amount.

- The carrier uses that higher number to claim the policy missed the required percentage.

- The carrier reduces the otherwise covered payment by that ratio.

- The homeowner is left arguing about both repair cost and building value at the same time.

That is why these claims feel rigged. The dispute is no longer just about fire, water, or storm damage. It becomes a fight over a rebuilding number the policyholder often never saw clearly during renewal.

If the dispute centers on the structure limit, review how homeowners insurance dwelling coverage works before accepting the insurer's position. That coverage line is usually where the carrier builds its coinsurance argument.

Total-loss claims expose a different underinsurance problem

In a total loss, the argument usually shifts away from a partial-loss percentage reduction and toward the hard policy limit. The policyholder still gets hit by underinsurance. The mechanics just change.

Instead of trimming a portion of the claim with a ratio, the insurer points to the cap on coverage and says that is all the money available. The financial result can be just as brutal, especially after a fire destroys an older home or commercial building that would cost much more to rebuild under current labor and material pricing.

Business property disputes get ugly fast

Commercial claims are often worse because building values change quickly and policy limits lag behind. A renewal done with stale numbers can haunt an owner after a storm, fire, or major water loss. Roof assemblies, tenant improvements, specialty finishes, and code-related rebuilding costs all become ammunition for the carrier.

Here is a significant problem in business claims. The insurer often gets to argue value after the loss using assumptions the owner never approved in any meaningful way. That gives the company room to say the building was worth more, the required insurance amount was higher, and the payout should be cut.

Policyholders should not treat that post-loss valuation as neutral. It is part of the claim fight.

Courts have recognized that coinsurance disputes often turn on valuation and policy wording, not just arithmetic. In practice, that means a home or business owner can challenge the carrier's result if the insurer used the wrong valuation date, inflated replacement cost, included items that do not belong in insurable value, or ignored endorsements that change how the clause applies.

For flood-related property disputes, the wording and framework may differ, especially under NFIP policies issued through Write Your Own carriers. The pattern is still familiar. Strict valuation language gets used to choke off payment right when the insured needs repair funds most.

How to Fight a Coinsurance Penalty and Dispute the Claim

Your claim can be approved, your damage can be obvious, and the carrier can still slash the payment by calling you underinsured. That is the coinsurance trap. The fight usually turns on one question. Did the insurer inflate the building value to create a penalty?

Start there. Force the carrier to defend every number it used.

Attack the insurer's value number

Insurance companies want this fight to look like simple math. It is usually a valuation dispute dressed up as math. If the carrier says your building should have been insured for more, make it prove that position with actual documents, not a conclusion in an adjuster email.

Demand the full valuation file in writing. Ask for the replacement cost worksheet, estimating software report, measurements, occupancy and construction assumptions, quality grade, pricing inputs, and the list of building components included in the insured value. If the company cannot show its work clearly, it should not be cutting your payment.

Then build your own record.

- Independent contractor estimate: Get a line-by-line rebuild estimate based on your actual structure, not a generic pricing model.

- Architect or building consultant review: Use this where square footage, roof design, custom finishes, tenant improvements, or code items are in dispute.

- Public adjuster estimate and policy review: A public adjuster can line up the scope, valuation, and policy language and show where the carrier stretched the numbers. If you need a practical roadmap, review this guide to disputing a low insurance claim payment.

Do not let the insurer hide behind software. Software reflects inputs. Inputs can be wrong.

Check the policy before you accept the reduction

Plenty of owners lose this argument because they rely on what the adjuster says the policy means. Get the full policy and endorsements. Read the wording the carrier is using against you.

Focus on four items:

- Coinsurance clause: Confirm the percentage and the exact wording.

- Declarations page: Verify the limit in force on the date of loss.

- Valuation condition: Check whether the policy uses replacement cost, actual cash value, or another method.

- Endorsements: Look for agreed value language, a waiver of coinsurance, margin clauses, or any form that changes the penalty.

One endorsement can change the whole dispute. If the policy language is vague or conflicting, press that issue hard. Insurers should not get to apply a harsh penalty based on muddy wording and a phone explanation.

The adjuster's summary is not the policy. If the carrier is cutting your money based on coinsurance, demand the exact clause and the exact calculation in writing.

Build a dispute package the carrier has to answer

A good challenge letter is organized, specific, and documented. Save the outrage for motivation. Use the paper trail to win.

Your dispute package should include:

- The insurer's calculation: Make the carrier commit to each step of the formula and each value used.

- Your competing valuation evidence: Contractor, architect, consultant, appraiser, or public adjuster support.

- Photos, plans, and upgrade records: Show the actual materials, layout, improvements, and pre-loss condition.

- Policy language and endorsements: Quote the wording that applies and the wording the insurer ignored.

- A direct demand for correction: Tell the carrier to remove or recalculate the coinsurance penalty and explain any refusal in writing.

Be blunt. State that you dispute the insurer's valuation, dispute the resulting penalty, and expect a revised payment decision.

If the company keeps repeating the same unsupported number, you have learned something useful. The issue is not that the reduction is automatic. The issue is that the carrier is counting on you to accept it. That is exactly why coinsurance gets used so often as an underpayment tool.

Avoid the Coinsurance Trap and Know When to Hire Help

Your claim gets approved. Then the check shows up thousands short because the carrier says you did not insure the building to the right percentage of value.

That is the coinsurance trap in real life. It turns a covered loss into a second fight over valuation, and the insurer usually controls the first number on paper. If you want to avoid that fight, or beat it when it starts, you need records, clear policy language, and outside help at the right time.

How to avoid this mess before the next loss

Prevention is cheaper than arguing with an adjuster after the damage is done. Review your limits before renewal, not after a fire, storm, or water loss exposes the gap.

Use this checklist:

- Review building limits at every renewal: Construction costs change. Your old limit can become badly outdated without you noticing.

- Update the policy after renovations or upgrades: Additions, custom finishes, tenant buildouts, and major remodels change replacement cost.

- Confirm whether coinsurance applies and at what percentage: Do not accept a vague answer from an agent or a declarations page summary.

- Get the full policy and all endorsements: The actual rule is in the policy wording, not the sales explanation.

- Ask whether agreed value, stated value, or waiver endorsements are available: Those options can reduce the insurer's ability to apply a penalty later.

- Keep proof of what the building contains: Store photos, plans, invoices, permits, and prior estimates so you can prove quality and scope if value becomes disputed.

One missed update can cost you twice. First in premium assumptions, then again at claim time.

When outside help makes sense

Hire help early if the carrier has already applied coinsurance and the file is getting technical. Waiting usually helps the insurer, not you.

Bring in support if any of this is happening:

- The carrier will not show the full calculation in writing

- Its replacement cost number is far above what local professionals support

- The repair estimate is low and the coinsurance penalty gets stacked on top

- You are being pushed to cash the check before the dispute is resolved

- The property is commercial or includes code upgrades, specialty materials, or tenant improvements

- The adjuster keeps repeating conclusions but will not answer document-based objections

At that point, you are dealing with a valuation dispute and a claim payment dispute at the same time. That takes more than a phone call.

A contractor can address rebuild cost. An architect or estimator can verify measurements, components, and finishes. A public adjuster can compare the policy language to the carrier's calculation, challenge bad assumptions, and negotiate the claim from the policyholder side. For policyholders in North Carolina and Virginia, For The Public Adjusters, Inc. handles property claim review and negotiation for homeowners and businesses dealing with underpaid damage claims.

Keep the dispute focused on the insurer's weak points

Insurers want to frame coinsurance as your mistake and their math. That frame is useful to them because it shifts attention away from whether their value number is inflated, whether their repair scope is cut down, and whether endorsements change the result.

Do not let them control the frame.

Focus on these issues instead:

- Was the building value calculated using the actual structure, materials, and finishes?

- Did the carrier include items that should not count toward the coinsurance calculation?

- Did it ignore endorsements, optional coverages, or valuation terms that limit the penalty?

- Did it understate the covered damage before applying the penalty?

- Did it provide the exact written basis for each number used?

If the adjuster says the penalty is automatic, inspect every assumption in the file. Automatic is what insurers say when they do not want the numbers challenged.

The hard truth about coinsurance disputes

Coinsurance is one of the cleanest tools carriers use to underpay a valid property claim. The math gives the reduction a false air of certainty, even when the underlying valuation is weak.

That is why delay hurts you. So does confusion. So does accepting a summary instead of demanding the actual clause, the full calculation, and the support for every number.

Get the policy. Get the endorsements. Get an independent valuation review. Put your dispute in writing. If the claim is large, technical, or stuck, bring in someone who represents policyholders.

If your home, dwelling, or business property claim was reduced because of coinsurance, don't assume the insurance company got it right. For The Public Adjusters, Inc. helps homeowners and business owners review policy language, challenge inflated valuation assumptions, document damage properly, and dispute underpaid property claims. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!