You've already done the hard part. You paid for coverage, reported the damage, answered questions, sent photos, and waited. Then the insurance company came back with a denial, a thin estimate, or weeks of silence while your house or business property sits torn up.

That's where a common challenge arises. Claimants assume the insurer's first number is final, or they get worn down by delays and repeated document requests. It isn't final. And if you're trying to figure out how to dispute an insurance claim, especially a homeowner or commercial property claim, you need to stop treating this like a customer service problem and start treating it like a documented business dispute.

A property claim fight usually isn't about whether damage happened. It's about scope, price, depreciation, exclusions, and delay tactics. That's why the smartest move is to challenge the file, not just complain about the outcome.

Table of Contents

- Your Claim Was Denied or Low-Balled Now What

- Analyze the Insurer's Math and Excuses

- Build an Evidence File They Cannot Ignore

- Master the Art of the Appeal and Negotiation

- What to Do When the Insurance Company Goes Silent

- Escalate Your Fight Get a Public Adjuster on Your Side

- Conclusion Take Control of Your Property Claim

Your Claim Was Denied or Low-Balled Now What

You open the letter thinking it's finally the help you've been waiting for. Instead, you get a payment that won't cover the work, a denial packed with policy language, or another vague explanation that somehow says a major loss is worth far less than any contractor would ever charge.

That reaction in your gut is usually right. Something is off.

This isn't rare bad luck. It's part of the normal claims process. In 2024, 65.2% of closed insurance complaints involved claim handling, and the most common issues were delays (22.2%) and unsatisfactory settlements or offers (12.2%), according to ValuePenguin's review of insurance complaint patterns.

Your first offer is often just the opening position

Insurance companies know most policyholders don't speak estimate language, don't read exclusions closely, and don't keep a clean paper trail. That's why a weak first response works so often. If you accept it, the file closes. If you don't challenge it properly, they can say you never supported your disagreement.

A denied claim or low-ball offer doesn't automatically mean the carrier is right. It often means the file was built in the insurer's favor.

Practical rule: Don't respond emotionally. Respond in writing, with documents, line items, and dates.

The real fight is usually about payment, not coverage alone

Homeowner and business property claims often get framed the wrong way. People think, “They denied me.” But a lot of disputes are really these problems:

- Missing scope: The estimate leaves out demolition, drying, code work, detach and reset, or finish matching.

- Thin pricing: The carrier's numbers don't reflect what qualified local contractors will charge.

- Depreciation abuse: They subtract value too aggressively, then act like the reduced figure is fair.

- Delay pressure: They drag things out until you're tempted to take whatever is on the table.

If you're learning how to dispute an insurance claim, understand this early. You are not begging for help. You are enforcing the policy you bought.

What to do first

Before you argue with anyone, do three things:

- Read the letter twice. Find the exact reason for the denial, reduction, or delay.

- Pull the estimate apart. Look for what's missing, underpriced, or misclassified.

- Stop relying on phone calls. A claim dispute without a written record is a weak dispute.

The insurer's first response is not the end of the claim. It's the first version of the fight.

Analyze the Insurer's Math and Excuses

Most bad claim outcomes hide behind paperwork that looks official. Don't let the formatting fool you. An estimate can be detailed and still be wrong. A denial letter can sound authoritative and still misapply the policy.

Property disputes often center on valuation, fair market value, depreciation formulas, and scope of repairs, and insurers often accept that a loss occurred while undervaluing what it takes to make the policyholder whole, as noted by United Policyholders in its guidance on resolving claim disputes.

Read the estimate like a contractor, not a customer

Start with the carrier's scope. Line by line. Room by room. Trade by trade.

Look for obvious omissions first. If there was water damage, did they include tear-out, drying-related work, insulation removal, baseboards, paint to full affected surfaces, and material replacement that matches what was there? If it's a storm loss, did they include all damaged elevations, flashing, underlayment, vents, accessories, and debris handling?

Then check pricing logic. An insurer may include a task but price it so low that the line item becomes meaningless.

Here's what deserves scrutiny:

- Depreciation entries that feel automatic instead of reasoned

- Partial repair assumptions where full replacement is more realistic

- Category mismatches where commercial-grade materials are priced like basic residential finishes

- Labor gaps for setup, protection, detach and reset, cleaning, or disposal

If you need a better handle on how insurers reduce payouts through valuation methods, read this breakdown of actual cash value in insurance.

Match every excuse to policy language

If the insurer says “wear and tear,” “long-term seepage,” “pre-existing damage,” or “not covered under the policy,” make them tie that claim to actual policy wording. Not a summary. Not an adjuster's paraphrase. The actual language.

Use this simple review method:

| What to review | What to look for |

|---|---|

| Denial or payment letter | Exact reason given for limiting payment |

| Policy form | The cited exclusion, condition, or limitation |

| Estimate | Missing items, underpriced items, wrong quantities |

| Photos and site facts | Proof that the field conditions don't match the carrier's assumptions |

Common low-ball patterns

A lot of underpayment files follow the same script.

The carrier agrees something happened, then shrinks the scope until the number looks manageable.

That's why “how to dispute insurance claim” questions so often come down to math, not just law. You're challenging the carrier's version of the loss. If their estimate says spot repair works and your contractor says full replacement is required, the issue is no longer abstract. It's a line-item dispute supported by facts.

Don't send a vague response saying the offer is unfair. Send a rebuttal that says, in effect, “Line 27 omits this. Line 41 underprices that. Your depreciation on these items is unsupported. Your exclusion doesn't fit the documented cause of loss.”

That's how you turn their excuse into your roadmap.

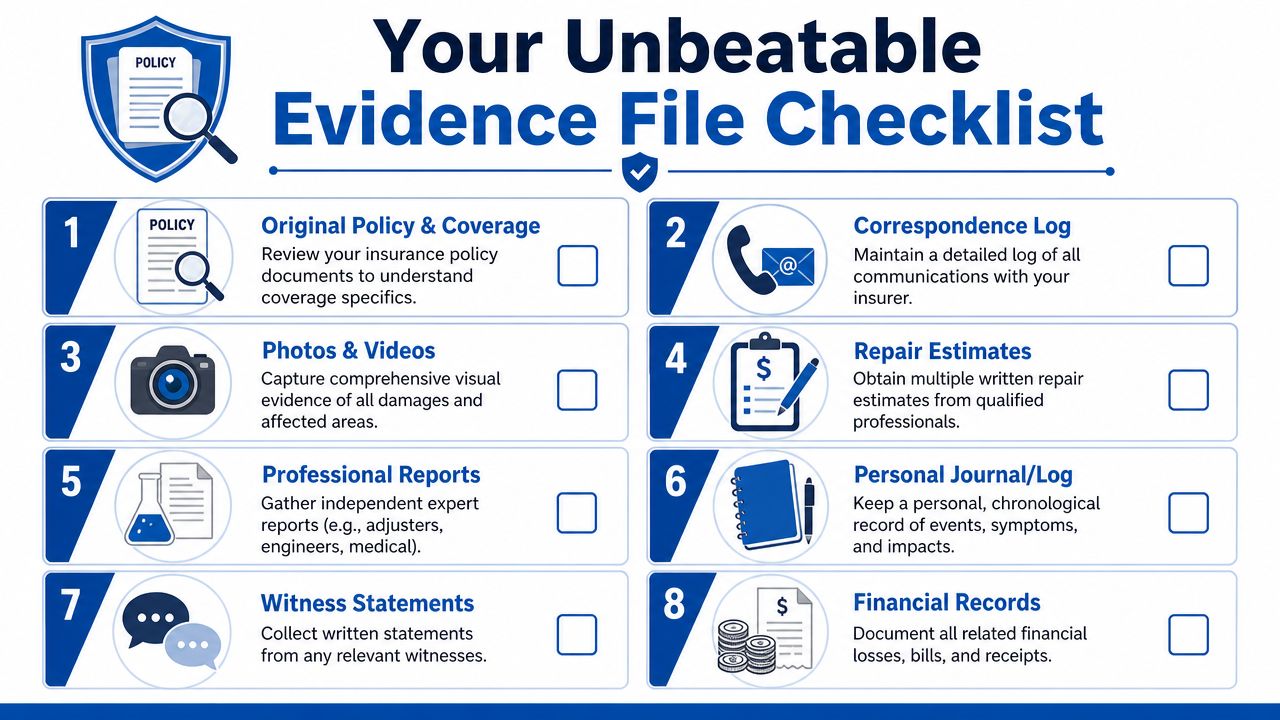

Build an Evidence File They Cannot Ignore

Most policyholders weaken their position because they keep the claim in conversation form. Calls. Voicemails. Frustrated emails. Verbal promises. None of that is enough when the carrier decides to dig in.

A serious dispute needs a serious file. Treat the insurer's first response like a failed audit of your damage. Then rebuild the record so cleanly that every weak spot in their position is exposed.

Practitioner guidance on disputing insurance claims recommends rebuilding the file with itemized photos, estimates, and a timeline that directly rebuts the stated reason for denial, and notes that deadlines are often short, commonly 30 to 60 days from the denial, with certified mail used to preserve the record, as explained in this guide on how to dispute insurance claims.

What belongs in a real dispute file

You need more than a few damage photos. You need a file that answers every question before the insurer asks it again.

Build it with these categories:

- Policy papers: Declarations page, endorsements, exclusions, and any carrier letters.

- Damage visuals: Wide shots, close-ups, elevation views, room-by-room photos, and video walkthroughs.

- Repair estimates: Independent, itemized estimates from qualified contractors. Not napkin totals.

- Contents support: Model numbers, receipts, photos, age, condition, and replacement information where available.

- Cause and condition records: Moisture readings, mitigation invoices, roofer findings, leak tracing, engineer or consultant reports if needed.

- Communication log: Date, time, person, title, phone number, email, and what was said.

- Timeline: Date of loss, inspection dates, document submissions, follow-ups, and payment or denial dates.

Your communication log matters more than people think

If the insurer rotates adjusters, claims they never received something, or changes explanations, your log becomes a weapon.

Keep it simple and consistent:

- Record every contact the same day

- Save every email as a PDF

- Confirm every phone conversation in writing

- Track every document you sent and how you sent it

If it isn't documented, the insurer can act like it never happened.

Build a rebuttal package, not a document dump

Don't just send a giant pile of attachments. Organize them so the carrier has to confront the issue.

A good package might look like this:

| Section | What it does |

|---|---|

| Cover letter | States the dispute clearly and requests revised review |

| Issue list | Identifies each denial point or underpaid item |

| Supporting estimate | Shows corrected scope and pricing |

| Photo index | Ties visuals to disputed line items |

| Timeline | Proves responsiveness and carrier delay or inconsistency |

| Backup documents | Invoices, reports, receipts, prior emails, and logs |

Use certified delivery and keep control of deadlines

Property claims get weaker when policyholders miss appeal windows or rely on “I left a message” as proof. Send the dispute in a way that creates a record. Certified mail works. So does another method that gives you proof of delivery and a complete submission copy.

Your file should do one job. It should make it hard for the insurer to say no without exposing exactly why they're saying no.

That shifts the advantage.

Master the Art of the Appeal and Negotiation

A good appeal doesn't rant. It corners. It answers the insurer's position point by point and leaves less room for hand-waving.

Start with a clean written appeal. Name the claim number, property address, date of loss, and the exact letter or estimate you're disputing. Then list each problem in plain English. Missing roof items. Improper depreciation. Incomplete water mitigation scope. Unsupported exclusion. Underpriced interior repairs.

What a strong appeal letter actually does

A strong appeal has structure. It doesn't wander.

Use this format:

- State the dispute clearly: Say whether you're disputing a denial, partial denial, scope, depreciation, or underpayment.

- Quote the insurer's reason: Use their words from the letter or estimate.

- Refute each point: Attach photos, contractor findings, invoices, and line-item corrections.

- Request specific action: Reinspect the property, revise the estimate, reverse the denial, or issue supplemental payment.

- Set a written response expectation: Ask for a written coverage or payment position.

If you need more guidance on handling the back-and-forth, this article on how to negotiate with an insurance adjuster is worth reading.

What to say and what not to say

Negotiation is where people accidentally weaken their own claim. They start guessing, softening, or arguing from frustration instead of evidence.

Use these habits:

- Stick to documents: “Please see attached estimate and photo references for the omitted items.”

- Ask direct questions: “What policy language supports this reduction?”

- Request written answers: Don't accept major claim decisions by phone alone.

Avoid these mistakes:

- Don't speculate: If you're unsure about cause, don't guess.

- Don't minimize damage: Casual comments get used against you.

- Don't accept verbal reassurances: Friendly isn't binding.

Negotiation rule: Never argue feelings against an estimate. Argue facts against line items.

A helpful visual explanation can make this easier to apply in practice:

Push for revision, not conversation

Your goal is not to have a pleasant call. Your goal is to force movement in the claim. Ask for a reinspection when the estimate is wrong. Ask for a revised scope when major items are omitted. Ask for the exact basis of any depreciation or causation split.

When you learn how to dispute an insurance claim the right way, you stop saying “This doesn't seem fair” and start saying “Your estimate omits these items, misprices these repairs, and fails to address the attached support.”

That's when negotiations start getting serious.

What to Do When the Insurance Company Goes Silent

Silence is its own tactic. Some carriers won't issue a clean denial because a denial gives you something concrete to attack. Instead, they drag the file through endless “review,” rotate adjusters, ask for the same records twice, and leave you stuck in claim limbo.

That kind of stalling wears people down. It also creates confusion. Homeowners and business owners start wondering whether they're supposed to wait, resend documents, or start over with the new desk adjuster who just inherited the file.

Guidance on claim appeals and regulator escalation notes that many policyholders face long-running delays rather than a clean denial, and that a key strategy is to build a timeline of carrier inaction, demand a written coverage position, and identify when escalation to a state regulator is appropriate, as discussed in the NAIC consumer guidance on appealing an insurance claim denial.

Know the difference between review and stalling

Not every delay is misconduct. Some claims do take time. But repeated unexplained delay is a different problem.

Watch for these patterns:

- Adjuster rotation: You explain the file again and again because the contact person keeps changing.

- Repeat requests: The carrier asks for documents you already sent and can prove you sent.

- No written position: They discuss the claim vaguely but won't commit in writing.

- Partial communication: They respond just enough to keep the file alive, but not enough to resolve anything.

When those patterns stack up, don't keep chasing them informally.

Build a delay timeline that creates pressure

A delay timeline should read like a clean business record, not a complaint diary.

Include:

| Date | Carrier action or inaction | Your response |

|---|---|---|

| Date claim reported | Claim opened | Initial documents submitted |

| Inspection date | Site inspected | Follow-up sent |

| Document request date | Requested items | Date you provided them |

| Follow-up date | No response received | Written reminder sent |

| Reassignment date | New adjuster assigned | Prior records resent |

This timeline matters because it shows a pattern. Not one missed call. A pattern.

Send a written demand for a coverage position when the carrier keeps talking around the issue.

Ask for a written coverage position

This is one of the most useful moves in a delayed property claim. Don't just ask, “Any updates?” Ask for a written coverage position and identify what remains unresolved.

Your letter should:

- Identify the claim and date of loss

- List what you already submitted

- State the unanswered issues

- Ask the insurer to confirm its position in writing

- Set a reasonable deadline for response

That forces the carrier to either move the file or create a record of continued nonresponse.

When delay starts looking like bad faith

If the insurer keeps collecting information but refuses to make a clear decision, you may be dealing with more than inefficiency. You may be dealing with conduct that needs escalation.

At that point, consider these options:

- Regulator complaint: Useful when the carrier won't communicate or follow process.

- Formal professional representation: Useful when the file has become technical or adversarial.

- Legal review: Useful when delay is extreme, coverage is being manipulated, or the damage is substantial.

Don't let silence control the pace of your recovery. Put the delay on paper, make the carrier answer, and preserve every missed step.

Escalate Your Fight Get a Public Adjuster on Your Side

Your roof is still tarped, your contractor says the insurer missed half the damage, and now a new desk adjuster wants documents you already sent twice. At that point, you do not have a simple claim. You have a valuation fight, and the carrier is betting you will get tired before they correct the number.

That is when bringing in a public adjuster starts making sense.

The company has people trained to protect its payout. You should have someone trained to protect your claim. A public adjuster represents the policyholder, not the insurance company. If you want a clearer breakdown of that role, read what a public adjuster does during a property claim dispute.

Who a public adjuster works for

| Role | Company Adjuster | Public Adjuster |

|---|---|---|

| Who they represent | The insurer | The policyholder |

| Primary job | Evaluate the claim for the carrier | Document, price, and negotiate the claim for you |

| Estimate approach | Starts with the carrier's scope and limits | Builds an independent scope based on the actual damage |

| Communication role | Defends the carrier's position | Challenges omissions, underpricing, and delay |

| Dispute support | Limited by company process | Supports supplements, rebuttals, and negotiation |

This matters most in underpayment and delay cases. A denial is obvious. A low-ball estimate hides behind line items, depreciation, excluded rooms, and vague notes like "repair instead of replace." A public adjuster knows where carriers shave the claim and how to force those issues into writing.

What changes when a professional steps in

A good public adjuster improves the file and changes the pressure on the insurer.

That usually includes:

- A fresh inspection: damaged materials, missed rooms, code-related items, and secondary damage get documented from your side

- A real scope of loss: the estimate is rebuilt to reflect the full repair, not the carrier's trimmed version

- Line-by-line valuation challenges: low pricing, missing labor, and unsupported depreciation get called out directly

- Policy-based negotiation: coverage language gets tied to the actual facts and repair needs

- A single point of pressure: the carrier stops getting away with repeating the same weak explanations to an exhausted policyholder

That last point matters. Insurers drag claims out because delay works. It wears people down. Professional representation cuts into that advantage.

A strong claim file makes underpayment harder to defend and delay harder to hide.

When handling it yourself stops being smart

Some claims can be managed without outside help. Small, straightforward disputes sometimes respond to a clean supplement and a firm written rebuttal.

Escalate if the carrier is doing any of the following:

- leaving obvious damage out of the estimate

- paying for patchwork repairs when replacement is justified

- reassigning adjusters and making you restart the file

- delaying decisions while asking for the same records again

- using technical language to shrink scope or value

- pushing a number that does not match contractor pricing or actual repair needs

Homeowners and business owners usually wait too long. They keep assuming one more phone call will fix it. It usually does not.

For policyholders in North Carolina and Virginia, For The Public Adjusters, Inc. is a licensed firm that represents homeowners and businesses in property damage disputes involving fire, water, wind, hail, hurricanes, tornadoes, theft, and vandalism.

If the insurer has turned your claim into a grind, stop treating it like a customer service problem. Treat it like a negotiation over money, scope, and proof. That is what it is.

Conclusion Take Control of Your Property Claim

You don't have to accept a bad estimate, a shaky denial, or endless delay as normal. You do have to respond the right way. Read the insurer's position closely. Break down the math. Build a file that proves the scope and cost of repair. Put everything in writing. Make the carrier answer specific points.

That's how you take control back.

A property claim dispute is usually won by the side with the better documentation, the better estimate, and the better paper trail. If you stay organized and aggressive, a low-ball offer can be challenged. A denial can be appealed. A stalled file can be forced toward a written decision.

Your policy is a contract. The insurer doesn't get to treat it like a suggestion. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your homeowner or business property claim was denied, delayed, or low-balled, For The Public Adjusters, Inc. can help review the damage, organize the evidence, and push back against underpayment with a documented claim dispute strategy.