Let’s get straight to it. Actual Cash Value (ACV) is what your damaged property was worth the second before it was destroyed.

Think of it like the Kelley Blue Book value for your car. It’s not what you’d pay for a shiny new one on the lot; it’s the used, real-world value. Insurance giants like State Farm and Allstate love this calculation because it’s a built-in strategy to pay you less and protect their bottom line.

How Your Insurer's Math Leaves You Holding the Bill

On paper, the insurance company will tell you that Actual Cash Value is a simple formula: the cost to replace something new, minus depreciation for its age and condition.

But that little minus sign creates a massive, often devastating, gap between the settlement check they send you and the actual money you need to fix your home. This is where the conflict of interest smacks you in the face. The same company that has to pay the claim gets to decide how much that claim is worth.

Imagine a hailstorm wrecks your five-year-old roof. You might think, "Great, my insurance will buy me a new roof." Not with an ACV policy.

- They don't pay for a new roof. They pay for a five-year-old roof.

- You eat the difference. That depreciation they subtract comes straight out of your pocket. It's on you to cover the gap to make yourself whole again.

- The math is rigged. The adjuster’s assessment of "wear and tear" can be brutally aggressive, always in the insurer's favor, shrinking your payout even more.

The Financial Gap Between ACV and RCV Settlements

This table shows the real-world financial difference between an Actual Cash Value (ACV) and a Replacement Cost Value (RCV) settlement for a typical roof damage claim. It's a clear picture of the payout gap homeowners often have to cover themselves.

| Metric | Replacement Cost Value (RCV) | Actual Cash Value (ACV) |

|---|---|---|

| Cost to Replace Roof Today | $18,000 | $18,000 |

| Roof Age | 5 years (out of 20-year lifespan) | 5 years (out of 20-year lifespan) |

| Total Depreciation (25%) | -$4,500 (Recoverable) | -$4,500 (Your Out-of-Pocket Cost) |

| Initial Payout (ACV) | $13,500 | $13,500 |

| Recoverable Depreciation Paid After Repairs | $4,500 | $0 |

| Total Payout After Repairs | $18,000 | $13,500 |

| Your Out-of-Pocket Expense (Excluding Deductible) | $0 | $4,500 |

As you can see, with an ACV policy, that $4,500 gap is your problem, not the insurance company's. This is how a "covered loss" still leaves you with a massive bill.

What This Looks Like in Real Life

This isn't some textbook theory. When Hurricane Florence tore through North Carolina, thousands of homeowners got a brutal education in ACV.

Let's say their five-year-old roof originally cost $15,000. With today’s inflated material and labor costs, replacing it now costs $18,000. The insurance company takes that $18,000, subtracts years of depreciation, and cuts a check for just $13,500 (before your deductible, of course).

FEMA data showed that a staggering 40% of claims in storm-ravaged areas like NC were settled on an ACV basis. This forced families to drain savings, take out loans, or leave repairs unfinished, all because of the policy they thought would protect them.

This is a classic underpayment tactic. It’s why you absolutely must understand the difference between valuation methods. For a deeper dive into this fight, check out our guide on how ACV vs. RCV policies can make or break your recovery. It's the first step in arming yourself against a lowball settlement.

The Hidden Math Insurers Use to Lower Your Payout

Ever stared at a settlement offer and felt that punch-in-the-gut feeling? The number is so low it feels like a slap in the face. You’re not alone. Insurance companies have a whole playbook of obscure, self-serving formulas to calculate the Actual Cash Value (ACV) of your damaged property, and trust me, these calculations are designed to protect their bottom line, not yours.

They’ll show you a simple formula, pretending it’s all straightforward. But the math they’re really using behind the scenes is anything but. The most common trick is Replacement Cost Value (RCV) less Depreciation. But don't be surprised if they pivot to a "Fair Market Value" approach or the intentionally vague "Broad Evidence Rule" when it saves them money. Each method is a lever for the adjuster to pull to aggressively devalue your property.

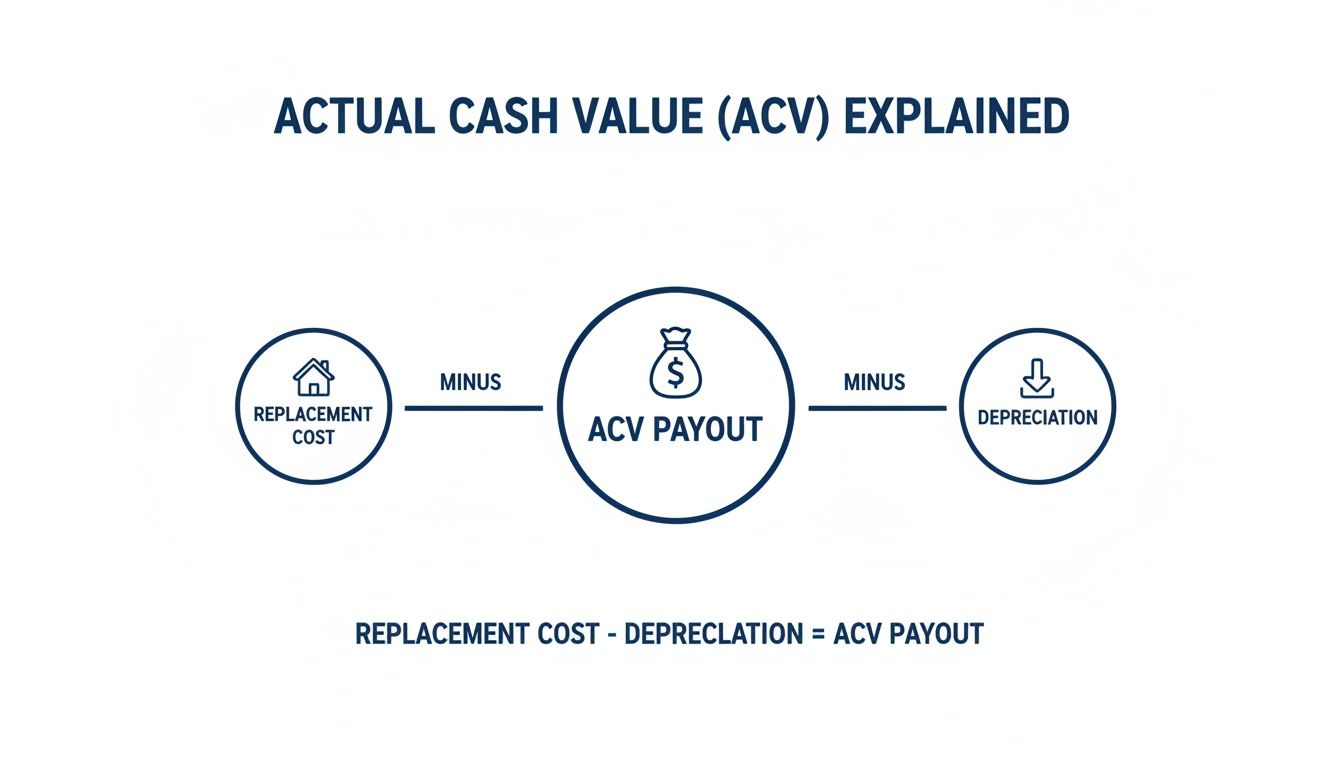

Here's the basic, almost deceptive, formula they want you to see.

The clean look of this graphic hides a dirty secret: the way insurance companies calculate that "depreciation" number is often where they gut your claim.

How Depreciation Becomes a Weapon

Here’s how it plays out in the real world. The insurance adjuster applies an aggressive, straight-line depreciation across everything—your roof, your floors, your siding, your personal belongings—based on little more than its age.

Imagine your beautiful 10-year-old kitchen. You've meticulously maintained it, maybe even upgraded the countertops a few years back. To an adjuster armed with a simple age-based formula, it's just "old." They can depreciate its value down to almost nothing, completely ignoring its actual condition and the hard-earned money you invested.

This isn’t just a scare tactic; it’s a reality we see every day. After the devastating 2011 Joplin, Missouri tornado, one family’s home, with a $300,000 replacement cost, was completely destroyed. The insurer slapped a 40% depreciation on it based on age alone, leaving them with a payout of just $180,000. FEMA audits later confirmed that in disaster zones, ACV claims averaged 28% less than RCV—a crippling financial blow for families desperate to rebuild.

Their initial ACV calculation is not a final decision—it's an opening offer. You have the right to challenge their numbers, and you absolutely should.

This is why you have to scrutinize every single part of their calculation. For big-ticket items like your roof, understanding recoverable depreciation in roofing claims can be the difference between a proper repair and a cheap patch job.

Don't let the insurance company's low-ball offer be the last word. Their math is just the start of a negotiation, and you need to be ready to fight back. Learn more about how to dispute their numbers in our deep dive on depreciation on insurance claims.

How ACV Policies Can Kill Your Business

If an Actual Cash Value policy is a financial punch in the gut for a homeowner, it’s an absolute death blow for a business. The same low-ball games insurers play on residential claims get amplified tenfold in the commercial world, where they aggressively depreciate every single thing that keeps your doors open.

This isn't just about a worn-out roof anymore. We're talking about your specialized production machinery, the computer network that runs your entire operation, and your shelves full of inventory. The insurance company knows if you can't replace these core assets fast, your business will bleed out—losing revenue, customers, and eventually, its pulse. The "savings" on that cheaper ACV premium? It's a high-stakes bet where you're gambling with your entire livelihood.

A Virginia Business Pushed to the Brink

Let's look at a scenario we see all the time. A commercial property owner in Virginia gets hit with catastrophic water damage. Their inventory and point-of-sale computer systems, which they bought for $50,000 just three years ago, are fried. To replace them today with comparable tech will cost $60,000.

But under their ACV policy, the insurance company couldn't care less about the replacement cost. Instead, they weaponize depreciation. Citing age, use, and "technological obsolescence," they slap the business with a massive $20,000 depreciation hit. The final check they cut? A measly $25,000—less than half of what the business actually needs to get back up and running.

This isn't some rare, worst-case scenario. This exact playbook was used in over 60% of U.S. commercial property claims in 2022. The data is damning: ACV policies resulted in average payouts 35% below what businesses needed to recover, leaving them high and dry. If you want a peek at how insurers cook the books, you can learn more about the technical definition of actual cash value and see their strategy for yourself.

Why You Need a Public Adjuster in Your Corner

When that first low-ball ACV offer lands—and it's not even close to enough to reopen your doors—your company's future is on the line. This is the exact moment a public adjuster becomes the most critical asset for a business owner.

Our job is to systematically dismantle the insurance company’s bogus valuation. We come in and bring our own team of experts to:

- Properly value specialized commercial equipment, shutting down their absurd depreciation schedules.

- Document every penny of your business interruption losses, a massive cost that insurers love to ignore or downplay.

- Go to war against the delay and deny tactics, forcing the carrier to stop stalling and start negotiating fairly.

Without a real expert fighting for you, your business is at the complete mercy of an insurance carrier whose profits depend on underpaying you. We level the playing field so you can get the capital you’re owed to make a full, fast recovery.

How a Public adjuster Fights Unfair ACV Calculations

When an insurance company like State Farm or Allstate slides a low-ball settlement offer across the table, it’s not an honest mistake—it’s a business strategy. They are betting you won’t have the energy, the expertise, or the resources to fight back. This is where a public adjuster flips the script and dismantles their weak arguments with facts, evidence, and an unwavering commitment to getting you paid what you're owed.

We don't just "review" the insurer's numbers; we throw them out and start from scratch. An experienced public adjuster doesn’t play defense. We build our own offensive case from the ground up, forcing the carrier to justify every single penny they tried to withhold.

Building an Ironclad Counter-Offensive

Let’s be clear: the insurance company's adjuster works for them. Their job is to minimize the payout. A public adjuster works only for you, and our entire process is designed to maximize it.

Here’s how we systematically break down their low-ball offer:

- Independent, Line-by-Line Damage Assessment: We conduct our own exhaustive inspection of the damage. We create a detailed scope of loss that almost always uncovers damages the company adjuster conveniently overlooked or ignored.

- Documenting Pre-Loss Condition: We dig for evidence. This means finding maintenance records, receipts for upgrades, and pre-loss photographs to prove the actual condition and quality of your property. This directly counters their aggressive and often baseless depreciation claims.

- Accurate Replacement Cost Research: We don't accept the numbers spit out by the insurer's outdated pricing software. We research current, local material and labor costs to establish a true, real-world replacement value for everything that was damaged.

By taking these steps, we expose the flaws in their initial assessment of what is actual cash value and build a powerful, undeniable case for a much higher settlement. For a more detailed look at our role, you can explore our guide on what a public adjuster does to fight for you.

Case Study: Raleigh Smoke Damage Claim Ignored

A homeowner in Raleigh recently had their world turned upside down by a kitchen fire that caused significant smoke damage. Their insurance company's adjuster rushed through the inspection, treating their beautiful custom cabinetry and high-end stainless-steel appliances like cheap, builder-grade junk.

They slapped a heavy depreciation schedule on everything, resulting in a shockingly low ACV offer. It wouldn't have covered even half the cost of proper restoration.

Our team stepped in and immediately went to work. We documented the superior quality of the materials, sourced receipts for recent appliance upgrades, and proved the homeowner's meticulous maintenance over the years. We presented an undeniable case that the insurer’s depreciation was not only unfair but completely unsupported by the facts.

The result? We forced the insurance company to completely re-evaluate their calculation. After our aggressive negotiation, the final settlement was over 60% higher than their initial insulting offer. This wasn't just about getting more money; it was about forcing the insurer to honor the actual value of our client's property and pay what they rightfully owed. This is the tangible difference a dedicated advocate makes in the fight for a fair claim.

From Low-Balled to Fully Paid: A Real Client's Story

Theory is one thing, but seeing how this fight plays out for a real homeowner hits differently. It’s easy to feel totally alone when your insurance company's adjuster looks you in the eye, dismisses your concerns, and slides a laughably low offer across the table.

But you are not alone in this battle.

So many of our clients find us after hitting a brick wall with their insurer. They’re stressed out, exhausted, and have no idea what to do next. They’ve been delayed, denied, and handed an Actual Cash Value settlement that wouldn’t even begin to cover the real cost of repairs. They feel defeated, convinced the insurance company holds all the power.

Here’s a review from a client who was in that exact spot, staring down a frustrating and fundamentally unfair claims process.

This isn't a one-off story; it’s a textbook example of a common insurance company tactic. The carrier’s adjuster was dismissive and came in with a rock-bottom ACV offer, hoping to leave the homeowner holding the bag for a massive financial burden.

Turning the Tables on the Insurer

This is where we come in. Once we were hired, we immediately took over all communication, shielding the homeowner from the stress of fighting an adjuster who clearly wasn't listening. We changed the entire dynamic of the claim.

Our process was simple but aggressive:

- We re-documented everything. Our team conducted a new, far more thorough inspection, uncovering significant damage the insurance company’s adjuster had conveniently “missed.”

- We tore apart their unfair ACV. We didn’t just disagree with their numbers; we fought back against the aggressive depreciation with hard evidence, industry data, and professional estimates to prove the true value of their property.

- We negotiated from a position of power. We didn't just ask for more money. We built an ironclad case that forced the insurer to abandon their low-ball games and pay the full settlement our client was owed under their policy.

This story takes a claim from the brink of disaster to a total success. It’s proof that with the right expert advocate in your corner, you absolutely can fight back against an insurer's unfair determination of what is actual cash value—and win.

Your Action Plan for Disputing a Low ACV Offer

Getting that low-ball settlement offer from your insurance company can feel like a punch to the gut. It's designed to make you feel defeated.

Don't fall for it.

That offer isn't the final word. It's the insurance company's opening shot in a negotiation—and you've got to be ready to fight back. What you do next is absolutely critical to protecting your right to get paid what you're truly owed.

The second you receive that check and the ACV breakdown, your game plan needs to kick in. You have to be methodical. Don't let the adjuster pressure you into making a fast decision that only benefits their bottom line.

Your First Moves Matter Most

How you respond right now sets the tone for the entire fight. Follow these steps to take back control of the claim and start building your case for a fair payout.

Do Not Cash the Check. Do Not Sign Anything. This is non-negotiable. Cashing that check or signing any kind of release form is exactly what they want you to do. Legally, it can be seen as you accepting their garbage offer, which slams the door shut on your claim. Put the check away and refuse to sign a single thing.

Demand a Line-by-Line Written Explanation. Fire off a written request—email is fine—for a complete, detailed breakdown from the adjuster. They are required to show their math. You need to see how they calculated the replacement cost and the depreciation for every single item. Vague excuses or summary numbers are not good enough.

Gather Your Counter-Evidence. Now it's your turn to prove them wrong. Dig up every piece of evidence you have: pre-loss photos of your home, receipts for that new flooring or those new appliances, and any maintenance records you can find. This is the proof that directly contradicts an adjuster's attempt to claim excessive "wear and tear."

Knowing how to talk to your insurance company is a skill, and it's one you need to learn fast when you're preparing to dispute their numbers.

Your most powerful next step is to get a professional second opinion. Contact a licensed public adjuster for a no-cost claim review. An expert will immediately spot where the insurer’s math is wrong and give you the professional leverage you need to fight back and win.

Common Questions About Fighting an Unfair ACV Settlement

Going head-to-head with an insurance company over your Actual Cash Value claim is designed to be confusing and exhausting. They're banking on you giving up and accepting their low-ball number. Here are the straight answers to the questions we hear from policyholders every single day.

Can I Really Dispute the Depreciation My Insurer Calculated?

Absolutely. The depreciation figure your insurance adjuster comes up with isn't a hard fact—it's their opinion, and it's an opinion crafted to pay you as little as possible.

This is where the fight really begins. A public adjuster will dismantle their weak argument by building a strong one for you. We gather the real evidence: maintenance records showing how well you cared for your property, photos from before the damage, and receipts for any upgrades or improvements you made. We use industry-standard data and expert analysis to expose their low-ball math and demand a valuation based on the actual condition and quality of your property.

My Policy Says ACV. Am I Just Stuck with Their Number?

Not necessarily. The policy language is the starting point, but it's not the end of the story. The real battle is over how that language gets interpreted and applied to your specific loss.

We can successfully argue that the insurance company's method for calculating ACV doesn't actually make you whole again, which is the fundamental promise of an insurance policy. The key is proving the true value and pre-loss condition of your property to force their hand and challenge that initial low-ball offer.

What's the Difference Between Fair Market Value and ACV?

This is a sneaky trap insurance companies love to use. They are not the same thing, and confusing them can cost you thousands.

Fair Market Value (FMV) is what someone would pay to buy your entire property on the open market. This number is often much lower because it gets dragged down by things like land value, location, and neighborhood comps—factors that have absolutely nothing to do with the cost of rebuilding your home.

Actual Cash Value (ACV) is supposed to be about one thing only: the cost to replace what was damaged, minus a fair amount for depreciation.

Insurers will sometimes try to slip in a low FMV appraisal to justify a tiny payout for your structural damage. A good public adjuster shuts that down immediately. We force them to base the settlement on the real-world cost to repair or replace what you lost, because that’s what your policy is actually for.

When your insurance company’s math doesn't add up, you need an expert on your side to fight for every dollar you're owed. The team at For The Public Adjusters, Inc. offers a no-cost claim review to show you exactly how to dispute an unfair ACV settlement. Visit us at https://forthepublicadjusters.com to get the help you deserve.