A Replacement Cost Endorsement is an insurance add-on that pays the full cost to repair or replace damaged property with new items of similar kind and quality—without deducting depreciation. This means you’re reimbursed based on current market prices, not the lower “actual cash value.” It’s commonly used for major losses like roof replacements, stolen electronics, or rebuilding a home after disasters such as fires or storms.

You opened your claim expecting help and got a spreadsheet instead. The carrier’s adjuster inspected your property, ran numbers through estimating software, and sent over an offer that doesn’t come close to what your contractor says it will take to repair or rebuild. If you have a replacement cost endorsement, that low-ball offer feels even worse, because you thought that endorsement meant the insurer had to pay what the work costs.

That frustration is justified. Insurance companies know most policyholders don’t speak policy language, don’t know how depreciation is being used against them, and don’t realize how many conditions sit between the words “replacement cost” and an actual full payment. If your home or business property suffered fire, smoke, water, wind, hail, or storm damage, you need to stop treating the carrier’s estimate like the truth. It’s a starting position. Usually a self-serving one.

A replacement cost endorsement can be one of the strongest tools you have in a claim dispute. But only if you know how insurers twist it, where the traps are, and how to force the issue with documentation, competing estimates, and policy-based objections.

Table of Contents

- Your Claim Was Low-Balled Now What

- RCV vs ACV The Core of Your Claim Dispute

- Decoding Your Policy’s Deceptive Language

- Red Flags How Insurers Systematically Underpay RCV Claims

- Special Claim Hurdles in North Carolina and Virginia

- Success Story From Low-Ball to Full Recovery

- Your Battle Plan to Maximize Your RCV Settlement

- Stop Fighting Alone Get Expert Claim Help

Your Claim Was Low-Balled Now What

You paid for coverage. Then the loss happened. Then the insurance company acted like your damaged property was a budgeting exercise.

That’s how most underpaid claims start. A fire leaves the home unlivable, a storm tears up roofing and interiors, or a major water loss affects more than what looks wet on day one. The carrier sends someone out, writes a narrow scope, trims line items, and hands you a number that might work on paper but won’t rebuild the property in practice.

This isn’t rare. Approximately 67% of homeowners maintain insufficient insurance coverage to fully rebuild their homes after a total loss, according to research on underinsurance rates. That matters because insurers already start from conservative assumptions, and when the policy limit is thin or the estimate is stripped down, the policyholder gets squeezed from both directions.

Why this happens so often

Insurance companies benefit when you assume their estimate is objective. It usually isn’t. Their adjuster works for them, not for you, and the company’s first number often reflects the cheapest defensible position, not the full scope of covered damage.

Common patterns show up fast:

- Narrow scoping: They price what they can see, while ignoring hidden damage, tear-out needs, smoke spread, or moisture migration.

- Cheap material assumptions: They swap in lower-grade products and call them equivalent.

- Payment staging games: They hold back money and act like you’re asking for extra, when you’re really asking for what the policy promised.

- Delay pressure: They know desperate policyholders accept weak offers when temporary living arrangements, contractor deposits, and business interruption costs start piling up.

Practical rule: If the insurer’s estimate doesn’t match what qualified contractors say the work costs, assume the dispute is real and start documenting it immediately.

Where your leverage actually is

If your policy includes a replacement cost endorsement, the carrier can’t just wave around a depreciated figure and pretend that ends the discussion. That endorsement gives you a basis to challenge underpayment. It doesn’t guarantee an easy payout, but it gives you contractual language to push back against low valuations.

Your job now is simple. Stop arguing from emotion and start arguing from scope, pricing, and policy wording. The insurance company wants you overwhelmed. You need to become organized.

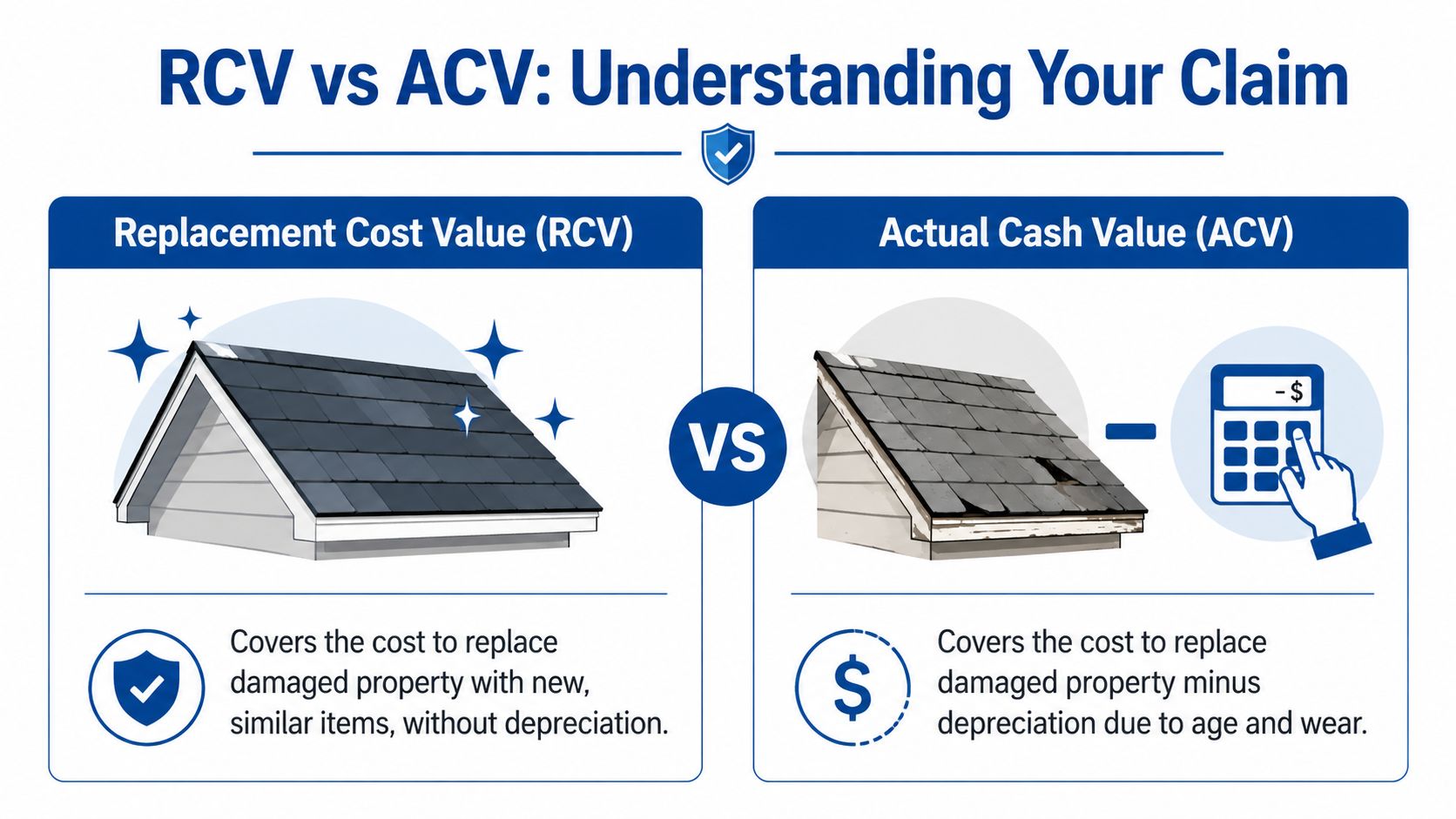

RCV vs ACV The Core of Your Claim Dispute

The biggest fight in many property claims comes down to two valuation methods: Replacement Cost Value (RCV) and Actual Cash Value (ACV). If you don’t understand that difference, the insurer has the upper hand.

Why the first check is often insulting

ACV is the carrier’s favorite place to start because depreciation does the dirty work for them. Your roof may have cost a certain amount to replace today, but under ACV they reduce payment for age and wear. Your kitchen cabinets may still function, but if they’re older, they’ll strip value out before they write the first check.

That’s why a low initial payment feels disconnected from reality. It is.

A verified explanation of this issue appears in this breakdown of replacement cost coverage conditions: a replacement cost endorsement requires the insurer to cover the full cost to replace damaged property with materials of like kind and quality at current prices, but only after repairs are completed; otherwise, they only pay ACV, which deducts depreciation and can result in 20% to 50% lower payouts.

The first payment is often not the real fight’s end point. It’s the insurer testing whether you know the difference between partial payment and full entitlement.

What replacement cost is supposed to do

RCV is meant to put you in a position to replace damaged property with new property of similar kind and quality at current prices. Not used materials. Not bargain-bin substitutions. Not an estimate built around visible damage only.

Here’s the plain-English difference:

| Replacement Cost (RCV) vs. Actual Cash Value (ACV) | Valuation Method | What It Pays For | Depreciation | Typical Use Case |

|---|---|---|---|---|

| RCV | Current cost to repair or replace with like kind and quality | New materials and current labor pricing, subject to policy terms and limits | Not deducted in the final replacement cost payment if policy conditions are met | Disputed dwelling and business property claims where the insured repairs or replaces |

| ACV | Replacement cost minus depreciation | Depreciated value of damaged property | Deducted based on age and wear | Initial payments, policies without replacement cost coverage, or claims where repairs are not completed |

This distinction becomes obvious when you look at building materials. If an insurer prices patchwork repairs or lower-grade products, compare that against the actual cost of replacing what was there. For example, when you’re understanding the true replacement costs of items like wood floor planks, you quickly see how far insurance numbers can drift from market reality once product matching, labor, and finish work are considered.

If you want a second explanation focused on policyholder disputes, this guide on actual cash value versus replacement cost is also worth reviewing before you challenge the carrier’s estimate.

The trap hidden inside recoverable depreciation

Most carriers don’t openly say, “We’re underpaying you.” They say, “This is the ACV amount for now.” Then they place the burden on you to complete repairs, submit invoices, and satisfy policy conditions before releasing the withheld amount.

That structure gives them an advantage:

- They control the starting estimate.

- They hold back depreciation.

- They demand proof of completed work.

- They dispute supplemental costs after the project is underway.

If the original scope is wrong, every later payment is built on a bad foundation. That’s why you don’t wait until the contractor is halfway through the job to challenge the estimate. You challenge the scope early, in writing, with supporting documentation.

Decoding Your Policy’s Deceptive Language

Insurance policies are packed with words that look harmless until the claim gets ugly. When carriers like State Farm or Allstate want to save money, they don’t need to invent new rules. They just lean hard on the words already in the endorsement.

Like kind and quality is where carriers start cutting corners

“Like kind and quality” sounds fair until the insurer starts using it to justify cheaper substitutes. You had custom trim. They price standard trim. You had a premium roof system. They price a lower-tier shingle. You had materials that matched throughout the home. They estimate only the visibly damaged section and ignore the mismatch problem.

That phrase is where many low-ball fights live.

The carrier will argue function. You need to argue comparability. If the original property had a certain grade, finish, profile, or integrated system, the estimate should reflect that. A replacement cost endorsement is not permission for the insurer to rebuild your property with the least expensive item that still vaguely works.

A useful way to think about it is how retailers explain coverage limits in product plans. Even a basic furniture protection plan usually spells out what types of accidental damage are addressed and what isn’t. Insurance companies do the same thing with more complexity and more room for abuse. If you don’t pin down the wording, they’ll use broad phrases to narrow your payment.

Actually repair or replace means conditions matter

Another phrase carriers love is the requirement that you repair or replace the damaged property. They use this to delay full payment and to frame withheld amounts as optional rather than owed.

The endorsement language matters. The verified policy wording states that the insurer is not liable under replacement cost coverage unless and until the damaged property is repaired or replaced by the insured using materials of like kind and quality with due diligence and dispatch. That means timing, proof, and compliance matter.

Here’s how insurers try to weaponize that:

- They question delays: If contractor schedules slip or permit issues arise, they may act like your claim to withheld funds expired.

- They challenge scope changes: If hidden damage is found mid-project, they may fight supplements instead of recognizing that demolition often reveals more.

- They scrutinize invoices: If your contractor’s paperwork is incomplete, they use that as an excuse to withhold payment.

- They dispute material selections: If you choose replacement materials that fairly match what you lost, they may call it an upgrade.

Your policy is a contract, not a slogan. Read the endorsement, declarations page, and every condition tied to replacement cost before you accept the insurer’s interpretation.

Words that should make you pause

When you read the carrier’s estimate or coverage letter, slow down when you see language like this:

- “Comparable” often means cheaper unless challenged.

- “Repair” may be a cost-cutting position when full replacement is more appropriate.

- “Subject to policy conditions” is where payment timing fights begin.

- “Reasonable” is usually the insurer’s opinion until you prove otherwise.

If you don’t define these terms with evidence, the insurance company will define them for you.

Red Flags How Insurers Systematically Underpay RCV Claims

You can usually spot an underpaid replacement cost claim before the coverage letter is even finished downloading. The estimate reads like someone priced the fastest, cheapest cosmetic fix possible and ignored what it really takes to restore the property.

They push repair when replacement is warranted

This is one of the oldest insurer moves in the book. They call for a repair because repair is cheaper, even when the damage pattern, matching issues, or material condition support full replacement.

You’ll see it in roofs, flooring, cabinets, siding, and smoke-damaged interiors. The company’s estimate narrows the affected area, ignores related components, and treats the property as if every damaged part can be surgically fixed without quality loss or visual mismatch.

Watch for these warning signs:

- Partial roof patching: The estimate replaces only a section even though the system’s integrity or matching is compromised.

- Selective interior painting: They price a single wall or room when the finish won’t match surrounding areas.

- Cabinet spot repairs: They assume isolated repairs can solve smoke, water, or finish damage across a larger assembly.

- Moisture scope minimization: They limit tear-out to visible staining while your mitigation contractor found broader affected areas.

They use functional replacement to cheapen the outcome

A major red flag is when the insurer starts steering the claim toward functional replacement cost logic, even when your expectation is true replacement with like kind and quality. According to IRMI’s definition of functional replacement cost endorsement, this approach allows an insurer to substitute damaged property with functionally equivalent modern alternatives, often resulting in payouts 20% to 40% below true replacement cost.

That sounds efficient until you’re the one living with the cheaper result.

Functional replacement is especially dangerous in older homes and commercial buildings where original materials, legacy systems, or architectural features matter. The carrier will say the substitute performs the same function. You’re the one left with a lower-quality outcome, reduced visual consistency, or a repair that changes the character of the property.

If your policy is supposed to provide replacement cost, don’t let the carrier quietly downgrade the claim into a “good enough” settlement.

Other patterns that deserve immediate pushback

Some tactics are less obvious, but they’re just as damaging:

- Code upgrades ignored: Basic estimates often exclude work required to meet current codes unless the policy adds ordinance or law coverage.

- Personal property depreciation games: They over-depreciate contents and force you into a paperwork chase for every withheld dollar.

- Missing line items: Detach and reset work, overhead tasks, or finish details vanish from the estimate because each missing item lowers the total.

- Software worship: The adjuster treats estimating software as if it overrides contractor reality. It doesn’t.

What to do when you see these red flags

Don’t answer a stripped-down estimate with a phone call alone. Build a paper trail.

Use a short written dispute that identifies the areas of disagreement, then attach contractor input, photos, product data, and any code-related concerns. Ask the carrier to explain why its scope excludes full replacement, matching, or required related work. Force clarity.

Once they have to defend the estimate line by line, weak positions start showing.

Special Claim Hurdles in North Carolina and Virginia

A replacement cost dispute gets harder in North Carolina and Virginia because the actual rebuild environment often moves faster than the insurer’s estimate. Hurricanes, wind events, and widespread storm damage create pricing pressure that standard carrier numbers often fail to capture.

Demand surge wrecks standard estimates

After a major regional event, labor tightens, materials get harder to source, and contractors become selective about the jobs they take. That’s when policyholders learn the insurance estimate may have been built from pricing that lags the actual market.

The problem gets worse when permits, specialized trades, and code compliance enter the picture. A clean line item for “replace drywall” or “replace roofing” doesn’t tell the whole story if your local jurisdiction requires more work during rebuild. The carrier may price the visible task while skipping the conditions attached to doing that work legally and properly.

In practice, that means your replacement cost endorsement matters, but so does the quality of the estimate beneath it. If the scope and pricing are stale, your so-called replacement cost claim can still be underfunded.

Extended replacement cost is not a cure for bad limits

Many policyholders assume extended replacement cost solves the problem. It helps, but it does not fix a bad starting point.

As explained in this review of extended replacement cost endorsements, ERC endorsements typically cap extra coverage between 10% and 50% of the dwelling limit, and that extra coverage is designed to address cost increases after the policy is written, not to correct an initially underestimated replacement value.

That distinction is brutal after a major loss. If the base dwelling limit was too low from the start, adding a percentage on top may still leave you short.

What NC and VA policyholders should check immediately

In this region, don’t assume the estimate reflects rebuild reality. Verify these issues early:

- Local contractor pricing: Ask whether the carrier’s estimate aligns with actual bids in your area.

- Permit-driven work: Confirm whether code-triggered items are included or excluded.

- Coverage cap exposure: Review whether your dwelling limit was realistic before the loss.

- Endorsement details: Read the declarations page and endorsements to see exactly what extra protection was purchased.

A replacement cost endorsement is useful. But in hurricane-prone and fast-moving rebuild markets, it only works as intended if the underlying numbers are honest.

Success Story From Low-Ball to Full Recovery

The theory matters, but results matter more. When a fire claim turns serious, the difference between the insurer’s version of the loss and the actual cost to rebuild can define whether a family recovers or gets trapped.

What changed after the policyholder got help

A common pattern in disputed fire losses looks like this: the insurance company writes a repair-focused scope, prices limited demolition, understates smoke spread, and ignores structural or systems-related consequences of the fire. The family gets an offer that may sound substantial, but the scope doesn’t restore the home.

What changes the outcome is not arguing louder. It’s documenting better.

A proper challenge to a fire loss estimate usually involves:

- A fuller scope of damage: Smoke, soot, odor migration, insulation contamination, framing exposure, and hidden affected components need to be identified.

- Current replacement pricing: The estimate has to reflect what qualified contractors will charge.

- Proof tied to policy language: The dispute should connect the missing work to covered building components and replacement cost obligations.

- Persistent negotiation: Carriers rarely expand a major scope because the policyholder asks politely once.

What this tells you about disputed fire claims

The strongest proof in these cases often comes from families who lived through the fight and saw what changed once someone pushed back against the insurer’s numbers. One Google review for the Raleigh office states:

“We recommend this company to everyone we know. We suffered a house fire back in 2021 that left our house unlivable. We reached out to FTPA and we can honestly say it was the BEST decision we made. They took so much stress off of us… They were always there to answer our MANY questions. Our claim was not an easy one… Without this company we would not be back in our newly built home that we are in today. Thank you so much for everything you all did for our family!”

Read the Google review for For The Public Adjusters, Inc. – Raleigh

That review matters because it reflects the complexities inherent in hard claims. They aren’t solved by trusting the first estimate. They’re solved by rebuilding the claim from the ground up, forcing the insurer to confront the actual loss, and refusing to let a low-ball scope become the final word.

If your fire claim still feels off, trust that instinct. Fire estimates are often missing more than you can see in the first draft.

Your Battle Plan to Maximize Your RCV Settlement

You don’t need more vague advice. You need a repeatable process that puts pressure on the carrier and supports every disagreement with evidence.

Build a claim file the carrier can’t ignore

Start with the insurer’s estimate and mark every item that looks incomplete, underpriced, or wrongly omitted. Then build your rebuttal around documents, not opinions.

Use this checklist:

- Get independent contractor estimates. Don’t rely on one quick opinion. Ask qualified contractors to identify missing work, matching issues, tear-out needs, and rebuild realities.

- Create a room-by-room damage record. Use photos, videos, and notes. Track what was damaged, what was removed, and what still needs to be addressed.

- Challenge the scope in writing. Identify disputed items clearly. A written dispute slows down the carrier’s ability to dodge specifics.

- Track invoices and replacement proof. If your policy requires completed repairs before full replacement cost is paid, documentation is not optional.

- Study cost components. A resource like a comprehensive construction cost breakdown helps policyholders understand why contractor pricing includes more than just visible labor and materials.

If you need a plain-language primer before you send a formal dispute, read this explanation of what replacement cost coverage means in practice. It’s useful when you’re matching your policy language to the carrier’s estimate.

Claim discipline: Every disagreement should be tied to one of three things. Scope, pricing, or policy interpretation. If your objection doesn’t fit one of those categories, tighten it up.

Know when to stop fighting alone

Some claims can be nudged into line. Others won’t move without professional pressure.

Call for help when:

- The carrier delays repeatedly and keeps asking for the same information.

- Major line items are denied with weak explanations.

- The adjuster refuses to revise obvious errors in scope or pricing.

- You’re being pushed into a cheap repair strategy that won’t restore the property properly.

- The paperwork burden is taking over your life while the claim still isn’t being valued correctly.

At that point, the issue isn’t just damage. It’s claim power.

Stop Fighting Alone Get Expert Claim Help

A replacement cost endorsement is only valuable if you enforce it. The insurance company already has trained adjusters, estimating software, internal review channels, and a financial incentive to keep your payout down. You shouldn’t face that alone.

If your claim has been delayed, denied in part, or underpaid, stop assuming the next phone call will fix it. Real progress comes from a full policy review, a detailed damage inspection, a corrected scope, and aggressive negotiation backed by documentation. That’s exactly why policyholders turn to a public claims adjuster who works for them instead of the insurance company.

You paid for coverage. You’re entitled to demand that the carrier honor it. Don’t settle for a number that leaves you unable to repair, rebuild, or recover.

If your homeowner, dwelling, or business property claim has been low-balled, delayed, or disputed, For The Public Adjusters, Inc. offers no-cost claim reviews for policyholders in North Carolina and Virginia. Their team represents you, not the insurance company, and helps document damage, interpret coverage, challenge bad estimates, and fight for the full amount owed under your policy.