Water Damage Coverage on Homeowners Insurance is often confusing. You found water where it never should’ve been. Under the floorboards. Behind a vanity. Running from a ceiling stain that wasn’t there last week. You did what responsible homeowners are told to do. You reported the loss, waited for the carrier to inspect, and expected help.

Then the adjuster called it “long-term.” Or “wear and tear.” Or offered a number so low it barely touched demolition, drying, and basic repairs.

That’s where a lot of homeowners freeze up. Don’t. Water damage coverage on homeowners insurance is one of the biggest battlegrounds in property claims, and the carrier knows exactly how to use confusion, exclusions, and delay against you.

Table of Contents

- Your Water Damage Claim Was Low-Balled or Denied Now What

- Deconstructing Your Policy What Water Damage Is Actually Covered

- The Insurer’s Playbook Common Exclusions and Endorsement Traps

- How to Prepare Your Claim to Fight a Low-Ball Offer

- Special Alert for NC & VA Homeowners Hurricane and Flood Claim Disputes

- When to Unleash an Expert For The Public Adjusters Inc

- Frequently Asked Questions About Water Damage Claim Disputes

Your Water Damage Claim Was Low-Balled or Denied Now What

A common version of this dispute looks like this. A homeowner finds soaked drywall from a pipe failure, reports the claim fast, and assumes the insurer will pay because the damage was sudden. Instead, the carrier sends out its adjuster, writes a narrow scope, ignores insulation, baseboards, cabinet damage, moisture spread, and odor treatment, then says the rest was pre-existing.

That isn’t an oddball outcome. Water damage and freezing are among the most frequent and costly homeowner claims, accounting for nearly 24% of all property damage claims, and the average claim payout exceeds $12,500, according to ConsumerAffairs’ summary of water damage insurance claim statistics. When losses are this common and this expensive, carriers have every financial incentive to narrow coverage and push smaller payments.

What the denial usually means

A denial or low-ball offer rarely means the damage wasn’t real. It usually means the insurer found a theory it could use.

The favorites are familiar:

- Gradual damage: They say the leak happened over time, even when the visible damage appeared all at once.

- Maintenance neglect: They shift focus from the loss to the age or condition of the plumbing.

- Limited scope: They pay for the obvious wet area and ignore what migrated beyond it.

- Excluded category: They reframe the source as backup, seepage, or flood to sidestep the main coverage grant.

Practical rule: Don’t treat the first estimate like a final answer. Treat it like the opening position in a dispute.

What you should do next

You need to stop reacting like a customer-service caller and start acting like a policyholder in a coverage fight.

Do three things immediately.

- Read the denial letter line by line. The reason matters. “Wear and tear,” “repeated seepage,” and “flood” each require different evidence.

- Compare the insurer’s estimate to the actual damage. If rooms, materials, or mitigation work are missing, that underpayment can be challenged.

- Push the claim back into dispute. If you need a roadmap for that process, start with this guide on appealing an insurance claim.

Stop assuming the adjuster is neutral

The carrier’s adjuster isn’t your advocate. That person was sent to control the insurer’s exposure. Some are competent. Some are careless. Many are under pressure to close files fast and cheap.

Your job is to challenge every bad assumption. If the insurer says the damage was old, make them prove it. If they ignored wet materials, make them account for them. If they boxed the claim into an exclusion, force the coverage analysis back to cause, timing, and documentation.

That’s how water damage claim disputes get turned around. Not by waiting. By pushing back.

Deconstructing Your Policy What Water Damage Is Actually Covered

Most homeowners think their policy either covers water damage or it doesn’t. That’s too simplistic. The fight usually turns on a few words buried in the policy and then manipulated by the carrier after the loss.

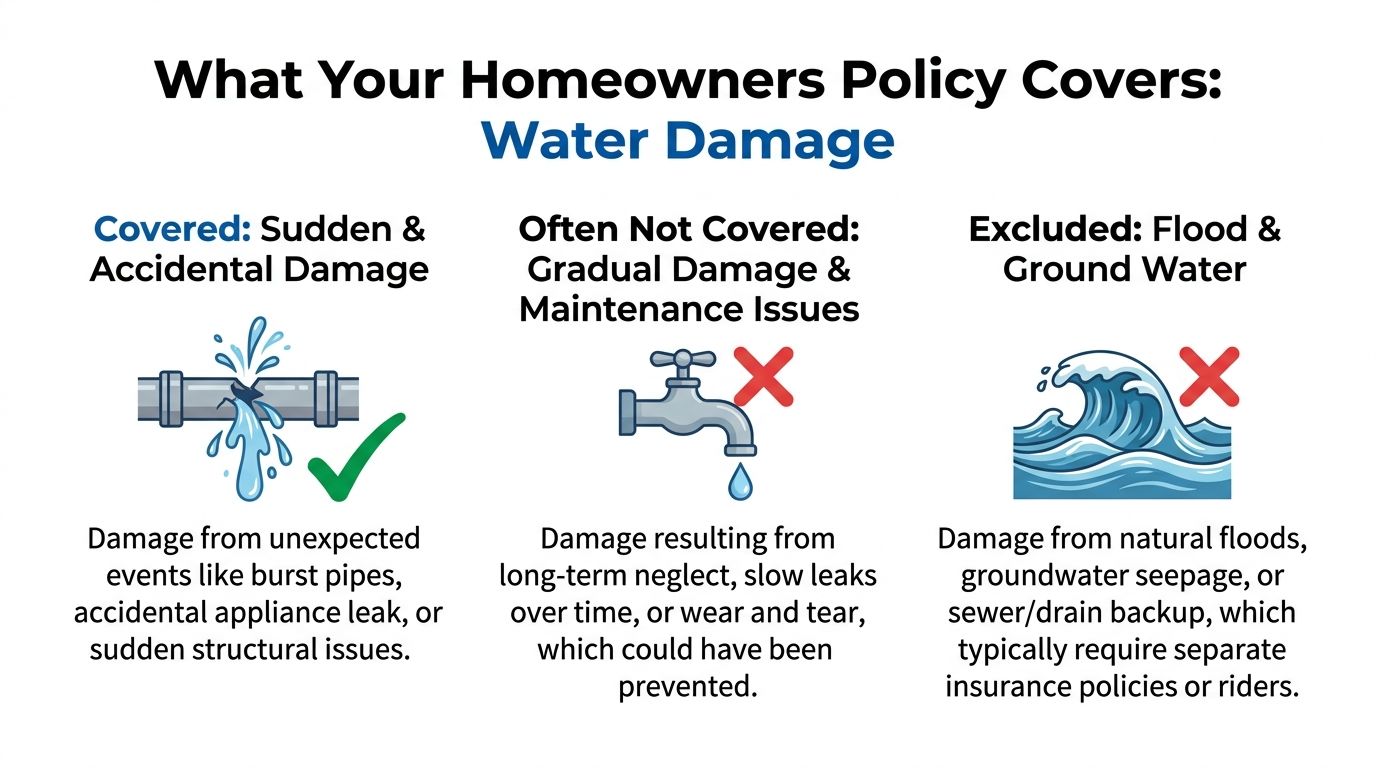

The core phrase is sudden and accidental.

In a standard HO-3 policy, sudden and accidental water damage from plumbing, heating, air conditioning systems, or household appliances is generally covered. A burst pipe is the classic example. If you kept the heat on and took reasonable care, the claim should be covered. Goosehead’s explanation of water coverage notes that freezing water can generate over 5,000 psi, which makes a freeze break a clearly sudden event, even though insurers still try to argue wear and tear.

Covered doesn’t mean uncontested

Homeowners hear “burst pipe is covered” and assume the carrier will honor that without a fight. That assumption gets people hurt.

The insurer looks for openings such as:

- Failure to maintain heat

- Vacancy issues

- Evidence of prior leakage

- Corrosion or deterioration

- Language suggesting repeated seepage instead of a single event

A pipe can fail suddenly, and the insurer will still try to move the claim into a maintenance bucket. That’s not a legal conclusion. It’s a strategy.

The line between sudden and gradual

This is the fault line in most disputes over water damage coverage on homeowners insurance.

A washing machine hose bursts overnight. Covered, in principle.

A pipe leaks inside a wall for months and stains the trim. Often denied under the base policy as a long-term condition.

The fight starts when the facts aren’t clean. Maybe the pipe had weak spots before it finally ruptured. Maybe the homeowner didn’t see hidden leakage until a cabinet toe-kick buckled. Maybe the insurer points to rust and says the whole thing was gradual. That’s where claim value rises or falls.

A sudden loss can involve older plumbing. Age alone doesn’t erase coverage. Cause and timing still matter.

What to look for in your own policy

Pull the declarations page and the actual form. Don’t rely on what the agent told you years ago.

Focus on these issues:

- Perils insured against: Find the grant of coverage for sudden accidental discharge or overflow.

- Exclusions: Read every water-related exclusion, especially seepage, leakage over time, neglect, mold, backup, and flood.

- Duties after loss: The insurer will use any claimed delay in mitigation or reporting against you.

- Endorsements: These can expand or restrict what would otherwise be covered.

If you suspect the source wasn’t obvious, practical leak evidence matters. A plumber’s findings, moisture mapping, and even outside guidance on detecting secret plumbing leaks can help you identify conditions the insurer later pretends were “visible all along.”

The policy is a contract, not a slogan

Insurance companies sell peace of mind. Claims departments sell interpretation.

That’s why you need to read beyond the marketing language and compare your coverage to the actual wording. If you want a deeper look at policy language around leaks and discharge claims, review this breakdown of whether homeowners insurance covers water leaks.

If the carrier is stretching “gradual” to avoid paying for a sudden loss, the dispute isn’t over coverage alone. It’s about proof.

The Insurer’s Playbook Common Exclusions and Endorsement Traps

Carriers don’t need to deny every water claim outright. They just need a believable reason to pay less. Water losses give them plenty of room to do that because the policy usually separates covered discharge, excluded seepage, excluded flood, excluded backup, and limited mold issues into different buckets.

That structure is where homeowners get boxed in.

The exclusions they lean on hardest

The first trap is gradual leakage. If staining, rot, swelling, or microbial growth suggests the moisture was present for a while, the carrier will argue the damage resulted from a condition that should’ve been discovered earlier.

The second is mold and secondary damage. A small covered leak can trigger a much larger drying and tear-out problem. Insurers often try to split those apart and say the original event may be covered, but the later consequences are limited or excluded.

The third is backup and overflow from drains or sump systems. Many homeowners don’t realize this often requires separate coverage.

The fourth is flood and ground water. If the water rose from outside the property or entered from the ground, standard homeowners coverage usually won’t respond.

Hidden damage is where many people lose

A major weakness in many policies is concealed seepage. That’s why the Hidden Water Damage endorsement matters so much. According to Best Version Media’s discussion of water damage coverage, hidden leaks are involved in 15% of all water claims, and that endorsement is designed to cover concealed seepage that the base policy often denies.

That matters because a homeowner can’t tear open every wall every month hunting for a pinhole leak. Carriers know that, but they still use “maintenance” as a weapon.

If the leak was concealed and undiscoverable without opening the structure, don’t accept a lazy “you should’ve known” denial.

Water Damage Coverage Covered vs. Excluded

| Scenario | Standard Policy Coverage (The Promise) | Common Insurer Tactic (The Reality) | Your Best Defense |

|---|---|---|---|

| Burst supply line under sink | Often covered as sudden accidental discharge | Claims corrosion or prior seepage made it long-term | Plumber report, photos of fresh break, immediate mitigation records |

| Slow leak behind shower wall | Often excluded under base form | Labels all resulting damage maintenance-related | Check for hidden water damage endorsement and document concealment |

| Sewer or drain backup | Often excluded unless endorsed | Says water source falls outside core plumbing discharge coverage | Confirm backup endorsement and preserve mitigation invoices |

| Rising storm water entering home | Excluded under standard homeowners policy | Directs claim away from homeowners coverage entirely | Evaluate separate flood coverage and causation evidence |

| Wind-driven rain through storm-created opening | Can be covered when wind created the opening | Blurs wind entry with flood or pre-existing deterioration | Roofing inspection, weather evidence, interior moisture path documentation |

Endorsements are not optional extras

Two endorsements deserve far more attention than agents usually give them.

- Hidden water damage coverage: This can be the difference between a paid concealed leak loss and a flat denial.

- Water backup coverage: This matters when the water source wasn’t a burst pipe but a drain, sewer, or sump-related event.

Policyholders also need to understand how valuation changes the outcome. If the carrier is paying on a lower basis than your policy allows, you need to review the role of a replacement cost endorsement and whether the estimate reflects full repair pricing instead of stripped-down settlement math.

Why agents and carriers leave this vague

Because ambiguity helps them later.

The sales side talks about broad protection. The claims side points to sublimits, endorsements you didn’t buy, conditions after loss, and exclusions you never knew existed. If your policy has gaps, fix them at renewal. If the loss already happened, focus on whether the insurer is stretching those gaps beyond what the language says.

That’s where disputes are won.

How to Prepare Your Claim to Fight a Low-Ball Offer

A weak file invites a weak payment. If the carrier controls the evidence, it controls the story. Your job is to build a record that shows cause, scope, and cost before the insurer narrows all three.

Start with the physical facts inside the home.

Build evidence before materials disappear

Water damage changes fast. Drywall dries in appearance before it recovers in value. Cabinets swell, then settle. Flooring cups, adhesive fails, trim separates, and the insurer later says the damage wasn’t as severe as claimed.

Do this early and do it thoroughly:

- Photograph the source: Get close shots and room-wide shots. Capture the broken line, failed fitting, overflow point, or visible entry path.

- Record the spread: Floors, walls, baseboards, insulation, cabinets, and contents all matter.

- Save damaged parts when possible: If a plumber removes a section of pipe or fitting, ask to retain it.

- Get written cause findings: A contractor’s verbal opinion won’t carry the same weight as a written report.

Keep a claim log like a professional

Most homeowners trust phone calls too much. Don’t.

Create a simple timeline with dates, names, who inspected, what they said, what they promised, and what they refused to include. If the desk adjuster changes the rationale later, your notes help expose it.

A solid file should include:

- Photos and video by date

- Plumber or mitigation invoices

- Moisture readings or drying documentation

- Carrier letters and estimate versions

- Receipts for emergency spending

- A room-by-room list of affected materials

The most persuasive dispute files don’t just say the insurer missed damage. They show exactly where, when, and how.

Don’t let the carrier choose reality for you

Insurers love “preferred vendors” because controlled inspections often lead to controlled scopes. You need independent eyes on the loss.

Get your own contractor estimate if the carrier’s numbers look thin. If cabinets were only partially scoped, challenge it. If flooring continuity matters, challenge piecemeal replacement. If demolition is needed to expose wet cavities, make sure that tear-out is included.

This short video gives a useful look at the kind of property evidence homeowners should think about when the insurer’s version of the loss doesn’t match what’s in the house.

What not to do during a dispute

Some mistakes hand the carrier ammunition.

- Don’t rush permanent repairs before the damage is fully documented.

- Don’t throw away wet materials unless they’ve been photographed and tied to the loss.

- Don’t give broad recorded statements without understanding the coverage issue in dispute.

- Don’t sign off on a partial scope just because the adjuster says supplements can be handled later.

The goal is leverage

You aren’t assembling paperwork for the sake of organization. You’re strengthening your position.

A detailed claim file makes it harder for the insurer to say the damage was minimal, old, unrelated, or partly excluded. That’s how you fight a low-ball offer. Not with outrage alone. With better evidence than the carrier has.

Special Alert for NC & VA Homeowners Hurricane and Flood Claim Disputes

North Carolina and Virginia homeowners deal with a brutal version of water damage disputes after hurricanes and major coastal storms. The reason is simple. More than one water source may hit the property at the same time.

Wind damages the roof. Rain enters through the opening. Water rises outside. Ground saturation follows. The insurer then starts slicing the loss into categories and assigning as much of it as possible to excluded flood instead of covered wind-related entry.

The wind versus water fight

This is one of the most important claim disputes in the region.

In North Carolina and Virginia, disputes over wind-driven rain versus flood surge are common after hurricanes, and public adjusters report 30% to 50% higher settlements when they use forensic methods to separate covered wind-related water entry from excluded rising floodwater, according to Allstate’s water damage resource as cited in the verified data.

That distinction decides whether the claim belongs under homeowners coverage, a separate flood policy, both, or neither in the carrier’s preferred version of events.

Why insurers blur the categories

Because blurred causation saves them money.

If water entered through a roof opening created by wind, that can trigger homeowners coverage. If the carrier can frame the interior damage as flood-related instead, it shifts the burden elsewhere. Homeowners then get stuck arguing over causation while the property continues to deteriorate.

The strongest disputes usually rely on a mix of evidence:

- Roof and exterior inspection findings

- Weather timing

- Interior moisture patterns

- Debris lines and water marks

- Photographs taken before cleanup changes the scene

In hurricane losses, the source of the water matters as much as the damage itself.

NFIP claims are a separate problem

Flood claims are their own maze. Standard homeowners insurance excludes flood damage from rising water, so that claim typically goes to the National Flood Insurance Program if the homeowner has a flood policy.

Those claims are technical, paperwork-heavy, and unforgiving. They involve specialized adjusters and proof requirements that many homeowners don’t understand until they’re already behind. General storm advice often fails here because the federal flood process is not the same as a normal homeowners claim.

If you’re evaluating contractors or restoration help after a storm, it also helps to review practical guidance on choosing flood damage professionals. The wrong cleanup team can destroy evidence that matters to both wind and flood claim disputes.

What NC and VA homeowners should do differently

Don’t let the carrier reduce a mixed-cause loss to a one-line denial.

You need separate documentation for each possible source of water. That means roof damage evidence, interior entry path evidence, and exterior flood indicators. Keep those categories distinct from the start. If you lump everything together, the insurer will use that confusion against you.

This is also where many homeowners wait too long. Hurricane claims become harder, not easier, once debris is removed, damaged materials are discarded, and the insurer has already locked its causation theory into the file.

When to Unleash an Expert For The Public Adjusters Inc

You sent photos, answered questions, waited for inspections, and still got the letter. The pipe break is now “long-term seepage.” The storm opening is now “pre-existing wear.” The estimate covers paint and ignores tear-out, drying, cabinets, insulation, and the materials behind the wall. That is the point where you stop hoping the carrier will fix its own numbers.

Bring in help early if the insurer has already chosen a story that cuts coverage.

The moments that justify outside help

Outside representation makes sense when the claim has turned into a technical fight instead of a basic adjustment. Common warning signs include:

- A denial based on gradual damage

- A low estimate that ignores demolition, drying, or full material replacement

- A hurricane loss involving both wind and water

- A flood claim with strict proof requirements

- Repeated delays, inspection reschedules, or shifting explanations

Once those issues appear, you are no longer dealing with a simple paperwork problem. You are dealing with coverage language, causation arguments, and an estimate built to save the carrier money.

Flood disputes are especially unforgiving

Flood disputes punish mistakes fast. The proof requirements are strict, the scope has to be documented carefully, and any missing category can turn into money you pay yourself. Homeowners who treat a flood claim like a standard water loss usually find out too late that the rules are different.

Experienced representation changes the outcome because the file gets built to meet the program’s requirements, with the right categories, the right support, and the right scope.

What experienced representation does

Good claim help is disciplined, detailed, and aggressive.

A strong public adjuster or policyholder advocate will usually:

- Read the policy for coverage language the carrier glossed over

- Inspect past the obvious wet area

- Prepare a fuller and more defensible scope of loss

- Challenge weak causation theories with facts, photos, and timelines

- Handle the back-and-forth the insurer hopes will wear you down

That work matters because water claims are often under-scoped on purpose. Carriers miss concealed wet materials, code items, matching, insulation, cabinetry parts, and finish work across connected areas. They also like to relabel sudden damage as gradual when the evidence is thin and the homeowner is unprepared.

A denial is not the end of the claim file. It is often the point where the work starts.

A note on homeowner confidence

Carriers count on hesitation. They know many homeowners will wait, trust the process, and accept a partial payment because fighting sounds exhausting.

Do not hand them that advantage.

If the insurer is using neglect, old damage, wear and tear, or exclusion language to force a bad result, get someone involved who knows how to break that argument apart. In NC and VA, that matters even more after hurricanes, where mixed-cause losses give insurers room to blur wind damage, interior water entry, and flood issues into one muddy denial.

The right expert does not just argue harder. They build a claim the carrier can no longer dismiss with a form letter.

Frequently Asked Questions About Water Damage Claim Disputes

These are the questions homeowners ask when the carrier stops acting like a safety net and starts acting like an obstacle.

FAQ on Water Damage Claim Disputes

| Question | Answer |

|---|---|

| My insurer says the leak was “gradual.” Can I still fight that? | Yes. “Gradual” is a common defense, not an automatic truth. The fight turns on where the leak occurred, whether it was concealed, when damage first became discoverable, and what evidence supports a sudden failure versus long-term seepage. |

| Is a burst pipe usually covered? | Often yes, especially when the loss was sudden and you took reasonable care of the property. The real dispute usually comes from the insurer trying to reframe the break as neglect or wear and tear. |

| Why is the estimate so much lower than contractor pricing? | Carrier estimates are often written to a narrower scope. They may omit demolition, drying-related tear-out, insulation, paint across connected areas, cabinetry components, or other items needed for a proper repair. |

| Should I let the insurance company’s vendor handle everything? | Not blindly. Preferred vendors may help with emergency work, but you still need independent documentation of the cause, spread, and full repair scope. Convenience can cost you leverage. |

| What if mold appeared after the leak? | Don’t assume that ends the claim. The timing and cause matter. If mold followed a covered water event, the insurer may still owe parts of the loss, even if it tries to limit or isolate that damage. |

| Does homeowners insurance cover flood water? | Standard homeowners coverage generally excludes rising water and flood. Those losses usually require separate flood coverage. In mixed storm losses, separating flood damage from wind-driven rain damage is critical. |

| When should I dispute a low-ball offer? | Immediately after you identify missing damage, bad causation assumptions, or underpriced repairs. Waiting usually helps the insurer, not you. |

| Do I need a public adjuster for every water claim? | No. But when the claim is denied, delayed, underpaid, or complicated by hurricane or flood issues, professional help often becomes the practical move. |

Final advice if you’re stuck

If the carrier is using confusion to wear you down, narrow the dispute to facts.

Ask: What was the source? When did it happen? What materials were affected? What does the policy say? What is missing from the estimate? Those questions cut through most insurer games fast.

And if the claim has turned into a technical fight, stop treating it like a customer complaint. It’s a property loss dispute. Handle it that way.

If your water damage claim was denied, delayed, or low-balled, For The Public Adjusters, Inc. can review the policy, inspect the damage, document the full scope, and deal directly with the carrier. They represent policyholders across North Carolina and help homeowners push back when the insurance company tries to shrink, stall, or sidestep a valid property claim.