After a disaster strikes your home or business, you expect your insurance company to help you rebuild. But the hard truth is, major carriers like State Farm and Allstate have a powerful tool they use to slash your payout right from the start: depreciation.

This isn't just about simple wear and tear. It's a calculated strategy designed to create a "low-ball" settlement, leaving you thousands of dollars short of what you actually need to fix the damage.

How Insurers Use Depreciation to Underpay Your Claim

From the moment you file a property damage claim, your insurance company’s primary goal is to protect its profits—not your financial recovery. One of the most effective ways they do this is by applying depreciation, which immediately cuts the value of your damaged property based on its age and condition.

That first check you get in the mail? It's almost never enough to cover the full cost of repairs. This initial payment is based on the Actual Cash Value (ACV) of your property.

Actual Cash Value (ACV) is what your property was worth the second before the damage happened. To get this number, the insurer takes the full cost to replace an item today and then subtracts a hefty chunk for depreciation.

This ACV check is just a fraction of what you're owed. It creates an immediate financial hole that the insurance company expects you to fill out of your own pocket just to get the work started.

The Conflict of Interest Baked into Your Claim

Here’s the real problem: the person deciding how much to depreciate your property works for the insurance company. They send their own adjuster—an employee or a contractor whose entire job is to minimize how much the company has to pay out.

This single person holds all the power in deciding how much value your 10-year-old roof or five-year-old hardwood floors have "lost." It’s a setup that is fundamentally rigged against you.

- Your Goal: Get enough money to restore your property and make it whole again.

- The Insurer's Goal: Pay as little as possible to protect their bottom line.

The adjuster hits their goal by aggressively depreciating every single line item on your claim, from the shingles on your roof and the siding on your walls to the cabinets in your kitchen.

ACV vs RCV A Breakdown Your Insurer Hopes You'll Won't See

To really grasp how this system is designed to shortchange you, you need to understand the difference between ACV and Replacement Cost Value (RCV). Most modern homeowners and business policies are RCV policies, which means you’re supposed to get the full cost of replacement. But they don't make it easy.

This table breaks down the game they're playing.

| Concept | Actual Cash Value (ACV) | Replacement Cost Value (RCV) |

|---|---|---|

| What It Is | The value of your property with depreciation deducted. It’s a reflection of age and wear and tear. | The full cost to replace your damaged property with brand new materials of similar kind and quality, without any deduction for depreciation. |

| When You Get It | This is the first check your insurance company sends. It’s the low-ball offer. | You only get the rest of the money after you prove the repairs are done and submit a mountain of paperwork. |

| The Result | An immediate, inadequate payment that isn't enough to cover the full cost of repairs, forcing you to pay upfront. | The full amount you are actually owed, but only if you fight to recover the money the insurer holds back (the depreciation). |

This two-check system is precisely where countless policyholders lose thousands of dollars. The insurance company is betting you'll be too overwhelmed, confused, or exhausted to chase down the rest of your money. And every dollar you don't claim is a dollar they get to keep.

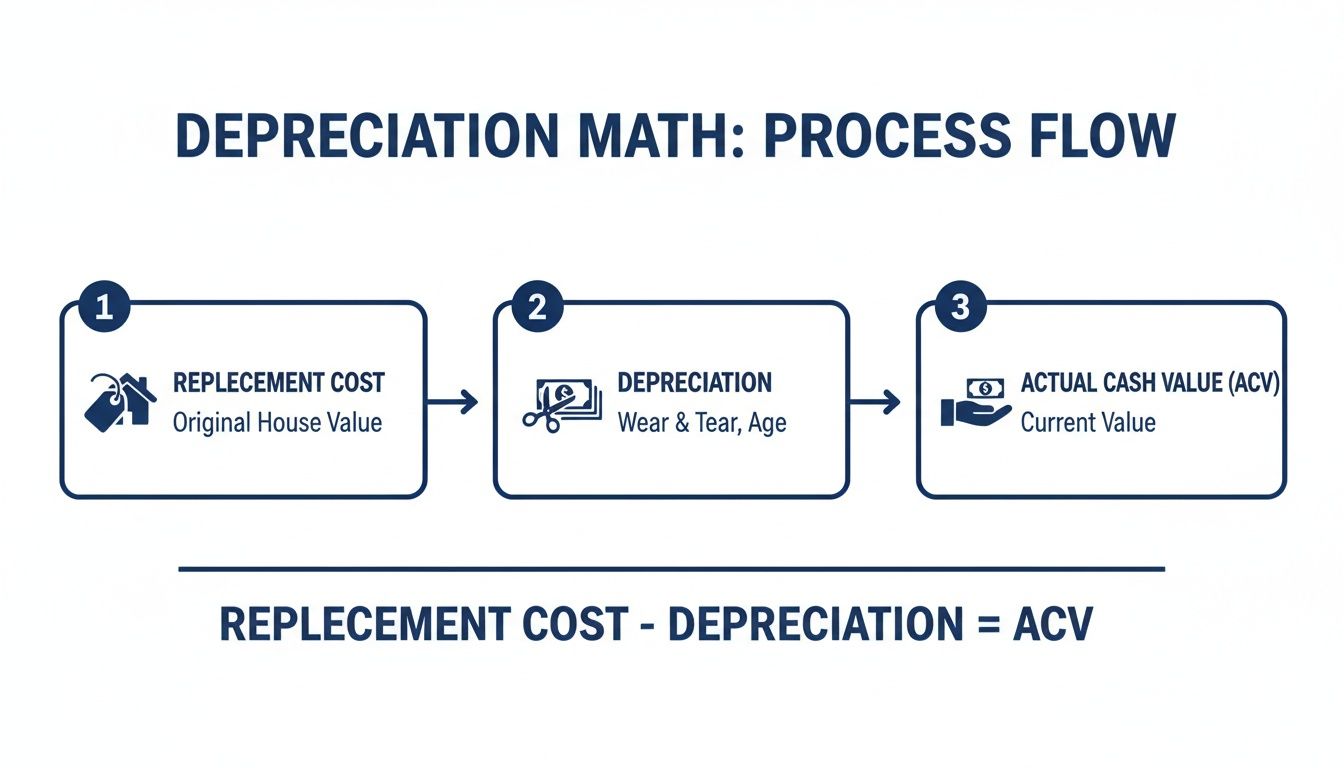

Decoding the Adjuster's Depreciation Math

Your insurance adjuster wants you to believe depreciation is some fixed, unshakeable number spit out by a secret formula. Don't buy it. The truth is, their calculations are incredibly subjective and almost always tilted in their employer's favor.

They aren't just pulling numbers out of thin air, but the methods they use are designed for one purpose: to justify paying you as little as possible.

It all boils down to a simple, yet devastating, formula that dictates the size of your first check:

Replacement Cost Value (RCV) – Depreciation = Actual Cash Value (ACV)

That "Depreciation" number is the adjuster's playground. Their main goal is to make it as big as they can to shrink the Actual Cash Value (ACV) payment. Understanding how they inflate this number is your first and most critical step in fighting back.

How Adjusters Justify Their Low Numbers

To defend their math, adjusters lean on standardized depreciation schedules and something called the "broad evidence rule." This rule sounds fair on the surface—it lets them consider any factor they think is relevant, like an item's age, condition, or resale value.

In reality, it gives them a shocking amount of leeway to aggressively devalue your property.

Take a perfectly good 15-year-old architectural shingle roof. It had another 15 years of life left before the storm, but the adjuster will slash its value by 50% or more based on age alone. They'll conveniently ignore its excellent pre-loss condition because that doesn't save their company money.

This same brutal logic gets applied to everything else:

- Flooring: Your 10-year-old hardwood floors? They’ll slap a standard 20-year lifespan on it and cut its value in half, just like that.

- Siding: Even vinyl siding that was in pristine shape before a hailstorm gets hammered with depreciation based solely on its installation date.

- Cabinets: Those beautiful custom kitchen cabinets can have their value gutted, leaving you with a fraction of what you need to actually replace them.

This systematic undervaluing is a core tactic in their playbook. To see exactly how this impacts your final payout, you need to read our guide on the difference between ACV and RCV policies.

The Problem with Standard Depreciation Schedules

To make their lowball offers seem official, insurance companies rely on depreciation guides. These tables assign a "useful life" to just about every nail, board, and shingle in your property. While it gives them a starting point, it's a deeply flawed system that fails to account for real-world conditions.

This isn’t just about building materials, either. Consider the salvage vehicle market, which saw a year-over-year depreciation of 17.8%. As you can see from trends on IAAI.com, these market forces directly impact what an insurer pays for a totaled vehicle. For property owners in North Carolina and Virginia dealing with storm damage, this just goes to show how aggressively insurers apply depreciation across all types of property.

Below is a table showing some of the typical lifespan estimates insurers use. It gives you a peek behind the curtain at how they justify their deductions.

Common Depreciation Schedules Your Insurance Company Uses

A look at the typical lifespan estimates insurers use to depreciate common property items, revealing how quickly they deduct value from your claim.

| Building Component or Item | Typical Lifespan (Years) | Example Annual Depreciation Rate |

|---|---|---|

| Architectural Shingles | 30 | 3.33% |

| 3-Tab Asphalt Shingles | 20 | 5.00% |

| Vinyl Siding | 50 | 2.00% |

| Hardwood Flooring | 50 | 2.00% |

| Carpet (Mid-Grade) | 10 | 10.00% |

| Kitchen Cabinets (Stock) | 20 | 5.00% |

| Interior Paint | 7 | 14.29% |

| Water Heater | 10 | 10.00% |

| HVAC System | 15 | 6.67% |

The biggest problem with these schedules is their rigidity. They completely ignore superior materials, expert craftsmanship, or the diligent maintenance you performed that extended an item's true life.

The adjuster’s job isn't to be fair; it’s to apply these schedules in whatever way benefits the insurance company most. By scrutinizing their estimate line by line, you can start to see where the math doesn't add up and begin building your case for the fair settlement you truly deserve.

Unlocking Your Recoverable Depreciation

Let’s talk about one of the most maddening parts of any property insurance claim: recoverable depreciation. In plain English, this is the money your insurance company legally owes you but holds back until you prove the repairs are actually done. It’s the gap between the full repair cost (Replacement Cost Value, or RCV) and that first lowball check they send you (Actual Cash Value, or ACV).

Your policy says you're entitled to this money. But insurers like Allstate and State Farm have turned the process into a nightmare of holdbacks and paperwork, betting you'll get frustrated and just walk away. When you do that, you’re forfeiting a huge chunk of your settlement—often 20-40% of your total claim value.

This isn't bonus money. This is your money, and you’re going to have to fight for it.

The image below breaks down the simple math they use to hold your money hostage.

This process is designed to deliberately shrink your initial payment, turning the rest into a carrot on a stick that you have to chase.

The Paperwork Gauntlet Your Insurer Creates

To get that depreciation money released, you have to jump through hoops. Insurers demand a mountain of proof showing you’ve completed the repairs and, more importantly, spent the money. They don't take your word for it. One tiny error on a form or a missing receipt can bring the whole process to a screeching halt.

They're forcing you to be a project manager, an accountant, and a file clerk, all while you're trying to put your life back together after a disaster. It's a calculated strategy designed to wear you down until you quit.

If you want every dollar you're owed, you have to be obsessive about your records. Here’s the kind of documentation they will demand:

- Final Contractor Invoices: Not just a bill with a final number. They want detailed, itemized invoices breaking down the cost of every nail, every 2×4, and every hour of labor.

- Proof of Payment: You need to show the money left your bank account. This means providing copies of canceled checks (front and back), credit card statements, or bank transfer confirmations.

- Material Receipts: If you bought any materials yourself, they’ll want to see the original receipts.

- Signed Certificate of Completion: This is a document signed by both you and your contractor, officially stating all work is finished as agreed.

The adjuster will go through every single page with a fine-tooth comb, looking for any reason—any excuse at all—to delay or deny payment. This isn’t by accident; it’s by design.

Common Tactics Insurers Use to Withhold Your Money

Insurance companies didn't get rich by paying claims quickly and fairly. They have a whole playbook of tricks to make claiming your recoverable depreciation a soul-crushing experience. Knowing what they are is your first line of defense.

Key Takeaway: The insurance company is counting on you to get overwhelmed. The stress, the paperwork, the endless phone calls—it’s all part of a strategy to make you give up on the depreciation holdback. Every dollar they don't release goes straight to their bottom line.

A classic move is to impose ridiculously short and arbitrary deadlines to finish the work, sometimes just 180 days from the date of the loss. After a major hurricane or storm when every good contractor is booked for months, that’s an impossible timeline.

They also love to reject perfectly valid paperwork. They’ll claim an invoice isn't "detailed enough" or argue that a receipt is for a slightly better material than you had before, even when the original is no longer made. This drags you into a frustrating back-and-forth of resubmitting documents, a delay tactic that only benefits them. When you understand these maneuvers, you can build a rock-solid case that leaves them no room to say no.

Your Guide to Disputing an Unfair Depreciation Assessment

Let’s get one thing straight: you do not have to accept an insurance adjuster's estimate just because they handed it to you. When you see excessive or unfair depreciation on your claim, it's not a final decision—it's an opening offer. Fighting back is your right, and with a clear strategy, you can absolutely challenge their low-ball numbers and demand the fair settlement you deserve.

The first step is to formally and professionally dispute their calculations. Don't waste your breath arguing over the phone; you need to create a paper trail.

Send a written request, either by email or certified mail, demanding that the adjuster provide the specific basis for their depreciation values. They need to justify every single percentage they applied to every line item. Ask them to send you the exact depreciation guide, manual, or software they used. This forces them to defend their math instead of hiding behind vague excuses like "standard procedure."

Gather Your Own Powerful Evidence

While the adjuster scrambles to justify their numbers, it’s your turn to build an undeniable case. The burden of proof is on you to demonstrate the true value and condition of your property before the loss. Your memory isn't enough—you need hard evidence that directly contradicts their assessment.

Your goal is to paint a crystal-clear picture of a well-maintained property, not the neglected one their depreciation schedule conveniently assumes. Here’s what you need to start collecting:

- Pre-Loss Photographs and Videos: Dig through your phone, social media accounts, and old family albums. Find pictures that show the condition of your roof, siding, flooring, and other damaged areas before the incident ever happened.

- Maintenance and Repair Records: That new roof you installed five years ago? Find the receipt. The invoice for the floors you had refinished? Get it. Records of regular HVAC servicing? Dig them out. These documents prove your property's actual age and condition were far better than "standard."

- Independent Contractor Estimates: Get detailed, itemized estimates from at least two reputable, local contractors. These reports are your counter-offer, and they’re incredibly powerful for exposing just how out of touch the insurer's estimate really is.

Invoke the Appraisal Clause in Your Policy

If the insurance company digs in its heels and refuses to negotiate in good faith, your policy contains a powerful but often overlooked tool: the Appraisal Clause. This provision is your secret weapon. It allows you to hire an independent appraiser to represent you in a dispute over the value of your loss.

The process usually works like this:

- You hire your own appraiser.

- The insurance company is forced to hire its own appraiser.

- The two appraisers then work together to agree on the amount of the loss.

- If they can't agree, they bring in a neutral third party, called an umpire, to make a final, binding decision.

Invoking appraisal takes the decision out of the insurance company's biased hands and moves it into a more neutral arena. It's a critical step for breaking a stalemate when the carrier just refuses to be reasonable. For a deeper dive into the overall process, our guide on how to dispute an insurance claim provides more strategies.

The principles that guide fair insurance practices are often rooted in broader consumer law, which is designed to empower policyholders to fight back against unfair assessments. And believe me, these disputes are getting bigger and more common. With global insured catastrophe losses hitting $100 billion in just the first half of a recent year, the stakes are incredibly high. Insurers are using every tool in their playbook—especially depreciation—to minimize payouts and protect their bottom line.

How a Public Adjuster Fights Back Against Unfair Depreciation

Theory is one thing, but seeing how a professional advocate can dismantle an insurance company’s bogus assessment shows you what’s really possible. It's proof that you don't have to accept their low-ball numbers.

Take a real case we handled for a North Carolina homeowner. A nasty hailstorm shredded their roof. The insurance company's adjuster came out, agreed it needed a full replacement, and then sent over a settlement offer that was a slap in the face. It was crippled by excessive and unfair depreciation.

The insurance company argued the roof was old and had lost most of its value. The ACV check they cut wasn't even close to what the homeowner needed to hire a decent contractor. They were left completely stuck, unable to afford the critical repairs their home desperately needed.

Dismantling the Insurer’s Bogus Math

This is where we came in. Our team at For The Public Adjusters, Inc. launched our own, far more thorough investigation. We didn't just glance at the shingles from the driveway—we got on the roof and performed a detailed, hands-on inspection to build an undeniable case.

Here’s how we did it:

- We Documented Everything: We took high-resolution photos showing the roof's true pre-storm condition. By using evidence from undamaged sections, we proved it was well-maintained and had plenty of life left.

- We Used Their Own Tools Against Them: We used the same industry-standard estimating software and local material costs that they do to build a precise, line-by-line estimate for a full replacement.

- We Challenged Their Flawed Numbers: Armed with hard facts and real data, we went straight at the carrier’s flawed depreciation math, proving their numbers were arbitrary and had no basis in the roof’s actual condition.

Our process exposed the carrier's assessment for what it was: a calculated tactic to underpay the claim. We see this all the time. In a similar case involving a devastating fire, our team was able to achieve dramatic results. You can read more about how a public adjuster secured a $330,100 increase after the insurance company tried to low-ball the settlement.

The Final Result: A Fair Payout

Through relentless negotiation and by presenting irrefutable evidence, we forced the insurance company to completely reverse its decision. The final settlement didn’t just give the homeowner a little more—it covered the full Replacement Cost Value of a brand-new roof, including every single dollar of depreciation they had initially tried to withhold.

This homeowner went from being completely stranded to having the full amount needed to make their home safe again. Stories like this aren't rare, and they highlight a critical truth: you do not have to fight your insurance company alone. Having an expert in your corner can change everything.

Here’s what one of our clients had to say after we helped them fight back:

Frequently Asked Questions About Depreciation

Wrestling with insurance depreciation can make your head spin. It’s a confusing and frustrating part of the claims process, but it’s where insurers often hide their biggest profit grabs. Here are some straight answers to the questions we hear every day from property owners just trying to get a fair shake.

Can My Insurance Company Depreciate Labor Costs?

This is a classic dirty trick and a massive point of conflict in claim disputes. In states like North Carolina, insurance companies will absolutely try to depreciate both the materials and the labor needed to install them. Their argument? They claim labor is just part of the overall replacement cost, so it’s fair game for depreciation.

Don’t fall for it. This is a predatory tactic, plain and simple. The cost to hire a roofer to install a brand-new roof is the same whether the old roof was one day old or 20 years old. Labor doesn't wear out. In a landmark case, Sproull v. State Farm Fire & Cas. Co., the Illinois Supreme Court ruled that "depreciation of labor is not appropriate" because labor does not lose value over time. Pushing back on this one point can put thousands of dollars right back into your pocket.

What if My Damaged Siding or Shingles Are Discontinued?

This is another favorite move carriers use to slash your payout. An adjuster will come out, see a few damaged pieces of siding, and offer to pay only for those specific pieces. The problem is, those materials are no longer made. You’re left with an ugly, mismatched patch job on your home or business that tanks your property value.

This is completely unacceptable. Your policy almost certainly contains language about "matching," which means the insurance company is obligated to restore your property to a uniform and consistent appearance. If the original materials are discontinued, that often means they have to pay for a full replacement of the siding or roof to make it whole again. You do not have to accept a patchwork repair.

How Long Do I Have to Claim My Recoverable Depreciation?

Insurance companies thrive on deadlines and fine print. Most policies give you a very specific, and often very short, window to complete repairs and claim your recoverable depreciation. It’s common to see a deadline as short as 180 days from the date they cut you the first check (the ACV payment).

If you miss that deadline, the money is gone. Forever. This is a deliberate strategy they use, knowing that after a major storm, good contractors are booked for months. You have to stay on top of it. If you’re facing delays that are out of your control, document every single phone call and email. Then, make sure you request an extension in writing before your deadline expires.

For business owners with unique assets, like commercial drones, the details of your policy are even more critical. Getting a handle on what's covered before you ever have to file a claim is key. A good guide on commercial UAV insurance can shed light on the specifics of how these policies work.

Are you tired of fighting an insurance company that's using depreciation to slash your payout? The team at For The Public Adjusters, Inc. is here to help you fight back. We level the playing field by documenting your claim, challenging unfair depreciation, and negotiating for the full settlement you are owed. Contact us today for a free, no-obligation claim review at https://forthepublicadjusters.com.