Shower leaks are among the most contested claims in North Carolina and Virginia. Because the damage often happens behind waterproof membranes and tile, insurers frequently default to the “Seepage and Leakage” exclusion to avoid payment. This guide provides forensic-level insights that move beyond “call a plumber” and into the technicalities of Access and Egress, Hydrostatic Testing, and NC/VA-specific case law.

You notice a brown stain on the ceiling below the bathroom. Or a musty smell that won’t leave, even after cleaning. Or a shower tile that suddenly feels loose under your hand. That’s usually the moment the claim problem starts, not the moment it ends.

Most homeowners think the primary fight is with the leak, the mold, or the contractor. It usually isn’t. The harder fight is with the insurance company adjuster who shows up ready to frame your water damage shower loss as “wear and tear,” “long-term seepage,” “poor maintenance,” or “faulty installation.” Those labels aren’t neutral. They’re payout reduction tools.

If you’re already dealing with a denied claim, a small estimate, or a carrier that keeps asking for “just one more inspection,” you need a strategy. Not more waiting. Not blind trust. Strategy.

The Drip You Don’t See Can Cost You Everything

A shower leak rarely announces itself with a dramatic flood. Most of the time, it starts with a small clue. A soft baseboard. Hairline grout cracks. A stain downstairs. A warped vanity side panel. Homeowners see something minor. The carrier sees an opening to underpay.

That’s why a water damage shower claim gets mishandled so often. The visible damage looks limited. The hidden damage usually isn’t. And once the insurer controls the narrative, they’ll try to box your loss into the cheapest explanation available.

Why this claim gets expensive fast

Water losses from bathrooms and showers are common and costly. About 1 in 60 insured homes files a water damage claim each year, the average payout is over $11,000, and mold can begin growing within 24 to 48 hours, according to water damage claim statistics for homeowners.

Those numbers matter because they explain carrier behavior. Insurers know these claims add up. So they scrutinize them aggressively.

Practical rule: If your insurer starts talking about “old staining,” “repeated exposure,” or “maintenance,” they’re not just asking questions. They’re building a denial path.

The physical problem is only half the battle

A bad shower pan, failed grout lines, a leaking valve, or poor waterproofing can send water into drywall, insulation, framing, and subflooring before you ever see a stain. By the time you’re looking at obvious damage, the carrier may already be preparing to argue that the problem took too long to notice.

That argument is convenient for them. It shifts blame away from coverage and onto you.

If you’re still figuring out whether the shower itself is failing, practical resources on leaking shower repair can help you understand the construction side. But don’t confuse repair advice with claim strategy. Fixing the shower and proving the scope of insured damage are two different jobs.

Here’s the hard truth. If you let the insurance company define the loss before you document it properly, you’re already behind.

Building Your Case Identifying the REAL Scope of Damage

Photos help. They are not enough.

If you want to win a shower leak dispute, you need to document the claim like you’re preparing for an argument with someone who intends to minimize every dollar. Because that’s exactly what’s happening.

Start before demolition changes the evidence

Before anyone tears out tile, drywall, or flooring, create a full visual record.

Use this checklist:

- Take wide shots first so the insurer can’t later claim the damage was isolated.

- Shoot close-ups of stains, separated caulk, cracked grout, swollen trim, warped cabinets, and any visible microbial growth.

- Record a slow video walkthrough and narrate what you smell, see, and feel.

- Capture adjacent rooms because shower leaks often spread beyond the bathroom.

- Save plumber and mitigation invoices the same day you receive them.

A small but smart move is preserving proof of the bathroom’s prior condition when you have it. Even a simple before photo can matter. This example of documenting pre-damage conditions shows why. If the carrier hints that your shower was already failing, older photos can knock that argument down fast.

Hidden moisture is where insurers cut scope

The biggest adjustment mistake in a water damage shower claim is treating visible damage as the full damage. It almost never is.

Professional restoration standards matter here. According to industry guidance on water damage restoration methods, thermal cameras can identify hidden moisture that may extend 70% beyond visible damage, and the drying phase typically runs 3 to 5 days when done correctly. DIY cleanup often misses this hidden spread, which is why so many “small” shower leaks turn into rot and mold disputes later.

That gives you an advantage. If the insurer writes an estimate for a patch, one fan, and a little paint, you can challenge the scope with objective standards.

Don’t argue with the carrier using frustration alone. Argue with moisture readings, photographs, invoices, expert reports, and drying records.

What to document besides the obvious

Look for the damage adjusters routinely ignore or downgrade:

- Wicking at drywall edges. Water often climbs upward behind baseboards.

- Subfloor softness around the shower entry, toilet base, or vanity toe-kick.

- Cabinet swelling at side panels and bottoms.

- Ceiling staining below the bathroom even if the bathroom itself looks “minor.”

- Door casing or trim expansion near the shower opening.

- Odor changes that suggest concealed moisture.

If mitigation has started, ask for daily moisture logs. If it hasn’t, ask why. No serious shower leak evaluation should rely on guesswork alone.

Build a claim file the carrier can’t casually dismiss

Your file should include:

| Item | Why it matters |

|---|---|

| Photos and videos | Locks in the original condition before cleanup |

| Plumber findings | Helps identify source and failure point |

| Mitigation report | Shows what got wet and what needed drying |

| Moisture readings | Proves hidden impact beyond stains |

| Material list | Supports full scope, not a cosmetic patch |

| Policy copy | Lets you challenge exclusions intelligently |

If your shower leak resembles broader plumbing-related damage elsewhere in the house, compare how those claims are evaluated in this guide on water damage from burst pipe. The same pattern shows up again and again. Carriers pay less when the policyholder accepts an incomplete scope.

Don’t let the first inspection become the final story

The field adjuster’s first visit often shapes everything that follows. If that inspection is rushed, shallow, or focused only on visible finishes, you’ll spend the rest of the claim trying to undo that damage.

That’s why your evidence needs to be stronger than their assumption. Not louder. Stronger.

The Insurer’s Playbook for Denying Your Shower Claim

The insurance company already has a script for shower leak claims. If you know the script, you can stop reacting to it and start dismantling it.

The favorite excuse is gradual damage

When water damage is hidden behind tile, inside a wall cavity, or under a shower pan, insurers love one phrase: gradual damage.

They use it because it sounds technical and responsible. In practice, it often means they’re trying to avoid paying for concealed damage that took time to reveal itself. That’s not the same thing as saying you ignored a known leak for months. But carriers blur that line constantly.

One of the most common tactics is labeling hidden shower leaks as “pre-existing conditions” or “gradual damage.” A 2025 industry report cited in this analysis of hidden shower leak denials says 40% of water claims are denied on those grounds, and public adjusters often recover 30% to 50% more by challenging that framing.

That doesn’t surprise me at all. I’ve seen carriers take fresh moisture damage and try to rebrand it as old neglect because a stain looked dark or a subfloor had layered damage.

They also blame workmanship when it helps them

If the shower pan failed, the membrane was bad, or the tile system was installed poorly, the carrier may shift from “gradual leak” to “faulty workmanship.” Same outcome for them. Less money out.

Here’s where homeowners get trapped. The insurer may say they don’t cover the defective construction itself, then pretend that means they also don’t owe for resulting covered damage to nearby materials. That’s not a small distinction. It’s often the whole dispute.

You need to separate these issues clearly:

- The failed component itself may be disputed.

- Resulting water damage to other property may still be covered.

- Tear-out access may also become a battleground, especially if the source is buried behind finished surfaces.

A lot of carrier estimates deliberately mash those categories together so the underpayment looks cleaner than it is.

If the insurer says “faulty installation,” your next question should be, “What resulting damage are you still accepting as covered, and where is that breakdown in writing?”

The low-ball patch job is another standard move

Big carriers like State Farm and Allstate don’t earn goodwill from me on these claims. Too often, they delay, re-inspect, narrow the scope, and offer a patch that leaves the homeowner with mismatched finishes, incomplete drying, and unresolved concealed damage.

They know people are tired. They know many homeowners need money fast. So they propose the cheapest path that sounds superficially reasonable.

That low-ball scope usually looks like this:

| Carrier tactic | What it really means |

|---|---|

| Spot paint only | They’re ignoring moisture spread |

| Replace one area of tile | They’re ignoring matching and continuity issues |

| No subfloor replacement | They didn’t investigate saturation deeply enough |

| Minimal drying equipment | They’re treating a hidden loss like a surface spill |

| “Monitor and repair later” | They want future damage blamed on you |

A common dispute pattern

A homeowner finds staining below an upstairs shower. The carrier inspects, notes old caulk and aged grout, and issues a letter saying the leak was long-term. End of claim, according to them.

But then the homeowner gets a plumber report identifying a failed drain assembly or pan connection, plus moisture readings showing active migration into the adjacent wall and subfloor. Suddenly the carrier’s “maintenance problem” story doesn’t hold up as well.

That shift happens when evidence gets specific. Not emotional. Specific.

Watch the language in every letter

If your insurer uses phrases like these, slow down and read carefully:

- “Repeated seepage”

- “Long-term leakage”

- “Visible signs should have alerted the insured”

- “Wear, tear, deterioration”

- “Construction defect”

- “Limited spot repair”

Each phrase is a signal. They’re narrowing either the cause, the timeline, or the repair scope.

Don’t answer casually. Ask for the exact policy language they’re relying on. Ask what inspection methods they used. Ask whether they performed moisture mapping. Ask whether they evaluated concealed damage beyond the visible bathroom finishes.

Most low-ball shower claims don’t start with a dramatic denial. They start with a controlled, partial acceptance that leaves out the expensive parts.

Fighting Back How a Public Adjuster Flips the Script

When the carrier controls the estimate, the vocabulary, and the paper trail, homeowners usually lose ground fast. A public adjuster changes that because the insurer no longer gets to be the only side documenting the loss.

A public adjuster works for the policyholder, not the insurance company. That difference matters more in shower leak disputes than almost anywhere else in residential property claims.

What changes when the policyholder has representation

A proper challenge to a water damage shower claim isn’t just “please take another look.” It’s a competing claim presentation.

That usually includes:

- A new scope of loss based on inspection, moisture findings, and repair sequencing

- A line-by-line estimate built to reflect real restoration and rebuild needs

- Policy analysis focused on resulting damage, tear-out, access, and valuation issues

- Direct negotiation with the carrier so you’re not stuck arguing from a kitchen table at a disadvantage

If you need a plain-language primer on the role itself, this overview of what a public adjuster does is useful.

They challenge bad assumptions with evidence

In hidden shower leak cases, a good public adjuster doesn’t just repeat your complaint. They rebuild the story of the loss with documentation the carrier can’t easily brush aside.

That can include thermal imaging, moisture mapping, contractor reports, plumber findings, drying records, code-related rebuild issues, and estimate software such as Xactimate. The point is simple. Replace the insurer’s vague theory with a documented scope.

Independent representation shows its teeth. If the carrier says, “We only owe for a small ceiling patch,” the response isn’t outrage. It’s a written scope showing affected drywall, insulation, subflooring, adjacent finishes, demolition requirements, and reconstruction sequencing.

A disputed claim gets stronger the moment someone translates damage into scope, scope into estimate, and estimate into policy-supported demand.

Curbless showers are becoming a major dispute zone

This issue is getting worse with newer bathroom designs. A 2025 report discussed in this review of curbless shower insurance disputes notes a 25% rise in related water damage claims, and insurers often deny them by citing design flaws or upgrade exclusions. The same source explains that a public adjuster can use engineering analysis and non-destructive testing to show that the claimed damage is covered.

That matters because curbless and zero-threshold showers often involve water migration arguments. The carrier says “bad design.” The homeowner says “covered water damage.” Without expert documentation, the insurer’s version usually gets more weight than it deserves.

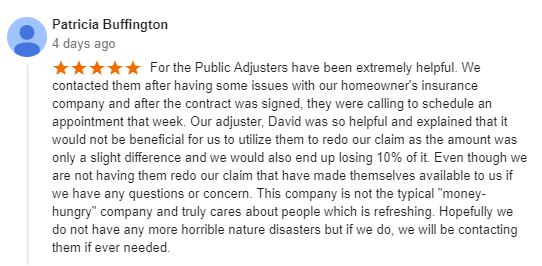

A real review matters because claim fights are personal

Homeowners don’t just want technical help. They want to know whether the people handling their dispute communicate, push back, and stay engaged.

Here is a customer review screenshot tied to For The Public Adjusters, Inc.:

In practical terms, the value of a public adjuster is not mystery or magic. It’s pressure, documentation, and competence. They force the insurer to respond to a developed record instead of an under-informed homeowner trying to decode denial language alone.

One factual option in North Carolina and Virginia is For The Public Adjusters, Inc., a state-licensed firm that represents policyholders in property damage disputes and provides claim reviews, inspections, estimate preparation, and direct carrier communication.

The denial isn’t always the end of the claim

A shower claim can look dead on paper and still be recoverable if the denial rests on weak inspection work, incomplete scope, or overbroad exclusion language. That’s why many homeowners make a costly mistake when they accept the first “no” as final.

The insurer has experience. That doesn’t mean they’re right.

The Legal Battleground When Insurers Refuse to Pay

Some carriers don’t move even after the claim is thoroughly documented. They delay. They recycle the same denial language. They pretend a shallow investigation was a reasonable one. That’s when the dispute starts moving toward a legal bad faith conversation.

Why these claims become legal fights

Water losses are expensive enough that insurers have a real financial incentive to minimize them. According to the Insurance Information Institute data referenced in this discussion of home insurance claim trends, water damage and freezing accounted for 22.6% of all home insurance claims from 2019 to 2023, and the average payout exceeded $15,000.

That kind of exposure explains a lot of the behavior policyholders see. Repeated inspections. Narrow readings of policy language. Pressure to accept partial payment. Silence after you submit support for reconsideration.

What bad faith usually looks like in practice

Bad faith isn’t just a carrier denying a claim you think should be covered. It’s the insurer acting unreasonably in the way it investigates, evaluates, or pays the claim.

Common warning signs include:

- Ignoring evidence from plumbers, mitigation crews, or moisture testing

- Misquoting policy language or relying on broad labels without analysis

- Delaying decisions while the property gets worse

- Refusing to explain the basis for a limited payment

- Changing denial theories after you answer the first one

Some insurers count on homeowner fatigue. If they can make the process aggravating enough, they don’t need a perfect denial. They just need you to stop pushing.

You don’t need to wait forever

If the insurer keeps stonewalling, escalate the dispute with structure. Preserve every email, letter, estimate, and inspection note. Keep the timeline clean. Ask direct written questions. Demand direct written answers.

If you’re already at the appeal stage, this guide on how to appeal a denied insurance claim gives a useful framework for tightening your record before the fight gets bigger.

I’m not going to invent a court case to make the point. The point stands without that. Insurers lose lawsuits when they underinvestigate, underpay, or hide behind sloppy claim handling. They are not untouchable, and a bad denial does not become valid just because it arrived on company letterhead.

Your Questions Answered Fighting a Shower Damage Claim

What if I live in a condo and the shower leak affected a shared wall or the unit below

Don’t assume the association’s insurer will handle everything, and don’t assume your insurer will tell you where their responsibility ends. Condo shower losses create finger-pointing fast.

Start by getting the governing documents, especially the maintenance and insurance sections. Then force each insurer to state its position in writing. One may owe for interior finishes. Another may owe for common elements. The downstairs neighbor’s carrier may come after someone later. Your job is to avoid being trapped in oral shrugging from three different adjusters.

Get a plumber or qualified building professional to identify the leak origin clearly. Origin matters in condos because coverage often turns on whether the failed component served only your unit or a common system.

Can my insurer cancel me for making a shower water damage claim

Maybe, maybe not. Policy and underwriting decisions vary, and carriers rarely speak plainly about future renewal decisions during an active claim. What you should not do is let fear of nonrenewal force you into accepting an underpaid settlement.

A badly underpaid claim can leave you paying for demolition, drying, rebuild, and mold-related correction out of pocket. That financial hit is immediate. A future underwriting decision is uncertain. Focus first on getting the current loss evaluated correctly.

If you’re worried about this issue, ask the carrier or your agent for written clarification on renewal status and underwriting review. Verbal reassurance is worthless if the policy later changes.

My mortgage company is listed on the check. Now what

That’s normal on larger property claims. It’s annoying, but normal.

The mortgage company has a financial interest in the property, so they often must endorse insurance proceeds. The problem is timing. Homeowners need funds to start repairs, while the lender may release money in stages.

Handle it like a project, not a side task:

- Call the mortgage servicer immediately and ask for their loss draft department procedures.

- Get the endorsement requirements in writing so you don’t lose time.

- Ask whether they require contractor paperwork, inspections, or signed affidavits before releasing funds.

- Track every submission date because lenders often create avoidable delay.

If the carrier already underpaid the claim, the mortgage check issue becomes even worse because now you’re fighting two bureaucracies with too little money.

What if the insurance company says the shower leak was old because there was mold or staining

That’s a common leap, and it’s often a dishonest one.

Staining does not automatically prove neglect. Mold does not automatically prove you knew about the leak. Hidden shower failures can go undiscovered behind tile, under pans, inside wall cavities, and below finished flooring. The key question is not whether damage developed over time before discovery. The key question is whether the loss was concealed, when it became reasonably discoverable, what failed, and what your policy says about resulting damage.

Ask the insurer to identify the actual evidence behind its timeline claim. Not assumptions. Evidence.

Should I complete repairs before the claim dispute is resolved

Do emergency mitigation and reasonable protection right away. Don’t let the property sit and get worse just because the carrier is dragging its feet.

But full reconstruction before the dispute is documented can create a proof problem. If you remove everything before proper inspection, the insurer may later argue there was never enough damage to justify the repair scope. Preserve samples, photos, moisture records, contractor findings, and damaged materials when practical.

The right sequence is usually: mitigate, document, inspect, then rebuild.

The adjuster says they’ll pay to patch but not to restore matching finishes. Is that fair

Often, no.

Patch-and-paint logic is one of the oldest carrier cost-cutting moves in property claims. Bathrooms make this worse because tile runs, waterproof assemblies, and finished surfaces don’t always allow unnoticeable partial repair. If matching materials aren’t available or replacement requires larger tear-out for proper installation, the insurer’s spot-fix proposal may be unrealistic.

Push for a written explanation of how the proposed repair returns the area to proper condition. If they want to replace only a few tiles, ask how they intend to handle continuity, waterproofing integrity, and material match.

What’s the difference between a shower leak claim and a flood claim

This distinction matters because insurers sometimes exploit homeowner confusion.

A shower leak is generally a property water damage issue under a homeowners, dwelling, or commercial property policy, subject to that policy’s terms, exclusions, and limitations. A flood claim is a different animal and usually falls under NFIP coverage or a write-your-own flood carrier when rising surface water caused the damage.

If water escaped from the shower, shower pan, drain assembly, valve, supply line, or adjacent bathroom plumbing, that is not the same thing as a natural flood event. Don’t let the carrier blur those categories because the words “water damage” appear in both situations.

The insurer keeps asking for more inspections. Should I cooperate

Yes, but on your terms.

Cooperate reasonably. Confirm appointments in writing. Ask who is attending and why. Request copies of reports when possible. Keep your own notes on what each person inspected and what they said.

Repeated inspections can be legitimate. They can also be a stalling tactic. If the process starts looping without progress, start asking sharper written questions about coverage position, remaining information needed, and expected decision date.

When should I stop trying to handle this myself

Stop when you see the pattern.

If the insurer is minimizing hidden damage, narrowing the repair scope, using vague exclusion language, dragging out inspections, or pushing a small settlement that won’t fund proper restoration, you’re no longer in a routine claim. You’re in a dispute.

That’s the point where trying to “be patient” often costs more than getting help.

2. Why do insurers deny shower claims as "Gradual Seepage"?

Most policies in NC and VA exclude damage that occurs over a period of 14 days or more. The Deep Dive: Adjusters look for mold, rotted wood, or "puckering" drywall as evidence of a long-term leak.

A leak can be "hidden" and "sudden" simultaneously. If the leak occurred inside a wall cavity where it was not visible to the naked eye, a Public Adjuster can argue that the "occurrence" was only discovered upon the manifestation of the stain. Use a thermal imaging camera to prove the moisture spread is active and not a result of long-term neglect.

3. Will insurance pay to tear out my shower tile to fix a leaking pipe?

Yes, under the "Access and Egress" rule. The Forensic Insight: This is the most overlooked part of a shower claim. While the policy may not pay for the $10 pipe fitting, the insurer must pay the cost to "tear out and replace any part of the building necessary to repair the system."

In high-end homes in Northern Virginia or Charlotte, removing a single tile often requires destroying the entire waterproof membrane. Since the system cannot be "patched" without compromising its integrity, the insurer may be on the hook for a total shower rebuild just to access a $10 pipe.

4. How do I prove the shower pan failed "suddenly"?

Perform a Hydrostatic Flood Test. The Strategy: Insurers claim shower pans fail due to age. You need to prove a specific failure.

Plug the drain and fill the shower base with 2 inches of water. If the water level drops and a leak appears downstairs immediately, it proves a mechanical failure of the pan or the clamping ring. Document this with video. In NC and VA, showing a "test-verified failure" makes it much harder for an adjuster to claim "slow seepage."

5. Does the "Matching Rule" apply to my bathroom tile in NC and VA?

This is a major point of dispute between the two states.

Virginia: Follows the "Reasonable Uniformity" standard (14VAC5-400-80). If they have to break three tiles to fix a pipe and the tile is discontinued, they may have to replace the entire bathroom to ensure it matches.

North Carolina: NC uses the "Broad Evidence Rule" (Surratt v. Grain Dealers).

Argue Diminution of Value. A master bath with mismatched "patchwork" tile significantly lowers the home's market value. Under NC common law, the insurer's duty is to restore you to your "pre-loss condition," which a mismatched repair fails to do.

6. Is mold behind the shower tile covered?

Only if it is the direct result of a covered water loss. The NC/VA Reality: Most policies have a Mold Sub-limit (usually $5,000).

If you tell the adjuster "it’s been smelling like mold for months," you just gave them a reason to deny the entire claim as "neglect." Instead, document that the mold was discovered only after the sudden leak necessitated the removal of the wall.

7. What if the leak is coming from the shower "wand" or "mixing valve"?

These are considered "Plumbing Fixtures" and are generally covered if they fail suddenly. The Expert Insight: If the mixing valve (the handle that controls temperature) cracks due to a "surge" in water pressure or a manufacturing defect, it is an accidental discharge.

Do not throw away the valve! The insurer's SIU (Special Investigations Unit) may want to inspect it. If you throw it away, they can deny the claim for "Spoliation of Evidence."

8. Why is my insurer asking for "Maintenance Records" for my shower?

They are looking for a reason to claim the leak was "preventable." The NC/VA Strategy: In Virginia and North Carolina, insurers are increasingly aggressive about "Duty to Maintain."

You are not a licensed plumber; you are not expected to see behind walls. If the shower appeared in good working order (clean grout, intact caulk) from the outside, you have fulfilled your duty. Provide photos of the bathroom prior to the leak to show the room was well-maintained.

9. Will insurance pay for a hotel if I only have one shower?

Yes, under Coverage D: Loss of Use. The Logic: If your only shower is being demolished for a covered repair, the home is "unfit for its intended use."

In NC and VA, if a home lacks a primary functioning bathing facility, it may be a building code violation to occupy it. Demand Additional Living Expenses (ALE) to stay in a local hotel or rental until the shower is functional.

10. How do I fight a "Wear and Tear" denial on a shower claim?

Invoke the Appraisal Clause. The Strategy: If the insurer agrees there is damage but says it’s only worth $1,000 (a "patch") while your contractor says $15,000 (a "rebuild"), use NCGS § 58-44-16 or VA Code § 38.2-2105.

Appraisal is a "mini-arbitration" where two appraisers and an umpire determine the true "amount of loss." This is the most effective way to force an insurer to pay for a full shower replacement when they are trying to "spot repair" a waterproof system.

If your shower leak claim has been delayed, denied, or low-balled, For The Public Adjusters, Inc. can review the loss, evaluate the carrier’s scope, and help you challenge an unfair outcome on your homeowners, dwelling, or commercial property claim in North Carolina or Virginia.