Water Damage Restoration Service Near Me… Who? What? When! Where? Why? The moment you see water gushing into your home, every instinct tells you to grab the phone and call your insurance company.

Don’t do it. That one phone call, made in a panic, can be the costliest mistake you ever make. The person on the other end of that line isn’t your neighbor; they are a highly trained professional whose job is to protect their company’s profits, not your property.

Your first call needs to be to someone who works for you and only you.

Why Your Insurer Is Not Your First Call

As soon as you discover water damage, an invisible clock starts ticking. Every decision you make from that moment forward will directly affect the outcome of your claim. While it seems perfectly logical to call State Farm, Allstate, or whoever your carrier is, you’re putting yourself on the defensive from the very first minute.

Their entire business model is built on one simple principle: pay out as little as possible. The adjuster they send to your home is their employee, working for their interests. They are not your ally.

From the second you report the claim, every word you say is on a recorded line, logged, and scrutinized. That insurance adjuster is trained to hunt for reasons to limit or deny your claim. Was it a slow leak? A pre-existing issue? A maintenance problem? They will use anything they can find against you.

They control the narrative from the get-go, often pushing you toward their “preferred” contractors—companies that know who butters their bread. These contractors often prioritize the insurer’s budget over doing the job right, leaving you with shoddy repairs. That initial conversation can lock you into a story that makes it nearly impossible to fight for the full settlement you’re owed later on.

The Conflict of Interest Is Immediate

Let’s be blunt: there’s a massive, unavoidable conflict of interest. Your goal is simple—to get your home and your life back to the way it was before the disaster. The insurance company’s goal is also simple—to protect its bottom line and keep shareholders happy by paying you as little as legally possible.

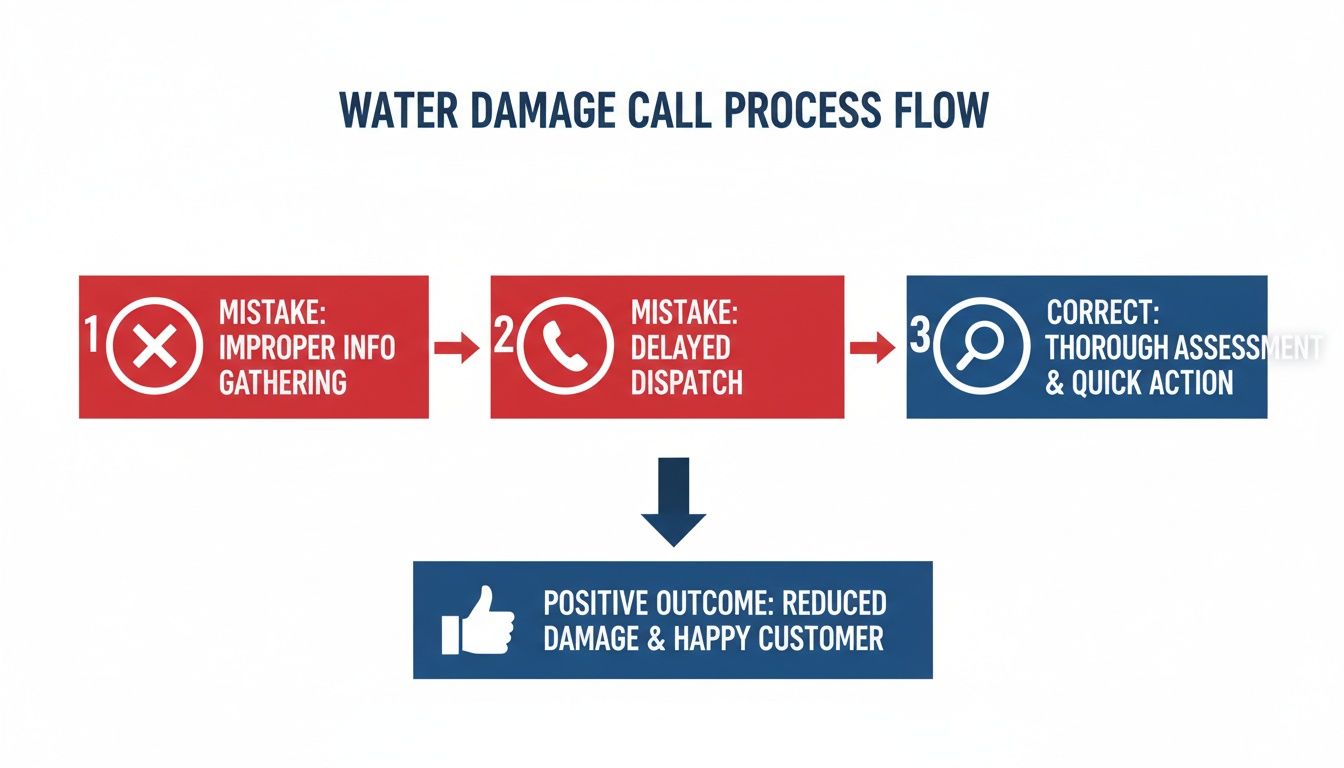

This flowchart lays it out perfectly. It shows the difference between the common mistake most homeowners make and the correct first move after finding water damage.

As you can see, calling an expert first puts you back in the driver’s seat.

Instead of calling the 1-800 number on your policy, your first call should be to a licensed public adjuster. We work exclusively for you, the policyholder. Period.

We level the playing field. We take over the entire claim, documenting every square inch of damage, digging into your policy to find every bit of coverage you’re entitled to, and building an ironclad case before the insurance company even knows there’s a problem.

This proactive strategy stops the insurer from controlling the story. It positions your claim for a fair and complete settlement from day one. You can get a deeper understanding by reading our guide on what a public adjuster does.

Finding The Right Restoration Team To Protect Your Claim

Here’s a hard truth: after a water disaster, your insurance company will rush to give you a list of their “preferred vendors.” It feels helpful, but it’s a strategic move designed to control one thing—their bottom line.

These contractors have cozy relationships with insurers, often agreeing to work within tight budgets. What does that mean for you? It means cut corners, rushed jobs, and repairs that don’t last.

Hiring the wrong team doesn’t just put your home at risk; it can completely tank your insurance claim. A vendor who gets most of their business from your insurance company isn’t working for you. Their loyalty is to the carrier, so their main goal is a quick, cheap fix that gets the claim off the insurer’s books.

This is why you absolutely must find an independent contractor who answers to you. A truly independent water damage restoration service near me will work hand-in-glove with your public adjuster, not the insurance company. Their only objective is to restore your property correctly and document every last detail to justify the full settlement you deserve.

Vetting Your Restoration Contractor

Finding a qualified, independent team is non-negotiable. The restoration industry has exploded, with over 35,000 companies now operating in the U.S. While more options can be good, it also means the market is flooded with inexperienced or outright shady operators.

When you’re on the phone with a potential contractor, you need to ask some pointed questions:

- Are you IICRC certified? The Institute of Inspection, Cleaning and Restoration Certification (IICRC) is the gold standard. If they don’t have this certification, hang up. It’s a massive red flag.

- Can you work directly with my public adjuster? You’re looking for a team player who knows their job is to fix the damage, while your adjuster’s job is to fight for the claim.

- Are you independent, or on an insurer’s preferred vendor list? Be direct. Politely turn down anyone who primarily gets their work from insurance carriers.

The Power of An Independent Team

When you’re choosing a restoration team, don’t forget to ask about their emergency response. A company that uses professional emergency answering services is far more likely to get boots on the ground 24/7, which is critical for stopping the damage from getting worse.

The right restoration company becomes your claim’s secret weapon. They provide the detailed scope of work, the photos, and the expert evidence that your public adjuster will use to go to war for you. This partnership ensures the repairs are based on what your home actually needs, not what your insurance company feels like paying for.

To see how this powerful partnership works in your favor, take a look at our guide on finding a public adjuster near you.

How To Fight Common Insurance Delay And Deny Tactics

Once you’ve hired an independent restoration contractor, the real fight begins. It’s you against your insurance company, and they have a playbook filled with tactics designed to wear you down, confuse you, and make you accept a lowball settlement just to get it over with.

They are counting on your exhaustion and lack of expertise in the fine print of your policy.

Their strategy is almost always the same: delay and deny. They’ll bury you in endless, often repetitive, requests for documentation. The friendly adjuster you first spoke to will suddenly become a ghost, impossible to reach for days or even weeks. These aren’t just clerical errors; they are deliberate tactics to make the process so miserable that you’ll take any offer they throw at you.

Dismantling Common Denial Excuses

One of the oldest tricks in the book is blaming the damage on “long-term issues” or “poor maintenance.” When their adjuster sees water damage, their first instinct isn’t to help you—it’s to find a way to frame it as a slow leak you should have fixed ages ago. Anything but the sudden, accidental event that your policy actually covers.

Case Study: The “Maintenance Issue” Denial

A homeowner in Raleigh, NC, had a pipe burst behind a kitchen wall, flooding the entire first floor. The insurance company denied the claim, saying the pipe was old and its failure was a maintenance issue, not a covered loss. Frustrated and overwhelmed, the homeowner called us. We brought in a forensic plumber who proved the pipe actually failed due to a sudden pressure surge—a classic “sudden and accidental” event. Faced with expert evidence they couldn’t refute, the insurer reversed their denial and paid the $42,000 claim in full.

This is exactly how insurers twist the facts. They hide behind vague policy language to deny legitimate claims, knowing most people don’t have the technical background to fight back.

A public adjuster’s job is to tear these flimsy arguments apart with cold, hard evidence. We use professional-grade tools like moisture mapping and thermal imaging to build an undeniable timeline, proving the damage is covered under your policy’s terms.

Holding Your Insurer Accountable for Delays

When your insurance company intentionally stalls your claim, it’s not just bad customer service—it’s often an act of bad faith. These delays aren’t just an inconvenience; they prevent you from making critical repairs, which allows secondary damage like mold to spread and makes your home unlivable.

This is a strategy, plain and simple.

To counter it, a public adjuster establishes a firm, professionally documented line of communication. Every phone call, email, and document request is meticulously tracked. We set clear, reasonable deadlines for responses and know exactly who to escalate to when those deadlines are ignored.

This relentless, professional pressure changes the dynamic entirely. It signals that you are not an easy target and that we will not let them drag their feet. We manage the entire process, holding them accountable at every step to push your claim toward a fair and timely resolution. If you’re wondering what “timely” means, you can get a better sense of the timeline by learning how long an insurance claim should take in our detailed guide.

Insurance carriers use a standard set of tactics to protect their bottom line. But once you understand their game, you can start to build a defense.

Common Insurer Tactics vs Policyholder Counter-Strategies

| Insurer Tactic | What It Looks Like | Public Adjuster Counter-Strategy |

|---|---|---|

| Endless Document Requests | They repeatedly ask for the same documents or send vague, confusing requests for information you’ve already provided. | We organize and submit a comprehensive evidence package upfront, creating a single source of truth and making repetitive requests easy to refute. |

| “Ghosting” by the Adjuster | Your calls and emails go unanswered for days or weeks, bringing your claim to a complete standstill. | We establish a formal communication schedule, follow up relentlessly, and escalate to management when the adjuster is non-responsive. |

| Blaming “Pre-Existing” Damage | The adjuster claims the damage was caused by a slow leak or poor maintenance, which isn’t covered by your policy. | We bring in independent experts (engineers, plumbers) to provide unbiased reports that prove the damage was sudden and accidental. |

| Lowball Settlement Offer | They present an offer that doesn’t come close to covering the actual cost of repairs, hoping you’ll accept it out of desperation. | We create our own highly detailed, line-by-line estimate using industry-standard software to prove the true value of the claim and negotiate from a position of strength. |

| Misinterpreting Policy Language | They use confusing or ambiguous language from your policy to justify a denial for a clearly covered event. | We are policy experts. We analyze the specific language of your contract and cite state statutes to hold the insurer to the coverage you paid for. |

These counter-strategies take the control away from the insurance company and put it back where it belongs—with you. It’s about leveling the playing field with expertise and documentation they simply can’t ignore.

The Hidden Costs Your Insurer Hopes You Overlook

That first estimate you get from the insurance company’s adjuster? Let’s be very clear about what it is: a starting offer. It’s the beginning of a negotiation, and it’s almost always designed to protect their bottom line, not make you whole again.

Insurers have a playbook for this. They routinely “overlook” critical secondary damages to keep their payout as low as possible, leaving you holding a check that doesn’t even come close to covering the real cost of putting your home back together. It’s a calculated strategy, and they’re betting you don’t know enough about construction to spot what they’ve left out.

Beyond The Surface Damage

Water damage isn’t just about a stained ceiling or warped floorboards. Water is insidious. It gets into every crack and crevice, and the real, expensive damage is almost always the stuff you can’t see. This is exactly what your insurer hopes you’ll miss.

- Hidden Mold and Rot: Once moisture gets trapped behind your walls, under flooring, or soaked into insulation, it becomes a ticking time bomb. It’s the perfect breeding ground for toxic mold and structural rot. An adjuster’s quick walk-through with a clipboard will never account for the cost of properly tearing out and remediating this kind of hazard.

- Compromised Electrical Systems: Water and wiring are a lethal combination. Any outlets, junction boxes, or wiring that got wet might look fine, but they could be a serious fire hazard waiting to happen. A proper repair means having a professional inspect and likely replace these components—a major cost that rarely makes it into that first lowball estimate.

- Damaged Personal Belongings: Your policy is supposed to cover your personal property, but adjusters are notorious for undervaluing or completely omitting items. A public adjuster, on the other hand, will document everything—from your sofa and TV down to your clothes and family photos—to make sure you get compensated for their true replacement value.

The True Cost of Rebuilding

Even when your insurer accounts for the obvious damage, their estimate is still likely to fall way short. They routinely leave out costs that are legally required for a proper rebuild, expecting you to eat the difference.

An insurer’s estimate is a reflection of their liability, not your recovery. They will omit anything they can plausibly deny, from code upgrades to the cost of matching your 10-year-old hardwood floors, hoping you won’t know enough to fight back.

They conveniently “forget” to include local building code upgrades that are triggered by major repairs. For example, if your damaged plumbing has to be brought up to current code during the repair, that’s a covered expense they absolutely should be paying for. They also love to use outdated material costs and lowball local labor rates, completely ignoring what it actually costs to get the work done right.

Water damage is a massive problem—around 14,000 Americans deal with a water emergency every single day, and it makes up nearly 30% of all homeowner claims. This isn’t a new game for the insurance companies. As industry statistics show, they’ve had plenty of practice perfecting the art of the lowball offer.

That’s why getting your own independent, line-by-line estimate from a public adjuster is the single most powerful thing you can do. It exposes all the gaps and gives you the ammunition you need to demand the full, fair settlement you’re owed.

A Real Client’s Victory Against A Low-Ball Offer

Talk is cheap. Real-world results are what matter. Let me tell you about a family right here in North Carolina whose home was completely wrecked by a burst pipe. We’re not talking about a small puddle—this was a disaster that soaked floors, ruined drywall, and destroyed their kitchen cabinets. Worse, it created the perfect dark, damp environment for hidden mold to explode.

Their insurance company, one of the big national names you see on TV, was out there fast. Their adjuster walked through for a few minutes, snapped some pictures, and a week later, sent over an offer. The check was for just under $28,000.

They were told it was more than enough. But the estimate from their trusted, independent water damage restoration service near me came in at nearly $60,000.

Suddenly, they were staring at a $32,000 hole, expected to pay for over half the repairs themselves. This is that gut-sinking moment where homeowners feel trapped and hopeless. It’s a classic low-ball strategy, and it almost worked.

How We Turned The Claim Around

Feeling totally defeated, the family gave us a call. We immediately took over the fight.

Our very first move was to bring in our own team of experts, including a certified mold remediation specialist and a structural engineer—not just a generalist with a clipboard. We deployed thermal imaging cameras and professional moisture meters to map out the true extent of the water’s path. We proved it had wicked deep into the wall cavities and subfloor, damaging areas the insurer’s adjuster conveniently overlooked.

We then built our own exhaustive, line-by-line estimate using the same software the insurance industry uses. But here’s the difference: our estimate was based on reality. It included everything they were actually owed under their policy.

- Costs to bring the home up to current building codes.

- The price for properly matching existing materials (not just cheap, mismatched patches).

- The true cost of skilled, local labor—not some national average.

Armed with an undeniable mountain of evidence, we went back to the insurance company. We didn’t just ask for more money; we proved, with expert reports and irrefutable photographic evidence, why their first offer wasn’t just low—it was an act of bad faith.

After some tough back-and-forth, they had no ground to stand on. The final settlement came in at $61,500.

That’s more than double their insulting first offer. It was enough to cover the entire restoration, allowing the family to rebuild their home the right way without draining their savings. This story isn’t a one-off; this is what we do.

Proof From A Satisfied Client

You don’t have to take our word for it. Here’s a review from another client who was in the exact same nightmare scenario and came out on top because they had an advocate in their corner.

When your insurance company offers you a fraction of what you need, everything is on the line. Having an expert who steps in to take over the fight is what separates a devastating financial loss from a complete, proper recovery.

Your Questions About Water Damage Claim Disputes Answered

When you’re trying to navigate a disputed water damage claim, the stress and confusion can be overwhelming. The insurance company starts throwing around technical jargon or flimsy excuses to deny coverage, and it feels like you’ve been pushed into a corner with no way out.

Let’s cut through the noise. Here are some direct, no-nonsense answers to the questions we hear from homeowners every single day.

“My Insurer Says The Damage Is From A ‘Slow Leak’ And Isn’t Covered. Can I Fight This?”

Yes, and you absolutely should. This is a classic denial tactic—one of their favorites, in fact. They blame you for “neglected maintenance” to shift the financial burden from their books to your bank account.

Don’t let them get away with it. A public adjuster’s first move is to counter this by bringing in our own team of independent plumbers or engineers. We don’t just take the insurance company’s word for it. We find out what really happened.

Using tools like moisture mapping and thermal imaging, we gather hard evidence to prove the loss was “sudden and accidental” as defined by your policy. This data-driven approach completely dismantles their weak argument and forces them to cover the claim like they should have from the start.

“The Insurance Company’s Check Doesn’t Even Come Close To The Restoration Estimate. What Now?”

Whatever you do, do not cash that check. This is critical. Cashing it can be legally interpreted as your acceptance of their lowball settlement offer, which slams the door shut on any further negotiation.

This is a standard playbook move. They’re banking on your desperation for funds, hoping you’ll take their unfair offer just to get things moving.

A public adjuster will perform a meticulous, line-by-line review of their estimate and compare it against the reality of your contractor’s scope of work. We find everything they conveniently “missed”—from local code upgrade requirements to the actual cost of matching your floors and cabinets. Then, we file a formal supplemental claim demanding every penny required to make you whole again, backed by indisputable proof.

“Is It Too Late To Hire A Public Adjuster If My Claim Was Already Denied?”

No, it is definitely not too late. In fact, a huge number of our clients come to us right after getting that dreaded denial letter. A denial isn’t the end of the road; it’s just the start of the real fight.

The moment we take your case, we get a copy of your entire policy and the insurer’s official reason for the denial. From there, we launch our own independent investigation to build a powerful new case with compelling evidence they never bothered to find. We handle all the frustrating phone calls and paperwork, file the formal dispute, and go to bat to get that denial overturned.

“Why Can’t My Restoration Contractor Just Negotiate The Claim For Me?”

This is a big one. In states like North Carolina and Virginia, it is flat-out illegal for a contractor to negotiate an insurance claim on your behalf. This is called the unauthorized practice of public adjusting.

Your contractor is an expert at fixing the damage—and you need them. But they are not licensed or legally allowed to interpret policy language, argue coverage disputes, or negotiate a financial settlement with the insurance company. They risk losing their license if they try.

Only a licensed public adjuster is legally empowered to act as your advocate against the insurance company. We are your dedicated representative, ensuring your rights are protected throughout the entire claims process. Your contractor repairs the damage; we make sure the insurer pays for it.

When you’re facing a water disaster and an insurance company that won’t cooperate, you need a fighter in your corner. The team at For The Public Adjusters, Inc. is ready to take on that fight for you.

Contact us today for a no-cost claim review and find out how we can secure the full and fair settlement you are owed. https://forthepublicadjusters.com

Trackbacks/Pingbacks