When your home or business gets hit by a devastating fire, flood, or storm, the absolute last thing you should have to deal with is a fight with your own insurance company.

Yet, that's the reality for too many policyholders. When you start searching online for a "public adjuster near me," you’re taking the first critical step toward leveling a playing field that is, by design, tilted heavily in the insurer's favor.

A public adjuster is a state-licensed advocate who works exclusively for you, the policyholder. Their entire job is to dispute lowball offers and fight to make sure you get the maximum, fair settlement you're entitled to under your policy.

Why Your Search for a Public Adjuster Is So Critical

The moment you file a claim, your insurance provider—whether it's Allstate, State Farm, or another big-name carrier—sends their own adjuster to your property. This person might seem friendly, even sympathetic. But don't be mistaken: their ultimate loyalty is to their employer.

Their primary role is to protect the insurance company's bottom line. That often means minimizing your payout through lowball offers, frustrating claim delays, and narrow, self-serving interpretations of your policy. It's an immediate and unavoidable conflict of interest.

You're not an insurance expert, but their adjuster is. They use complicated policy jargon and proprietary estimating software to justify paying you far less than what you actually need to rebuild your life. A public adjuster is your countermeasure to this unfair advantage.

Who Is Really on Your Side in a Property Damage Claim

It’s easy to get confused about who is working for whom. This table breaks down the fundamental difference between the adjuster your insurer sends and the public adjuster you hire.

| Attribute | The Insurer's Adjuster | Your Public Adjuster |

|---|---|---|

| Who They Work For | The insurance company. | You, the policyholder. |

| Primary Loyalty | To protect the insurer's financial interests. | To protect your financial interests. |

| Main Goal | To minimize the claim payout. | To maximize your fair settlement. |

| Motivation | Salary and bonuses from the insurer. | A small percentage of the final settlement. |

The takeaway is simple: the insurance company’s adjuster is paid to save them money. Your public adjuster is paid only when they get you more money.

An Advocate on Your Side

Hiring a public adjuster isn't just about getting a second opinion; it's about securing professional representation dedicated solely to your recovery. They become your personal advocate, tasked with meticulously documenting your loss, accurately valuing every detail of the damage, and negotiating aggressively on your behalf.

Here’s what that actually means for you:

- Expert Damage Assessment: They perform a forensic-level inspection of your property to find all the damage—especially the hidden issues the insurer's adjuster might conveniently "overlook."

- Policy Mastery: They know the fine print of your policy inside and out. They use that language to your advantage, making sure every single covered loss is identified and claimed.

- Stress Reduction: They take over. All the phone calls, the endless paperwork, and the looming deadlines are no longer your problem, freeing you to focus on your family or business.

The claims adjusting industry has exploded into a massive field, with revenues hitting $14.6 billion on the back of a 9.6% annual growth rate. This isn't random; it reflects the skyrocketing number of property damage claims from events like the hurricanes and storms that regularly impact homeowners across North Carolina and Virginia.

Public adjusters exist to counter this massive industry and fight for fair outcomes. By understanding what a public adjuster does, you can see just how essential they are in this high-stakes process.

How to Find the Right Public Adjuster to Represent You

When you’re staring down a lowball offer from a massive insurance carrier, you can't afford to bring just anyone into the fight. You need a seasoned pro on your side—someone with a documented history of turning around the unfair, low-end settlements that companies like State Farm and Allstate are notorious for.

Finding that person isn’t about a quick Google search. It’s a careful vetting process.

Your first move, always, is to verify their license. For us here in North Carolina, that means running their name through the NC Department of Insurance database. If you're in Virginia, you'll use the VA Bureau of Insurance. An active license isn't just a nice-to-have; it's the absolute minimum. Without it, you're dealing with an illegal operator who has zero authority to represent your claim.

Vetting Credentials That Matter

A license is just the ticket to the game. You need to dig deeper.

For complex claims involving fire, smoke, or water damage, look for certifications from the Institute of Inspection, Cleaning and Restoration Certification (IICRC). This is non-negotiable. These credentials prove the adjuster truly understands the science behind the damage. They can build a claim based on industry-standard restoration methods, not the insurer’s cheap shortcuts.

Next, ask for local references. And don't just ask—actually check them. Get the contact information for a few past clients in your area who had a similar disaster. A reputable adjuster with a solid track record will be happy to connect you. If they hesitate, that's a huge red flag. It helps to understand the general factors influencing a homeowner's hiring decision for any professional, because the core principles of trust and proven results are what matter most.

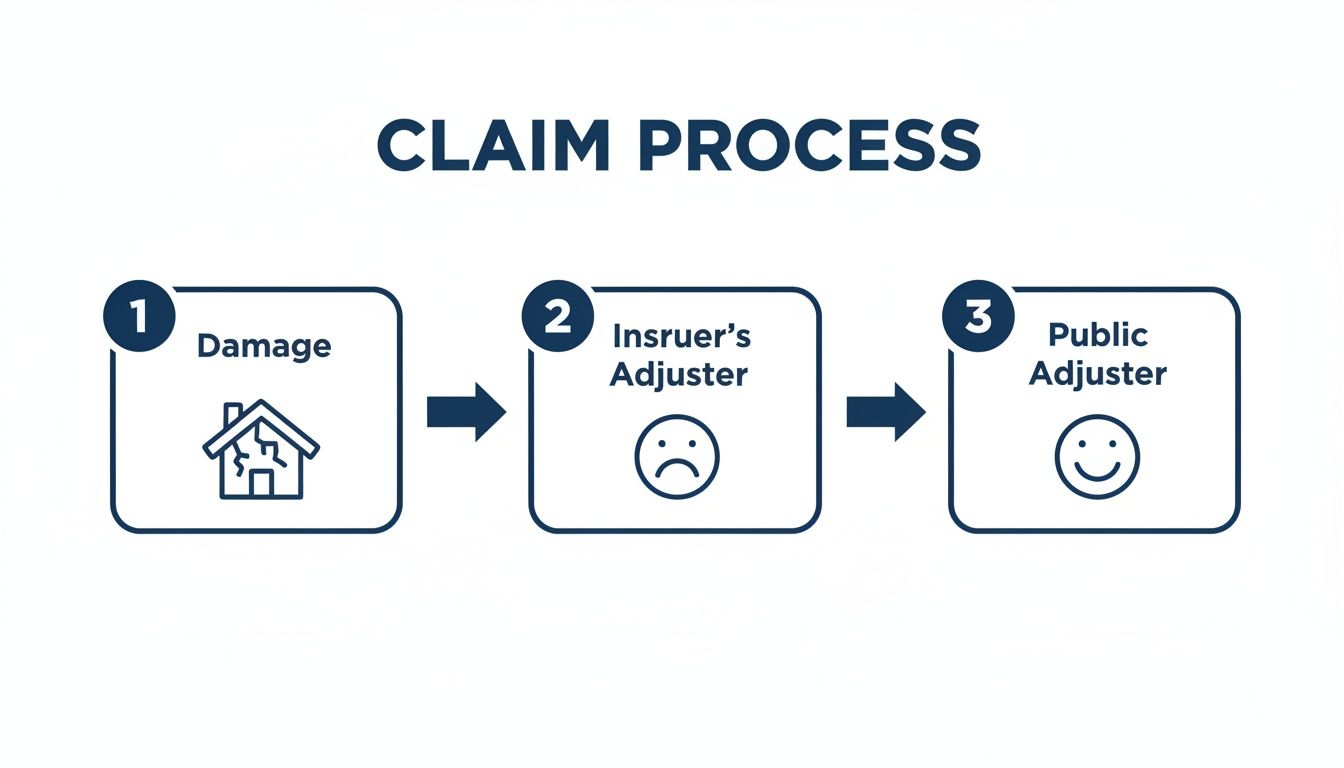

This whole process is about shifting the power dynamic back in your favor.

The image says it all. Hiring your own adjuster transforms the experience from one of frustration and fighting to one driven by a dedicated advocate on your side.

Spotting Common Red Flags

Knowing what to run from is just as important as knowing what to look for.

Be extremely wary of anyone asking for money upfront. The industry standard for a public adjuster is a contingency fee. This means they are paid a small, agreed-upon percentage of the final settlement they recover for you. No settlement, no fee. Simple as that.

A contingency fee model ensures the public adjuster’s financial interests are perfectly aligned with yours. Their only path to getting paid is by maximizing your settlement.

Another giant red flag is pressure. If someone shows up at the scene of your disaster and pushes you to sign a contract on the spot, walk away. These high-pressure sales tactics are the calling card of less reputable "storm chasers."

A true professional will offer a no-cost review of your claim and give you the time and space you need to make an informed decision. Taking a moment to really understand the critical differences between a public adjuster vs insurance adjuster will empower you to choose an advocate who actually works for you, not the insurance company.

Getting Your Ducks in a Row Before You Hire a Public Adjuster

Once you've got a promising public adjuster in your sights, the next move is yours. You need to equip them to fight for you.

Walking into that first meeting organized and ready can make a world of difference. It speeds everything up and gives a good public adjuster the ammo they need to start picking apart the insurance company's weak arguments right from the get-go.

Think of it as putting together the opening argument for your case. The more thorough your documentation, the faster a sharp adjuster can find the holes in your insurer's assessment. This prep work is what allows them to conduct a powerful, no-cost claim review and immediately spot where your carrier is vulnerable.

Your Essential Document Checklist

Before you sit down with anyone, you need to gather every scrap of paper and every digital file connected to your claim. This isn't just about being tidy; it's about building a fortress of evidence your insurance company simply can't ignore.

Here’s the critical information you absolutely must have ready:

- Your Complete Insurance Policy: I don't just mean the declarations page. You need the entire policy—all the endorsements, all the riders. This is the contract your insurer is bending in their favor, and your advocate needs to see every single word.

- All Communication with the Insurer: Get every email, certified letter, and text message you've exchanged with the insurance company. Pay very close attention to any official denial letters or documents explaining why they underpaid you. These are often full of flimsy excuses that a public adjuster loves to tear apart.

- Proof of Damage: This is your visual firepower. Round up every photo and video you took right after the damage happened and anything you documented during cleanup. If they're time-stamped, even better.

- Contractor Estimates: Have you had any contractors out to give you a quote for repairs? Bring those estimates. Even if they're just initial ballpark figures, they help establish a realistic baseline for what it actually costs to fix things, not the lowball number your insurer dreamed up.

Why This Preparation Matters So Much

Showing up with this organized file does two crucial things. First, it shows you're a serious, on-the-ball policyholder, which sets a professional tone for your new partnership. Second, it lets a public adjuster start strategizing immediately.

They can cross-reference the damage in your photos with the fine print in your policy and stack your contractor's estimate against the insurer's insultingly low offer. This initial analysis is how they draw the roadmap to either overturn a denial or blow a lowball settlement out of the water.

Imagine a business owner whose fire damage claim was short-changed by Allstate because their adjuster claimed to have "missed" the smoke and soot contamination in an adjoining office. By showing up with photos of the soot, the insurer's letter, and an estimate from a professional remediation company, that owner gives a public adjuster everything they need to prove the carrier's negligence on day one.

Being prepared isn’t just a nice-to-have. It’s your first real offensive move in the fight for a fair settlement. It turns that first meeting from a simple introduction into a full-blown strategy session.

What Happens After You Hire a Public Adjuster

The moment you bring a public adjuster on board, the entire dynamic of your claim shifts. You're no longer on the defensive, trying to fend off an insurance company's adjuster who is trained to protect their employer's bottom line.

Now, you're on the offensive. You have a licensed expert in your corner, ready to systematically dismantle the carrier's lowball offer and build an undeniable case for the full amount you're actually owed.

This process is both methodical and aggressive. Your new advocate takes the reins, launching a forensic-level reinvestigation of the damage. This isn't just another quick walk-through; it's a deep dive to find every single detail the insurance company's adjuster conveniently overlooked or intentionally left out.

Building an Overwhelming Case for a Full Payout

The first order of business is to create a new, incredibly detailed scope of loss. This document becomes the bedrock of your fight.

While the insurer’s initial scope might list some cheap, superficial repairs, your public adjuster’s version will be exhaustive. It accounts for hidden structural damage, necessary code-compliance upgrades, and the real-world costs for proper repairs—not the cut-rate alternatives the carrier wants you to accept.

With this detailed scope in hand, your adjuster officially supplements your claim. They formally notify the insurance company that their initial assessment is rejected and present a comprehensive package of evidence. This package is loaded with the new scope, expert reports, extensive photo and video documentation, and a firm demand for a much higher settlement.

The negotiation phase starts here, but it's not some friendly back-and-forth. It’s an evidence-based battle where your adjuster refutes every argument, delay tactic, and excuse the insurance company throws at them.

Think of it like this: A Raleigh, NC, business owner had his fire claim severely underpaid. The insurer’s adjuster completely ignored the smoke and soot damage that had seeped into an adjacent, supposedly "undamaged" unit. Our team brought in an industrial hygienist whose air quality tests proved widespread contamination, making the entire space unsafe and unusable. Faced with that undeniable expert evidence, the carrier was forced to triple their initial offer to cover the full remediation and business interruption losses.

Aggressive Negotiation and Final Settlement

This is where a public adjuster really earns their fee. They take over all communications, shielding you from the stress while they apply relentless, strategic pressure on the insurance company. They know the carrier's weak points and exactly how to use your policy language and state regulations as leverage.

This is why homeowners and business owners who hire representation almost always get better results. It's not magic; it's about leveling a playing field that's intentionally tilted in the insurer's favor. Your public adjuster is the counterweight to the inherent conflict of interest that exists when an insurance company uses its own people to decide how much they should pay you. For a closer look at what this takes, check out these strategies for powerful claims.

The fight ends when the insurance company finally agrees to a fair settlement based on the overwhelming evidence presented. Your public adjuster will review the final offer with you to ensure it covers the full scope of your loss. Only then, after you approve, do they collect their pre-agreed contingency fee from the new money they secured for you.

You're finally made whole—not because your insurer did the right thing, but because your advocate forced them to.

Navigating Claims in North Carolina and Virginia

Local knowledge is a powerful weapon in any insurance dispute. The challenges a homeowner faces in coastal Virginia after a hurricane are a world away from someone dealing with ice dams in the North Carolina mountains. A generic, one-size-fits-all approach just doesn’t cut it when you're up against an insurer looking for any reason to deny or underpay your claim.

When you hire a local public adjuster, you’re partnering with someone who lives and breathes these regional risks. They know the specific tactics carriers use in our states. More importantly, they know how to push back using state-specific consumer protection laws. This localized expertise is everything, especially when you get dragged into the bureaucratic nightmare of federal flood insurance.

The Unique Challenge of NFIP Flood Claims

When a storm surge or flash flood wrecks your property, you're usually not dealing with your regular homeowners insurance company. Instead, you get thrown into the rigid and unforgiving world of the National Flood Insurance Program (NFIP), which is managed by FEMA. These claims are notoriously difficult.

The adjusters they send out typically work for "Write Your Own" (WYO) insurance companies contracted by the government. These folks operate under a strict set of federal guidelines that leave almost zero room for common sense or negotiation. They're known for their inflexible bureaucracy and tough-as-nails denials.

A public adjuster with real NFIP experience understands this system inside and out. They know the exact documentation needed for a Proof of Loss form and how to build a claim that meets FEMA's incredibly precise standards. Without that specialized knowledge, homeowners often get hit with devastating denials over minor paperwork errors.

A Virginia Beach business owner learned this the hard way after Hurricane Matthew. The WYO adjuster denied a huge part of their claim, citing insufficient proof. A public adjuster reopened the case, brought in meticulously detailed engineering reports and building material analysis, and successfully overturned the denial—recovering an additional $280,000 for the client.

Leveraging Local Laws to Fight Back

It’s not just about flood claims. Both North Carolina and Virginia have specific laws on the books designed to protect policyholders from bad-faith insurance practices. An experienced public adjuster uses these statutes as leverage.

When an insurer like Allstate or State Farm starts playing games with unreasonable claim delays or throws out an insulting lowball offer, your advocate can document this behavior as a violation of state law.

Suddenly, the fight isn't just about repair costs anymore. It becomes a potential legal battle the insurance company wants no part of.

Whether you need to know how to get more money from your fire damage adjuster in NC or VA or you're fighting a complex flood claim, a local public adjuster brings the specialized expertise you need to hold these giant companies accountable and get the settlement you rightfully deserve.

Common Questions About Fighting Your Insurer

When you’re staring at a damaged home and dealing with an insurance company that’s dragging its feet, you’ve got questions. The thought of searching for a "public adjuster near me" usually brings up a few key concerns about the cost, the timing, and what it means for your relationship with your insurer.

Let's clear the air on those right now. Getting answers upfront will give you the confidence you need to take back control of your claim.

How Does a Public Adjuster Get Paid?

This is the most important question, and the answer is simple: a legitimate public adjuster works on a contingency fee.

What does that mean? They get paid a small, agreed-upon percentage of the money they recover for you from your insurance company. There are no upfront fees. No retainers. No hidden charges. If anyone asks you for money to get started, you’re talking to the wrong person.

This structure is your protection. It aligns our goals perfectly with yours—if you don't get paid, we don't get paid. It’s that straightforward.

Can I Hire an Adjuster After My Claim Was Denied?

Yes. In fact, that's often the best time to bring in a professional. A denial letter from a big carrier like State Farm or Allstate isn't the final word. Think of it as their opening offer in a negotiation you didn't even know you were in.

Public adjusters are experts at picking apart denial letters. We know how to spot an insurer’s weak arguments, misinterpretations of your policy, or flat-out errors. We then reopen the claim with a mountain of new evidence, expert reports, and a formal dispute that they can’t ignore. Some of our biggest wins started with a flat-out, unfair denial.

A denial is a tactic, not a final verdict. It's the insurer's attempt to make you give up. An experienced public adjuster sees it as an invitation to prove them wrong with overwhelming evidence.

Will My Insurer Retaliate if I Hire a Public Adjuster?

This is a common fear, but the answer is a firm no. It is illegal for an insurance company to cancel your policy, raise your rates, or punish you in any way for exercising your right to hire a licensed public adjuster.

Public adjusting is a state-regulated profession created specifically to level the playing field between you and a massive insurance corporation. The law recognizes that power imbalance. Any threats or intimidation from your carrier’s adjuster are classic bad-faith tactics, and a good PA will document them immediately to use as leverage in your favor.

Don't let your insurance company dictate the value of your recovery. If you're struggling with a denied, delayed, or underpaid claim in North Carolina or Virginia, the team at For The Public Adjusters, Inc. is ready to fight for you. Contact us for a no-cost, no-obligation review of your claim today.

Get Your Free Claim Review Now