You’ve probably heard the term thrown around after a big storm, but because it’s an uncommon term, many ask, “What is Assignment of Benefits?

An Assignment of Benefits, or AOB, is a legal document. When you sign it, you’re giving a third party—usually the contractor fixing your property—the power to take over your insurance claim. They can bill your insurer directly, collect the payment, and manage the whole process for you.

If you have any questions about anything claim related we are here to help. Have your claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster.

Decoding an Assignment of Benefits

Let’s paint a picture. A nasty hailstorm just rolled through and your roof is a mess. A roofer knocks on your door and says, “Don’t worry about a thing. Just sign here, and we’ll handle the insurance company for you.”

That form is almost certainly an Assignment of Benefits. By putting your signature on it, you’re essentially handing them the keys to your insurance claim.

The big selling point is convenience. When you’re stressed and looking at a damaged home, letting someone else take over the paperwork and phone calls with your insurer sounds like a dream. The contractor gets to work right away, and you don’t have to pay out of pocket. But that convenience can come at a steep price: you lose all control over your own claim.

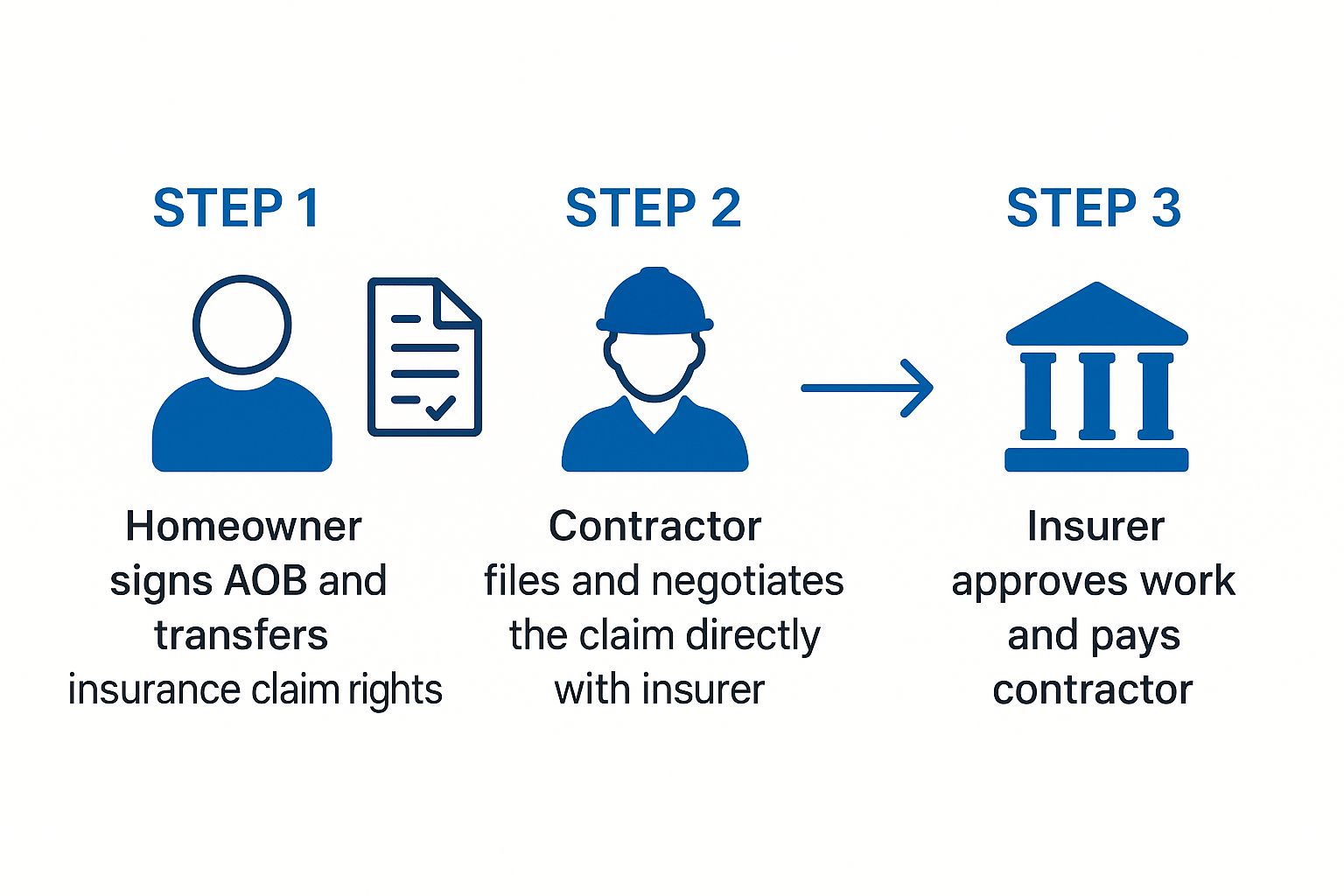

This visual gives you a quick look at how the AOB process works from start to finish.

As you can see, once you sign that document, you’re pretty much out of the loop on the money side of things. All financial talks happen between the contractor and the insurance company.

The Core Concept Explained

At its heart, an AOB is just a legal switcheroo. It changes who has the authority to use your policy benefits for that specific claim. This isn’t some new-fangled idea, either. The concept of assigning benefits has been a legal tool for over a century, originally common in healthcare to make sure doctors got paid by insurers. If you’re curious, you can explore more historical context about this legal tool and see how it’s changed over the years.

When you sign an AOB, the contractor basically steps into your shoes. They now have the power to:

- File the initial claim with your insurance company.

- Negotiate the repair costs and what work needs to be done.

- Send the bill straight to your insurer.

- Collect the insurance check—it never even touches your hands.

- And here’s the big one: Sue your insurance company if they don’t agree on the payment.

This transfer of power is legally binding and a real pain to undo. That’s why it’s so critical to know exactly what you’re signing before you pick up that pen.

To make it even clearer, let’s break down who does what before and after an AOB is signed.

Assignment of Benefits At a Glance

| Party | Role Before AOB | Role After AOB |

|---|---|---|

| You (The Homeowner) | In control of the claim. Communicates with the insurer, hires contractors, and receives the insurance payment. | Out of the financial loop. No longer controls claim negotiations or receives payment directly. |

| Your Contractor | Hired by you to perform repairs. You pay them directly, often using funds from the insurance check. | In control of the claim. Deals directly with the insurer, negotiates scope and cost, and receives payment from the insurer. |

| Your Insurance Company | Communicates with you. Issues payment directly to you (and your mortgage company, if applicable). | Communicates with the contractor. Issues payment directly to the contractor who holds the AOB. |

This table shows just how much the dynamic shifts. You go from being the one in the driver’s seat to a passenger along for the ride.

How an Assignment of Benefits Actually Works

To really wrap your head around what an AOB means for you, let’s walk through a situation we see all the time. Imagine a nasty hailstorm barrels through your town, tearing up your roof and causing a leak in the attic. What happens next is where the Assignment of Benefits contract enters the picture.

Panicked, you call the first roofer you can find for an emergency tarp and an estimate. The contractor shows up, walks the roof, and hands you a clipboard with their standard work agreement. But tucked in with that paperwork is another form: the Assignment of Benefits.

The contractor might sell it as a convenience, explaining that if you just sign it, they’ll handle the entire insurance mess for you. No more phone calls, no more adjusters—they take care of it all. It sounds great, but this is a critical moment where your next move can change everything.

The AOB Process in Action

The second your pen touches that AOB form, a whole chain of events kicks off, and you’re no longer in the driver’s seat for the financial side of things. Here’s a step-by-step look at what really goes down:

- You Sign Over Your Policy Rights: When you sign an AOB, you are legally transferring your rights and benefits for that specific claim directly to the contractor. This isn’t just giving them permission to talk to the insurance company; it’s a complete handover of your authority.

- The Contractor Takes Control: The roofing company is now, for all intents and purposes, you. They file the claim, write up the scope of work, and send every piece of documentation to your insurer. You may never even lay eyes on the final bill they submit.

- Negotiations Happen—Without You: Now, the contractor’s team starts haggling with the insurance adjuster over the cost of repairs. This is a huge potential conflict point. The contractor wants to get paid as much as possible, while the insurer wants to pay out as little as possible. This clash often leads to major disagreements and can even end up in court. We see this all the time when handling insurance claims and disputes.

- Payment Goes Straight to the Contractor: Once a settlement is reached (or awarded), the insurance company cuts a check and sends it directly to the contractor. The money never even hits your bank account, and you have zero say in approving that final payout amount.

Key Takeaway: An AOB fundamentally shifts your role from the person in charge of your claim to a mere spectator. The contractor isn’t just working for you anymore; they are now legally acting as you on all financial matters tied to the claim.

This process lays bare the core trade-off of an AOB. Sure, you get the convenience of offloading the claims paperwork. But what you give up is massive: you lose all control over the money, the scope of work, and the final outcome of your own insurance policy.

Weighing the Benefits and Risks of an AOB

Signing an Assignment of Benefits contract can feel like a double-edged sword. On one side, it offers a seemingly simple fix during a chaotic and stressful time. But on the other, it can pull you into a world of serious financial and legal headaches.

It’s absolutely critical to understand both sides of this coin before you even think about putting pen to paper.

The Upside of Convenience

Let’s be honest, the main appeal of an AOB is pure convenience. When your home has just been turned upside down by damage, the last thing you want is a second full-time job managing a complicated insurance claim.

By signing an AOB, you’re essentially handing the keys to the contractor. They take over the endless phone calls, the mountain of paperwork, and the frustrating back-and-forth negotiations with your insurance company. This can feel like a huge weight lifted off your shoulders when you’re already maxed out with stress.

For many homeowners, it seems like the fastest way to get repairs started. After all, the contractor is motivated to get the claim approved so they can get paid and get to work.

The Downside of Losing Control

While that convenience is tempting, the risks that come with an AOB are massive and can have devastating consequences. When you sign that document, you’re not just handing over the claim—you’re giving up your power.

You lose your seat at the negotiating table. Suddenly, you can’t talk to your own insurer, you can’t review the scope of work, and you have no say in the final costs. This throws the door wide open for a shady contractor to inflate the bill far beyond what’s reasonable.

If your insurance company pushes back and disputes the inflated charges, the contractor can sue them in your name, often without you even knowing. If the contractor loses that lawsuit, guess who they might come after for the money? You. Some will even slap a lien on your property, making it impossible to sell or refinance until their bill is paid.

The real danger with an AOB is that the contractor’s goals are no longer aligned with yours. Their mission is to get the biggest possible check from the insurer, which can lead to overblown costs, unnecessary work, and legal fights that put your home and your savings on the line.

Unfortunately, the rise in AOBs has also been tied to a spike in outright fraud. Some contractors have been caught billing insurers for double or triple the normal rates, charging for work they never did, or submitting duplicate claims. You can read more about how assignment of benefits fraud impacts insurers and homeowners alike.

Deciding whether to sign an AOB is a major decision. Here’s a simple breakdown to help you see the differences clearly.

Weighing Your Options AOB vs Direct Claim

| Aspect of Claim | With an AOB | Without an AOB (Direct Claim) |

|---|---|---|

| Control | Contractor makes all decisions. | You remain in full control. |

| Communication | Contractor speaks to the insurer. | You communicate directly with your insurer. |

| Payment | Insurance pays the contractor directly. | Insurance pays you directly. |

| Legal Rights | You sign over your rights to sue the insurer. | You keep all your legal rights. |

| Motivation | Contractor is motivated to maximize their payout. | You are motivated to get a fair and accurate settlement. |

Seeing it laid out like this makes the trade-offs pretty clear.

You are essentially trusting a contractor not just with repairing your home, but with your entire financial and legal standing. This is why it’s so important to explore safer alternatives. For example, learning about the benefits of hiring a public insurance adjuster shows you how to get expert help without signing away your rights. A public adjuster works for you, not the contractor, making sure your best interests are protected every step of the way.

Red Flags to Spot Before Signing an AOB

When you’re reeling from property damage, a contractor showing up and offering a fast solution can feel like a godsend. But if they immediately push an Assignment of Benefits form in front of you, that’s your cue to hit the brakes. Learning to spot the predatory tactics is the only way to protect yourself from financial ruin and keep control of your own insurance claim.

Shady contractors count on your stress and confusion to trick you into signing a bad deal. Knowing their playbook is your single best defense.

High-Pressure Tactics

One of the oldest tricks in the book is creating a false sense of urgency. A contractor might try to rush you into signing an AOB on the spot, using lines designed to make you panic.

- “This deal is only good for today.” This is a classic sales gimmick meant to stop you from reading the fine print or getting a second opinion.

- “We have to start right now to stop more damage.” While this can be true, it’s often used as an excuse to get you to sign away your rights before you’ve had a chance to think.

- “All your neighbors are using us.” They’re banking on social pressure, making you feel like you’re missing out if you don’t jump on board immediately.

A true professional will always give you the time and space you need to review a contract and make a clear-headed decision. They won’t try to manufacture a crisis.

Vague or Incomplete Contracts

You should never, ever sign a document with blank spaces or fuzzy details. An AOB is a legally binding contract, and you can bet that any ambiguity will be used to the contractor’s advantage, not yours.

Crucial Reminder: A legitimate contract will spell everything out: a clear scope of work, a line-by-line cost estimate, and all terms and conditions. If a contractor hands you a blank AOB and says they’ll “fill it in later,” show them the door. That’s not just a red flag—it’s a blaring siren.

Promises That Seem Too Good to Be True

If a contractor’s pitch sounds like a late-night infomercial, it’s time to be skeptical. These too-good-to-be-true offers are just bait to get you to sign the AOB, and they often stray into the territory of insurance fraud.

Be on high alert for any contractor who offers to:

- Waive your deductible: Your deductible is a non-negotiable part of your insurance policy. A contractor who says they’ll “eat the cost” is usually just jacking up their bill to your insurer to make up the difference. This is illegal in many states.

- Give you a “free” roof or kitchen: There’s no such thing as a free lunch, and there’s definitely no such thing as a free remodel. This is just code for, “We’re going to massively overbill your insurance company,” a move that can get your claim denied and land you in legal hot water.

A legitimate Assignment of Benefits has to be built on a clear, honest agreement. These red flags are a pretty clear sign that the contractor doesn’t have your best interests at heart.

Safer Alternatives to Signing an AOB

If the idea of signing away your rights in an Assignment of Benefits agreement feels wrong, that’s because it often is. There are much safer ways to handle your claim. Handing over the keys to your insurance policy isn’t the only way to get your home or business repaired.

Let’s look at some better options that keep you in control of your claim and your money.

The simplest path is to manage the claim directly. This keeps you in the driver’s seat, plain and simple. You talk to your insurer, you hire the contractor you trust, and the settlement check comes to you. You pay the contractor only when you’re satisfied with the work, giving you the final say on quality.

Using a Direction to Pay

A Direction to Pay is a much safer, stripped-down document. Think of it as a specific instruction slip for your insurance company. It simply authorizes them to pay your contractor a set, agreed-upon amount directly from your settlement.

Unlike an AOB, it doesn’t transfer any of your policy rights. You’re still in charge of all negotiations and any legal steps that might be needed.

Hiring a Public Adjuster

For property owners who want an expert in their corner without giving up control, hiring a licensed public adjuster is the best move you can make. A public adjuster is a state-licensed claims professional who works for you—not the insurance company and not the contractor.

A public adjuster’s job is to get you the biggest and fairest settlement possible. Their success is tied directly to yours, as they’re paid a small percentage of the final claim amount.

This expert takes the entire claims process off your shoulders, handling everything from:

- Thoroughly documenting every last bit of damage.

- Negotiating with the insurance company to get you a fair settlement.

- Managing all the tedious paperwork and communication.

This frees you up to focus on getting your life back to normal while a dedicated advocate fights for your best interests. You can learn more about how a public insurance adjuster can be your best defense during the process.

Sadly, the misuse of AOBs has created massive problems. Industry reports show AOB-related fraud and abuse can inflate claim costs by a staggering 20-40% in some states, which ends up driving up insurance premiums for everyone. You can read more about how AOBs impact consumers on floir.com. Choosing a safer alternative doesn’t just protect your claim—it helps keep the entire insurance market fair.

Your Top Questions About AOBs Answered

Property insurance claims are confusing enough on their own. Throw an Assignment of Benefits agreement into the mix, and it’s easy to feel lost. Let’s clear things up by tackling the most common questions homeowners have when a contractor hands them an AOB to sign.

Can I Get Out of an AOB After I’ve Signed It?

This is a huge question, and the answer comes down to where you live. Some states, like Florida, have passed laws giving homeowners a “right of rescission.” This gives you a very short window—usually just a few days—to cancel the AOB without any penalty.

But in many other states, including North Carolina and Virginia, an AOB is a legally binding contract the second your pen leaves the paper. Once it’s signed, you can’t just change your mind. That’s why you should never sign one of these when you feel pressured or rushed.

What Happens if My Insurance Company Pays Less Than the Contractor’s Bill?

This is where homeowners get into serious trouble with AOBs. Let’s say your contractor submits a huge invoice, but your insurance company pushes back, arguing the bill is inflated or covers work that wasn’t necessary. A fight is pretty much guaranteed.

Because the contractor now holds your legal rights, they can sue your insurance company directly. If they lose that lawsuit, or if the insurer simply won’t budge on the payment, the contractor might turn their attention back to you. They could put a lien on your property or even sue you personally for the remaining balance. You’re left stuck in the middle, on the hook for thousands over a dispute you had zero control over.

The Hard Truth: An AOB does not get you off the hook financially. When your contractor and insurer disagree on the price, you’re the one who could end up paying the difference.

The Contractor Offered to Waive My Deductible. Is That a Red Flag?

Yes, it’s a massive red flag. In fact, in most states, this is considered insurance fraud. Your deductible is the portion of the claim you agreed to pay in your policy—it’s your skin in the game.

When a contractor says they’ll “waive,” “absorb,” or “cover” it, what they’re usually doing is secretly padding their bill to the insurance company to make up that money.

Consider it a blaring warning sign that you’re dealing with a shady operator. A reputable, honest contractor will never ask you to get involved in a scheme that puts both you and your claim in legal hot water.

Trying to figure out these complex situations when your home is damaged is overwhelming. The team at For The Public Adjusters, Inc. is here to bring clarity and fight for your best interests. We make sure you get a fair settlement without ever having to sign away your rights. Learn how we can help at https://forthepublicadjusters.com.