What is replacement cost coverage? Replacement cost coverage is a policy loss-settlement method that pays to repair or replace damaged property with materials of like kind and quality at today’s prices — without subtracting depreciation. Unlike actual cash value, it does not penalize you for the age or wear of what was destroyed.

Written by a licensed public adjuster serving homeowners and commercial property owners in North Carolina and Virginia. NC Department of Insurance licensed public adjuster.

You open the claim packet, look at the insurer's estimate, and the numbers don't come close to what contractors are telling you. The check is small. The language is muddy. The adjuster keeps saying you have “replacement cost coverage,” but somehow you're still staring at a shortfall.

That's not confusion on your part. That's where a lot of property claims go off the rails.

I've seen this pattern over and over in homeowner and business property claims across North Carolina and Virginia. The carrier throws around terms like replacement cost, actual cash value, depreciation, and limits, then acts like the low number on page one is the complete picture. It usually isn't. If your house, rental, office, or building suffered fire, water, wind, hail, hurricane, or storm damage, you need to understand exactly what the policy owes and where the insurance company will try to shave it down.

Table of Contents

- Your Insurer's Low-Ball Offer on Replacement Cost Coverage

- Replacement Cost vs Actual Cash Value The Insurer's Shell Game

- How Do I Recover Withheld Depreciation Under a Replacement Cost Policy?

- What Are the Biggest Replacement Cost Claim Traps for NC and VA Homeowners After a Hurricane?

- What Policy Loopholes Do Insurers Use to Reduce Your Replacement Cost Payout?

- When Should You Hire a Public Adjuster to Fight a Replacement Cost Claim Dispute?

- Don't Accept a Low-Ball Offer Get Expert Claim Help Now

Your Insurer's Low-Ball Offer on Replacement Cost Coverage

The scene is familiar. A pipe bursts, a kitchen fire spreads smoke through the house, or hurricane winds tear off roofing and let water in. You report the loss. The insurance company sends its adjuster. Then you get an estimate that reads like someone inspected your property from the end of the driveway.

The floors are undercounted. The trim is missing. The paint scope is chopped up room by room when the repair requires full continuity. The insurer prices “spot repairs” while your contractor explains that the damaged material can't be matched or safely patched.

That's when people start wondering whether replacement cost coverage means anything at all.

What the low-ball usually looks like

A low-ball offer rarely arrives with a label that says “we're underpaying you.” It shows up dressed as an official estimate. It may include just enough line items to look legitimate while subtly excluding the actual cost to restore the property.

Common patterns include:

- Partial scoping: The insurer pays for visible damage but ignores what has to be removed to reach it.

- Cheap material assumptions: The estimate uses lower-grade finishes than what was present in the home or building.

- Labor shortcuts: Tasks are broken apart in a way that strips out the true cost of coordination, setup, protection, and finishing.

- Premature depreciation: The carrier acts as if old materials justify paying less even when the policy promises replacement cost.

If you're trying to sanity-check floor damage, a practical comparison point is this guide to understanding wood floor replacement expenses. Not because it sets your claim value by itself, but because it helps you see how fast real-world repair decisions get more complicated than an insurer's stripped-down line item.

Practical rule: If the insurance estimate doesn't reflect how a contractor would actually perform the repair, it's probably not enough.

The real issue

Replacement cost coverage is supposed to pay to repair or replace damaged property with materials of like kind and quality at today's prices, not some bargain-bin version of your loss. When the carrier low-balls the scope, the unit pricing, or both, the policy problem isn't academic. It becomes your out-of-pocket burden.

You don't need to accept the first number just because it came on insurance company letterhead.

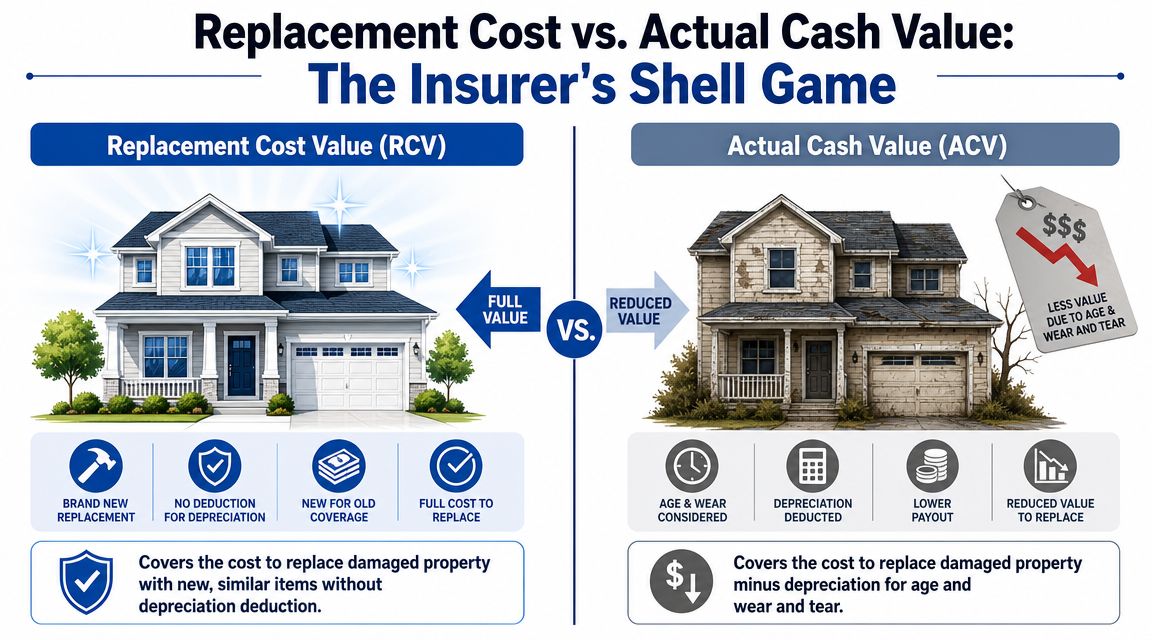

Replacement Cost vs Actual Cash Value The Insurer's Shell Game

You open the claim letter expecting replacement cost coverage. Instead, the insurer sends a check based on a lower number, then buries the rest behind conditions, depreciation, and paperwork. That is the shell game.

What Replacement Cost Coverage Promises

Replacement cost coverage is a loss-settlement method. It should pay what it costs to repair or replace damaged property with materials of like kind and quality at current prices.

Actual cash value works differently. It subtracts depreciation for age, wear, and condition before the insurer pays. That difference matters because no contractor is rebuilding your roof, cabinets, or flooring with old labor rates and half-worn materials.

Insurers count on policyholders to treat these terms like harmless definitions. They are not harmless. They decide how much cash you get now, how much gets held back, and how hard it will be to finish repairs without draining your own savings.

If you need the side-by-side breakdown in plain English, read this guide on actual cash value vs replacement cost.

How Carriers Turn RCV Into an ACV Claim

Many insurers do not start by paying full replacement cost, even under an RCV policy. They issue an initial payment based on ACV and hold back depreciation until repairs are completed and documented, as the North Carolina Department of Insurance explains in its ACV vs replacement cost guidance.

That delay is not neutral. It gives the carrier control.

They send less money up front. You scramble to cover demolition, materials, labor deposits, and code-related costs. If you cannot bridge the gap, the project stalls. Then the insurer acts like the unpaid balance is your problem, not the result of their payment structure.

Here is what that usually looks like:

| Settlement method | What the insurer pays first | What you must do to get more |

|---|---|---|

| ACV | Depreciated amount | Nothing more is owed under that method |

| Replacement cost coverage | Often an initial ACV-style payment | Complete repair or replacement and submit proof |

For policyholders in North Carolina and Virginia after a hurricane, this setup can get ugly fast. Roofs need tarping. Interiors need drying. Contractors want deposits. Materials cost what they cost. A thin first check can force bad repair decisions, long delays, or unfinished work that the carrier later uses against you.

A short explainer on the issue can help before you read the policy again:

The carrier may talk about replacement cost as if it is cash you can spend immediately. In many claims, it is a reimbursement system with strings attached.

Read the estimate line by line. Check whether the payment is ACV, whether depreciation was withheld, what conditions apply to recover it, and whether the insurer is using your policy limits as cover for an under-scoped claim. The first offer is rarely the true value of the loss.

How Do I Recover Withheld Depreciation Under a Replacement Cost Policy?

Recoverable depreciation is money the insurer owes under the right circumstances, but they won't hand it over just because your policy includes replacement cost coverage. You have to earn it in their system. That's the fight.

What the Insurer Is Betting You Won't Do

The carrier is counting on delay, confusion, and exhaustion. They know many policyholders won't keep clean records, won't understand the repair deadlines, or won't realize the policy includes conditions that can wipe out part of the recovery.

One trap is timing. Under functional replacement cost coverage, the policyholder may have to start repairs within 180 days to qualify for full payment, and if the insured amount is below 80% of functional replacement cost, the insurer can apply a proportionate coinsurance reduction, as discussed in this analysis of functional replacement cost coverage deadlines and coinsurance.

That means you can be right about the damage and still lose money because the insurer says you missed a condition.

The Paper Trail That Wins This Fight

You need documents. Not opinions. Not verbal assurances. Documents.

Build your file like you're preparing for an argument with someone who will pretend not to remember anything unless it's attached as a PDF.

- Signed contractor agreements: If the work requires replacement, your contract should say replacement.

- Detailed invoices: Line-item invoices beat vague bills every time.

- Proof of payment: Cancelled checks, card statements, wire confirmations, and receipts matter.

- Before-and-after photos: Show the damaged condition and the completed repair.

- Email confirmations: If the adjuster approved a scope revision, save it.

If you want a focused explanation of how depreciation gets applied and disputed, review depreciation on insurance claims.

Don't send a pile of receipts with no explanation. Send an organized demand that ties each invoice to a damaged building component the insurer already acknowledged or should have acknowledged.

A strong depreciation recovery submission usually does three things at once:

- It identifies the exact withheld amount.

- It shows the repair or replacement was completed.

- It closes off excuses about missing support.

Where carriers push back

Insurers commonly challenge the release of held-back money by saying the work was “different,” “upgraded,” “not comparable,” or “not yet complete.” Sometimes they approve replacement in theory but dispute the invoice when the bill arrives. Sometimes they accept the contractor's scope only after weeks of back-and-forth, hoping you give up.

If the depreciation is substantial or the repair is complex, get professional help early. Fighting over held-back money after the fact is harder than setting up the claim correctly from the beginning.

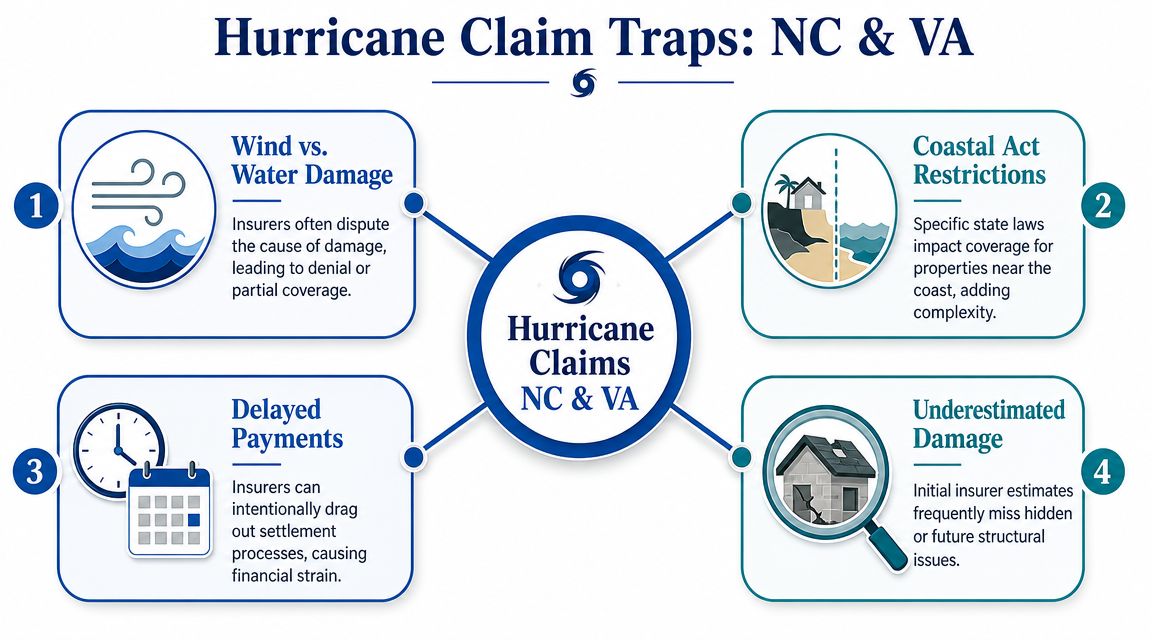

What Are the Biggest Replacement Cost Claim Traps for NC and VA Homeowners After a Hurricane?

Hurricane claims in North Carolina and Virginia are where replacement cost coverage gets stress-tested. Not in theory. In the world, after widespread damage, with roofers booked out, materials delayed, and every insurer trying to control claim severity at the same time.

Demand Surge Hits Fast After Major Storms

One of the biggest traps is assuming your dwelling limit or extension will automatically keep up with real rebuilding costs after a catastrophe. It may not.

In major-loss events, demand surge and labor/material inflation can push rebuilding costs beyond both the base dwelling limit and the typical 10% to 50% extended replacement cost cap, so policyholders may still face a significant out-of-pocket shortfall even when they “have replacement cost,” as described in this discussion of extended replacement cost limits after major losses.

That matters in coastal and inland storm zones alike. A limit that looked fine at renewal can become thin fast after a regional event.

There's another point people miss. Replacement cost for a dwelling is tied to rebuilding inputs, not market value. Insurers generally estimate it from local rebuild factors, often using a square-foot rebuild cost multiplied by home size, and the Coverage A limit may be based on that estimate, according to Progressive's explanation of home replacement cost calculations.

So when prices spike after a hurricane, you can run into trouble even if your home would sell for less or more than the insured amount. Claims are paid based on policy limits and rebuild obligations, not your opinion of market value.

Flood Is a Different Claim Entirely

Many hurricane losses can become problematic. Standard homeowners insurance and separate flood coverage are not the same thing.

If wind tears off roofing and rain enters through storm-created openings, that's one coverage analysis. If rising water, storm surge, or surface water enters the building, that's a different claim path. For flood losses, homeowners in North Carolina need to focus on NFIP flood coverage and the flood adjuster process, whether the adjuster is working through the National Flood Insurance Program or a Write Your Own carrier.

If your insurer keeps blending wind damage and flood damage into one blurry explanation, stop accepting verbal summaries. Demand a written position on causation and coverage.

Older homes and code issues

After a hurricane, older homes often need code-driven upgrades during repair. That can affect roofing assemblies, electrical work, framing details, openings, and other components. If your policy has ordinance or law coverage, that issue needs to be developed early. If it doesn't, you may be stuck funding required upgrades yourself.

Watch for these traps in storm claims:

- Cause disputes: The insurer blames excluded water when wind clearly contributed.

- Outdated pricing: Their estimate uses stale rates while contractors are pricing current conditions.

- Incomplete scope: Hidden wet materials, detached components, and code-triggered work get missed.

- Extension myths: The carrier talks as if extra limit language solves every rebuild problem. It doesn't.

Hurricane claims are won on details. Not slogans.

What Policy Loopholes Do Insurers Use to Reduce Your Replacement Cost Payout?

Replacement cost coverage sounds broad until the fine print shows up. Then the carrier starts pointing to conditions, definitions, and valuation methods that trim what should have been a straightforward payment.

Underinsurance and Coinsurance Penalties

A lot of policyholders think the hardest part is proving damage. Sometimes the harder part is proving they bought enough coverage in the first place.

Between 2000 and 2022, homeowners insurance expenditures grew at a 5.3% annualized rate, while median household income grew only 2.6% annualized. By 2022, the average homeowner spent 2.09% of income on homeowners insurance, up from 1.19% in 2001, according to the Insurance Research Council's homeowners expenditure data. That pressure leads people to carry limits that don't reflect current rebuild reality.

When limits fall behind, the insurer gets another opening. In some policies, underinsurance can trigger reduced recovery through coinsurance-style calculations or other limit-based restrictions. The math varies by form, but the outcome is the same. You paid for meaningful protection and discover after the loss that the policy's valuation setup punishes you for being short.

Functional Replacement and Matching Fights

Another tactic is the quiet downgrade from true replacement cost to functional replacement cost. That matters most with older homes, historic structures, and buildings with distinctive finishes.

Functional replacement doesn't always restore what was there. It can substitute modern materials that serve the same function but don't match the original character, quality, or appearance. For an old plaster wall, ornate trim, custom millwork, slate-style roofing component, or specialty siding, that can be a major loss disguised as a settlement method.

Then there's the matching fight. Here, the carrier agrees that some siding, shingles, flooring, or cabinets were damaged, but only pays to replace the exact affected area, leaving the property mismatched. The result can be a patched-looking home or business that no owner would have chosen before the loss.

Common insurer positions include:

- “Only the physically damaged portion is owed.”

- “The new material is close enough.”

- “Aesthetic mismatch isn't covered.”

- “Functional replacement satisfies the policy.”

Those arguments aren't the end of the story. Matching disputes turn on policy wording, state law, product availability, and the practical reality of repair. If a line is discontinued or the surrounding materials can't be blended, the insurer's “partial” solution may not restore the property.

Replacement cost coverage isn't just about whether something can be nailed, glued, or painted back in place. It's about whether the property is truly restored with like kind and quality.

The takeaway is simple. Don't read the declarations page and assume you know the claim outcome. The valuation wording and endorsements often decide whether the insurer owes a real restoration or a cosmetically compromised fix.

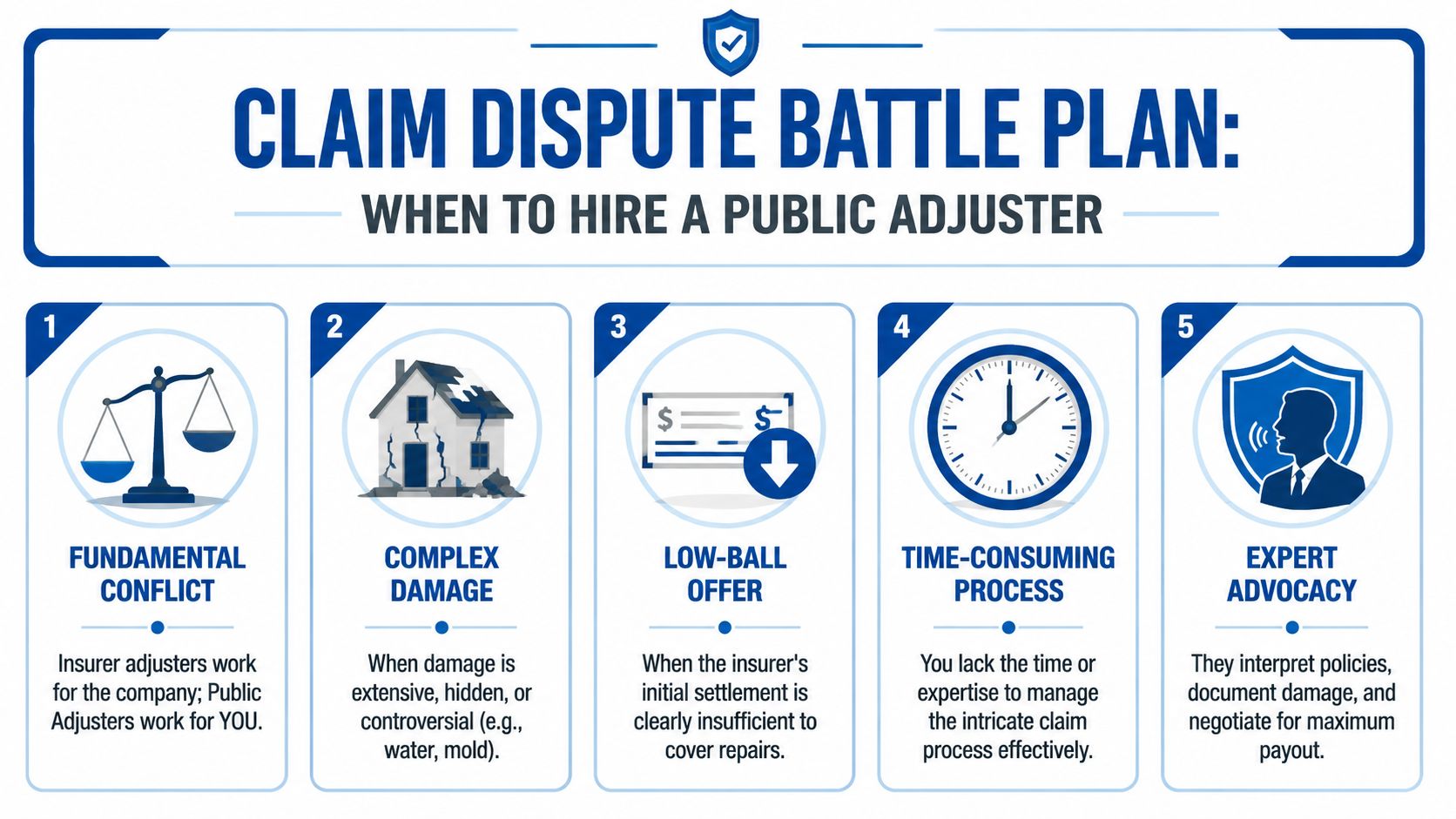

When Should You Hire a Public Adjuster to Fight a Replacement Cost Claim Dispute?

You open the estimate after a hurricane and see a number that does not cover the roof, does not cover interior tear-out, and does not release the depreciation the carrier held back. Then the adjuster tells you to send more documents and wait. That is not a routine claim anymore. It is a controlled underpayment.

Recognize the conflict early

The carrier's adjuster represents the carrier. Their file is built to limit payout, contain scope, and protect the insurer's position on replacement cost coverage. If you are arguing over missing line items, low unit pricing, code upgrades, overhead and profit, or held-back depreciation, you are in a valuation dispute.

A public adjuster represents the policyholder. The job is to inspect, document, estimate, apply policy language, and push back when the insurer tries to shrink the claim. If you want a clearer explanation of that role, read what a public adjuster does.

This matters even more in North Carolina and Virginia after major storms. Carriers know many owners are under pressure to clean up fast, hire contractors fast, and accept partial payments fast. That pressure leads to cheap settlements.

Hire help when these warning signs show up

Bring in a public adjuster when the claim starts showing any of these patterns:

- The insurer's estimate misses obvious damage. Wet insulation, detached accessories, hidden moisture, detached gutters, interior staining, and required tear-out often get cut or ignored.

- The payment does not match real repair pricing. If contractors are telling you the insurer's number is fantasy, believe the market, not the desk estimate.

- Recoverable depreciation is being used like a hostage payment. The carrier knows many policyholders will not understand the paperwork, deadlines, or proof needed to get that money released.

- The explanation keeps changing. First it is wear and tear. Then it is policy limits. Then it is incomplete documentation. That pattern usually means the file was never valued correctly in the first place.

- The loss is too technical to fight in your spare time. Water, fire, structural damage, code compliance, and large contents claims require documentation that holds up under scrutiny.

A good public adjuster does not bring slogans. They build pressure with evidence. Better photos. Better scope. Better pricing support. Better policy arguments. That is how low-ball replacement cost offers get forced upward.

For North Carolina and Virginia property owners, For The Public Adjusters, Inc. is one option for documenting, valuing, and negotiating property damage claims on the policyholder's side.

What you should do before you hire anyone

Get your file in order first. Save every estimate, invoice, receipt, email, text, photo, and adjuster report. If contents are part of the dispute, tighten your proof with a home inventory for insurance, because weak documentation gives the carrier another excuse to delay or deny part of the claim.

Then ask direct questions. Will the public adjuster inspect the full property? Will they prepare their own estimate? Will they address code items, depreciation, and supplements? Will they explain fee terms in writing? If the answers are vague, keep looking.

You hire a public adjuster when the insurer stops adjusting fairly and starts wearing you down. That is the moment to stop reacting and start building a case.

Don't Accept a Low-Ball Offer Get Expert Claim Help Now

You open the carrier's latest letter and see the same pattern again. A thin estimate, vague policy citations, held-back depreciation, and just enough payment to make you wonder whether fighting is worth the trouble. That is how underpaid replacement cost claims often happen, especially after major storms in North Carolina and Virginia.

Do not treat that offer like the end of the claim. Treat it like the insurer's opening position.

Start tightening the file today. Save every estimate, receipt, photo, invoice, email, text, inspection note, and contractor communication. If contents are part of the dispute, build cleaner proof with a home inventory for insurance. Weak documentation gives the carrier room to argue, delay, and shave dollars off items it should be paying.

Then get experienced claim help if the carrier keeps stalling, under-scoping, or hiding behind confusing replacement cost rules. Time matters. Deadlines matter more.

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us with questions.

For homeowners and business owners dealing with denied, delayed, or low-ball property claims, For The Public Adjusters, Inc. provides policyholder-side help with damage review, claim documentation, estimate analysis, and negotiation support for fire, water, wind, hail, hurricane, and other property losses in North Carolina and Virginia.

Finishing What the Insurer Left Incomplete: Recoverable Depreciation, Full

If the insured amount on a functional replacement cost policy is below 80% of the functional replacement cost at the time of loss, a coinsurance-style penalty kicks in and the carrier pays only a proportionate share of the loss — meaning you absorb part of the shortfall even if you complete repairs on time. This is one of the most overlooked traps in commercial and older residential policies.

The Paper Trail That Wins This Fight

To collect recoverable depreciation you need: (1) a signed contractor invoice or receipt showing work was actually performed, (2) photos of completed repairs tied to the scope of loss, (3) a written demand letter to the carrier citing the specific policy language on recoverable depreciation, and (4) proof the work was completed within the policy’s required timeframe — commonly 180 days from the date of loss, though some NC and VA policies allow up to 365 days or a reasonable extension if you request one in writing before the deadline passes.

Where Carriers Push Back

Insurers most commonly deny or reduce recoverable depreciation by arguing: the repairs were not “like kind and quality,” the work was done by the policyholder rather than a licensed contractor, or the receipts cover only materials and not labor. Counter each of these with itemized contractor invoices, contractor license numbers, and a line-by-line comparison to the original estimate scope.

Underinsurance and Coinsurance Penalties

Many NC and VA property owners discover after a loss that their policy limit was set years ago and no longer reflects construction costs. When coverage falls below the required percentage of the building’s replacement cost value — commonly 80% on homeowner policies and 90% on commercial policies — the insurer applies a coinsurance penalty. The formula: (amount of insurance carried ÷ amount required) × loss amount = what they pay. The remainder is your problem. Demand surge after a major hurricane makes this worse because local rebuild costs spike exactly when you need them most.

Functional Replacement Cost vs. Standard RCV: What’s the Difference?

Standard replacement cost coverage pays to restore damaged property with materials of like kind and quality at current market prices. Functional replacement cost coverage — common on older homes with plaster walls, ornate millwork, or discontinued materials — pays only for a functional modern equivalent, not an exact match. The distinction matters enormously if you own a pre-1980 home or a historic commercial building: the insurer may argue that drywall is a functional replacement for plaster, cutting your payout significantly. Review your declarations page to confirm which settlement basis applies.

Frequently Asked Questions

How long do I have to file for recoverable depreciation after my insurance claim?

Most replacement cost policies in North Carolina and Virginia require you to complete repairs and submit proof within 180 days of the date of loss. Some policies extend this to 365 days, and many carriers will grant a written extension if you request one before the original deadline — especially after a declared disaster when contractor availability is strained. Check your policy’s “Loss Settlement” or “Conditions” section for the exact language, then send any extension request by certified mail so you have a timestamped record.

What is the difference between functional replacement cost and standard replacement cost coverage?

Standard replacement cost pays to rebuild with materials of like kind and quality — if you had tongue-and-groove pine floors, you get tongue-and-groove pine floors priced at today’s rates. Functional replacement cost pays only for a modern equivalent that performs the same function — so the insurer could argue that engineered flooring satisfies the obligation. Functional replacement cost policies typically carry lower premiums but can leave you with a significant gap on older or custom properties.

Can the insurance company depreciate labor costs, not just materials?

Yes, and this is one of the most disputed issues in NC and VA property claims. Some carriers apply depreciation to embedded labor — the labor that cannot be separated from the material, such as the cost of installing a shingle that is 15 years old. North Carolina courts and the NC Department of Insurance have weighed in on this issue, but the outcome depends on your specific policy language. If your estimate shows labor depreciation, flag it and contest it in writing.

What can I do if the insurer’s estimate is too low to complete repairs?

Start by getting two to three independent contractor estimates that match the actual scope of damage — not a stripped-down version. Submit those estimates to the insurer in writing as a formal supplement request. If the carrier refuses to revise, your policy likely includes an appraisal clause that allows each side to hire an independent appraiser; if the two appraisers disagree, an umpire decides. A licensed public adjuster can manage this process, document the true scope of loss, and negotiate or invoke appraisal on your behalf without requiring you to hire an attorney.

Does replacement cost coverage apply to my personal property or just the building?

It depends on your policy. Many homeowner policies offer replacement cost coverage on the dwelling (Coverage A) but default to actual cash value for personal property (Coverage C) unless you specifically added a personal property replacement cost endorsement. Check both sections of your declarations page. If your furniture, appliances, and electronics were damaged in a fire or hurricane and your policy shows ACV for contents, you are receiving depreciated values — and an endorsement upgrade at renewal could prevent that shortfall on future claims.