A fire is one of the most devastating events a homeowner or business owner can experience. The emotional and financial toll is immense, and you turn to your insurance company, expecting them to honor the policy you've faithfully paid for. However, many policyholders are shocked when their insurer’s first instinct isn't to help, but to find ways to deny, delay, and underpay a legitimate claim.

Insurance providers are for-profit businesses, and their adjusters are often trained to protect the company's bottom line, which comes at your expense. Insurers like State Farm and Allstate have a long history of employing tactics like deliberate delays, complex policy interpretations, and unfairly low estimates to wear you down and pressure you into accepting less than you are owed. This isn't just a possibility; it's a common reality for many who have suffered a catastrophic loss. The fight you face against your own insurance company after the fire can feel just as damaging as the fire itself.

This guide is designed to level the playing field. We will expose the most common reasons insurance companies deny fire claims and provide the actionable strategies you need to fight back effectively. By understanding their playbook, from citing obscure policy exclusions to questioning the cause of the fire, you can prepare a stronger case and challenge an unjust denial. Knowing what to expect is the first and most critical step in ensuring you don't become another victim of an insurance company's profit-driven tactics. This article provides the blueprint for disputing your claim and securing the full and fair settlement you deserve.

1. Lack of Adequate Documentation and Proof of Loss

One of the most frequent and frustrating reasons insurance companies deny fire claims is a failure by the policyholder to provide sufficient documentation. After a devastating fire, your insurer isn't just going to take your word for what was lost. They require a mountain of evidence, and any gaps or inconsistencies can be used by carriers like State Farm or Allstate to justify a denial or a lowball settlement offer, shifting the burden entirely onto you during a traumatic time.

This requirement is not just a suggestion; it's a contractual obligation. Your policy contains a "Duties After a Loss" section that mandates you submit a sworn statement known as a Proof of Loss form, typically within 60 days. This formal document, along with a detailed inventory of every single destroyed item, is the foundation of your claim. Insurers often use this tight deadline to their advantage, knowing that a grieving family will struggle to meet such a demanding requirement, leading to an easy denial on a technicality.

How to Prevent a Documentation-Based Denial

Proactive preparation is your strongest defense against this common tactic. Don't wait for a disaster to happen.

- Create a Digital Inventory: Annually, walk through your home or business with a video camera, narrating what you're recording. Take still photos of high-value items, serial numbers, and collections.

- Cloud Storage is Key: Store these videos, photos, and digital copies of receipts, appraisals, and warranties in a secure cloud service like Google Drive or Dropbox. This ensures your proof isn't lost in the very fire you need to document.

- Protect Physical Documents: For original deeds, titles, and certificates of authenticity, use a fireproof safe or an off-site bank safe deposit box.

How to Fight a Denial for Lack of Proof

If you're facing a denial because the insurance company claims your documentation is inadequate, don't give up. The insurer’s adjuster works to protect their employer’s financial interests, not yours. This is a critical moment to seek professional help. A public adjuster can be instrumental in meticulously recreating your inventory, valuing your losses accurately, and formally presenting the claim in a way the insurance company cannot easily dismiss. They understand the complex requirements of a Proof of Loss and can ensure your submission is comprehensive and timely, forcing the insurer to negotiate in good faith. A skilled public adjuster recently helped a family in Virginia whose claim was denied for "insufficient proof" after a fire. By using fragments of receipts, online purchase histories, and family photos, the public adjuster reconstructed a 50-page inventory list, forcing the carrier to reverse their denial and pay the claim in full.

2. Policy Exclusions and Coverage Limitations

One of the most insidious reasons insurance companies deny fire claims isn't an outright rejection, but death by a thousand cuts through policy exclusions and coverage limitations. Policyholders often believe their coverage is comprehensive, only to discover after a fire that the fine print contains specific conditions, hazards, and property types that are explicitly not covered. Insurers like Nationwide or USAA will meticulously comb through your policy's language to find any applicable exclusion to justify denying your claim or drastically reducing your payout.

This isn't an accident; it's by design. Your policy is a complex legal contract filled with carefully worded exclusions for things like "neglect" or damages arising from undisclosed business operations. It also contains sub-limits, which are caps on coverage for specific categories like jewelry, firearms, or electronics. For example, you might have $500,000 in personal property coverage, but the policy may only pay a maximum of $2,500 for all your lost jewelry, a detail adjusters are quick to enforce.

How to Prevent a Denial Based on Exclusions

Understanding your policy before a loss is the only effective defense against this tactic. Don't rely on the agent's summary; you must review the document yourself.

- Request a "Specimen" Policy: Before you buy or renew, ask for a complete copy of the policy document. Read the "Exclusions" and "Conditions" sections carefully.

- Schedule High-Value Items: Anything of significant value, like art, antiques, or high-end electronics, should be appraised and added to the policy as a "scheduled personal property endorsement." This provides specific, guaranteed coverage.

- Choose Replacement Cost Value (RCV): Default "Actual Cash Value" (ACV) policies allow insurers to deduct depreciation, drastically lowering your payout. Insist on RCV coverage to be reimbursed for the cost of buying new items.

- Disclose Everything: If you run a small business from home, have a tenant, or have made significant renovations, inform your insurer. Hiding these details can trigger an exclusion and void your coverage entirely.

How to Fight a Denial Due to an Exclusion

If your insurer denies your fire claim based on a policy exclusion or a coverage limit, do not accept their interpretation as final. The language in these policies can be ambiguous and is often subject to legal interpretation that may favor you, the policyholder. This is a clear signal that you need an expert on your side. In the case of Vantage View, Inc. v. QBE Ins. Corp., a federal court ruled that the insurance company could not use a broad "faulty workmanship" exclusion to deny a massive claim, finding the policy language ambiguous and interpreting it in favor of the policyholder. A public adjuster can perform a detailed policy review, cite relevant case law, challenge the insurer’s application of an exclusion, and fight to maximize your recovery under the existing terms, preventing the insurance company from using the fine print against you.

3. Non-Disclosure or Misrepresentation on the Application

An insurance policy is a contract built on good faith, but carriers will use any initial inaccuracy to their advantage after a loss. One of the most severe reasons insurance companies deny fire claims is "material misrepresentation," which occurs when you provide false, incomplete, or misleading information on your insurance application. Insurers like Allstate and State Farm will meticulously review your original application after a fire, searching for any discrepancy they can use to declare the entire policy void from the start, leaving you with no coverage at all.

This isn't just about outright lies; even an innocent omission can be grounds for denial. The insurance company will argue that had they known the "true" facts, such as the presence of old aluminum wiring, a previous fire claim ten years ago, or that the property was vacant instead of owner-occupied, they would have charged a higher premium or refused to issue the policy altogether. They use this as legal justification to rescind the contract, return your premiums, and walk away from their obligation to cover your catastrophic fire damage.

How to Prevent a Misrepresentation-Based Denial

Honesty and thoroughness during the application process are your only shields against this aggressive tactic. Treat the application not as a formality but as a foundational legal document.

- Be Meticulously Honest: Disclose everything the application asks for, including prior claims, known property defects (like a deteriorating roof), and business activities conducted on the premises. If you are unsure about a question, ask for clarification in writing.

- Update Your Insurer: Life changes, and so do property risks. If you undertake a major renovation, leave the property vacant for an extended period, or get a certain breed of dog, you must inform your insurer. These changes materially affect their risk assessment.

- Keep Your Paperwork: Always retain a complete copy of your insurance application. This document is crucial evidence if the insurer later claims you misrepresented information that you, in fact, disclosed accurately.

How to Fight a Denial for Misrepresentation

A denial based on misrepresentation or non-disclosure is an insurer's attempt to erase their contractual duty. They are betting you won't fight back. This is not a simple disagreement over the value of your loss; it's a challenge to the validity of your entire policy.

This is a scenario where professional intervention is non-negotiable. A public adjuster can analyze the insurer's allegations of "materiality," arguing that the undisclosed information was not significant enough to have altered the underwriting decision. They will scrutinize the original application against the insurer's claims, gather evidence to prove your intent was not to deceive, and build a powerful counter-argument to force the carrier to honor the policy. This action is critical to prevent the insurance company from using a technicality to abandon you after a disaster.

4. Lack of Property Maintenance and Negligence

Insurance companies frequently deny fire claims by arguing the policyholder was negligent, effectively blaming you for the fire. Your insurance policy is a contract that assumes you will take reasonable steps to maintain your property and prevent foreseeable disasters. When an insurer like Allstate or State Farm can point to deferred maintenance or a known hazard as the fire's origin, they will seize the opportunity to deny your claim, shifting financial responsibility from their bottom line directly onto your shoulders.

This tactic often appears after fires caused by faulty wiring that was never updated, a chimney that hadn't been cleaned in years, or even an appliance that was subject to a safety recall. The insurer will investigate the cause and origin of the fire, and if their findings suggest your inaction contributed to the loss, they will argue you violated the terms of your policy. They essentially claim that because the hazard was preventable through routine upkeep, they are not obligated to cover the resulting damage, leaving you to face the catastrophic loss alone.

How to Prevent a Negligence-Based Denial

The most effective way to combat a potential negligence denial is to meticulously document your property's upkeep. This creates a powerful record that counters the insurer’s attempts to portray you as careless.

- Keep Detailed Maintenance Logs: Keep a file with receipts and invoices for all major system maintenance, including your HVAC, electrical, and plumbing systems. Note the dates of service and what was done.

- Address Known Hazards Immediately: If a home inspection or a contractor points out a defect, such as outdated wiring or a roofing issue, have it professionally repaired and keep the documentation.

- Clean and Inspect Annually: Schedule annual professional cleanings for chimneys and dryer vents. To understand how easily a lack of upkeep can lead to a fire, review these common causes of dryer fires and prevention tips.

- Monitor Appliance Recalls: Register your major appliances with the manufacturer to receive notifications for safety recalls and address them promptly.

How to Fight a Denial for Negligence

If your insurance carrier denies your fire claim based on alleged negligence or poor maintenance, do not accept their decision as final. The insurer’s investigation is designed to find reasons to avoid paying, not to find the truth. This is a clear signal that you need an expert advocate. A public adjuster can challenge the insurance company’s biased findings, hire independent cause-and-origin experts to conduct a fair investigation, and use your maintenance records to prove you fulfilled your duties as a homeowner. They can build a powerful counter-argument that forces the insurer to abandon their unfounded denial and pay the full value of your claim.

5. Disputes Over Causation and Fire Origin

One of the most complex and contentious reasons insurance companies deny fire claims involves disputes over how and where the fire started. Following a fire, your insurer will dispatch their own investigators to determine the "origin and cause." If their handpicked expert concludes the fire was a result of something excluded in your policy, like an intentional act (arson), it provides a powerful, ready-made justification for an outright denial, leaving you to fight a serious allegation while grappling with a catastrophic loss.

This scenario creates an immediate conflict of interest. The investigator is paid by the insurance company, and their findings can save their employer millions. For example, they might interpret evidence of an accelerant as proof of arson, when it could be residue from household cleaning supplies. They may also classify a fire from an overloaded electrical panel as intentional tampering rather than a covered malfunction, shifting blame and financial responsibility squarely onto you.

How to Prevent a Causation-Based Denial

Protecting yourself requires challenging the insurer’s narrative from the very beginning. You cannot afford to let their investigation be the only version of the story.

- Preserve the Scene: As much as safely possible, do not disturb the fire scene. Do not move debris or discard potential evidence until it has been professionally documented by your own expert.

- Document Everything: Immediately write down a detailed timeline of events leading up to the fire: where you were, who was present, and any unusual circumstances you observed.

- Request All Reports: Formally request copies of every report, photo, and lab result from your insurer's investigation. Scrutinize these documents for any inconsistencies or biased conclusions.

How to Fight a Denial Over Fire Origin

If your insurer denies your claim based on their investigator's findings, you are facing an uphill battle that requires specialized expertise. This is not a situation where you can simply argue with the adjuster. Insurers like Allstate and State Farm rely on their expert reports to shut down claims, and you must counter their "evidence" with stronger evidence of your own.

This is precisely when engaging a public adjuster is critical. They can immediately hire an independent, certified fire investigator (CFI) to conduct a separate, unbiased analysis of the scene. This independent expert will examine the evidence, challenge the insurer's conclusions, and provide a competing report that can dismantle the denial. A public adjuster levels the playing field, ensuring the cause of the fire is determined by objective science, not by the insurance company’s financial interests.

6. Lapsed Coverage or Policy Cancellation Issues

One of the most clear-cut reasons insurance companies deny fire claims is a gap in coverage. If your policy has lapsed, been cancelled, or was not properly renewed, any fire damage that occurs during that gap will not be covered. Insurers like Nationwide or USAA will seize on this issue, arguing that no contract was in force at the time of loss, leaving you to bear the entire financial burden of recovery alone.

This is not always a simple case of a missed payment. Ambiguous cancellation notices, grace periods that are not honored, premium payments lost in the mail, or even a simple administrative error like an expired credit card on an auto-pay account can create a lapse. Insurers have also been known to retroactively cancel policies for alleged non-disclosure after a fire occurs, a tactic designed to escape paying a legitimate claim by arguing the policy was never valid to begin with.

How to Prevent a Coverage-Lapse Denial

Maintaining continuous, uninterrupted coverage is your responsibility, but you can take steps to protect yourself from errors and bad-faith practices.

- Automate and Verify: Set up automatic payments for your premiums, but also set a calendar reminder a few days before the due date to confirm the payment was successfully processed.

- Keep Meticulous Records: Retain digital and physical copies of all payment confirmations, renewal notices, and any written communication from your insurer or agent. This documentation is your best defense against a wrongful cancellation claim.

- Communicate in Writing: When renewing or making changes to your policy, follow up with an email to your agent to create a written record of the conversation and request confirmation that your policy is active.

How to Fight a Denial for a Policy Lapse

A denial based on a lapsed policy can feel like a final judgment, but it may be contestable. The insurer’s adjuster has a duty to find any reason to deny the claim, and they will not help you prove their company made a mistake. If you believe your policy was cancelled in error or without proper legal notice, you must act quickly to challenge the decision.

This is a complex situation where a public adjuster’s expertise is invaluable. They can conduct a thorough review of your payment history, policy documents, and all correspondence with the insurer to identify any procedural errors or wrongful actions. By meticulously reconstructing the timeline and presenting evidence that you made a good-faith effort to maintain coverage, a public adjuster can effectively challenge an improper denial and force the insurance company to re-evaluate its position and honor its contractual obligations.

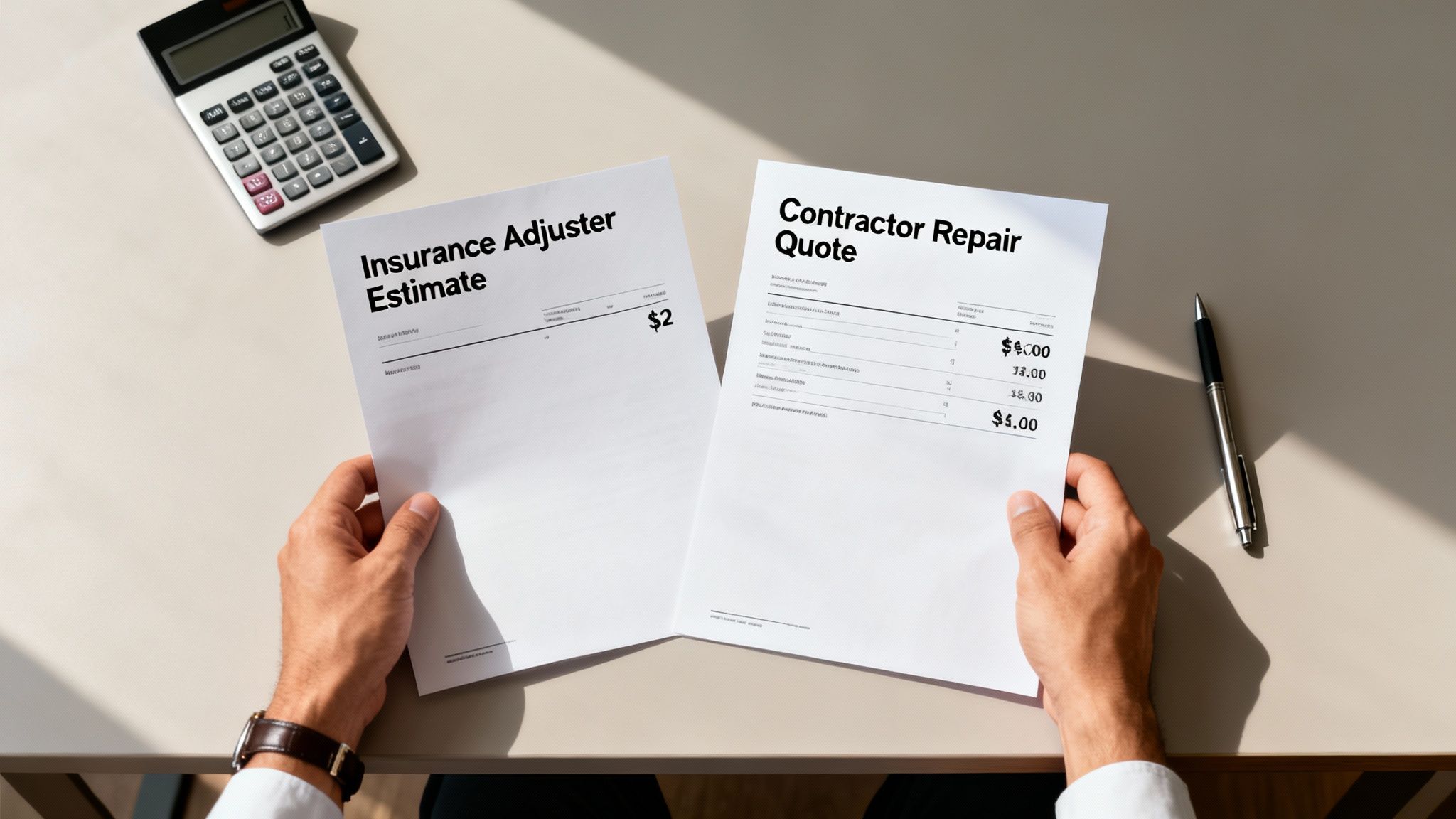

7. Inadequate or Inflated Damage Assessments

One of the most insidious reasons insurance companies deny fire claims, or more commonly, drastically underpay them, is through disputes over the valuation and scope of the loss. Your insurer will send their own adjuster, who works for them, not you, to create an estimate. This estimate often undervalues the cost of repairs, omits critical damage, or applies excessive depreciation, leaving you with a settlement that falls far short of what you need to rebuild. Carriers like Allstate and State Farm frequently use their own pricing software and "market rates" that don't reflect the true, local cost of labor and materials, putting the financial burden of their lowball offer directly on you.

This tactic is a core part of their business model. For example, their adjuster might estimate a complete home rebuild at $200,000, while your licensed contractor provides a detailed quote for $350,000. The insurer may refuse to budge, citing their internal data. They may also conveniently "forget" to include the cost of treating pervasive smoke damage in your furniture and clothing or deny claims for water damage from firefighting efforts, arguing it's a separate, uncovered peril. These are not honest mistakes; they are calculated strategies designed to minimize their payout.

How to Prevent a Valuation-Based Denial

You must build your own independent case for the true value of your loss to combat the insurer’s low estimate. Never accept their first offer without performing your own due diligence.

- Get Independent Quotes: Before agreeing to anything, obtain at least two detailed, line-item estimates from reputable, licensed, and insured local contractors.

- Document Everything: Photograph and list every single damaged item. Note smoke and water damage specifically, as adjusters often overlook this secondary damage.

- Challenge Depreciation: If the insurer applies depreciation to items like kitchen cabinets or flooring, ask for their written justification and calculation. You can counter with evidence of your home's excellent pre-fire condition and quality of materials.

How to Fight a Claim Underpaid Due to a Low Assessment

When an insurer presents a lowball offer, it is a clear sign that their priority is protecting their profits. This is not a negotiation between equals; they hold the power until you bring in an expert of your own. A public adjuster is your advocate, equipped with the same tools and expertise as the insurance company. They will conduct their own forensic evaluation of the damage, create a competing estimate using industry-standard software, and document every detail of your loss. By preparing a comprehensive and professionally packaged fire damage claim, a public adjuster forces the carrier to address the true scope of the damage and negotiate a fair settlement based on facts, not on their attempt to save money.

8. Procedural Compliance Failures and Bad Faith Practices

Insurance companies often use your policy's complex procedural rules as a weapon to deny legitimate fire claims. A simple misstep, like reporting the claim a few days late or missing a tight deadline, can be used by carriers like Allstate and State Farm as a technicality to reject your entire claim. This is often where procedural failures bleed into insurer bad faith, as a carrier may enforce a minor rule with unreasonable strictness, not to ensure fairness, but to protect its own profits at your expense.

This is a twofold problem: you must perfectly navigate a maze of contractual obligations while you are at your most vulnerable, and the insurer may be actively looking for a reason to trip you up. The "Duties After a Loss" section of your policy isn't just a guide; it's a series of potential traps. Insurers know that a homeowner reeling from a fire is unlikely to meet every single deadline and requirement, making procedural denials one of the easiest reasons insurance companies deny fire claims. They may also engage in bad faith tactics like unreasonable delays or purposefully misinterpreting policy language to support their denial.

How to Prevent a Denial Based on Procedural Errors or Bad Faith

Meticulous organization and immediate action are your best defenses against these tactics. You must show the insurer that you are proactively and diligently meeting all your obligations.

- Report Immediately: Notify your insurance company of the fire as soon as it is safe to do so, ideally within 24 hours. Get a claim number and document the name of the person you spoke with, plus the date and time.

- Document Everything: Keep a detailed log of every interaction with your insurer. Note dates, times, names, and a summary of every phone call and email. This creates a paper trail that can be crucial later.

- Meet Every Deadline: Pay close attention to deadlines for submitting forms like the Proof of Loss. If you cannot meet a deadline, request an extension in writing and get the insurer's approval in writing.

- Cooperate Reasonably: Allow the insurer’s adjusters and investigators to access the property, but you have the right to be present or have a representative there. Do not sign any documents you don't fully understand.

How to Fight a Denial for Procedural Reasons

If your claim is denied based on a procedural technicality or you suspect the insurer is acting in bad faith, it's time to fight back. An insurer's refusal to investigate, their endless delays, or their reliance on a minor missed deadline to deny a catastrophic loss are all red flags. This is no longer a simple claims issue; it's a potential legal battle.

A public adjuster is your first line of defense. They can analyze the insurer's denial letter, review your policy and communications log, and determine if the denial was justified or a pretext. They understand the procedural games that carriers play and can build a comprehensive counter-argument, often forcing the insurer to reverse its decision and handle the claim in good faith. If the insurer continues to act improperly, a public adjuster can provide the critical documentation needed to escalate the matter with an attorney or your state's insurance commissioner.

8-Point Comparison: Fire Claim Denials

| Item | ???? Complexity | ⚡ Resource requirements | ???? Expected outcomes | ???? Ideal use cases | ⭐ Key advantages |

|---|---|---|---|---|---|

| Lack of Adequate Documentation and Proof of Loss | Moderate — time‑sensitive record gathering; multiple forms required | Moderate — inventories, photos, receipts, possible public adjuster | Higher chance of full settlement if documentation complete; otherwise partial/denial | Claims with many personal items or unclear ownership | Strengthens claim credibility; supports accurate valuation |

| Policy Exclusions and Coverage Limitations | High — complex policy language and sublimits | Low–Moderate — policy review, possible endorsements or appraisal | Clarifies what is/aren’t covered; may limit recovery without endorsements | Policy review, pre‑loss planning, disputes over limits | Defines coverage boundaries; prevents unexpected gaps |

| Non-Disclosure or Misrepresentation on the Application | High — legal/materiality issues; potential rescission | Moderate — application records, CLUE reports, possible legal support | Risk of rescission or denial if material misstatement proven; may be contestable | Disputes where insurer alleges inaccurate application information | Ensures underwriting integrity; clear basis for insurer action |

| Lack of Property Maintenance and Negligence | Moderate — causation often disputed and fact‑specific | Moderate — maintenance records, repair receipts, expert testimony | Possible denial or reduced recovery if negligence shown; can be rebutted | Older homes, deferred repairs, claims citing maintenance failures | Incentivizes loss prevention; insurers may accept with proof of upkeep |

| Disputes Over Causation and Fire Origin | Very high — technical fire science, competing experts | High — independent investigators, lab tests, expert reports | Outcome depends on expert evidence; conflicting opinions common | Cases alleging arson/intention or unclear origin of fire | Objective determination when resolved; can overturn exclusion claims |

| Lapsed Coverage or Policy Cancellation Issues | Low–Moderate — administrative but decisive | Low — payment records, renewal notices, agent correspondence | Denial likely if gap exists; sometimes overturnable with proof of payment | Payment processing disputes, missed renewals, grace period issues | Clear resolution when documentary proof exists; fixable administratively |

| Inadequate or Inflated Damage Assessments | Moderate — valuation disputes require line‑item review | Moderate–High — contractor bids, appraisals, public adjuster expertise | Often underpayment initially; potential for increased settlement when challenged | Major rebuilds, disputed repair vs. replacement costs | Can materially increase recovery by challenging low estimates |

| Procedural Compliance Failures and Bad Faith Practices | Moderate–High — deadlines and legal standards involved | High — thorough documentation, communication logs, legal counsel | Technical denials common; bad faith can yield legal remedies | Delays, ignored evidence, unreasonable insurer conduct | Provides legal recourse and protection against improper denials |

You Don't Have to Fight Them Alone: Take Control of Your Fire Claim

Navigating the aftermath of a fire is a harrowing experience, but receiving a denial letter from your insurance company can feel like a second disaster. As we've detailed, the reasons insurance companies deny fire claims are numerous and often complex, ranging from allegations of negligence and misrepresentation to disputes over the fire's origin and the true value of your losses. Your insurer, whether it's State Farm, Allstate, or another major carrier, has a team of adjusters, investigators, and legal experts whose primary role is to protect the company's financial interests, not necessarily yours. They are counting on you to feel overwhelmed, exhausted, and ultimately, to accept their decision without a fight.

This is precisely where their strategy succeeds: policyholders often lack the specific expertise, emotional energy, and time required to mount a successful appeal. The denial letter, filled with technical jargon and policy citations, is designed to be intimidating. It is a calculated move to discourage you from questioning their authority. But it is crucial to remember that a denial is not the final word; it is the opening move in a negotiation you may not have realized you were in.

From Denial to Determined Action

The key takeaway from this guide is that you have the power to challenge an unfair denial. The insurance company's initial assessment is just that: an initial assessment, often biased in their favor. To effectively counter it, you must shift from a reactive position to a proactive one. This involves a strategic and methodical approach that mirrors the very process the insurer used to deny you.

- Re-examine Your Documentation: Compare their denial reason against the proof of loss, inventory lists, and expert reports you submitted. Identify the specific points of contention.

- Scrutinize Your Policy: Don't just take their interpretation of an exclusion or limitation at face value. Policy language can be ambiguous, and courts have often sided with policyholders when interpretations are unclear.

- Demand Their Evidence: You have the right to see the reports from their "independent" investigators, engineers, and cause-and-origin specialists. Look for inconsistencies, biases, or incomplete analyses.

- Document Everything: From this point forward, maintain a meticulous record of every phone call, email, and letter exchanged with the insurer. This documentation is vital for demonstrating bad faith practices if their conduct becomes unreasonable.

Understanding the broader landscape of dealing with carriers can be incredibly beneficial. For homeowners seeking more general guidance on this process, resources detailing professional assistance with insurance claims can provide a foundational understanding of what to expect.

Leveling the Playing Field with Professional Advocacy

The most significant step you can take is to recognize when you are outmatched. Insurance companies have a deep well of resources. Trying to fight them alone is like stepping into a courtroom without a lawyer. A licensed public adjuster is your dedicated advocate, an expert who works exclusively for you, the policyholder. They understand the tactics insurers use to underpay or deny claims and possess the IICRC certifications and claims expertise needed to dismantle weak arguments.

A public adjuster will conduct an independent investigation, hire their own trusted experts, meticulously document the full scope of your damages, and negotiate directly with the insurance company from a position of strength. They translate the complexities of your policy and present your claim in the language the insurer cannot ignore. This professional intervention transforms the power dynamic, forcing the carrier to justify its position against a knowledgeable peer and often leading to a reversed denial or a significantly increased settlement. You paid your premiums faithfully; now is the time to ensure you receive the protection you paid for.

Don't let an unfair denial dictate your future. The team at For The Public Adjusters, Inc. specializes in fighting for North Carolina and Virginia policyholders who have been wronged by their insurance companies. We dissect the reasons insurance companies deny fire claims and build an undeniable case to secure the maximum settlement you are rightfully owed. Visit us online at For The Public Adjusters, Inc. for a no-cost claim review and learn how we can help you take back control.