A public adjuster is your state-licensed advocate, an insurance professional who fights exclusively for you—the policyholder—when your property gets damaged. They are your expert negotiator against an insurance company that denies, delays, or tries to underpay what you are rightfully owed for damages to your home or business.

Why You Need an Advocate Against Your Insurance Company

Getting a denied or lowball claim offer from your insurance company feels like a betrayal. You’ve paid your premiums on time for years, believing they’d have your back. But when disaster actually hits, the big insurance carriers like State Farm or Allstate suddenly seem more focused on their profits than on helping you recover.

Let’s be clear: this isn't just a bad feeling; it's their business model. These massive corporations have armies of adjusters, lawyers, and so-called "experts" whose job is to pay out as little as possible. They use confusing policy jargon, stall tactics, and insulting settlement offers to wear you down until you finally give up and accept a fraction of what your claim is worth. For a homeowner or business owner already overwhelmed by a catastrophe, it’s a David-and-Goliath fight.

Leveling the Playing Field with a Public Adjuster

This is where you hire a public adjuster and draw a line in the sand. Think of them as your personal claims expert, brought in to even the odds. Their job isn’t just about filling out paperwork; it’s about launching a strategic, evidence-backed fight against the insurer’s games. They document every last detail of your loss, find the language in your own policy that works to your advantage, and negotiate aggressively to get you the full settlement you’re owed.

A public adjuster is the only claims adjuster who works for you, the policyholder. Their loyalty is to your financial recovery, not the insurance company’s bottom line.

Success Story: After Hurricane Ian, a Florida homeowner's claim was lowballed at $50,000 by their carrier, who claimed most of the damage was from uncovered flooding. The homeowner hired a public adjuster who proved the majority of the destruction was from wind-driven rain, a covered peril. By meticulously documenting the roof's failure and the resulting interior damage, the public adjuster successfully reopened the claim and secured a final settlement of over $400,000, enabling the family to rebuild their home. You can find more details about what a public adjuster does at insuranceclaimrecoverysupport.com.

Hiring a public adjuster sends a clear signal to your insurance company: you won’t be bullied, and you won’t settle for less. It’s the most powerful move you can make to turn a nightmare fight into a successful recovery.

Understanding Who Each Adjuster Really Works For

When your home or business is damaged, an insurance adjuster will show up pretty quickly. But here's the critical part they won't tell you: not all adjusters are the same, and most of them don't work for you.

Let’s get one thing straight: the claims process is a battlefield with three types of adjusters, and figuring out who they really work for tells you everything you need to know.

The Insurance Company’s Team

The first two types—staff adjusters and independent adjusters—are both paid to protect the insurance company's bottom line, not yours.

A staff adjuster is a direct employee of your insurance carrier, whether it's State Farm, Allstate, or another big name. Their job, their paycheck, and their promotions all hinge on one thing: how much money they can save their employer. That usually means minimizing your claim payout.

Then you have the independent adjuster. These are freelancers the insurance company hires when they’re swamped, like after a hurricane rips through town. Don't let the "independent" title fool you. They get their marching orders—and their checks—directly from your insurer. Their goal is the same: close your claim fast and cheap.

The Policyholder’s Exclusive Ally

This is where a public adjuster changes the entire game. A public adjuster is the only type of adjuster licensed by the state to represent you, the policyholder. Period. We have zero connection to the insurance company.

Our only job, legally and ethically, is to fight for your best interests. We dive into your policy, document every ounce of damage, and build an airtight case to get you the maximum possible settlement you're entitled to.

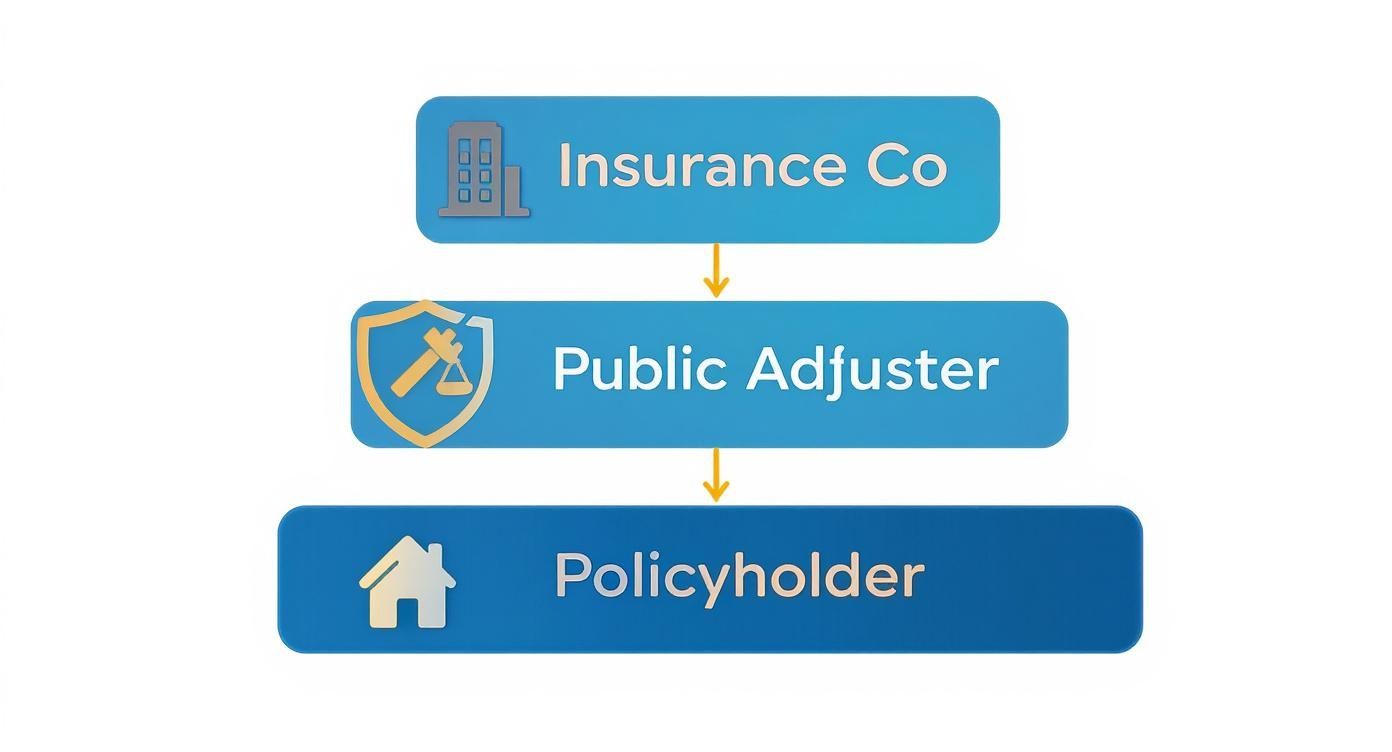

This diagram cuts through the noise and shows you exactly how a public adjuster levels the playing field.

As you can see, we stand between you and the insurance company, acting as your expert advocate and shield.

To put it bluntly, the adjuster your insurance company sends is trained to find policy loopholes and reasons to pay you less. We are trained to find every bit of coverage you're owed and force them to honor it. You can get an even more detailed breakdown in our guide on the differences between a public adjuster vs an insurance adjuster.

Who Does Your Adjuster Really Work For?

When you’re in the middle of a claim, it can be tough to keep track of who is on your side. This table makes it crystal clear.

| Adjuster Type | Who They Work For | Primary Goal | Who Pays Them |

|---|---|---|---|

| Staff Adjuster | The Insurance Company | To minimize the claim payout and protect the company's profits. | The Insurance Company |

| Independent Adjuster | The Insurance Company | To process claims according to the insurer's guidelines, often leading to lower settlements. | The Insurance Company |

| Public Adjuster | You, The Policyholder | To maximize your claim settlement and ensure a fair recovery. | You (from the settlement) |

This is the fundamental conflict of interest that forces homeowners and business owners to hire their own representation. While the company adjuster is busy looking for excuses to deny or underpay your claim, your public adjuster is building an undeniable case to make them pay what’s fair.

How a Public adjuster Dismantles an Unfair Denial

Let's get one thing straight: when your insurance company sends you a denial letter, it's not a mistake. It's a calculated business decision. Carriers like Allstate and State Farm are betting you'll feel defeated, give up, and eat the cost of the damages yourself.

But for a seasoned public adjuster, that denial letter isn't the end. It's the starting gun.

An unfair denial is almost never about the reality of your loss. It’s about the carrier's self-serving interpretation of your policy, a lazy inspection by their adjuster, and their hope that you're too intimidated to challenge them. Our first job is to tear that flimsy reasoning apart, piece by piece.

The Forensic Re-Evaluation Process

The moment we take on a denied claim, we start our own investigation from scratch. We treat your property like a fresh crime scene and completely ignore the company adjuster's report, because frankly, it’s often rushed, biased, and incomplete.

We then launch a meticulous, forensic re-evaluation of the damage. This isn't a 15-minute walkthrough. A real public adjuster will:

- Hunt for Overlooked Damage: We use professional-grade tools like thermal imaging cameras and moisture meters to uncover the hidden water damage creeping behind your walls or the soot contamination inside your HVAC system that their adjuster "somehow" missed.

- Document Everything: We take hundreds—sometimes thousands—of high-resolution photos and detailed videos. This creates an undeniable visual record of the loss that a claims manager in a cubicle hundreds of miles away can't ignore.

- Call in the Experts: If the insurer is trying to get away with a bogus engineering report, we bring in our own structural engineers, industrial hygienists, or master roofers whose expert opinions will shred their weak conclusions.

This ground-up re-inspection is how we build a new, rock-solid evidence package that your insurer can't just brush aside.

Weaponizing Your Own Insurance Policy

Insurance policies are deliberately written to be confusing. They're dense legal contracts designed to give the insurer loopholes. The company adjuster is trained to cherry-pick specific clauses and exclusions to justify their denial.

A public adjuster flips that strategy on its head. We know how to find the exact language, endorsements, and provisions in your policy that actually compel them to provide coverage.

We re-frame the entire narrative of the loss using the policy's own terms, showing the insurance company precisely how their denial violates the very contract they wrote.

A public adjuster doesn't just argue facts; we argue from a position of authority on policy language. We force the insurance company to defend its denial against its own words.

This deep policy analysis is the game-changer. It shifts the fight from your word against theirs to a battle over contractual obligation—a fight they are far less comfortable having with an expert. It's also how we systematically defeat the common Top Insurance Claim Denial Reasons they rely on.

Building an Undeniable Evidence Package

Armed with fresh evidence and a powerful policy-based argument, we build a new, comprehensive claim submission. This isn't some polite email asking them to reconsider. It's a formal, professional demand package that includes:

- A detailed, line-item-by-line-item estimate built with Xactimate, the same software they use. The difference is, our estimate includes everything required to bring your property back to its pre-loss condition, using accurate local labor and material costs.

- A formal "Sworn Statement in Proof of Loss," a critical legal document that officially states the full value of your claim. Knowing how to prepare and submit this document is absolutely vital, which is why a Proof of Loss is such an important tool in claim disputes.

- All supporting documents: expert reports, photo logs, videos, and receipts, all organized to dismantle their original denial point by point.

This isn't a negotiation anymore. It's a confrontation. We force them to reopen the file and deal with a licensed professional who has overwhelming evidence on their side. Suddenly, their initial denial looks weak, unsupported, and dangerously close to an act of bad faith. This is how we turn their "no" into the settlement you're owed.

The Claim Battles We Win for Policyholders

A public adjuster's real value isn't just in handling paperwork; it's in winning the fights that policyholders can't win alone. We step in when the stakes are highest—after a devastating loss where your insurance carrier is looking for any excuse to underpay or deny your claim.

Let’s be clear: when a catastrophe hits, insurers know you're overwhelmed, confused, and exhausted. They bank on that chaos to push through a quick, lowball settlement before you know what hit you. Our job is to level the playing field and force them to pay every single dollar they owe.

The Aftermath of a Devastating Fire

A fire claim is one of the most brutal, complex battles you can face. The damage you see—the charred walls and burned structure—is just the tip of the iceberg. Insurers love to focus only on what’s obviously burned, conveniently ignoring the far more expensive secondary damage.

A seasoned public adjuster knows their game and documents everything they try to hide:

- Widespread Smoke and Soot Damage: Smoke is acidic. It doesn't just stain walls; it seeps into drywall, insulation, and your entire HVAC system, contaminating everything it touches. We prove this hidden damage requires total remediation or replacement, not just a coat of paint.

- Structural Integrity Issues: The intense heat from a fire can weaken steel beams, compromise concrete, and warp your building's frame, even if it doesn't look burned. We bring in engineers to expose these hidden dangers that the company adjuster "missed."

- Business Interruption Costs: For a business, the fire is just the beginning of the financial nightmare. We meticulously calculate and fight for every penny of lost income, ongoing operational costs, and temporary relocation expenses while you're shut down.

Case Study in Action: A North Carolina business was gutted by a fire. Their insurer, State Farm, came in with a ridiculously low offer of $200,000, only covering the most obvious repairs. The owner hired us. We conducted a forensic deep-dive, documenting massive smoke damage, proving the need for code upgrades, and calculating six months of lost business income. The final settlement we negotiated was over $750,000—a 275% increase from their initial offer.

Catastrophic Water and Storm Damage

Major storms are a one-two punch of wind and water, and insurers use that chaos to their advantage. They love to play games, arguing over whether the damage was caused by wind-driven rain (which is often covered) or rising floodwaters (which usually isn't). It's a classic tactic to deny a claim.

We shut that argument down. A public adjuster pinpoints the exact cause and documents the full extent of the destruction, from the initial roof breach caused by wind to the subsequent interior water damage. We find the saturated insulation and hidden mold growth that the insurance company’s adjuster always seems to overlook.

The need for this kind of advocacy is exploding. The claims adjusting industry has ballooned into a $14.6 billion market, growing at an astonishing 9.6% each year for the past three years. This isn't just random growth; it’s driven by policyholders who are tired of being bullied. You can explore more about the claims adjusting market landscape to see the scale of the fight.

The Nightmare of Federal Flood Claims

Let's get one thing straight: your standard homeowner's or business policy covers zero flood damage. For that, you need a separate policy from the National Flood Insurance Program (NFIP), which is run by FEMA. These claims are a bureaucratic nightmare, and NFIP adjusters—whether from FEMA directly or a Write Your Own (WYO) company—are notoriously difficult.

NFIP adjusters operate under rigid, unforgiving federal rules. The red tape is designed to make you fail, and one tiny mistake on a form can get your entire claim thrown out. They often lowball repair estimates, ignore hidden damage, and are not incentivized to help you.

Fighting an NFIP claim without an expert is a recipe for financial disaster. A public adjuster with an NFIP certification is your only real weapon. We know their playbook, we speak their language, and we know how to navigate the maze of FEMA and their WYO carriers to dispute their low offers. We turn a guaranteed denial into a funded recovery.

The True Cost of Hiring a Public Adjuster

Let's talk about the cost. It’s the number one reason homeowners hesitate to call a public adjuster, and it’s a concern deliberately stoked by insurance company propaganda. They want you to worry about the fee.

The real question you should be asking is: what’s the true cost of not hiring a public adjuster? When your insurer is playing games, taking their first insultingly low offer is almost always the most expensive mistake you can make.

This Is an Investment, Not an Expense

First, let’s get one thing straight: there are absolutely no upfront fees or out-of-pocket costs. A legitimate public adjuster works on a contingency fee. That means we only get paid if we recover money for you, and our fee is just a small, agreed-upon percentage of the final settlement.

This structure is everything. It locks our financial interests directly to yours. We are 100% motivated to fight for the biggest possible settlement because our success is tied directly to your success. If you don’t get paid, we don’t get paid. It’s that simple.

Think of our fee not as a cost, but as a strategic investment in your financial recovery. You’re using a small piece of the money you would have never seen anyway to gain a massive advantage over the insurance company.

This setup takes all the risk off your shoulders. You get a licensed expert in your corner, fighting for you, without paying a single penny until your claim check is in hand.

The Simple Math of Getting What You’re Owed

Let me walk you through a scenario we see every single week. A homeowner has a major pipe burst, causing severe water damage. Their insurer, let's say Allstate, sends out their adjuster and offers a pathetic $40,000 to fix everything, knowing it won't even cover half the real damage.

The homeowner, feeling cornered, calls us. We come in, find all the hidden damage the company adjuster "missed," document everything meticulously, and force Allstate to the negotiating table with an ironclad estimate. The final, hard-won settlement comes in at $200,000.

Now for the fee. After our typical 15% contingency fee ($30,000), the homeowner walks away with $170,000 in their pocket. That’s $130,000 more than they would have gotten trying to fight this alone.

So, where was the "cost"? There wasn't one. Our fee was paid entirely from the extra money we recovered for them. It’s not an expense; it’s the key that unlocks the funds you actually need to put your life back together. Hiring an expert is how you make sure you don’t leave tens—or even hundreds—of thousands of dollars on the table.

How to Choose the Right Public Adjuster for Your Fight

When you’re going head-to-head with a multi-billion-dollar insurance company, the last thing you need is an amateur in your corner. Let’s be clear: hiring the right public adjuster isn’t just a good idea—it’s the single most important decision you’ll make in your fight for a fair settlement.

Not all adjusters are created equal. Choosing the wrong one can be just as damaging as the initial loss itself.

You need a licensed, experienced professional with a proven track record of forcing insurers like State Farm and Allstate to pay what they owe. This isn't about finding another contractor; it's about finding a strategic ally. Your goal is to vet candidates so thoroughly that you know they have the expertise, resources, and aggressive mindset required to dismantle an insurer's denial and win your claim.

Essential Questions to Ask Before You Sign Anything

Before you even think about signing a contract, you need to conduct a serious interview. A reputable public adjuster will welcome your questions and give you straight answers. If they get defensive or evasive, that’s your first major red flag.

Here's a checklist of critical questions to ask every single public adjuster you consider:

- Are you licensed in North Carolina (or Virginia)? This is non-negotiable. Ask to see their license number, then verify it with the state’s Department of Insurance. An unlicensed adjuster is operating illegally and has zero authority to represent you.

- Can you provide references from clients with claims like mine? Don’t just ask for a generic list. You want to talk to people who had the same type of damage (fire, water, storm) and the same insurer as you. This proves they have relevant, battle-tested experience.

- What is your exact strategy for fighting my insurer's denial? A vague answer won’t cut it. A true professional should be able to outline a clear, step-by-step plan for re-inspecting the damage, dissecting your policy, and building a new evidence package to force their hand.

- Who is actually handling my claim? Will it be the seasoned expert you're speaking with now, or will your file get passed off to a junior associate? You need to know exactly who your day-to-day contact will be.

- Are you an expert in NFIP flood claims? If your damage involves flooding, this is a deal-breaker. Federal flood claims are a nightmare of red tape and unique rules. You need an adjuster with specific NFIP certification and experience, period.

Critical Red Flags to Watch Out For

Just as important as knowing what to look for is knowing what to run from. Bad actors in this industry often prey on policyholders when they are most vulnerable.

Watch out for these massive warning signs:

- High-Pressure Sales Tactics: An adjuster who shows up uninvited and pressures you to sign a contract on the spot is bad news. A professional gives you the time and space to make an informed decision.

- Unrealistic Promises: If anyone guarantees a specific settlement amount before they’ve even done a deep dive into your damage and policy, they are lying to you. It's that simple.

- Asking for Upfront Fees: Legitimate public adjusters work on a contingency fee basis. Full stop. They get paid when you get paid. They never ask for money upfront.

- Also Working as a Contractor: This is a huge conflict of interest. A public adjuster’s only job is to get you the maximum settlement. They should not also be the contractor who stands to profit from the repairs.

Making the right choice is everything. For a deeper look into this critical decision, our guide on whether you should hire a public adjuster can provide more clarity. Finding the right partner ensures your fight against the insurance company is a fair one from the start.

Frequently Asked Questions About Public Adjusters

When your insurance company slams the door on your claim with a denial or a pathetic lowball offer, it's easy to feel overwhelmed. You’re left wondering what to do next, staring down a massive corporation that holds all the cards. But you have rights. Here are the straight-up answers to the questions we hear every single day from property owners just like you.

Is It Too Late to Hire a Public Adjuster if My Claim Was Denied?

Let’s get one thing straight: absolutely not. A denied claim isn't the end of the road; it's the beginning of the real fight. In fact, this is precisely when a public adjuster’s expertise becomes most powerful.

We specialize in ripping apart weak denial letters, finding the holes in the insurance company's logic, and reopening claims they wrongfully closed. We bring in overwhelming new evidence and force them to re-evaluate their initial, unfair decision. A landmark case, State Farm Fire & Cas. Co. v. Simmons (1998), showed how courts can penalize insurers for wrongfully denying claims, which is exactly the kind of leverage an expert advocate helps you build.

Will My Insurance Company Retaliate if I Hire an Advocate?

No. It is 100% illegal for your insurance company to punish you for hiring a public adjuster. They cannot legally cancel your policy, jack up your rates, or penalize you in any way for exercising your right to get professional help.

Think of it this way: your policy is a contract. You're simply bringing in an expert to make sure they honor their side of the deal. Any move they make against you for hiring representation is a clear act of bad faith, and it opens them up to a world of legal trouble.

A public adjuster levels the playing field. The insurance company has a team of experts on their side; hiring a public adjuster gives you an expert on yours. It's about forcing fairness, not starting a war.

What Is the Difference Between a Public Adjuster and an Attorney?

This is a critical distinction and a common point of confusion. A public adjuster is a state-licensed expert in one thing: property insurance claims. Our job is to investigate the damage, interpret the complex language in your policy, and negotiate with the insurance company to get you the maximum possible settlement without going to court.

An attorney steps in when the fight has to move to the courthouse—if your insurer acts in bad faith or flat-out refuses to negotiate a fair settlement. A good public adjuster builds such a rock-solid case that the insurance company knows a lawsuit would be a losing battle for them. We handle the claim; the attorney handles the lawsuit if it becomes absolutely necessary.

When you’re facing an uphill battle against your insurance provider, you don't have to fight alone. The team at For The Public Adjusters, Inc. is here to provide the expert advocacy you need to secure a fair settlement. We offer a no-cost, no-obligation claim review to help you understand your options. Contact us today to get the help you deserve.