Property Claim Adjuster In Raleigh: You’ve already lived through the damage. Now you’re dealing with the second disaster: the insurance claim.

The ceiling is still stained. The flooring is buckled. Your contractor sees obvious damage. Then the insurance company’s property claim adjuster shows up, spends a short time at the property, and sends back an estimate that doesn’t come close to what it will take to repair the loss. Or worse, they deny part of the claim and bury the reason in policy language that reads like it was written to confuse you.

That’s when most homeowners realize the truth. This process isn’t customer service. It’s negotiation. Sometimes it’s a fight.

If you’re frustrated, you’re not overreacting. You’re seeing the claim process for what it often becomes when the carrier starts low-balling, delaying, or denying damage that should be paid.

Table of Contents

- Your Claim is a Fight Not a Request

- The Three Types of Property Claim Adjusters Who Works for You

- When to Hire a Public Adjuster The Red Flags of a Bad Faith Claim

- The Public Adjuster Claim Process How We Fight for Your Settlement

- Success Stories Real Results Against Low-Ball Insurers

- Hiring a Public Adjuster in NC and VA Licensing Fees and Key Questions

- Conclusion Dont Accept a Low-Ball Offer Fight Back

- Frequently Asked Questions About Property Claim Adjusters

Your Claim is a Fight Not a Request

A lot of people start the same way. They’ve paid premiums for years, reported the damage promptly, cooperated fully, and expected a fair review. Then the estimate comes in thin, obvious damage is omitted, and the adjuster acts like you should be grateful they offered anything at all.

That’s not a misunderstanding. That’s an advantage.

When an insurance company controls the inspection, the estimate, the wording in the letters, and the pace of communication, it starts the claim with the advantage. If you don’t push back early, their version of the loss becomes the file history. Once that happens, every supplement gets harder.

What the carrier wants you to do

The insurance company wants you tired, rushed, and isolated. They want you to rely on their adjuster, their numbers, and their interpretation of the policy. If you’re juggling mitigation, contractors, temporary living issues, and work, that pressure works.

Here’s the hard truth. The insurer’s property claim adjuster is not your advocate.

A public property claim adjuster in Raleigh is different. That professional is licensed to represent the policyholder, not the carrier. That changes the entire posture of the claim. Instead of reacting to the insurer’s numbers, you put your own evidence, scope, and valuation on the table.

Practical rule: If the insurance company’s estimate doesn’t match what it will actually cost to repair the property, stop treating the claim like paperwork and start treating it like a dispute.

Why this shift matters

Homeowners usually call for help after the carrier has already framed the damage too narrowly. Maybe they priced only visible water staining and ignored trapped moisture. Maybe they scoped roof repair when replacement is the actual issue. Maybe they paid for cleanup but not full restoration.

The point isn’t to argue emotionally. The point is to document better than the carrier did.

That’s where a good public adjuster changes the outcome. They review the policy, inspect the property with the right tools, prepare a complete estimate, and push back when the insurance company plays games with scope, pricing, depreciation, causation, or delay.

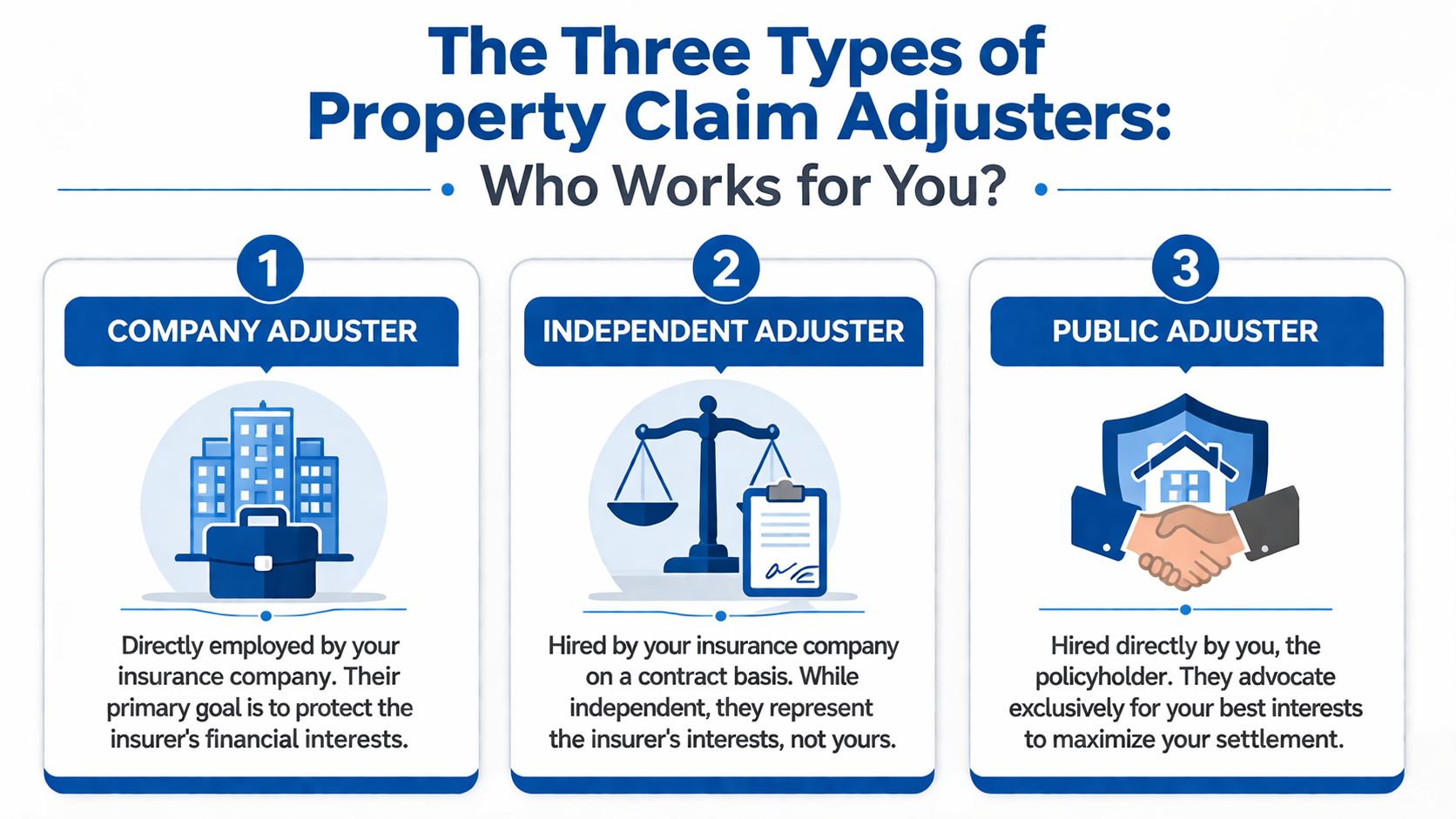

The Three Types of Property Claim Adjusters Who Works for You

The phrase property claim adjuster confuses people because it sounds like one job. It isn’t. There are three types, and the difference is loyalty.

If you don’t understand that, you’ll trust the wrong person.

One title, three loyalties

| Adjuster type | Who hires them | Who they represent | What that means for you |

|---|---|---|---|

| Company adjuster | The insurance company | The insurance company | They work inside the carrier’s system and answer to carrier management |

| Independent adjuster | The insurance company | The insurance company | They may be outsourced, but they still protect the insurer’s position |

| Public adjuster | You | You | They document and negotiate for the policyholder |

A company adjuster is a direct employee of the carrier. If State Farm, Allstate, or another insurer assigns one, that person’s job is to adjust the loss within the company’s rules, authority, and internal expectations.

An independent adjuster sounds neutral. Don’t be fooled by the name. Independent means they aren’t a salaried employee of the carrier. It does not mean they work for you. The insurer hires them, pays them, and expects them to represent the insurer’s interests.

A public adjuster is the only one in this lineup whose job is to advocate for the insured.

Why the insurer adjuster isn’t your advocate

Insurance company adjusters often work within preset authority limits. Claims that threaten to exceed those limits, often $10,000 to $50,000, can trigger escalation and delay. Those escalations can extend resolution timelines by 30 to 60 days, according to this property adjuster authority and reserve management reference.

That matters because it explains behavior homeowners see all the time. The adjuster looks agreeable in person, then the numbers come back low. Or they say they need more review the moment the actual scope gets expensive.

The person inspecting your house may sound helpful. The file still belongs to the insurance company.

Here’s the practical breakdown:

- Company adjuster: Usually knows the carrier’s software, guidelines, and preferred claim path. That can mean a narrow scope from the start.

- Independent adjuster: Often gets deployed during storm volume or catastrophe seasons. Speed becomes the priority, and fast files often miss damage.

- Public adjuster: Reviews the loss from the policyholder’s side and has no reason to defend the carrier’s low estimate.

If you want a deeper side-by-side explanation, read this comparison of an insurance adjuster vs public adjuster.

One more point matters here. The broader claims profession is large and varied. The U.S. workforce included 367,687 claims adjusters, appraisers, examiners, and investigators in 2024, with an average yearly wage of $73,083, while the occupation’s median annual wage was $76,790 as of May 2024, according to the Bureau of Labor Statistics overview of claims adjusters. That tells you this is a real profession. It does not tell you loyalty. Loyalty depends on who signs the adjuster’s paycheck on your claim.

When to Hire a Public Adjuster The Red Flags of a Bad Faith Claim

Your kitchen ceiling is open, the floors are buckling, and the insurer keeps asking for one more document while the house gets worse. That is the moment to stop waiting for the carrier to “get there” and bring in a public adjuster.

Hire one as soon as the insurance company starts controlling the story of the loss instead of paying for the full scope of it. The longer you let a weak inspection, a thin estimate, or a vague denial sit in the file, the harder it becomes to correct the claim.

What should put you on alert

Bad claims handling usually starts small. A missed room. A short inspection. A polite email that answers nothing. Then the pattern becomes clear.

Watch for these red flags:

- The estimate is far below the actual repair cost: The carrier is setting the claim baseline low and hoping you accept it.

- The inspection feels rushed or incomplete: They skip the attic, ignore insulation, miss moisture spread, or fail to look behind obvious damaged areas.

- The denial letter is hard to understand on purpose: It uses policy language as cover without clearly tying the facts of your loss to the denial.

- The file keeps stalling: Calls go unreturned, emails drag out, and new adjusters keep stepping in and asking for the same material.

- Parts of the claim are carved out: They allow tear-out but not put-back. They pay for drying but not the damage caused by the water. They approve a patch where full replacement is the only honest repair.

That is how underpayment gets built.

If you want a plain-English explanation of the legal conduct behind these tactics, read this overview of insurance company bad faith. It helps you spot the point where delay, denial, and distortion stop looking routine and start looking deliberate.

Confusion helps the carrier. Clarity helps your claim.

Commercial claims go sideways for a different reason

Business owners get squeezed from two directions at once. The building estimate comes in light, and the income loss gets pushed aside or treated like an afterthought.

I see this all the time. A restaurant loses weeks of revenue after a kitchen fire, but the insurer stays locked on tile, paint, and equipment cleaning. A retail store has water damage and reduced foot traffic, yet the carrier acts as if the only issue is drywall. A warehouse can’t fully operate, but the claim gets handled like a basic repair file.

That is exactly when a public adjuster becomes a weapon, not a convenience.

Commercial losses often involve business interruption, extra expense, delayed reopening, damaged inventory, and lease issues. If the carrier is only talking about the building and avoiding the financial hit to the business, get backup immediately.

Claims that deserve immediate backup

Some losses are too expensive, too technical, or too easy for an insurer to narrow.

Bring in a public adjuster fast if your claim involves:

- Fire and smoke damage: Cleaning scope, hidden smoke spread, contents damage, and odor treatment are regularly cut short.

- Large water losses: Moisture mapping, insulation damage, subfloor issues, and mold-related conditions get minimized when no one pushes the file.

- Wind and storm damage: Roof systems, flashing, siding match, interior leaks, and code items are often split apart to reduce payout.

- Commercial property losses: Business interruption and extra expense need proof, calculation, and pressure. They do not get paid correctly by accident.

- Repeated delays or changing explanations: If the carrier keeps shifting its position, the claim is already off track.

Trust what you are seeing. If the insurance company is steering the claim toward a cheaper outcome, hire your own expert before that version of the loss hardens into the file.

The Public Adjuster Claim Process How We Fight for Your Settlement

A public adjuster doesn’t just argue with the carrier. A good one rebuilds the claim from the ground up.

That means policy analysis, evidence collection, estimating, and negotiation. It’s a disciplined process. When done right, it takes control away from the insurance company’s version of the loss and puts the facts back where they belong.

Start with the policy, not the carrier estimate

The first mistake homeowners make is assuming the insurance company’s estimate tells them what the policy covers. It doesn’t. It tells you what the insurer decided to include.

A public adjuster starts with the policy itself. Coverage grants, exclusions, endorsements, depreciation rules, ordinance issues, contents provisions, and loss settlement language all matter. If you skip that step, you’re arguing price before you’ve nailed down coverage.

That’s also where a qualified firm like For The Public Adjusters, Inc. and its public claim adjuster services can be useful. The work includes claim review, documentation, estimate preparation, and direct negotiation from the policyholder side.

Document what the insurer missed

The inspection is where weak claims get exposed and strong claims get built.

Public adjusters use tools that many homeowners never see during the carrier’s first visit. Thermal imaging can identify hidden moisture and electrical or water-related problems that aren’t visible on the surface. Left undetected, that kind of hidden water damage can increase repair costs by 20% to 50% due to mold. The same technology can reduce assessment time by up to 40% and increase recoverable claim values by 15% to 30% in storm-related claims, according to this technical discussion of thermal imaging and 3D mapping in property loss adjustment.

3D mapping matters too. It creates measurable models of damaged areas, which helps when the insurer tries to shrink quantities or ignore affected sections of the property.

A proper documentation package can include:

- Thermal imaging results: Useful for hidden moisture behind walls and ceilings.

- 3D measurements: Helps support room dimensions, roof areas, and repair scope.

- Photo sequencing: Before, during, and after mitigation.

- Room-by-room damage notes: Not broad labels like “minor water.”

- Contractor and specialist input: Especially where structure, smoke, or complex repairs are involved.

Here’s a useful explainer before we get deeper into tactics:

Build the demand and force the response

Once the evidence is organized, the public adjuster prepares a full estimate and claim package. At this stage, the carrier loses the benefit of vagueness.

Instead of saying, “I think they missed damage,” you now have a documented scope, measurements, photos, pricing logic, and policy support. That changes the negotiation.

A strong claim file makes the insurer explain its low number line by line. That’s where weak carrier estimates start falling apart.

Then comes negotiation. The public adjuster pushes for revised scope, challenges unsupported exclusions, disputes low valuations, and keeps the pressure on the file. If the insurer changes adjusters, resets the conversation, or tries to wear you down, the paper trail stays intact.

That’s the true value. Not noise. Advantage.

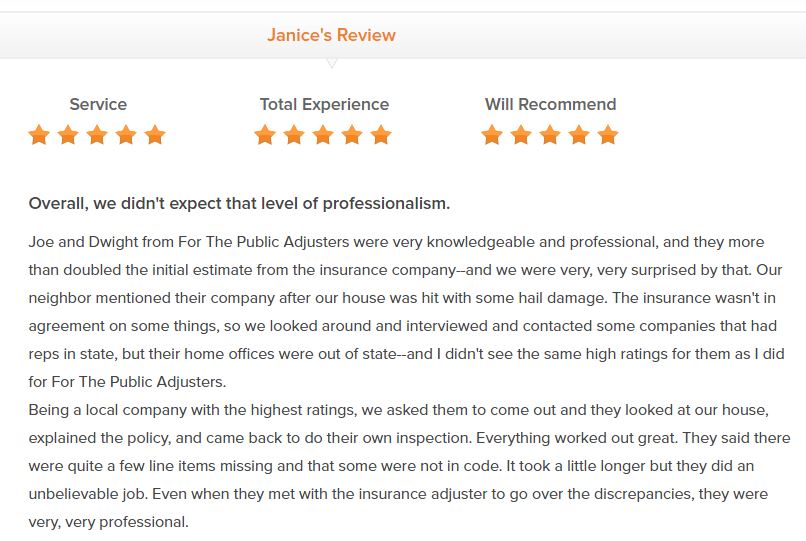

Success Stories Real Results Against Low-Ball Insurers

People don’t hire a public adjuster because they like paperwork. They hire one because they’re tired of getting pushed around.

And when they finally get someone on their side, the reaction is usually the same. Relief first. Then anger that they didn’t do it sooner.

What real clients care about

They care that somebody returned their call. They care that someone inspected the loss carefully. They care that the insurance company stopped dictating the story.

That’s what shows up again and again in customer feedback. Policyholders talk about better communication, stronger documentation, and settlements that made practical repair possible instead of forcing half-measures.

Because the instructions for this article prohibit inventing quotes, case values, or lawsuit results that aren’t verified, I’m not going to do what a lot of marketing articles do and make up a dramatic fire claim number or pretend a court handed down a victory we can’t substantiate here. You should be skeptical of any article that does.

What I can say plainly is this: when a public adjuster steps into a poorly handled homeowner or commercial property claim, the file usually gets sharper fast. Missing damage gets documented. Carrier estimates get challenged. Weak denials get tested against the policy language and the physical evidence.

Why these stories matter

A review screenshot matters because it shows you other policyholders have already been in the spot you’re in now. They dealt with stress, carrier resistance, and uncertainty about whether pushing back was worth it.

Here’s what to focus on when you read reviews for any public adjuster:

- Did the reviewer mention communication? Silence kills claims.

- Did they describe a dispute, not just a smooth claim? You need help when things are going wrong.

- Did the adjuster stay involved through negotiation? A quick inspection is not representation.

- Did the reviewer sound informed by the end? Good adjusters don’t just argue. They educate the client.

You’re not looking for a friendly salesperson. You’re looking for someone who can carry a disputed property claim without blinking when the insurer pushes back.

The best success stories aren’t flashy. They’re practical. A homeowner gets enough money to repair the home correctly. A business owner gets the carrier to deal with the claim seriously. A family stops feeling trapped by a low-ball number.

That’s a real result.

Hiring a Public Adjuster in NC and VA Licensing Fees and Key Questions

Once you decide to get help, don’t hire the first person who sounds confident. This industry has solid professionals and weak ones. You need to separate them quickly.

What to verify before you sign

Start with licensing. In North Carolina and Virginia, you should verify that the public adjuster is properly licensed in the state where your property claim is being handled. If someone gets vague when you ask about their license, walk away.

Ask how they get paid. Most public adjusters work on a contingency fee, which means they’re paid from the claim recovery rather than by an upfront retainer. The exact percentage can vary, so get the fee agreement in writing and read it carefully before signing.

Then check whether they handle your kind of claim. A homeowner water loss, a fire claim, a wind claim, and a commercial business owner policy dispute are not interchangeable files.

A useful starting point is this guide on whether you should hire a public adjuster.

Questions that expose weak adjusters fast

Don’t ask, “How long have you been in business?” only. Plenty of people stay in business and still do weak work. Ask sharper questions.

- Who will inspect my property? You want to know whether the person pitching you is the person handling the file.

- How do you document hidden damage? Listen for real tools and methods, not vague promises.

- How often will you update me? If they can’t define communication, expect frustration.

- Have you handled disputes like mine in NC or VA? Local claim experience matters.

- What happens if the insurer changes adjusters or delays response? Their answer will tell you whether they know how claims play out.

- Do you review the policy before building the estimate? If they start with price only, that’s a problem.

A strong public adjuster should be able to explain their process in plain English. If they hide behind buzzwords, they probably can’t defend the claim when the carrier starts pushing back.

Here’s my opinion. Hire the adjuster who talks like a file builder, not a closer. You don’t need charisma. You need discipline, documentation, and persistence.

Conclusion Dont Accept a Low-Ball Offer Fight Back

If the insurance company underpaid, delayed, or denied your property claim, you don’t have to accept their first version of the loss.

That first estimate is often a negotiating position. It is not a verdict.

The carrier has professionals working the file to protect its money. You need a professional working to protect your recovery. That’s what a public property claim adjuster in Raleigh does. They inspect, document, estimate, and negotiate from your side of the table.

If your claim involves a home, dwelling, or commercial property loss and the insurer is playing games, stop waiting for them to suddenly become reasonable. Most don’t.

Get the damage reviewed. Get the policy examined. Get the numbers challenged.

A low-ball offer only wins if you treat it like the final word.

Frequently Asked Questions About Property Claim Adjusters in Raleigh

Common questions from homeowners and business owners

Can I hire a public adjuster after I already got an insurance estimate?

Yes. In many disputed claims, that’s exactly when people do it. A low estimate often becomes the reason to bring in a public adjuster, not a reason to give up.

What if I already cashed the insurance check?

You may still have options, depending on the facts of the claim, what the check represented, and whether additional damage or underpayment issues remain. Don’t assume cashing a check ends every dispute. Have the claim file and settlement documents reviewed before you surrender your advantage.

Can the insurance company punish me for hiring a public adjuster?

You have the right to get representation on a property claim. A carrier may not like losing control of the conversation, but that doesn’t change your right to bring in your own licensed advocate.

Are public adjusters especially important in flood claims?

Yes, especially with NFIP flood claims. These files have their own rules, deadlines, and proof requirements. After major hurricanes in North Carolina, over 25% of NFIP claims were initially underpaid or denied due to disputes, and public adjusters help policyholders deal with the strict proof-of-loss requirements, according to this NFIP flood claim dispute overview.

What kinds of property claims make the strongest case for hiring one?

Complex claims. Fire, smoke, widespread water damage, storm losses with hidden damage, and commercial claims with business interruption issues are the ones most likely to get mishandled when the insurer controls the scope unchallenged.

Will a public adjuster speed up my claim?

Sometimes the carrier moves faster once it realizes the file is being documented and tracked properly. Other times the insurer still delays. The primary benefit is that the claim becomes organized, supported, and much harder for the carrier to dismiss with weak explanations.

If your homeowner, dwelling, or commercial property claim has been delayed, denied, or underpaid, talk to For The Public Adjusters, Inc. about a no-cost claim review and find out whether the insurance company’s numbers hold up under real scrutiny.