When you file a property damage claim against your homeowner or business owner policy, you’re not asking for a favor. You’re demanding the protection you paid for. A public claim adjuster is a state-licensed insurance professional who fights for one person and one person only: you, the policyholder. Their job is to make sure you get every single penny you’re owed under your policy, and they work exclusively for you—never for the insurance company.

A Public Claim Adjuster Is Your Expert Ally in the Fight Against Insurers

That first settlement offer from your insurance company often feels like a slap in the face. After a fire, flood, or hurricane devastates your property, seeing a shockingly low number is more than just disappointing; it’s a betrayal. But this isn’t some accident or simple miscalculation. It’s a calculated business strategy.

Huge insurance carriers like State Farm and Allstate are built to protect their bottom line. That business model leads directly to infuriating claim delays, confusing denials, and lowball offers that don’t even begin to cover the real cost of your damages. They are not looking out for you; they are looking out for their shareholders.

This is the exact moment a public claim adjuster becomes your most powerful weapon. They are licensed experts who step into the ring to fight on your behalf.

Leveling an Unfair Playing Field

The second you report a loss, you’re thrown into a battle against a multi-billion-dollar corporation. They have armies of adjusters, lawyers, and engineers all trained with one goal in mind: minimize what they have to pay you. They wrote the policy, they know the loopholes, and they exploit every single one.

A public adjuster’s entire mission is to turn the tables on these tactics. Here’s how they do it:

- Meticulous Damage Documentation: They perform their own exhaustive inspection of your property, uncovering every bit of damage the insurance company’s adjuster conveniently overlooked or ignored.

- Deep Policy Analysis: They tear apart the dense, confusing language of your insurance policy to find and prove all areas of coverage you’re entitled to claim.

- Aggressive Negotiation: Armed with indisputable evidence and a damage estimate that reflects the true cost of rebuilding, they go to war with the insurer, dismantling their lowball offer and fighting for the settlement you actually deserve.

This is an adversarial system, and it’s why so many homeowners feel beaten down before the fight even begins. The numbers don’t lie: the average home insurance company denies a shocking 37% of all claims. Some of the biggest carriers in the country reject between 40% and 50% of cases they see. This explosion in denials is exactly why the demand for public adjusters has skyrocketed. You can learn more about how claim denials are pushing homeowners to seek help.

A public claim adjuster fundamentally changes the dynamic. It’s no longer you against a corporate giant. It’s an expert vs. expert, forcing the insurance company to deal with someone who speaks their language and won’t be bullied.

When you hire a public claim adjuster, you’re not just getting help with some forms. You are bringing in a professional ally who is dedicated to turning a rigged game into a fair fight—one you can win. This allows you to focus on what matters: getting your life, home, or business back together with the full compensation you are owed.

Decoding Who Really Works for You in a Claim

After you file a homeowner or business property damage claim, the insurance world suddenly gets very crowded. You’ll hear the word “adjuster” thrown around a lot, but you have to understand one hard truth: only one of them actually works for you. Getting this distinction right is the key to getting the money you need to rebuild.

The first person you’ll meet is the adjuster sent by your insurance company. This person might be a direct employee, known as a staff adjuster, or a contractor they hired, called an independent adjuster. It doesn’t matter what they call themselves—they have one thing in common: your insurance company signs their paychecks.

Their job, their performance reviews, and their career all depend on protecting the insurer’s bottom line. They are trained to evaluate your loss through a lens that serves the insurance company’s financial interests, which almost always means one thing: paying you as little as legally possible.

This is a massive conflict of interest. The person responsible for assessing your devastating loss is professionally and financially motivated to shrink your payout. They are not your advocate. They are not your friend. They are an agent of the insurance company.

The Unwavering Loyalty of a Public Claim Adjuster

Then there’s the public claim adjuster. This is a state-licensed professional that you hire to represent you and only you. Their loyalty is never divided. They work on your behalf, and their single mission is to fight for the absolute maximum settlement you’re entitled to under your policy.

Think of it this way: if you were sued, would you ask the other side’s lawyer for advice? Of course not. You’d hire your own attorney to fight for you. An insurance claim is no different. Relying on the insurance company’s adjuster is like letting their lawyer build your case against them.

A public adjuster levels the playing field. They become your dedicated expert, your advocate, your fighter. They take over the entire process—from documenting every last detail of damage to battling the insurer in negotiations. To go deeper, check out the key differences between a public adjuster vs. an insurance adjuster in our guide.

The core difference is simple: The insurance company’s adjuster serves the company’s financial interests. A public claim adjuster serves your financial interests.

This isn’t a small detail—it’s everything. It’s the most critical factor that will determine whether you get a fair settlement or a lowball offer. Understanding who works for whom is the first step toward taking back control of your claim.

A Breakdown of Adjuster Loyalties

Let’s put this in black and white so there’s no confusion about where each adjuster’s allegiance lies and what they’re trying to accomplish.

Comparison of Adjuster Loyalties

| Adjuster Type | Who They Work For | Primary Objective |

|---|---|---|

| Staff Adjuster | Your Insurance Company (Direct Employee) | Minimize the claim payout to protect the company’s profits and meet internal goals. |

| Independent Adjuster | Your Insurance Company (Contractor) | Minimize the payout to secure future contracts and satisfy their client, the insurer. |

| Public Claim Adjuster | You, the Policyholder (Your Employee) | Maximize your settlement by thoroughly documenting all damages and negotiating aggressively. |

As you can see, their goals are in complete opposition to yours. The adjusters sent by your insurer are trained to find loopholes in your policy and reasons to deny or underpay your claim. They use their own software that is notorious for spitting out low-cost estimates and often miss hidden or complex damages.

When you hire a public adjuster, you flip the script. They bring their own expertise, their own estimating software, and an encyclopedic knowledge of insurance policies to build an ironclad case for your claim’s true value. They don’t work for Allstate, State Farm, or any other carrier. They work for you. Their success is tied directly to yours, and that means they fight for every single dollar you deserve.

How Public Adjusters Dismantle Lowball Offers

When disaster hits your home or business, that first settlement offer from your insurance company feels like a punch in the gut. It’s almost always insultingly low, leaving you completely stunned and wondering how you’ll ever rebuild.

This isn’t a mistake. It’s a strategy.

Insurance giants like State Farm and Allstate have built entire systems designed to pay out as little as legally possible. But a lowball offer isn’t the end of the story—it’s the start of a fight. And a public claim adjuster is the best weapon you can have in that fight.

They don’t just argue for a bigger check; they systematically dismantle the insurance company’s entire argument for underpaying you. It’s a methodical, evidence-based counter-attack designed to leave your insurer with no other option but to pay what you’re actually owed.

The Independent Investigation and Damage Discovery

It all starts with a completely independent and ridiculously thorough inspection of your property. The insurance company’s adjuster might have spent 30 minutes going through a checklist on their iPad. A public adjuster will spend hours, sometimes even days, documenting every single crack, stain, and piece of warped wood.

They’re trained to find what the company adjuster is paid to ignore. This includes:

- Hidden Damage: They go way beyond the obvious. They’re looking for things like smoke damage that has penetrated deep inside your walls, hidden water saturation that guarantees a future mold problem, or a compromised structural beam the company adjuster “missed.”

- Code Upgrades: They know that if your property was built years ago, it must be rebuilt to meet today’s much stricter building codes. They calculate the cost of these mandatory upgrades—something insurers conveniently “forget” to include in their initial offers all the time.

- Full Scope of Loss: For a business, this isn’t just about a damaged roof or broken equipment. It’s about the lost income during downtime, the extra expenses needed to operate from a temporary location, and the real-world cost of business interruption.

This deep-dive investigation is how a public adjuster begins to build an undeniable case. They aren’t playing by the insurer’s rules; they’re writing a new rulebook based on the truth of your loss.

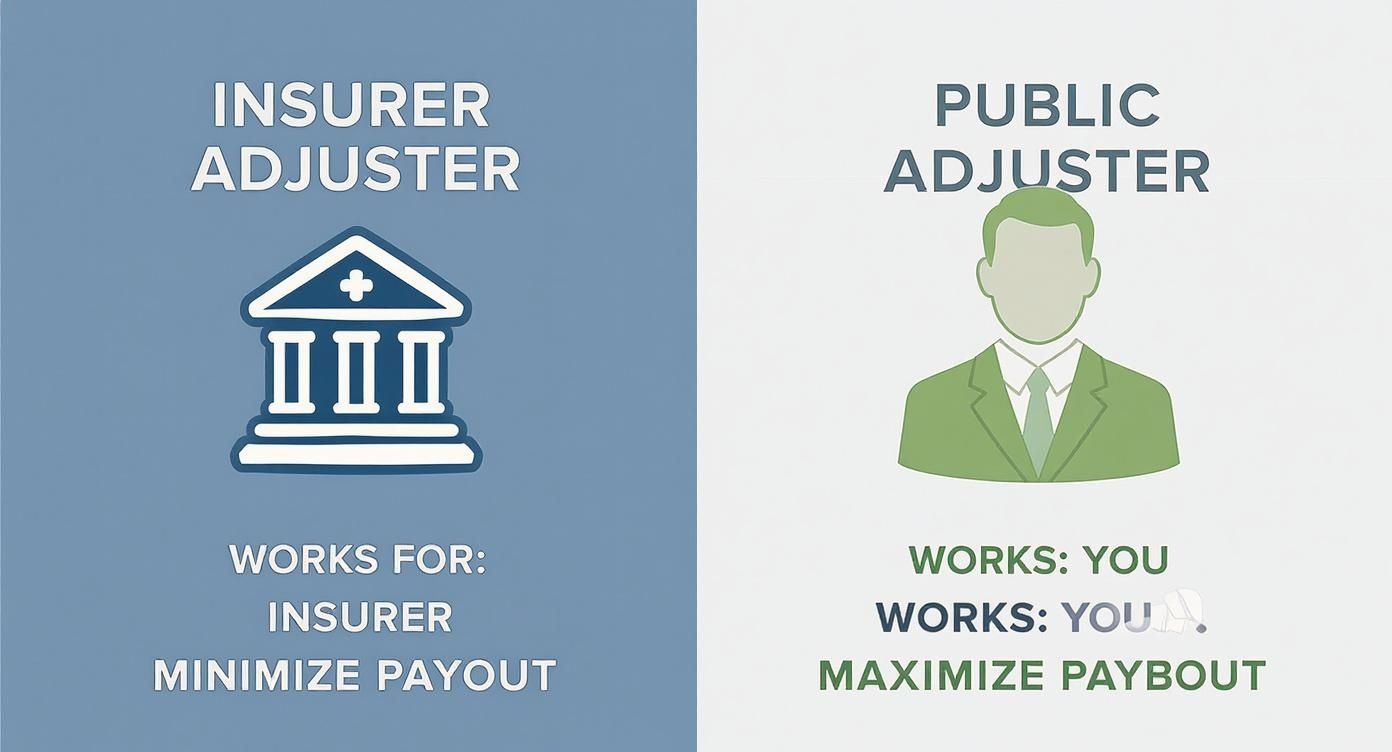

The infographic below nails the fundamental difference in who each adjuster really works for.

This visual gets right to the point of the built-in conflict of interest: the insurance company’s guy is there to protect their bottom line. The public adjuster is there to fight for yours.

Assembling an Arsenal of Evidence

Once the true scope of damage is uncovered, the next move is to build a mountain of proof. A weak claim based on your word against theirs is easy for an insurer to deny. An ironclad claim backed by indisputable evidence is impossible for them to ignore.

A public adjuster gathers and organizes every piece of documentation needed to force the insurer’s hand. This evidence package usually includes:

- Detailed inventories of every single lost item, from furniture and electronics down to the last fork and spoon, all with meticulously researched replacement cost values.

- Expert reports from third-party professionals like structural engineers, roofing consultants, or industrial hygienists to prove the extent of the damage.

- Multiple, independent repair estimates from trusted local contractors—not the cheap, corner-cutting vendors on the insurance company’s preferred list.

This arsenal of proof systematically tears apart the insurance company’s lowball estimate, replacing their faulty assumptions with hard, undeniable facts. When you learn how a public adjuster can secure higher compensation for property damage claims, you begin to see the raw power of having a professional advocate on your side.

Case Study in Action: A Florida homeowner’s claim for hurricane damage was lowballed by his insurer at just $17,000, which wouldn’t even cover the roof replacement. He hired a public claim adjuster who conducted a thorough investigation, uncovering extensive water damage inside the walls and attic that the company adjuster had completely ignored. Armed with expert reports and detailed estimates, the public adjuster reopened the claim and negotiated a final settlement of $98,000—nearly six times the original insulting offer.

Leveraging Your Policy for Maximum Payout

With that mountain of evidence ready, the public adjuster then attacks the insurance policy itself. These documents are deliberately written to be dense and confusing, filled with legal jargon that benefits one party: the insurer.

Your public adjuster knows how to read between the lines and turn that complex language into your advantage.

They find every clause, endorsement, and provision that supports your claim and use it against the insurance company. They present a powerful, evidence-backed demand package that speaks the insurer’s own language, leaving them no room to argue or wiggle out of their obligations.

They don’t just ask for more money. They prove, line by line from your own policy, why you are owed every last penny. This is how they dismantle a lowball offer and force the insurance company to finally pay the full and fair value of your claim.

Why Insurers Deny Claims and How to Fight Back

Let’s start with a hard truth: your insurance company is not your friend. It’s a for-profit business, and its first and most important legal duty is to its shareholders, not to you.

This creates a brutal conflict of interest from the moment you file a claim. Every single dollar they pay you for your fire, flood, or hurricane damage is a dollar taken directly from their bottom line.

This isn’t a secret. The relentless pressure to boost profits has baked a toxic culture into the industry, a strategy often called “delay, deny, defend.” It’s a cynical playbook where valid claims from honest people who pay their premiums are systematically stonewalled, undervalued, or flat-out rejected for the flimsiest of reasons.

This isn’t just a few frustrated homeowners complaining. It’s a documented strategy that has been exposed in courtrooms for decades.

The Profit-Driven Playbook of Major Insurers

The tactics insurance carriers use are designed to break you. They know that after a disaster, you’re exhausted, stressed, and financially desperate. By dragging their feet on your claim or throwing a pathetic lowball offer your way, they’re betting you’ll give up.

They’re betting you’ll get so worn down that you’ll accept pennies on the dollar just to get something to start rebuilding your life.

This is a dirty game with a well-worn set of rules:

- Twisting Your Policy Language: They’ll take the dense, confusing wording in your own policy and use it against you, claiming your specific type of damage isn’t covered when it absolutely is.

- Blaming “Old” Damage: This is a classic. They’ll argue that your leaking roof wasn’t caused by the hurricane but by “pre-existing conditions” or “poor maintenance.” It’s a blatant attempt to shift the blame and avoid paying.

- Using Bogus Estimates: The adjuster they send uses proprietary software that spits out ridiculously low, outdated prices for labor and materials. This guarantees their first offer won’t come close to what it actually costs to fix the damage.

A public claim adjuster has seen this playbook thousands of times. They recognize these moves for what they are—not honest mistakes, but calculated business decisions designed to protect profits.

In the landmark case of State Farm Mut. Auto. Ins. Co. v. Campbell, the U.S. Supreme Court found that State Farm had engaged in a nationwide scheme of bad faith practices to cap payouts on claims. This case exposed internal documents that revealed a corporate culture focused on denying claims and lowballing settlements to meet financial targets, proving that these tactics often come from the very top.

These legal battles blew the lid off a systemic effort to put profits over people. They proved that homeowners and businesses were being forced to sue just to get the money they were owed under their own policies. This is the adversarial world you step into the moment you file a claim.

Fighting Back with an Expert on Your Side

Trying to fight these bad-faith tactics on your own is an exhausting, uphill battle. The insurance company has an army of lawyers and adjusters on its side. You need a professional in your corner, too.

A public claim adjuster is your advocate. They are armed with the expertise to dismantle the insurance company’s weak arguments and force them to honor the contract you paid for.

They know the legal precedents. They know which documents, expert reports, and specific policy clauses are needed to build an ironclad case that the insurance company can’t just brush aside.

Think of it this way: your insurance company has built a fortress of legal jargon and delay tactics to guard its money. A public claim adjuster knows exactly where the cracks are in that fortress. They apply targeted pressure, backed by cold, hard evidence, to make the insurer pay what they rightfully owe you.

They don’t just ask for a fair settlement. They build a case that legally and factually demands it.

How Does a Public Adjuster Get Paid?

Let’s get straight to the point most people worry about: the cost. After your property gets slammed by a disaster, the last thing you want is another bill. The insurance companies know this. They count on you being too overwhelmed and cash-strapped to even consider hiring your own expert.

But here’s the critical piece of information they hope you never learn: a public adjuster works on a contingency fee basis.

That means you pay absolutely nothing upfront. No retainer. No hourly rate. No out-of-pocket expenses. Their fee is a small, pre-negotiated percentage of the final insurance settlement they win for you.

This isn’t just a payment model; it’s a built-in guarantee. It perfectly aligns their success with your success.

It’s an Investment, Not an Expense

Think about it. A public adjuster only gets paid when you get paid. And the bigger the settlement they force the insurance company to pay you, the more they earn. This flips the entire script. Their fee isn’t a “cost” you have to bear; it’s a powerful investment in your own financial recovery.

Here’s why this changes everything:

- You Risk Nothing: Hiring them costs you zero dollars out of pocket. All the risk is on them to perform.

- They Fight for Every Dollar: Their only incentive is to maximize your claim payout, not to quickly close the file for their employer.

- You Get Your Life Back: You can focus on your family and your business while a hardened expert battles the insurance company for you.

To keep things fair, most states—including North Carolina and Virginia—put legal caps on these contingency fees. The exact percentage is always laid out in plain English and signed before any work starts, so you’ll never face a surprise bill.

Don’t Get Fooled by the Insurance Company’s Math

This is where homeowners get tricked. They see a fee and think they’re losing money. The reality is the polar opposite. The massive increase in your settlement that a public adjuster secures will almost always dwarf their fee.

Let’s run the numbers. The insurer’s adjuster shows up and offers you a pathetic $50,000. You hire a public adjuster who documents every last detail, fights back against the lowball tactics, and forces a final settlement of $150,000 for a 10% fee ($15,000).

You are not “losing” $15,000. You are gaining an extra $85,000 you were never going to see. You walk away with $135,000 instead of the original $50,000 insult.

This payment structure is what separates your advocate from their employee. A public adjuster’s compensation, typically between 5% and 20% of the settlement, is directly tied to the results they get for you. That’s a world away from the salaried company adjuster whose real job is to protect the insurer’s bottom line. You can discover more insights about adjuster compensation models to see just how deep this conflict of interest runs.

Hiring a public claim adjuster isn’t about giving up a slice of your settlement. It’s about fighting to get the whole pie—that extra 80-90% of the money you’re owed but would have been forced to leave on the table. It is the single best investment you can make to get the funds you need to truly rebuild.

When You Should Hire a Public Claim Adjuster

Knowing the right moment to call for backup can be the difference between a fair settlement and financial disaster. The single best time to bring a public claim adjuster into the fight is right after the damage happens, but most people are not aware that such help even exists. However, there will usually be some classic red flags from insurers that scream you need a pro on your side—and fast.

If your insurer slides an insultingly low settlement offer across the table, denies your claim with a vague or nonsensical excuse, or starts dragging their feet with endless delays, it’s time to hire an expert. Don’t wait. That’s your signal that a battle has begun.

Recognizing the Triggers for Professional Help

Some types of property damage are notoriously complex, and they almost always demand professional intervention. The more complicated the damage, the more loopholes and excuses your insurance company will find to underpay or deny your claim.

It’s time to seriously consider calling a public adjuster if you’re dealing with:

- Large or Complex Losses: A major fire, a burst pipe that floods multiple rooms, or extensive smoke damage—these disasters create hidden problems that the insurance company’s adjuster is trained to ignore. A public adjuster knows exactly where to look for the costly damages that aren’t obvious at first glance.

- Business Interruption Claims: Trying to calculate the full financial fallout from a business shutdown is a nightmare. You’re not just dealing with repairs; you’re dealing with lost income, extra expenses, and operational downtime. Insurers almost always undervalue these claims, so expert documentation is non-negotiable.

- Feeling Overwhelmed: This is the big one. If you feel outgunned, confused by your own policy, or bullied by the adjuster, that’s your gut telling you that you need an advocate in your corner.

The reality is, the claims process has become more and more of a fight, which is why the demand for policyholder advocates has exploded. The claims adjusting industry has ballooned into a $14.6 billion market, rocketing up at a 9.6% annual rate. That growth isn’t an accident; it’s a direct response to homeowners and businesses needing experts to force insurance companies to pay what they owe. You can discover more insights about this industry’s expansion.

Why Acting Early Is So Critical

Getting a public adjuster involved from the very beginning stops you from making costly, irreversible mistakes. Accepting a lowball offer because you’re desperate or signing a release form without realizing you’re signing away your rights can cost you tens of thousands of dollars. An expert takes control from day one.

A public claim adjuster ensures your claim is documented and presented correctly from the start, shutting down the insurer’s delay-and-deny tactics before they even get off the ground. They protect you and let you focus on getting your life back.

What specific specialized tools and methods does a Public Claim Adjuster use that the average policyholder does not have?

Public Adjusters use specialized forensic tools like thermal imaging cameras and moisture mapping to find hidden damage, and industry-standard estimating software like Xactimate to generate a repair estimate that speaks the insurer's professional language, forcing an apples-to-apples negotiation.

How can a Public Adjuster ensure all my insurance policy's coverage extensions and sub-limits are fully applied to my claim?

The Public Adjuster conducts a forensic Policy Analysis to uncover often-missed benefits, such as Code Upgrade coverage (Ordinance or Law), full Additional Living Expenses (ALE), and debris removal beyond the basic coverage limit, maximizing every dollar paid for in the premium.

What critical documentation errors does a Public Adjuster prevent that lead to claim denials or massive underpayment?

We prevent the two worst errors: 1) Failing to file a timely and accurate Proof of Loss statement, which is a contractual requirement; and 2) Disposing of damaged contents before a full, replacement-cost inventory is professionally documented, making the loss impossible to prove.

How much more can I expect to receive on my claim settlement after paying the Public Adjuster's contingency fee?

While results vary, studies consistently show that policyholders who hire a Public Adjuster receive settlements that are significantly higher—often 20% to 700% higher—than the insurer's initial offer, meaning the increased recovery typically more than covers the adjuster's fee.

When is the absolute latest point in the claims process I can hire a Public Adjuster?

While early retention is best, you can hire a Public Adjuster at any stage: after a denial, after receiving a low offer, or even after a claim has been closed. We specialize in reopening denied claims and filing supplemental claims to recover funds the insurer missed.

How does a Public Adjuster fight the insurer's argument that my roof damage is "wear and tear" instead of hail/wind damage?

The Public Adjuster counters with forensic engineering reports and meteorological data (weather reports) that scientifically tie the damage date to a specific covered storm event, shifting the burden of proof back to the insurer to disprove the covered peril.

If my claim is stuck in a dispute over the dollar amount, how does a Public Adjuster leverage the Appraisal process?

The Public Adjuster acts as your dedicated Appraiser, submitting an expertly prepared, independent valuation. This forces the insurer into the Appraisal mechanism, which is a binding contractual resolution that often bypasses litigation, saving you time and legal fees.

What recourse do I have if the insurance company uses my recorded statement against my claim?

if your initial recorded statement contained inaccuracies or misstatements (a common error), your Public Adjuster can use subsequent sworn documentation (like the Proof of Loss and expert reports) to clarify the facts and demonstrate the actual scope of the loss. Never give a recorded statement without expert preparation.

Are Public Adjusters legally licensed and regulated, and how can I verify their credentials?

Yes. Public Adjusters are state-licensed professionals regulated by the Department of Insurance (DOI) in their operating state. You should always verify their current license status and check for consumer complaints directly on the state's DOI website before hiring.

How does the contingency fee model ensure the Public Adjuster is fully aligned with my recovery goal?

The contingency fee (typically 10-20% of the settlement) means the Public Adjuster only gets paid if and when you receive a payout. This model fully aligns our financial incentive with yours: the higher your settlement is, the higher our fee is, guaranteeing our commitment to maximum recovery.

What should my contract with a Public Adjuster include to protect me from unexpected costs?

The contract should clearly state the contingency fee percentage and specify that the fee is only charged on the final settlement amount—and that there are no upfront fees or charges if no recovery is made. The contract must also include your right to cancel within the state-mandated timeframe.

Wondering if your situation calls for a professional? We break down the specific scenarios in our detailed guide on if you should hire a public adjuster. It’s a must-read that will help you make the right call when everything is on the line.