Filing an insurance water damage claim should be a straightforward process. You fulfill your end of the bargain by paying premiums month after month, and in return, they are supposed to have your back when disaster strikes. But the reality for many homeowners and business owners is that this process quickly devolves into an exhausting fight against the very company you trusted to protect your property.

Let’s be brutally honest: Your insurer’s primary goal isn’t your recovery. It’s protecting their profits.

Why Your Insurer Is Not on Your Side

Finding water gushing through your property is a gut-wrenching experience. The real shock, though, often comes later when you realize your insurance company—whether it’s State Farm, Allstate, or any other big name—is becoming your biggest problem.

This isn’t just a string of bad luck. It’s a conflict of interest baked right into their business model. Every single dollar they pay out on your claim is one less dollar of profit for them.

This financial reality creates a system built on three things: delay, deny, and underpay. The adjuster they send out might seem friendly, but their job isn’t to help you. Their job is to find reasons to pay you as little as legally possible.

The Adjuster Works for Them, Not You

The insurance company’s adjuster is a trained professional. They are experts at interpreting your policy in the most restrictive way possible to benefit their employer.

They will hunt for exclusions, question the origin of the water, and pick apart every single item on your list of damages. It’s a systematic process designed to shut down your claim from the moment they walk through your door.

You’ll hear them use confusing insurance jargon or point to an obscure clause in your policy to justify a laughably low offer. A classic move is to claim the damage is from “long-term seepage” instead of a “sudden and accidental” leak—a common excuse used by companies like State Farm to deny coverage entirely. It’s this adversarial game that leaves so many homeowners and business owners feeling completely betrayed after a disaster.

A System Designed for Underpayment

For insurance carriers, water damage is a massive and expensive problem. In fact, industry data shows water damage and freezing accounted for about 43.21% of all home insurance claims in 2024. It’s one of their biggest expenses.

To control those costs, they’ve created internal playbooks that push adjusters toward limiting payouts. It’s not personal; it’s just business.

Here’s how this strategy usually plays out for you:

- Calculated Delays: Those slow email responses and constant requests for more paperwork aren’t just bad service. They’re often a deliberate strategy to wear you down until you’re so frustrated and exhausted that you’ll accept any offer they throw at you just to make it stop.

- Lowball Offers: The first offer is almost never their best one. They are banking on you being desperate, uninformed, and willing to accept a fraction of what you’re actually owed just to get a check in your hand.

- Intimidating Tactics: For bigger, more complex claims, they might get aggressive. You could be hit with intense questioning or even a demand for a formal, recorded statement. Before you ever agree to that, you need to understand what an Examination Under Oath entails before you agree to one.

At the end of the day, getting this one thing straight is the most important step you can take: you are in a fight for what you’re rightfully owed. Your insurer has a whole team of experts working to protect their money. You need an expert on your side to protect yours.

How to Build an Ironclad Case for Your Claim

The second your insurance company gets the call about your water damage, their team starts building a case—against you. Their only objective is to find any reason, real or imagined, to pay you as little as possible. To fight back, you need to build a stronger, more detailed case for yourself, starting immediately.

This isn’t about snapping a few quick photos on your phone. It’s about creating a mountain of undeniable evidence that leaves no room for your insurer to argue. They want to control the narrative, but a powerful evidence log puts you in charge.

Master the Art of Visual Documentation

Photographs and videos are your most powerful tools, but how you use them makes all the difference. Your goal here is to tell a complete story of the damage, from its origin to its full impact, that an adjuster sitting in a cubicle hundreds of miles away simply can’t dispute.

- Create a Video Walkthrough: Before one thing is moved or cleaned up, record a slow, detailed video of the entire affected area. Make sure to narrate what you’re seeing, stating the date and time out loud. Show where the water came from, the path it took, and every single wet or damaged item.

- Timestamp Everything: Use a timestamp app on your phone for all your photos. This creates an official record of when the damage was documented, and it stops the insurer from later claiming the damage got worse over time because you were negligent.

- Capture the Unseen Damage: Don’t just focus on the obvious puddles. Get close-up shots of water lines on drywall, swollen baseboards, warped cabinet bottoms, and any moisture bubbling under the flooring. These are the subtle details where insurers love to cut corners on payouts.

The Game-Changing Power of Independent Moisture Readings

Here’s a tactic that insurance companies like State Farm absolutely hate: get your own evidence before their adjuster ever sets foot on your property. The adjuster will show up with a moisture meter and act like they are the sole authority on what’s wet and what isn’t. You have to beat them to it.

Hire your own trusted, IICRC-certified water mitigation company to perform a comprehensive moisture inspection right away. Their report, complete with professional moisture readings and thermal imaging, creates an independent, third-party baseline of the damage.

When the insurance adjuster arrives and claims a wall is “mostly dry,” you can present your expert’s report showing it was completely saturated 48 hours earlier. This simple step shuts down one of their most common tactics for minimizing the scope of repairs.

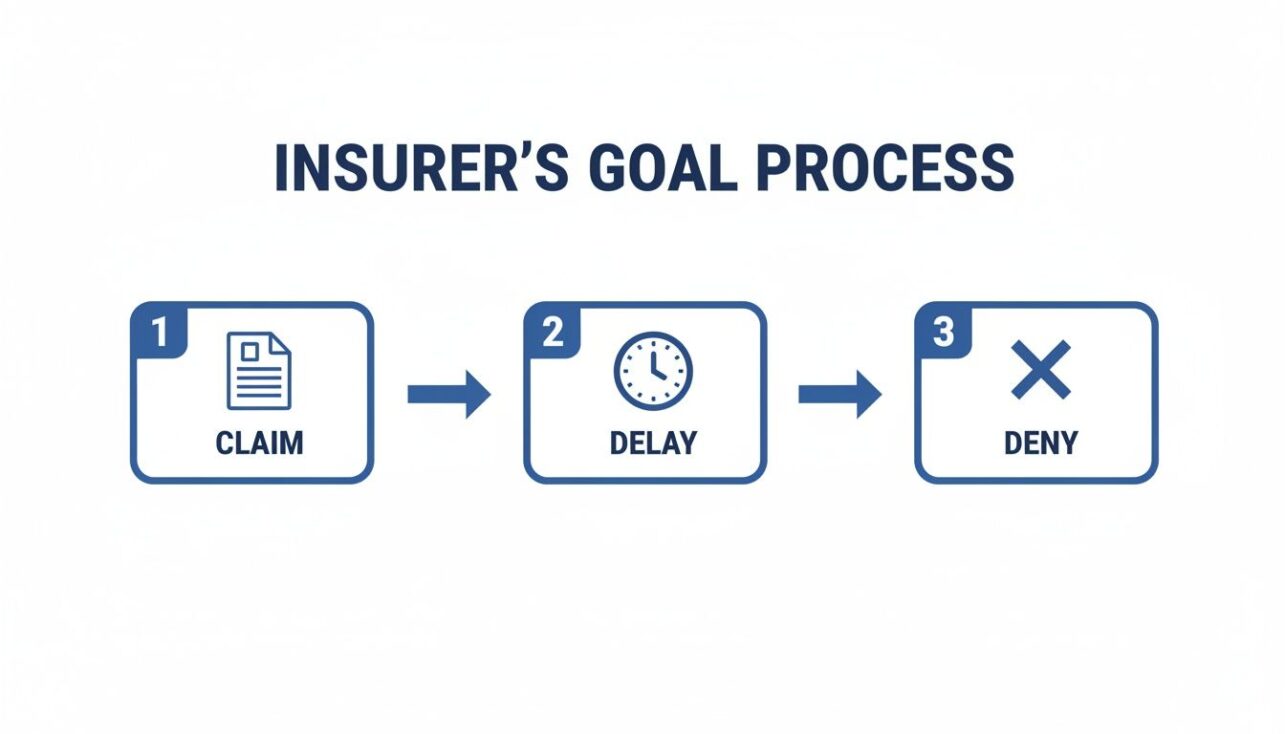

This entire process is just part of the standard insurance company playbook, which is almost always designed to work against you.

This simple flow—Claim, Delay, Deny—is the exact strategy they use to wear you down until you accept a lowball offer out of sheer exhaustion.

Create an Exhaustive Inventory of Damaged Property

An adjuster will not spend the time to carefully inventory every single item you lost. They’ll glance around, throw out a lowball estimate for “contents,” and move on to their next appointment. It’s on you to create a detailed list they cannot ignore.

For every single damaged item, you need to document the following:

- Item Description: Be specific (e.g., “Samsung 55-inch 4K Smart TV,” not just “TV”).

- Make and Model Number: This is absolutely critical for accurate pricing.

- Age and Purchase Date: Dig up receipts or credit card statements if you can.

- Original Cost and Estimated Replacement Cost: Research what it would cost to buy the item new today.

This detailed inventory becomes a crucial part of your Proof of Loss form, a sworn statement of the facts about your claim that the insurer requires. For a deeper understanding of how to correctly complete this document, you can learn more about the formal Proof of Loss requirements in our detailed guide.

A key piece of building a strong claim is showing you took immediate and effective action. Learning how to go about drying wet carpet fast and preventing mold is a perfect example of this. Your meticulous records prove you took every necessary step to protect your property, which can prevent them from blaming you for escalating damages.

Decoding Your Policy to Counter Insurer Tactics

Let’s get one thing straight: your insurance policy isn’t a friendly guide. It’s a legal contract, meticulously crafted by armies of lawyers to protect the insurer’s bottom line.

Companies like State Farm and Allstate intentionally load these documents with confusing jargon, ambiguous clauses, and a maze of exclusions. This isn’t by accident. It’s designed to give them the upper hand the moment you file an insurance water damage claim. Understanding how to dissect this document isn’t just helpful—it’s your primary weapon against their lowball tactics.

Your insurer sees the policy as a rulebook they can interpret however they want. You need to see it for what it is: the contract they are legally bound to, and use their own words to dismantle their arguments and get them to pay what they owe.

The “Sudden and Accidental” Trap

One of the first battlegrounds in any water damage claim is the “sudden and accidental” clause. Insurers absolutely love this phrase. Why? It’s just vague enough to be twisted to their advantage. They’ll try to argue that any damage not caused by a single, spectacular event—like a pipe exploding—is simply not covered.

Their adjuster will hunt for any sign of a slow leak, a bit of rust, or a worn-out seal. The moment they find one, they’ll label the cause “long-term seepage” or “failure due to wear and tear.” These are just code words for denial.

But here’s the thing: your policy defines those terms, and you must hold them to their own definition. If a supply line under your sink suddenly let go, that is the “sudden and accidental” event. The fact that the fitting might have been slowly corroding for years is often completely irrelevant. The failure itself was abrupt. That’s what triggers coverage.

Spotting Your Coverage in a Sea of Exclusions

Insurance policies are notoriously heavy on exclusions. In fact, adjusters are trained to start their investigation by looking for every possible reason not to cover your loss. Your job is to flip that script. Find the specific language that confirms your coverage and build your entire case around it.

Don’t get lost in the endless pages of things that aren’t covered. Go straight for the core insuring agreement for water damage. It will typically grant broad coverage for direct physical loss from water, and then list the exceptions.

A powerful strategy is to find the exact sentence that covers your situation and make it the cornerstone of every communication. If your policy covers “accidental discharge or overflow of water… from within a plumbing… system,” and your dishwasher line broke, you will repeat that precise language in every email, letter, and phone call.

This forces the adjuster to argue against the exact text of the contract they wrote and sold you. It immediately puts them on the defensive.

Anticipating the Denial Excuses

Big insurance companies don’t invent new excuses for every claim. They use a well-worn playbook of common tactics to deny or underpay claims, especially for water damage. If you understand these tactics in advance, you can prepare your counter-arguments before the adjuster even picks up the phone.

A revealing California court case, Tong v. State Farm, provided a rare glimpse into this playbook. The insurer was forced to produce internal documents showing they used standardized claim denial templates. They trained adjusters to lean heavily on specific exclusions, like a clause for water lines “below the surface of the ground,” even when evidence clearly showed the damage should have been covered.

This tells you everything you need to know. The adjuster isn’t making a unique assessment of your home; they are often just following a script designed to save the company money.

Knowing this, you can anticipate their moves. Here’s a look at their common excuses and how you can fight back.

Common Insurer Excuses vs Your Reality

| Insurer’s Tactic or Excuse | What They Really Mean | Your Strategic Counter-Argument |

|---|---|---|

| “This is long-term seepage, not a sudden event.” | “We found a tiny bit of rust, so we’re denying the whole claim.” | Present dated photos and videos showing the area was dry before the incident, proving the damage was recent and abrupt. |

| “The damage was caused by a lack of maintenance.” | “You should have known this old pipe would fail, so it’s your fault.” | Provide records of any past plumbing work or inspections. Argue that policies are meant to cover unexpected failures, not just brand-new components. |

| “This type of water loss is excluded.” | “We’re hoping you won’t read your policy closely enough to challenge this.” | Cite the exact policy language that grants coverage, putting the burden of proof back on them to show how the exclusion specifically applies. |

By preparing for these arguments with your own documentation and a firm understanding of your policy’s language, you shift the power dynamic. You stop being a victim and start being a prepared opponent they have to take seriously.

Why a Public Adjuster Is Your Best Weapon

After a water disaster, you quickly realize there are two types of adjusters in the world. Only one of them works for you.

First, there’s the company adjuster, sent by your insurer. Their job is to protect their employer’s bottom line. Then there’s a public adjuster—a state-licensed professional you hire to represent your interests and only your interests.

Trying to take on a multi-billion dollar corporation like Allstate or State Farm by yourself isn’t just difficult; it’s an unfair fight from the start. They have armies of lawyers and adjusters whose entire job is to minimize what they pay out on your insurance water damage claim. A public adjuster is the expert in your corner, the equalizer you need to make it a fair fight.

Leveling an Unfair Playing Field

The insurance company’s biggest weapon is information. They know your policy inside and out, they track repair costs down to the penny, and they know every loophole they can use to underpay you. A public adjuster takes that advantage away.

They start by conducting their own exhaustive inspection of your property, documenting every bit of damage—especially the things the company adjuster conveniently overlooks. They understand the real-world costs of materials and labor, stopping the insurer from using outdated pricing or lowball estimates to slash your payout.

Most importantly, a public adjuster takes over all the stressful and time-consuming communications. No more infuriating phone calls or endless email chains designed to wear you down. They manage the entire fight, from filing the paperwork to negotiating the final settlement, freeing you up to focus on putting your life back together. To see just how much they can help, explore the benefits of hiring a public adjuster in our detailed guide.

A Real-World Case Study in Maximizing a Claim

Recently, business owner we worked with on their Raleigh water damage claim after their property was saturated after a main water line burst. Their insurance carrier, a major national brand, sent their adjuster who did a quick walkthrough and came back with a settlement offer of just $87,000.

The owner knew that wouldn’t even begin to cover the repairs and business interruption, so he called us. We immediately brought in engineers and commercial contractors for a proper assessment. We found significant structural damage and hidden moisture the first adjuster had completely missed. After compiling a new evidence package and aggressively renegotiating, the final settlement was $310,000—more than 3.5 times the original offer.

This isn’t a rare occurrence. It’s a perfect example of the value gap. The insurance company’s first offer is never their best; it’s a starting point in a negotiation they hope you’re too overwhelmed to fight.

This proves that having professional representation isn’t a luxury. It’s often a financial necessity if you want to get a fair outcome.

An Investment in a Fair Outcome

Hiring a public adjuster isn’t a cost—it’s an investment. They work on a contingency fee, which means they only get paid a small percentage of the settlement money they recover for you. Their incentive is directly aligned with yours: get the absolute maximum payout from the insurance company.

There has always been a massive gap between the economic losses people suffer and what insurance actually pays out. Aon reported a record-low protection gap of 38% globally in the first half of 2025, but that still means a huge portion of losses go completely uncovered. A public adjuster’s expertise is your best defense against falling into that gap.

They force the insurance company to honor the policy you’ve been paying for. By documenting everything, speaking the insurer’s language, and negotiating from a position of strength, they turn a potential financial disaster into a proper recovery.

How to Escalate the Fight and Win

When your insurance company slams the door with a final “no” or slides a settlement offer across the table that’s just plain insulting, it’s easy to feel cornered. That’s exactly what they want. Big carriers like State Farm and Allstate are betting on your exhaustion and frustration to make you walk away.

But this isn’t the end of the road. This is the moment you stop asking nicely and start escalating the fight for your insurance water damage claim. There are powerful, formal processes designed specifically to challenge their decisions and hold them accountable for their tactics.

Invoke Your Right to Appraisal

Buried deep in the fine print of your policy is a powerful clause most homeowners never even know exists: the Appraisal Provision. This is your relief from dealing with the carrier adjuster when the argument is purely about the cost of the repairs, not whether the damage is covered in the first place.

Let’s say the insurer agrees that the burst pipe is a covered loss. But they’re offering you $15,000 while your contractor’s estimate is a solid $45,000. That’s not a coverage dispute; it’s a valuation dispute. The appraisal process is your right, and it’s how you resolve it.

Here’s how it works:

- You hire your own appraiser. This needs to be an unbiased, seasoned expert—often a public adjuster or a contractor who lives and breathes insurance disputes.

- The insurance company hires their appraiser. You can bet they’ll pick someone who shares their perspective on keeping costs down.

- The two appraisers select a neutral “umpire.” If they can’t agree on who to pick, a court will step in and appoint one.

- Both sides make their case. The appraisers dig into the evidence—estimates, photos, reports—and try to agree on the real cost of repairs.

- The umpire makes the final call. If the two appraisers are at a stalemate, the umpire reviews both positions and makes a binding decision. An agreement between any two of the three parties sets the final claim amount, and it’s over.

Invoking appraisal yanks the decision-making power away from the insurance company and places it in the hands of a more neutral panel. It forces them to actually defend their lowball number against a real industry pro.

File a Complaint with the Department of Insurance

Every state has a Department of Insurance (DOI) that acts as a watchdog, regulating insurers and protecting consumers like you. Filing a formal complaint is a free, simple, and surprisingly effective way to put regulatory heat on your carrier.

Insurance companies absolutely hate dealing with the DOI. A complaint creates a paper trail of their bad behavior and can trigger a formal investigation. While the DOI won’t cut you a check directly, a call from a state regulator asking pointed questions has a funny way of making a stubborn adjuster suddenly see reason.

Make your complaint sharp, clear, and packed with evidence. Include your policy number, claim number, and a clean timeline of events. Attach everything: your photos, contractor estimates, and the log of every single frustrating phone call. Show them you have a rock-solid case and the insurer is simply refusing to play fair.

When to Bring in a Bad Faith Attorney

Sometimes, an insurer’s behavior goes beyond a simple disagreement over money. It crosses a line into what the law calls “bad faith.” This is a serious legal term for when an insurance company blatantly violates its contractual duty to treat you fairly and honestly.

What does bad faith look like?

- Endless, unreasonable delays in handling your claim.

- Denying the claim without even doing a proper investigation.

- Twisting the language in your own policy to weasel out of paying.

- Refusing to offer a fair settlement when it’s crystal clear they are liable.

A revealing court case, Tong v. State Farm, showed just how far this can go. The company denied a homeowner’s claim for a burst pipe, hiding behind a bogus exclusion. It wasn’t until the homeowner sued and put the adjusters under oath that State Farm caved and paid $274,000. That delay and the need for a lawsuit became the foundation for a separate, successful bad faith claim.

If you even suspect your insurer is acting in bad faith, it’s time to talk to an attorney who specializes in these fights. They can sue not just for the money you were owed in the first place, but also for punitive damages—extra money designed to punish the insurance company for its malicious conduct. Often, these damages can be far more than the value of your original water damage claim.

The Tough Questions About Disputed Water Damage Claims

When you’re fighting an insurance company over water damage, you’re going to have a lot of questions. That’s normal. In fact, your insurer is counting on your uncertainty to keep them in the driver’s seat.

Getting straight answers is how you take back control.

How Much Does a Public Adjuster Cost?

This is usually the first thing people ask. They’re already facing a huge, unexpected expense and the thought of another bill is overwhelming.

The answer is simple: Zero upfront.

Public adjusters don’t charge you a dime out of pocket. We work on a contingency fee. That means our fee is a small, agreed-upon percentage of the final settlement we win for you from your insurance company.

If we don’t get you paid, we don’t get paid. Period. Our interests are perfectly aligned with yours—the bigger your settlement, the better it is for both of us. Think of it as an investment in a much better outcome, not another expense.

Can My Insurer Cancel My Policy if I Fight Back?

It’s a common fear. You worry that if you push back against a lowball offer, the insurance company will get angry and just cancel your policy in retaliation.

Let’s be crystal clear: That is illegal.

State insurance regulations strictly prohibit an insurer from canceling your policy mid-term just because you filed a legitimate claim or disputed their offer. You are simply exercising the rights laid out in your contract. They can’t punish you for that.

Now, there’s a difference between cancellation and non-renewal. They can’t drop you in the middle of a policy term for fighting a claim, but they can choose not to renew your policy when it expires. It’s a dirty tactic some carriers use, but it doesn’t change your right to get every dollar you’re owed on your current claim.

What’s the Difference Between Mitigation and Repairs?

Insurance adjusters absolutely love to blur the lines between these two things to slash your payout. Knowing the difference is your first line of defense.

- Mitigation: This is the emergency response. It’s everything done to stop the water damage from spreading. Think water extraction, tearing out soaked carpet and drywall, and setting up massive fans and dehumidifiers.

- Repairs: This is the rebuild. It’s the work required to put your property back to the way it was before the disaster. We’re talking new floors, fresh drywall, painting, replacing cabinets, and fixing whatever pipe or appliance caused the mess in the first place.

A favorite trick of adjusters, especially from companies like Allstate, is to pay the mitigation company’s bill and then act like the claim is closed. They’ll send a check for the cleanup and hope you think that’s all you get. Don’t fall for it. Your policy covers both mitigation and the full cost of repairs.

The average water damage claim payout is around $13,954 for a reason—it’s supposed to cover the whole job, not just the initial cleanup.

What if the Adjuster Blames a “Slow Leak”?

This is the number one excuse insurance companies use to deny water damage claims. The adjuster will poke around, find a little bit of rust on a pipe fitting, and declare the whole disaster is due to “long-term seepage” or “poor maintenance”—which, conveniently for them, isn’t covered.

This is a deliberate and cynical misreading of your policy.

The trigger for coverage is the “sudden and accidental” discharge of water. The fact that a part was aging doesn’t matter. The moment it finally failed and unleashed water into your home was the sudden and accidental event. Your detailed photos and videos are your best weapon here, especially if you can show the area was perfectly fine before the incident.

2. What specialized tools do PAs use to document "Hidden" water damage that insurance adjusters often overlook?

Insurance adjusters typically only scope the visible damage. Our expertise is finding the damage that extends deep into the structure, which dramatically increases the claim value. The core technology we rely on is thermal imaging and moisture mapping.

Thermal Imaging (Infrared Cameras): This technology detects temperature differences within walls, ceilings, and floors. Water-damaged areas often have a lower surface temperature due to evaporation, making them appear as distinct color differentials on the thermal image. This proves the extent of moisture migration that is completely invisible to the naked eye.

Moisture Meters: We use non-penetrating and penetrating moisture meters to create a Moisture Map. This map provides objective, quantifiable readings of water saturation levels within building materials (e.g., drywall, wood framing). This documentation is essential for justifying the full scope of necessary drying, demolition, and mold prevention protocols (IICRC S500 standards).

3. How do Public Adjusters maximize coverage when my policy has a $5,000 (or low) mold remediation sub-limit?

Most homeowners policies include a specific sub-limit for mold remediation, often capped at a low amount (e.g., $5,000 or $10,000). A professional approach is essential to avoid using that sub-limit prematurely.

The Allocation Strategy: Mold coverage generally falls into two buckets: a) Mold that resulted from a covered peril (e.g., a burst pipe) and b) Mold that is unrelated to a covered peril (e.g., from long-term humidity). A PA fights to have the costs related to tear-out and replacement of water-damaged materials (like sheetrock and wood) paid for under the standard Dwelling Coverage limit, which is much higher.

Defining Remediation: We argue that the mold sub-limit should only apply to specialized mold treatment and air scrubbing, not the removal and replacement of the structure itself.

Proving Timeframe: We secure reports from industrial hygienists to confirm the mold growth was directly related to the covered, sudden water event, not a long-term issue.

4. Does my homeowner's policy cover the cost to repair the broken pipe or the appliance that caused the water damage?

This is a critical distinction in water claims:

Damage is Covered: Standard homeowners insurance (HO-3) policies are designed to cover the resulting damage to the structure and contents caused by the sudden discharge of water (e.g., the ruined flooring, ceiling, and walls).

Source is Not Covered: Generally, the policy does not cover the cost to repair or replace the failed system itself—the broken pipe, the faulty hot water heater, or the washing machine. This is considered maintenance or wear and tear.

5. Why is my carrier saying my emergency "water mitigation" costs are unreasonably high?

Emergency mitigation (drying, water extraction, debris removal) is typically the first and most expensive step. Carriers frequently challenge these costs, claiming the scope or pricing was excessive.

PA Due Diligence: We establish that the policyholder has a contractual "duty to mitigate" the loss, meaning they must take reasonable steps to prevent further damage (like mold growth). Failure to do so can lead to a full claim denial.

The Xactimate Advantage: We ensure the mitigation contractor's invoices are created using Xactimate, the same standardized estimating software used by insurance carriers. We cross-reference the line-item codes to guarantee industry-standard pricing. If the carrier attempts to unilaterally reduce the hourly rate or drying equipment rentals, we formally dispute it with clear market data.

6. What is the difference between "Clean Water" (Category 1) and "Black Water" (Category 3), and how does it affect my claim value?

Water is categorized based on its source and contamination level (IICRC S500 standard). This categorization dramatically impacts the scope of demolition and the overall claim value.

| Water Category | Contamination Level | PA Claim Impact |

| Category 1 (Clean Water) | Source is clean (e.g., burst pipe, supply line). | Materials may be salvable. Drying and disinfection may be sufficient for non-porous materials. |

| Category 2 (Gray Water) | Some contaminants (e.g., dishwasher overflow, toilet overflow without feces). | Porous materials (carpet pad, drywall) are non-salvable. Requires full removal/disposal and advanced disinfection. |

| Category 3 (Black Water) | Highly contaminated (e.g., sewage backup, floodwater from the ground). | All porous materials must be removed and disposed of. Requires intensive structural decontamination, sometimes called sub-surface decontamination. |

7. If my claim is denied due to "Sump Pump Failure" or "Sewer Backup," can a Public Adjuster get it covered?

Damage caused by water entering the home from outside or below the foundation (e.g., sewer, drain, sump pump failure) is typically excluded from standard HO-3 policies.

The Endorsement Check: The first step is determining if the policyholder purchased a specific Water Backup and Sump Overflow Endorsement. If this endorsement exists, the PA ensures the carrier applies the coverage correctly, even if the limit is subject to a sub-limit (e.g., $10,000).

The "Cause" Dispute: If the water came from a clogged toilet drain within the home (above the main sewer line), we may argue that it was a sudden plumbing system failure covered by the main policy, not an excluded "sewer backup."

8. My insurance company is only offering Actual Cash Value (ACV). How does a PA secure the full Replacement Cost Value (RCV)?

Policies are either written as ACV (Replacement Cost minus Depreciation) or RCV (Full cost to replace the item). Most homeowners policies offer RCV coverage, but the carrier first pays the ACV amount.

The Depreciation Holdback: Carriers withhold the recoverable depreciation (the difference between ACV and RCV) until the policyholder provides proof that the repairs have been completed.

The PA's Role: We submit a finalized, expert-level scope and estimate (using Xactimate) to the carrier that details the true, pre-loss RCV. This ensures the initial ACV payment is maximized. More importantly, we stick with you during during your repair process and the final documentation (contractor invoices, lien waivers) to secure the final depreciation holdback check quickly and efficiently.

9. What is "Bad Faith" in a water damage claim, and what is the Public Adjuster's legal leverage?

Bad Faith occurs when an insurance carrier unreasonably delays, low-balls, or denies a legitimate claim without proper investigation or justification.

PA as the Shield: When a PA is retained, all communication and negotiations are handled by us. This formal representation immediately signals to the carrier that the policyholder is informed and prepared for litigation if necessary.

Leveraging Evidence: The PA's comprehensive claim package (thermal imaging, detailed Xactimate scope, microbial reports) leaves no room for the carrier to argue they lack sufficient information. A denial or low-ball offer against this evidence becomes much harder to defend as being made in "good faith."

10. Can a claim cover the cost of upgrading my plumbing system to prevent future water damage?

Generally, no. Policies do not pay for betterments, preventative maintenance, or upgrades (e.g., replacing old copper pipes with PEX).

Code Compliance Loophole: We check for Ordinance or Law coverage. If the water damage is extensive enough that local building codes now require the entire plumbing system to be brought up to current code during the repair, this coverage may apply, potentially paying for the upgrade of undamaged pipes adjacent to the repair area.

11. How does a PA ensure correct pricing for repairs in a volatile, post-disaster construction market?

Insurance estimates rely on a static pricing database (Xactimate). However, after a major area-wide disaster, costs for labor, materials, and specialized equipment (like dehumidifiers) spike due to high demand.

Surcharges and Market Conditions: A PA does not blindly accept the default Xactimate pricing. We apply justifiable surcharges, such as General Contractor Overhead and Profit (GCOP), and specialized Demand Surcharges to account for the actual, inflated costs contractors face in a busy market.

Non-Standard Materials: If the damaged tile or flooring is discontinued, a PA secures quotes for the closest Like Kind and Quality replacement, even if that replacement is significantly more expensive than the original material, forcing the carrier to indemnify the policyholder properly.

12. My water claim is for a rental property. How can a Public Adjuster secure coverage for lost rent?

If a rental property becomes uninhabitable due to a covered water loss, the policyholder can claim Fair Rental Value (FRV) or Loss of Rents coverage (often called Additional Living Expense - ALE or Loss of Use on a primary residence policy).

PA Documentation: We immediately collect the lease agreement, bank records proving rent payment history, and provide local rental market comparisons for similar properties.

The Uninhabitable Clock: The PA ensures the carrier pays for the lost rent for the full duration it takes to make the property habitable again, including the time required for structural drying, demolition, permitting, and reconstruction. This clock often runs much longer than the carrier initially estimates.

You don’t have to accept an unfair denial or a lowball offer. The team at For The Public Adjusters, Inc. fights for policyholders to get the full, fair settlement they are legally owed. Contact us today for a free, no-obligation review of your claim. Learn more and get help now.