When your insurance company denies, delays, or just plain lowballs your claim after a hurricane, you need more than just help—you need a legal enforcer. That's exactly what a hurricane claim lawyer is: a legal professional who steps in to represent you and force your insurer to honor the policy you paid for.

The Battle After the Storm: Why Insurers Don't Pay

The hurricane was just the first fight. For countless homeowners and business owners across North Carolina and Virginia, the real battle begins the second you file a claim. It’s a frustrating, gut-wrenching reality most people are completely unprepared for.

After a major storm, insurance giants like State Farm and Allstate are buried under an avalanche of claims. Their goal shifts instantly from customer service to damage control for their own bottom line. Suddenly, that friendly agent who sold you the policy is nowhere to be found, replaced by an adjuster trained to minimize every single payout.

Common Tactics Insurers Use

If you feel like you're being taken for a ride, you're not alone. It’s not just bad luck; it’s a playbook. Insurance companies rely on predictable tactics designed to wear you down until you accept far less than you deserve.

Common moves include:

- Offensively Low Settlement Offers: Their first offer is almost always a joke—a fraction of what it will actually cost to repair your property. It's a test to see if you'll just take it and go away.

- Confusing Denial Letters: They’ll bury the reason for denial in obscure policy language and complex jargon, betting you won’t have the energy or expertise to fight back.

- Endless Delays: By "needing more paperwork" or dragging out their investigation, they crank up the financial pressure. The goal is to make you so desperate you’ll accept any offer just to get some money in your hands.

This isn’t a fair fight; it’s a business strategy. In recent years, the U.S. has been slammed by 115 billion-dollar weather disasters, with damages piling up to nearly $3 trillion since 1980. When a hurricane hits, claim volumes explode, and adjusters are overwhelmed. This chaos leads directly to systematic underpayments and unfair denials. You can see the staggering financial impact for yourself in NOAA’s research on these costly events.

Think of this guide as your strategic playbook for fighting back. While allies like public adjusters are invaluable for documenting your damage, a hurricane claim lawyer becomes absolutely essential when your insurer digs in its heels and refuses to play by the rules. We’re here to validate your struggle and give you a clear path to taking back control and getting the full settlement you are owed.

Public Adjuster vs. Hurricane Claim Lawyer: Knowing Your Ally

After a hurricane, your first instinct is to get your claim filed and start putting your life back together. But when the insurance company comes back with a ridiculously low offer or an outright denial, you realize you need a pro in your corner.

That’s when the big question hits: Who do you call? A public adjuster or a hurricane claim lawyer?

Choosing the right expert at the right time can make or break your recovery. It’s not about one being “better” than the other. It’s about deploying the right ally for the specific battle you’re facing, because they each play a powerful—and very different—role in the fight for a fair payout.

The Master Builder: Your Public Adjuster

Think of a public adjuster as the master builder of your insurance claim. They are state-licensed professionals who work only for you, the policyholder—never for the insurance company. Their entire job is to meticulously inspect, document, and value every last detail of your property damage.

They construct an undeniable case for what you are truly owed. This isn’t a quick walk-through; it’s a deep dive that includes:

- Forensic Damage Assessment: Going far beyond the surface-level glance you’ll get from the insurance company’s adjuster.

- Policy Deconstruction: Scouring your policy to find every single bit of coverage you're entitled to.

- Ironclad Estimates: Creating a comprehensive, line-by-line estimate of all repair and replacement costs using the same software the insurance companies use.

- Hard-Nosed Negotiation: Taking this bulletproof claim to the insurer and fighting for a full and fair settlement.

A public adjuster is your frontline advocate. They are the expert who proves what your loss is actually worth, ensuring your claim is built on a rock-solid foundation of evidence. To see just how different their job is from the adjuster your carrier sends out, check out our guide on the differences between an insurance adjuster vs a public adjuster.

The Legal Enforcer: Your Hurricane Claim Lawyer

A hurricane claim lawyer, on the other hand, is the legal firepower you bring in when the insurance company sees your perfectly documented claim and still refuses to pay you fairly.

Their job isn't to put a price tag on your damage—that’s the public adjuster's territory. Their job is to hold the insurance company legally accountable when they break the rules of the contract you paid for.

You need a lawyer when the fight shifts from valuation to legal tactics. This is what it looks like when your insurer is:

- Acting in bad faith.

- Issuing a wrongful denial based on a twisted interpretation of your policy.

- Using legal delays and stonewalling to wear you down.

- Refusing to negotiate reasonably, even when faced with overwhelming proof.

A lawyer’s primary weapon is the law itself. They can file a lawsuit, force the insurance company to turn over internal documents, and drag them into a courtroom to answer for their actions.

Your public adjuster proves the value of your claim. Your hurricane claim lawyer enforces your right to collect it when the insurer breaks the law.

To really nail down the distinction, this table breaks down their unique roles in your fight.

Public Adjuster vs. Hurricane Claim Lawyer Key Differences

| Area of Focus | Public Adjuster | Hurricane Claim Lawyer |

|---|---|---|

| Primary Function | To document, value, and negotiate the financial total of the property damage claim. | To litigate and enforce the policyholder's legal rights against the insurance company. |

| When to Hire | At the beginning of a claim, especially if it's large, complex, or you've received a low offer. | When the insurer denies the claim, acts in bad faith, or refuses a fair settlement after negotiation. |

| Core Skills | Damage assessment, construction estimating, policy analysis, and claim negotiation. | Legal strategy, litigation, knowledge of insurance law, and courtroom advocacy. |

| End Goal | Secure the maximum possible settlement through negotiation and documentation. | Win a legal judgment or force a settlement through legal pressure, often including damages for bad faith. |

Understanding these roles is the first step. A public adjuster builds the case, and a lawyer brings the hammer down when the carrier refuses to listen to reason. Together, they create a powerful one-two punch for policyholders.

Recognizing Bad Faith: When It's Time to Call a Lawyer

After a hurricane, a little back-and-forth with your insurance company is normal. But there’s a massive difference between a tough negotiation and an insurer breaking the law. When they cross that line, they’re acting in bad faith, and that’s your cue to stop talking to them and start talking to an attorney.

Knowing how to spot bad faith is everything. It’s the sign that you’re no longer in a simple dispute over repair costs; you’re in a fight against a company that has decided its profits are more important than its legal duty to you. Insurers like State Farm and Allstate have playbooks filled with tactics that feel like simple frustration but are actually calculated strategies to wear you down.

The Tell-Tale Signs of Bad Faith

Bad faith isn't just about a low offer. It's a pattern of dishonest, unfair, and deceptive behavior designed to avoid paying what they rightfully owe on your claim. If you're seeing these red flags, your insurer is likely breaking the law.

Watch out for these classic moves:

- Unreasonable Delays Without Explanation: The adjuster keeps asking for the same documents you've already sent, or they just go silent for weeks on end. They're hoping the financial pressure of being out of your home will force you to accept whatever scraps they eventually offer.

- Twisting Your Policy Language: They deny the claim by pointing to some obscure exclusion or interpreting a clause in a way that makes no sense. They're betting you won't have the energy or expertise to challenge their "official" reading of the contract.

- Failing to Do a Real Investigation: The adjuster shows up, walks around your heavily damaged property for 15 minutes, barely looks at the roof, and then writes a report based on a quick glance. This isn't an investigation; it's a justification for a denial.

- Lowballing With No Justification: You get an offer that doesn't even come close to your contractor's estimate, but the insurer provides zero evidence or detailed reasoning to back up their ridiculously low number.

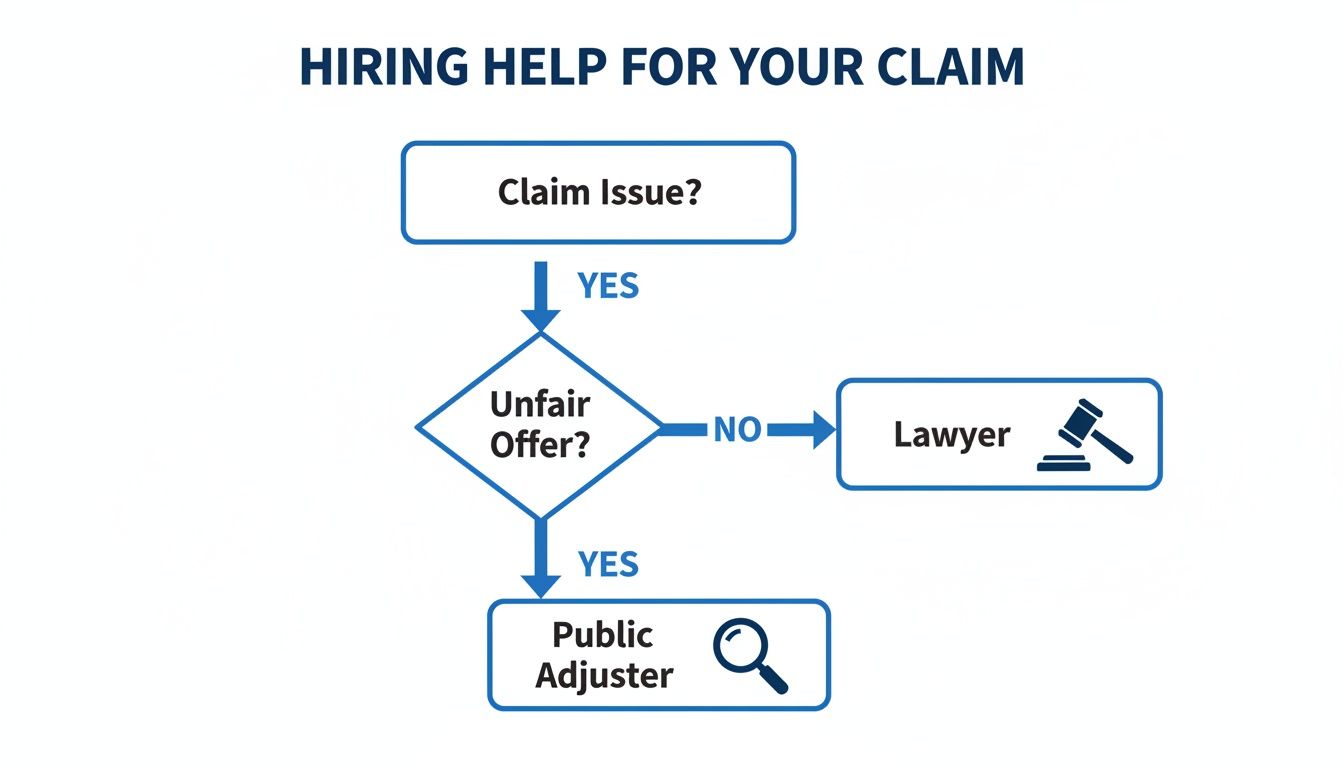

This decision tree can help you see when you need to bring in the heavy artillery of a lawyer versus a public adjuster.

As you can see, a public adjuster is your best ally when you're fighting an unfair offer. But when the insurance company flat-out refuses to cooperate or acts illegally, you need a lawyer.

Why Bad Faith Tactics Are on the Rise

Let's be clear: insurance companies are under tremendous pressure. The global industry is getting hammered by natural catastrophe losses, which recently hit a staggering USD 137 billion. As storms get stronger and more frequent, insurers get more desperate to protect their bottom line by any means necessary—including illegal denials and delays. This reality makes having an expert advocate on your side more critical than ever. You can discover more insights about these insurance industry trends and see for yourself how the game is changing.

But their financial problems don't give them a free pass to break the law. An insurance policy is a contract, and both sides have to act fairly. When your insurer refuses, a lawsuit isn't just an option—it's your right.

A bad faith lawsuit isn’t just about getting the money for your repairs. It’s about holding the insurance company accountable for its illegal behavior, which can lead to additional damages designed to punish them. That is the ultimate leverage a hurricane claim lawyer brings to the fight.

Case Study: A Homeowner Fights Back and Wins

Think about a Virginia Beach homeowner whose roof was shredded by a hurricane. Their insurer, one of the big national brands, denied the claim. The reason? They said the damage was just "wear and tear," not from the storm—a classic, cynical excuse. The homeowner's own roofer confirmed the damage was brand new and absolutely caused by the storm.

Stonewalled and furious, the homeowner hired a hurricane claim lawyer. The lawyer didn't just ask for the claim to be paid; they immediately filed a lawsuit for both the roof repair and bad faith. During the discovery process, they hit the jackpot: internal company emails revealed the adjuster was being pressured by his bosses to deny claims to meet cost-cutting quotas.

Faced with proof of their scheme, the insurance company folded immediately. The homeowner got the full amount for a new roof, plus a significant settlement for the company's fraudulent conduct. This is what happens when you fight back. A lawyer doesn't just get your claim paid; they make the insurance company pay for trying to cheat you in the first place.

Navigating Difficult NFIP Flood Claims

If your hurricane damage includes rising water, you’ve just been thrown into a completely different, more brutal arena. Flood damage isn't covered by your standard homeowner's policy. Instead, you're forced to file a claim with the National Flood Insurance Program (NFIP), a federal program infamous for its soul-crushing red tape and rigid rules.

This means you’re not dealing with a typical insurance company like Allstate or State Farm. You're now up against FEMA and its network of "Write Your Own" (WYO) insurance companies that administer these policies. These companies operate under a completely different set of regulations designed to protect federal funds, not to make you whole.

The adjusters they send are trained to scrutinize every single item and minimize payouts at every turn. They are not on your side. Their primary job is to limit the government's financial exposure.

The NFIP's Unforgiving System

The NFIP claim process is a minefield of unforgiving deadlines and complex paperwork deliberately designed to trip you up. The single most critical document is the Proof of Loss—a sworn statement detailing the exact amount you are claiming. Unlike a standard homeowner’s claim where there might be some wiggle room, an error or a missed deadline on your NFIP Proof of Loss can be fatal to your claim.

Here’s what makes this system so punishing:

- Strict Deadlines: You typically have only 60 days from the date of the flood to submit a fully documented and signed Proof of Loss. That’s an incredibly tight window when you're also dealing with the immediate chaos of a disaster.

- Rigid Documentation: The NFIP demands meticulous, itemized lists of damaged property with receipts, photos, and precise valuations. An adjuster from a WYO company won’t help you create this list; they will only pick apart the one you submit.

- No Bad Faith Claims: Because it's a federal program, you cannot sue the NFIP or its WYO partners for bad faith insurance practices. This strips you of a massive piece of leverage that a hurricane claim lawyer would normally use to hold an insurer accountable.

Why a Public Adjuster Is Your First Line of Defense

In this rigid system, a public adjuster isn't just a good idea—they are practically a necessity. They understand the intricate rules of the NFIP and take over the burden of documenting your loss correctly from day one.

A public adjuster experienced with FEMA and the WYO companies will build your claim to withstand the intense scrutiny it's guaranteed to face. They will meticulously document every detail, prepare the Proof of Loss form with precision, and ensure it’s submitted on time. When the NFIP adjuster arrives with their lowball assessment, your public adjuster will be ready with a detailed, evidence-based counter-argument. You can learn more by reading our comprehensive guide on handling flood damage claims.

The NFIP system is stacked against policyholders. The adjusters are trained to deny and underpay, and the paperwork is designed to be confusing. Fighting them alone is a recipe for financial disaster.

Ultimately, navigating an NFIP claim is less about negotiation and more about compliance. A public adjuster ensures you meet every requirement perfectly, building an ironclad case from the ground up. If the NFIP still refuses to pay what you’re owed after a flawless claim submission, that’s when a hurricane claim lawyer may be needed to file a federal lawsuit and force them to pay the benefits you deserve.

Deadlines in North Carolina and Virginia That Can Kill Your Claim

After a hurricane, your insurance company knows the clock is ticking. And you better believe they’ll use it against you. One of the most powerful weapons they have isn't buried in your policy’s fine print—it's on the calendar. It’s called the statute of limitations.

This is a hard legal deadline for filing a lawsuit against your insurer for breaking their promise to you. If you miss it, your right to sue them is gone. Forever. It doesn’t matter how strong your case is or how badly they cheated you out of your money. The court will toss your case, and the insurance company gets away with it.

Insurers Weaponize the Clock

Don't mistake an insurer's delays for incompetence. It's a calculated strategy. Big carriers like State Farm and Allstate are masters of the stall game, and they know that every day they drag their feet is another day closer to your deadline expiring.

They’ll bury you in endless requests for the same documents you’ve already sent. They’ll go silent for weeks at a time. They’ll order pointless inspections and appraisals. The goal is to make the claim process so exhausting and frustrating that you either give up or—even better for them—run out of time to fight back in court.

Critical State-Specific Deadlines

In North Carolina and Virginia, these deadlines are unforgiving. Knowing them isn’t just important; it’s the difference between getting paid and getting nothing.

- North Carolina: You generally have three years from the date the insurer breached their contract with you. That clock often starts ticking the day they send you a denial or a lowball payment.

- Virginia: The deadline is typically five years for a written contract.

Five years might sound like a long time, but it flies by when you’re stuck in a back-and-forth battle with an adjuster, scrambling for contractor estimates, and trying to manage repairs. A hurricane claim lawyer is there to make sure this critical window doesn't slam shut on you.

Waiting too long is the single biggest mistake a policyholder can make. An insurer’s promise to "re-evaluate" your claim doesn’t stop the clock on your legal rights. Only filing a lawsuit can do that.

Natural catastrophes are generating mind-boggling losses, with one recent nine-month period seeing USD 105 billion in insured damages. You can discover more insights about these massive catastrophe losses on InsuranceJournal.com. When storms create billions in claims, insurers use every tool they have to control their payouts, and delay tactics are at the top of their list. Don't let their stall tactics become your financial ruin. Understanding how long an insurance company has to settle a claim is your first step in fighting back.

How a Public Adjuster Builds Your Lawsuit From Day One

Let's be blunt: the smartest way to win a fight with your insurance company is to prepare for it from the moment the storm passes. Hope for a fair settlement, but always plan for a battle.

This is where hiring a public adjuster first isn't just a good idea—it’s the single most powerful strategic move you can make. Their job isn’t just to get you a decent offer. It’s to build an ironclad, undeniable record of your loss that will stand up in court if it comes to that.

Every single thing they do is meant to build a fortress of evidence around your claim. This groundwork becomes the backbone of any legal action, making the lawyer's job infinitely easier down the road.

Laying the Foundation for a Winning Case

Think of your public adjuster as the lead investigator for your side of the story. They don’t just glance at the damage; they build a comprehensive file that leaves zero room for the insurance company to argue, deny, or twist the facts.

This isn't just a stack of papers. It's a meticulously assembled case file that includes:

- Detailed, Line-Item Estimates: Using the exact same professional software as the insurance carriers, they create a precise scope of work. It details the cost of every nail, every shingle, and every hour of labor needed to put your property back together.

- Exhaustive Photo and Video Evidence: They document every square inch of the damage. This creates a visual record that proves the extent of your loss far more powerfully than words on a page ever could.

- Expert Reports and Consultations: If your insurer tries to play games, the PA brings in the heavy hitters. They’ll hire structural engineers, roofing consultants, or moisture-mapping experts to provide third-party validation that shuts down any bogus arguments from the carrier.

This complete claim file is more than just paperwork; it’s ammunition. It’s a carefully crafted case that proves exactly what you are owed and why. This level of professional preparation sends a clear message to the insurance company: you are serious, and you will not be pushed around.

The Perfect Handoff to a Hurricane Claim Lawyer

So, what happens if your insurance company, staring at this mountain of undeniable proof, still refuses to do the right thing? The fight isn't over. It just escalates.

This is the moment your public adjuster hands their perfectly prepared file over to an experienced hurricane claim lawyer.

For the lawyer, this is a dream scenario. They don't have to start from scratch, trying to piece together evidence months after the storm when memories have faded and proof has been lost. Instead, they get a case that is already organized, documented, and ready for war. It lets them go on the offensive immediately, often by filing a powerful bad faith lawsuit.

Success Story: The One-Two Punch in Action

Think about a business owner in North Carolina whose commercial building was torn apart by hurricane winds. Their insurer, a huge national company, sent out an adjuster who came back with a ridiculously low offer. It wouldn't even cover half the cost of a new roof, let alone the massive interior water damage.

The owner knew they were being played, so they hired a public adjuster. The PA spent weeks documenting everything. They brought in an industrial hygienist to prove the extent of the water intrusion and a commercial roofing consultant to detail every bit of wind damage. They put together a comprehensive claim package worth nearly triple the insurance company's pathetic offer. Still, the insurer refused to budge.

That’s when the public adjuster referred the case to a hurricane claim lawyer. Armed with that airtight file, the lawyer didn't just sue for the claim amount—they sued for bad faith and unfair and deceptive trade practices.

Faced with irrefutable evidence and the very real threat of getting hammered with punitive damages, the insurance company’s lawyers quickly advised them to settle. The business owner got the full amount of their claim, plus significant additional damages, and never had to step foot in a courtroom.

That victory wasn't just won by the lawyer. It was secured from day one by the public adjuster who laid all the groundwork. It's proof that making the right first move is what paves the way for winning the entire fight.

Common Questions About Hurricane Insurance Disputes

When a storm wrecks your property, the last thing you need is a fight with your insurance company. But it happens all the time. The confusion and frustration can feel as overwhelming as the hurricane itself. Getting straight answers is the first step to taking back control. Here are the questions we hear most often from property owners who are getting the runaround.

Can I Reopen a Claim My Insurer Already Closed?

Yes. Let's be very clear about this: you absolutely can. Maybe you took that first check because you were desperate, only to find out it doesn't even cover half the damage. Or maybe you discovered new cracks in the foundation weeks later that weren't visible before. This is what a supplemental claim is for.

Of course, the insurance company will make it sound impossible. They are banking on you giving up and accepting their first lowball offer as the final word. This is where a public adjuster becomes your most powerful asset. They will meticulously document all the new or undervalued damage, build an ironclad case, and force the insurer to reopen the file and pay what you're actually owed.

What if My Mortgage Company Is Holding the Insurance Money?

This is one of the most maddening situations a homeowner can face. Because the bank has a financial stake in your property, the insurance check often comes with both your name and your mortgage lender's name on it. The lender then puts the money in an escrow account and doles it out in pieces as you complete repairs.

The problem? Many mortgage companies are slow, bureaucratic nightmares. They lose paperwork and create endless delays that bring your repairs to a screeching halt. If your lender is holding your money hostage with red tape, a hurricane claim lawyer can step in. They know how to apply legal pressure to force the bank to release the funds according to state law and your mortgage agreement, getting your recovery back on track.

Do I Have to Accept the Contractor My Insurer Recommends?

Not a chance. Your insurer might push a "preferred" contractor on you, but you need to be extremely cautious. These contractors get a steady stream of business from the insurance company, and their loyalty is often to the carrier, not to you. Their goal is to do the job as cheaply as possible to keep the insurer happy, not to properly restore your home.

You have the absolute right to choose your own licensed and insured contractor. A good public adjuster will have a network of trusted, independent contractors who work for you, not the insurance company.

When Is It Too Late to Get Help?

The biggest mistake you can make is thinking you have plenty of time. Every state has a strict statute of limitations—a hard deadline for filing a lawsuit against an insurance company. For example, in North Carolina, it's typically three years, and in Virginia, it's often five.

But here's the trap: your policy may have clauses that shorten that window even more. The insurance company knows these deadlines down to the day and will use every delay tactic in the book to run out the clock on your right to sue. The second you feel your claim is being delayed, underpaid, or unfairly denied, you need to call a public adjuster or a hurricane claim lawyer. Waiting is the single most expensive mistake you can make.

When you're facing a difficult hurricane claim, you don't have to fight alone. The team at For The Public Adjusters, Inc. provides expert, no-cost claim reviews to help you understand your rights and secure the full settlement you are owed. Visit us online to get the help you deserve.