The check shows up. You open it. Your house still smells like smoke, the drywall is swelling from trapped moisture, or your roof is still exposed after a storm, and the insurance company sends an amount that doesn't come close to putting the property back together.

That's the moment many homeowners and business owners first learn what actual cash value in insurance really means. Not from the policy sale. Not from the nice promises at renewal. From a low payment and a weak explanation.

Insurers love ACV because it gives them a clean-sounding label for paying less. They'll say they accounted for age, wear, and condition. What they usually mean is this: they found a way to shrink the claim by loading depreciation into the estimate. If your loss includes wet walls, damaged ceilings, flooring, cabinets, roofing, or business contents, ACV is often where the fight starts.

Table of Contents

- The Low-Ball Check Has Arrived What Is Actual Cash Value

- Replacement Cost Minus Depreciation The Insurer's Formula for Profit

- ACV vs Replacement Cost The Financial Gap That Insurers Won't Explain

- How Insurers Weaponize Depreciation to Deny Fair Payment

- Special ACV Hurdles NC VA Rules and NFIP Flood Claims

- Your Battle Plan to Dispute a Lowball ACV Settlement

- Don't Fight Them Alone How a Public Adjuster Wins the ACV Battle

The Low-Ball Check Has Arrived What Is Actual Cash Value

A lot of people think insurance is supposed to pay what it takes to repair the damage. That assumption dies fast when the carrier sends an estimate packed with depreciation and labels the payment actual cash value.

The North Carolina Department of Insurance definition, quoted by the NAIC, is blunt. ACV is “the amount of money needed to fix your home, minus the decrease in value of your property because of age or use,” while replacement cost coverage pays what's needed to repair or replace at today's prices, as explained in the NAIC discussion of ACV versus replacement cost coverage. That's the whole game. The company starts with a repair number, then cuts it down.

If you've got water damage, this gets ugly fast. A leak behind a wall can ruin insulation, framing, paint, flooring, and ceilings before the insurer even finishes its first inspection. If you're dealing with hidden wall damage, this breakdown of drywall damage from water issues is worth reviewing because it shows how much loss can sit behind a surface that an adjuster may treat like a simple patch job.

Why policyholders get blindsided

Policyholders often don't read the loss settlement language until after a fire, storm, or plumbing failure. By then, the carrier has already framed the dispute.

They don't call it a cut. They call it depreciation. They don't say you're being left short. They say they applied policy terms. Same result.

Practical rule: If your payment doesn't cover real repair pricing, assume the ACV calculation deserves scrutiny before you cash the check and move on.

Where the pressure shows up

You'll usually see the pain in places like these:

- Roof claims: Older shingles become an excuse for aggressive depreciation.

- Water losses: Cabinets, flooring, drywall, trim, and paint get treated as if age matters more than actual condition.

- Fire claims: Smoke cleanup, finishes, and contents often get devalued hard.

- Business property losses: Fixtures, shelving, equipment, and inventory support items may be reduced with little explanation.

ACV isn't just a definition in a booklet. It's the mechanism insurers use to make you absorb part of the loss yourself.

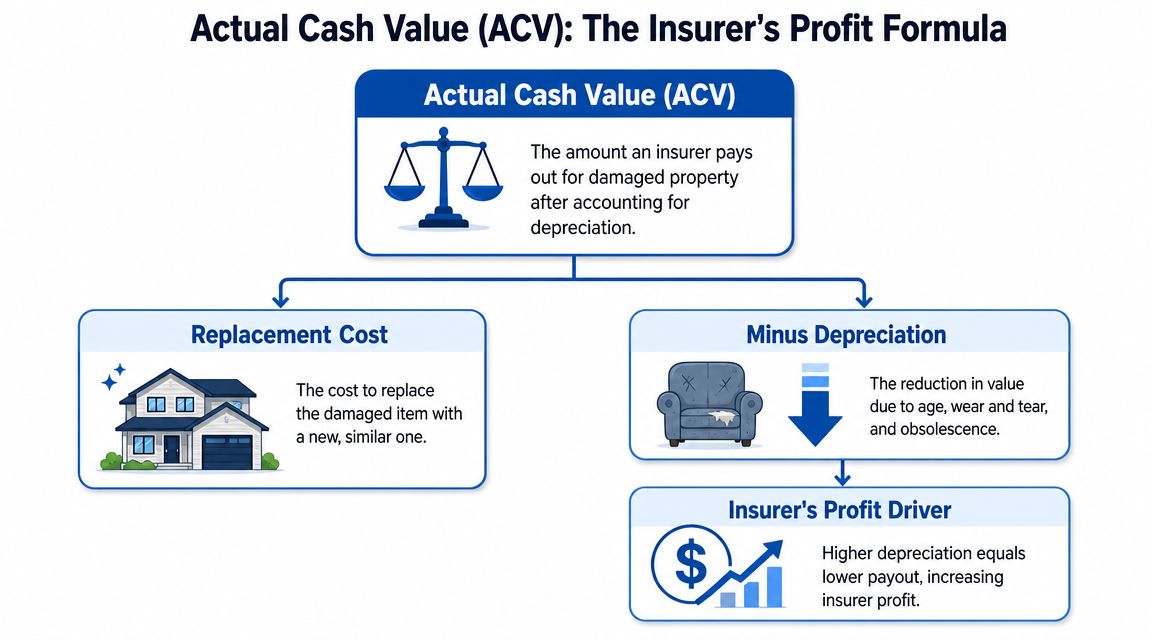

Replacement Cost Minus Depreciation The Insurer's Formula for Profit

You get a payment estimate for a damaged roof or soaked first floor. The top number looks reasonable. Then you hit the depreciation line and watch thousands disappear. That cut is where the carrier protects its money, not your property.

Actual cash value starts with replacement cost, then subtracts depreciation for age, wear, and use, as noted earlier. So a loss that costs far more to repair in practice can turn into a much smaller check once the company applies its own depreciation logic and your deductible.

Replacement cost is only the starting point

Carriers like to show you the replacement cost figure because it makes the estimate look fair. It is not the number that controls your payment on an ACV settlement.

The true fight starts after that line.

If the insurer says your cabinets were old, your flooring was near the end of its life, or your commercial fixtures had limited remaining value, the company can carve the estimate down fast. That is why property owners confuse a covered claim with a fully paid claim. Those are two different things.

If you have replacement cost coverage available under your policy, learn how that endorsement changes the payment structure before you accept the carrier's math. This guide on a replacement cost endorsement and how it affects claim payments lays out the difference.

Depreciation is the insurer's pressure point

Depreciation is rarely as objective as carriers pretend. It is built from adjuster judgment, estimating software, condition assumptions, and photos taken on the insurer's timetable. A room can be well maintained for years and still get hit with aggressive depreciation because the materials are not new.

That gives the company room to underpay without issuing a denial. They approve the loss, then shrink the value.

A twenty-year-old roof is the obvious example, but the same tactic shows up in water and fire losses. Drywall, trim, flooring, cabinets, storefront finishes, shelving, and built-ins all get tagged with age-based reductions that often ignore actual condition and useful life.

Why this formula favors the carrier

The carrier controls the early record, and that matters more than most policyholders realize.

- They write the first scope: Missed items create an estimate that is too low before depreciation is even applied.

- They choose the condition assumptions: "Old" gets treated as "worn out" even when the material was functional and serviceable before the loss.

- They anchor the dispute with the first check: Many owners assume the first payment reflects a neutral valuation. It does not.

That first number is a negotiating position.

What to do with this section of the estimate

Read the depreciation line item by line item. Do not accept a single percentage applied across dissimilar materials. Roof shingles, custom cabinets, tile, and office buildout components do not age the same way and should not be depreciated the same way.

Ask for the basis of every major depreciation decision in writing. Demand the age used, the condition assumed, the expected useful life, and the support for that conclusion. If the carrier cannot explain the percentage, challenge it.

Treat the ACV estimate as a document built to save the insurer money until you prove otherwise. That mindset will save you from signing off on a short payment.

ACV vs Replacement Cost The Financial Gap That Insurers Won't Explain

Your contractor says the roof replacement will cost far more than the check on your kitchen counter. That is the moment ACV stops sounding like insurance jargon and starts hitting your bank account.

A lot of property owners hear "covered loss" and assume the carrier will fund the repair. Then they learn the claim is being settled on actual cash value, not replacement cost. The difference is simple. Replacement cost is built around what it takes to repair or replace damaged property today, subject to policy terms. ACV cuts that number down and leaves you to carry the shortfall.

A roof loss makes the gap obvious, but the same problem shows up with siding, flooring, cabinetry, tenant improvements, and business interiors. The insurer can approve the claim and still leave you thousands short of what the job actually costs.

Side by side reality

The chart below shows why ACV creates a cash crisis after a loss.

| Cost Category | Replacement Cost Value (RCV) Policy | Actual Cash Value (ACV) Policy |

|---|---|---|

| Covered damage amount | Repair or replacement is valued at current prices | Repair or replacement starts at current prices, then gets reduced |

| Depreciation effect | Depreciation may matter during the claim process, but it does not control the final rebuild amount if policy terms are met | Depreciation directly reduces what the carrier pays up front |

| Example of damage amount | A homeowner with $10,000 in damage looks to coverage designed to fund repair or replacement at current cost | A homeowner with $10,000 in damage may receive substantially less after depreciation is applied |

| Out-of-pocket repair gap | Usually smaller if the policy pays as expected and the work is completed | Often much larger because the owner must cover the difference between the ACV payment and the real repair bill |

| Typical dispute point | Scope, code items, and whether all repairs are included | Scope, depreciation, condition, age, and whether the carrier undervalued the property before applying ACV |

That gap is where carriers make money.

The sales pitch for insurance focuses on being protected after a disaster. The settlement letter tells a different story. If your policy pays ACV, or if the carrier pays ACV first and holds back the rest, you are the one financing the repair while the insurer keeps control of the money.

Why this catches people off guard

Agents rarely spend enough time on this because it makes the policy sound less attractive. "Covered" sounds reassuring. "Covered, but only after depreciation and only if you can front the difference" does not.

Homeowners get trapped when they cannot start repairs without more funds. Business owners get hit even harder. A stripped-down ACV payment can delay reopening, slow rent recovery, and force ugly choices about temporary fixes instead of proper restoration.

If you need to understand how replacement-focused coverage changes that outcome, read this explanation of a replacement cost endorsement. That language matters a lot more after a loss than it did when the policy was sold.

Ask this before you discuss anything else

Do not ask whether the claim is covered first.

Ask this: "Is this being adjusted on actual cash value or replacement cost, and what amount is being withheld or reduced before full repair payment?"

That question gets to the heart of the matter. It forces the adjuster to explain the settlement basis instead of hiding behind a vague coverage approval.

If the estimate says "covered" but the check does not complete the repair, you are dealing with an underpayment problem. Treat it that way from the start.

How Insurers Weaponize Depreciation to Deny Fair Payment

The biggest lie in many ACV disputes is that depreciation is objective. It often isn't. It's a set of choices, and those choices can be pushed hard against the policyholder.

Major insurance references recognize that ACV is not a single universal formula. IRMI describes at least three valuation approaches: replacement or repair cost minus depreciation, fair market value, and the broad evidence rule, which weighs all relevant evidence of value, as outlined in the IRMI definition of actual cash value. If the method can change the payout, then the method itself is a dispute point.

The tricks show up in the estimate

A lot of homeowners stare at a long estimate and assume the detail means accuracy. That's a mistake. Detail can also hide bad assumptions.

Common pressure points include these:

- Generic age schedules: The adjuster treats an item as old and therefore heavily depreciated, even if it was well maintained.

- Condition gets ignored: A roof, floor, cabinet set, or built-in can be in strong pre-loss condition and still get hit with rough depreciation.

- Line items are split in the carrier's favor: Materials may be grouped in ways that maximize reduction.

- Partial repairs get devalued: The insurer acts like damaged components had limited remaining life, even where replacement matching or overall condition tell a different story.

If you want a close look at how carriers apply and defend these reductions, review this guide on depreciation on insurance claims. It helps you spot where the estimate stops being reasonable and starts becoming strategic.

Broad evidence means more than age

The broad evidence approach matters because it looks beyond a simple age chart. It can include relevant facts about condition, maintenance, use, and other indicators of value.

That matters in real property claims. A ten-year-old component that was maintained, repaired, cleaned, and still performing well before the loss shouldn't automatically be treated like a worn-out item at the end of its life. Carriers know this. They just don't volunteer it when a blunt depreciation assumption helps them.

What to challenge: Not just the depreciation amount, but the valuation method the carrier used to reach it.

Where homeowners and business owners get trapped

The company sends a spreadsheet. The owner sees numbers, percentages, categories, and long item descriptions. It feels technical, so people back off.

Don't. If the carrier chose a harsh depreciation model, ignored market evidence, or failed to account for actual pre-loss condition, the estimate deserves a direct challenge.

For business owners, this fight can be worse. Fixtures, custom improvements, shelving, office buildouts, and specialized contents can all be devalued with broad assumptions that don't reflect real market replacement pressure. For homeowners, roofs, siding, flooring, cabinetry, and interior finishes are frequent targets.

The insurer's version of depreciation is not the final word unless you let it be.

Special ACV Hurdles NC VA Rules and NFIP Flood Claims

North Carolina and Virginia policyholders deal with the same core ACV problem. The carrier controls the early estimate, frames the valuation, and counts on the owner being too overwhelmed to challenge the numbers.

North Carolina's insurance framework shows how ACV functions as a settlement ceiling. In the auto context, the state uses a Total Loss Formula where repair cost plus salvage value is greater than or equal to ACV rather than a simple percentage trigger, as discussed in this North Carolina total loss formula explanation. This article is about property claims, not auto claims, but the principle still matters. ACV serves as the benchmark for settlement value, and that ceiling mindset carries into property claim handling.

What that means for property losses in NC and VA

For a house or commercial building, the fight usually isn't over whether ACV exists. It's over how low the carrier pushes that value.

That's why owners in NC and VA need to press for:

- A full line-item estimate: Not a summary sheet.

- The depreciation logic: Ask what age, condition, and useful life assumptions were used.

- Support for the valuation method: If the company picked a method that cuts the payout, make them explain it.

Flood claims are a different animal

If the damage is from flood, you're in a more specialized dispute. FEMA and NFIP claims are not standard homeowners claims, and policyholders often learn that the hard way.

NFIP and Write Your Own flood claim handling can feel rigid, narrow, and unfriendly to the actual conditions at the property. The adjuster may focus on technical categories, strict documentation, and narrow interpretations while the owner is dealing with soaked materials, contamination concerns, demolition decisions, and mounting repair pressure.

If your loss involves flood, don't assume the standard homeowners claim playbook applies. Review this guide to flood damage claim help so you understand how these disputes differ and why documentation gets even more important.

Flood policyholders often think the hardest part is proving damage happened. In practice, the harder part is proving the full extent and value of that damage under a rule-heavy system.

Clear recommendation for NC and VA owners

Treat ACV as a negotiation battleground from day one. If the carrier is settling on depreciated value, demand the basis for every major reduction. If it's an NFIP flood loss, get organized early and expect resistance.

Your Battle Plan to Dispute a Lowball ACV Settlement

You don't beat a lowball ACV offer by complaining that the number feels unfair. You beat it by attacking the estimate, the depreciation logic, and the missing support behind the carrier's valuation.

The key factor is documentation. A legal and industry review highlighted that most ACV explainers don't address the fundamental question, which is how depreciation gets challenged, and that the difference between age-based and condition-based depreciation can be significant but requires receipts, photos, and expert argument, as discussed in this review of ACV language and valuation disputes.

Start with the written estimate

Do not argue in the abstract. Get the insurer's paperwork.

Ask for the full estimate showing every line item, every depreciation entry, and any notes about age, condition, and useful life. If they only send a summary, push again.

Your first job is to find where the money disappeared.

- Missing scope: Rooms, finishes, or building components left out entirely.

- Weak pricing: Numbers that don't reflect what local contractors are telling you.

- Heavy depreciation: Categories that got reduced without a clear basis.

Build your condition file

Most claimants are often unprepared. The insurer counts on that.

Your file should include:

- Pre-loss photos: Roof condition, interior finishes, cabinets, flooring, exterior elevations.

- Maintenance records: Repairs, cleaning, upgrades, service invoices, contractor receipts.

- Post-loss photos and videos: Wide shots and close-ups.

- Contractor observations: Written notes about damage extent, material condition, and repair needs.

If you're dealing with storm-related damage, this outside perspective on KC storm damage insurance advice is useful because it shows how important documentation and estimate comparison are when an adjuster tries to control the narrative.

Push back item by item

Don't send the insurer a vague message saying the estimate is too low. Send a pointed rebuttal.

Challenge things like:

Condition assumptions

If the carrier depreciated a component mainly because of age, show maintenance and pre-loss condition evidence.Improper grouping

If they rolled unlike items together under one depreciation approach, separate them.Short useful-life assumptions

Ask what source they used and why it fits your specific property.Ignored repairs or updates

If part of the system had been repaired or improved, the blanket depreciation may be wrong.

A strong dispute letter doesn't say “please reconsider.” It says “your depreciation on these listed items is unsupported for these listed reasons.”

Here's a practical explainer that helps frame the negotiation mindset before you send that response:

Know when to bring in outside help

Some disputes stall because the owner has reached the limit of what the carrier will take seriously from a policyholder alone. That's usually the point where independent help matters.

Options can include a qualified contractor with a detailed scope, a coverage attorney when legal issues are central, or a licensed public adjuster who can review valuation, documentation, and negotiation strategy. For The Public Adjusters, Inc. handles residential and commercial property claims in North Carolina and Virginia by reviewing insurer estimates, documenting losses, and negotiating disputed property damage valuations.

Never assume the first offer is the best the insurer can do. In ACV disputes, the first offer is often just the opening position.

Don't Fight Them Alone How a Public Adjuster Wins the ACV Battle

ACV disputes wear people down because the insurer gets to sound technical while the property owner is stuck living with the damage. That imbalance is the core problem. The carrier has adjusters, software, estimating systems, and internal review channels. You have a damaged home or business and a check that doesn't solve it.

That's why these cases turn on evidence and pressure. A public adjuster changes both. They can challenge the insurer's scope, test the depreciation line by line, assemble maintenance and condition evidence, and force the discussion away from generic assumptions and back onto the actual property.

What winning usually looks like

It doesn't always mean some dramatic courtroom showdown. More often, it means:

- Revising the scope of damage

- Reducing unsupported depreciation

- Documenting better pre-loss condition

- Pushing the carrier to justify weak valuation choices

- Keeping the claim from being closed prematurely on bad numbers

When the insurer's estimate becomes a document that has to be defended, not just accepted, the balance starts to shift.

The hard truth

Insurance companies don't mind confused policyholders. Confusion saves them money. ACV gives them a respectable-sounding way to pay less, especially when the homeowner or business owner doesn't know what to challenge.

If your fire, water, wind, hail, or storm claim has been low-balled, delayed, or buried under aggressive depreciation, don't treat that estimate as final. Treat it as the start of the dispute.

If your insurance company is using actual cash value to shrink your property claim, get a second set of eyes on the estimate before you give up or pay the gap yourself. For The Public Adjusters, Inc. offers no-cost claim reviews for homeowners and business owners in North Carolina and Virginia who need help disputing underpaid property damage claims.