So, your insurance claim was denied. What now? How to Appeal Insurance Claim Denial.

That denial letter for your homeowner or business property claim feels like a gut punch. After surviving a fire, flood, or hurricane, seeing the words “claim denied” is the last thing you want to deal with. But I need you to understand something critical right now: a denial is not the end of the road. More often than not, it’s just the opening chess move from your insurance provider.

Insurance giants like State Farm and Allstate are massive, for-profit corporations. Their primary responsibility is to their shareholders, not to you. Their entire business model is built on one thing: minimizing payouts. Denying a perfectly valid claim, delaying the process, or throwing a lowball offer at you are all standard plays from their book. They’re banking on you feeling overwhelmed, exhausted, and just giving up. Don’t do it. You have every right to fight their decision, and learning how to appeal an insurance claim denial is the most powerful weapon in your arsenal. The system is designed to be confusing and intimidating, but with the right strategy, you can turn the tables.

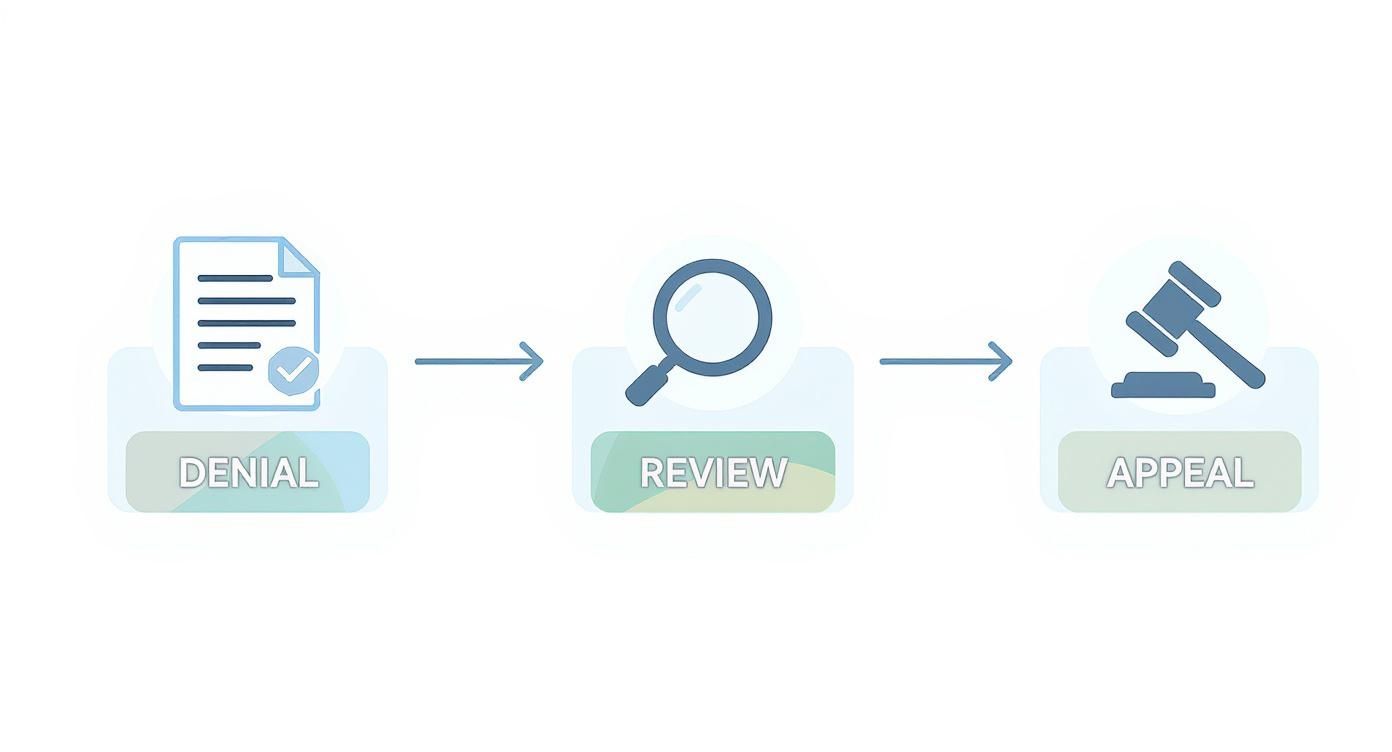

The Path Forward After a Denial

The journey from a denial to a successful appeal isn’t magic; it’s a methodical process. It starts with dissecting their flimsy reasoning and ends with you presenting a rock-solid, evidence-based case they can’t ignore.

Here’s a quick look at the road ahead.

As you can see, their denial is just the starting whistle. The real game begins now, with the ball back in your court.

Decoding Your Denial Letter Key Sections to Review First

Your denial letter is more than just bad news—it’s a treasure map. It tells you exactly where the insurer thinks your claim is weak, giving you the precise coordinates for your counter-attack. You need to read it not as a final judgment, but as your opponent’s playbook.

| Letter Section | What to Look For | Why It Matters for Your Appeal |

|---|---|---|

| The “Reason for Denial” Paragraph | The specific policy language, exclusion, or condition they are citing. They must reference a direct part of your policy. | This is the heart of their argument. Your appeal needs to directly challenge this specific point with your own evidence and interpretation of the policy. |

| List of Documents Reviewed | The adjuster’s report, photos, expert opinions, or any other evidence they list as part of their decision-making process. | If they are missing key documents you provided, or if their “expert” report seems biased, you’ve found a major weakness to exploit in your appeal. |

| Specific Policy Exclusions | The exact wording of the exclusion clause they are using to deny coverage (e.g., “wear and tear,” “faulty workmanship”). | You need to prove this exclusion doesn’t apply. Was the damage from a sudden event, not gradual wear? This is where your photos and contractor reports come in. |

| Appeal Instructions and Deadlines | The strict timeline for submitting your appeal (often 30-60 days) and the required format or address. | Missing this deadline is an automatic loss. It’s the first hurdle they set up, hoping you’ll trip over it. Mark this date on your calendar immediately. |

Once you’ve broken down their reasoning, you can start building your case piece by piece, directly refuting every point they’ve made.

Shifting From Defeated to Empowered

The single most important part of a successful appeal is a shift in your mindset. Stop seeing the denial as a verdict and start seeing it as an invitation to build a bulletproof case. Your insurer has laid out their position; now it’s your turn to dismantle it.

A denial letter isn’t a brick wall—it’s a blueprint. It tells you exactly which parts of your claim the insurer is challenging, giving you a precise roadmap for where to focus your fight.

This isn’t about arguing with the adjuster on the phone. It’s about becoming the undisputed expert on your own claim. You need to organize every photo, every receipt, and every contractor’s estimate. You need to articulate your arguments professionally in writing and—most importantly—hit every single deadline they give you.

Insurers absolutely rely on procedural tripwires and tight timelines to get rid of claims. One of the most common questions we get is about these deadlines. Understanding how long an insurance company has to settle a claim gives you crucial context and helps you hold them accountable.

When you treat this appeal like a methodical, evidence-based project instead of an emotional battle, you dramatically increase your odds of overturning their decision and getting the settlement you’re owed.

Deconstructing the Denial to Build Your Case

That denial letter in your hands isn’t a final verdict. Think of it as the insurance company showing its entire hand—a roadmap detailing every flimsy excuse, every misinterpretation, and every weak point in their argument. Getting that letter is frustrating, but it’s also your single best opportunity. Your first move in appealing a claim denial is to treat this document like an intelligence report.

Let’s be clear: insurance carriers like Allstate and State Farm are experts in crafting vague, confusing language. They bank on you being too overwhelmed or intimidated to push back. Your job is to call their bluff by taking their reasoning apart, piece by piece, until you find the cracks.

Pinpointing the Insurer’s Weaknesses

Every denial has to hang its hat on something specific—usually a particular policy exclusion or condition. That’s your target. Your entire appeal will be built on proving their interpretation is flat-out wrong or that the exclusion simply doesn’t apply to what happened.

Keep an eye out for these all-too-common (and questionable) tactics:

- Blaming “Wear and Tear”: This is a classic. The insurer claims your 10-year-old roof failed because of its age, conveniently ignoring the massive hailstorm that just blew through town. Your appeal needs to hammer home the fact that the damage was caused by a sudden, covered event.

- Misinterpreting Policy Exclusions: A business owner might get a business interruption claim denied because of a “utility service exclusion,” even though the power went out as a direct result of a fire on the property—a covered peril. The sequence of events is everything.

- Relying on Biased Experts: That “independent” engineer or contractor they sent out? They were hired and paid by the insurance company. It’s no surprise their report almost always backs the insurer’s decision. This is a huge point of leverage for you.

The practice of denying claims is baked into the system. Insurance companies routinely deny valid property claims, hoping that policyholders will be too intimidated or exhausted to fight back. This is a business strategy designed to protect their profits, not to honor your policy. You must be prepared to challenge their decision with a strong, evidence-based appeal.

Going Beyond the Denial Letter

The letter itself is just the opening salvo. To really build a waterproof case, you need to formally request a complete copy of your claim file. This isn’t a courtesy; it’s your right as a policyholder.

Don’t just argue against the denial letter—demand the entire claim file. This file contains every note, photo, report, and internal communication related to your claim, often revealing evidence they hoped you’d never see.

This file is a goldmine. It contains the adjuster’s private notes, every photograph they took (including the ones that prove your point), and the full reports from their experts. You might discover the adjuster completely ignored evidence you sent them or that their expert’s damning conclusions were based on a quick, five-minute walkthrough.

Real-World Denial Scenarios

Let’s see how this plays out in the real world. Imagine a pipe bursts inside a wall of your commercial building, leading to major water and mold damage. The insurer denies the claim, pointing to a “mold exclusion” in your policy.

Here’s how you deconstruct that denial:

- Causation: The root cause wasn’t mold. The loss was caused by a “sudden and accidental discharge of water,” which is a standard covered peril. The mold is a consequence, not the cause.

- Policy Language: You argue that since the mold grew as a direct result of the covered water damage, the cost to fix it should be part of the original water damage claim.

- Claim File Evidence: You get the claim file and find the adjuster’s own photos clearly showing the broken pipe. Their internal notes might even acknowledge the pipe burst but show they were instructed to focus only on the mold exclusion.

By meticulously dismantling their logic and using their own internal documents against them, you flip the script. You’re no longer just defending against their denial—you’re on the offensive, building a powerful case that systematically proves them wrong and sets you up for a successful appeal.

Gathering Evidence to Overturn the Denial

An appeal without hard proof is just an opinion, and I can tell you from experience, insurance companies like State Farm and Allstate are experts at dismissing opinions. When you’re learning how to appeal an insurance claim denial, you have to get one thing straight: the quality of your evidence is everything.

This isn’t about just telling them they’re wrong. It’s about building a case so loaded with undeniable facts that it leaves them no room to argue.

Your mission is to systematically take apart every reason they gave for the denial and bury it under a mountain of proof. Think of yourself as an investigator building a case for trial. Every photo, every email, every receipt adds to a narrative they simply can’t ignore.

Documenting the Damage The Right Way

The evidence you gather has to paint an undeniable “before and after” picture. Insurers love to fall back on excuses like pre-existing conditions or “wear and tear,” but solid visual proof shuts that down cold.

Your visual evidence portfolio needs to be airtight:

- Pre-Loss Photographs: If you have any pictures of your property from before the damage, they are pure gold. A photo of your pristine roof from six months ago is the perfect weapon against a “wear and tear” denial after a hailstorm.

- Post-Damage Photos and Videos: Don’t just take wide shots from the curb. Get right up close to the damage. Capture it from different angles. Then, take a video walkthrough of the entire affected area, narrating what you’re seeing. This shows the full scope in a way that a stack of photos never can.

- Timestamped Evidence: Make sure your phone or camera has the date and time stamp feature turned on. This creates a concrete timeline that ties the damage directly to the covered event.

Your goal is to make it impossible for the person reviewing your appeal to question the property’s condition before the loss or the severity of the damage after. A well-documented visual timeline is your strongest opening salvo.

This level of detail is the foundation of any strong property damage claim and it becomes absolutely critical when you’re fighting a denial.

Countering the Insurer’s Lowball Estimates

One of the oldest tricks in the book is for the insurer to send out their “preferred vendor” or a staff adjuster who writes up an estimate that barely covers the cost of paint. Never, ever accept their number as the final word.

You need to get your own independent estimates from reputable, local contractors—the kind who specialize in insurance restoration work. Don’t stop at one. Get at least two, preferably three.

Hand each contractor a copy of your insurer’s estimate. Ask them to create their own detailed, line-item bid that specifically points out why the insurance company’s scope of work is a joke. This will likely include:

- Missing line items for crucial steps like debris removal, permits, or site prep.

- Incorrect measurements that conveniently shrink the size of the damaged areas.

- Low-quality material pricing that doesn’t match what you actually had before the loss.

When you hit them back with multiple professional estimates that are all significantly higher than theirs, it exposes their number for what it is: an intentional lowball, not a legitimate assessment.

Creating a Communication Log to Expose Bad Faith

Insurance companies often weaponize delays, hoping you’ll get exhausted, frustrated, and just give up. Your best defense is a meticulous communication log. It creates a timeline that can expose patterns of bad faith, like constantly missed deadlines or contradictory statements.

Every single time you talk to someone from the insurance company, log it.

Your record for each interaction should include:

- Date and Time: Be exact.

- Name and Title: Get the full name and title of who you spoke with.

- Method of Communication: Phone call, email, letter, carrier pigeon—write it down.

- Summary of Discussion: Note the key points, what they promised, and what you asked.

This log is more powerful than you think. If an adjuster tells you on May 1st that the engineer’s report will be ready in a week, and you don’t receive it until July 15th, your log proves they failed to act in good faith. This kind of detailed record is often the key to showing they handled your claim unfairly, and it adds serious leverage to your appeal.

Writing an Appeal Letter That Gets Results

Your appeal letter isn’t just some form you fill out—it’s the core of your fightback plan. When you’re trying to figure out how to appeal an insurance claim denial, this letter is your one real shot to lay out a logical, evidence-packed argument that forces the insurance company to take a second look.

Forget about emotional pleas. This is all business. You’re building a professional, airtight case they can’t just brush aside.

This isn’t the time for an angry email. Think of it as a formal business communication designed to get one thing: a reversal of their decision. Every single sentence needs to be deliberate, factual, and aimed at dismantling their denial while proving your claim.

The Core Components of a Winning Letter

A powerful appeal letter is structured and methodical, not a rambling mess. It needs a logical flow that makes it easy for the claims supervisor to follow your argument. Big insurers like State Farm and Allstate see thousands of these. Yours has to cut through the noise with clarity and professionalism.

Make sure your letter hits these essential points:

- A Clear Statement of Disagreement: Right up front, state that you are appealing the denial of claim number [Your Claim Number] and that you formally disagree with their findings.

- A Point-by-Point Rebuttal: Go through their denial letter and address every single reason they gave. Use their own words as a guide and systematically tear down each point with your evidence.

- Reference Your Policy: Pull the exact language from your policy that backs up your claim. This isn’t just a suggestion; it’s a reminder of the contract they are legally obligated to honor.

- A List of New Evidence: Clearly itemize every new piece of documentation you’re including, whether it’s an independent contractor’s estimate, an engineer’s report, or more photos of the damage.

This structure forces them to engage with your facts. It makes it much harder for them to just dismiss your appeal without a proper review.

Setting the Right Tone: Assertive, Not Aggressive

The single biggest mistake I see policyholders make is letting their anger and frustration take over. While you have every right to be furious, venting in your appeal letter will only backfire. The goal is to be firm, factual, and professional—nothing more, nothing less.

You are presenting a business case, plain and simple. Stick to the facts you’ve gathered.

Instead of writing this: “Your adjuster was useless and completely ignored the real damage!”

Write this: “The enclosed estimate from Certified Restoration details an additional $22,500 in damages not included in the adjuster’s initial report, specifically related to smoke damage in the attic.”

See the difference? That shift from accusation to evidence is what separates a letter that gets ignored from one that gets taken seriously. It shows you’re organized and ready to defend your position with facts, not feelings.

Your appeal letter should read like a legal brief, not a personal complaint. Focus on policy language, documented evidence, and factual inconsistencies in their denial. Emotion clouds judgment; facts win appeals.

The Final, Crucial Steps You Cannot Skip

Just writing the letter isn’t enough. How you send it and follow up can make or break your entire appeal. Insurance companies count on policyholders tripping up on these small procedural details.

Don’t give them an easy out.

First, send it via certified mail. Always. Get a return receipt requested. This creates a legal paper trail proving exactly when they received your appeal package. No excuses, no “we never got it.”

Second, respect the deadline. Your denial letter will state a strict deadline for filing an appeal. If you miss that date by even one day, they can—and likely will—refuse your appeal on a technicality. Mark that date on your calendar and send your letter well in advance.

Denials are a standard part of the insurance playbook. While the following data reflects a different insurance sector, the strategy is the same. read more about these payer denial tactics to understand why persistence pays off across the industry. Insurers know that a huge percentage of people will just give up. By sending a professional, evidence-backed letter via certified mail, you are sending a clear signal: you aren’t one of them.

Escalating Your Fight When They Still Say No

You did everything right. You wrote a solid appeal letter, backed it up with undeniable proof, and even sent it via certified mail. Then, the insurance company sends back another denial. Or worse, you get nothing but silence.

This isn’t an accident. It’s a calculated strategy. Insurers like State Farm and Allstate are banking on this second rejection to be the one that finally breaks your will, forcing you to accept their ridiculously low offer or just walk away defeated.

Don’t let them win. An internal appeal is just one move in this game. When the insurance company digs in its heels, it’s time to stop playing by their rules and start leveling the playing field.

Bringing in Your Own Expert: The Public Adjuster

Up until now, you’ve been dealing with the insurance company’s adjuster—someone paid to protect their employer’s bottom line. Now, it’s time to hire your own expert: a public adjuster.

Unlike the company adjuster, a public adjuster is a state-licensed professional who works only for you, the policyholder. They become your advocate, your negotiator, and your expert guide through the toughest parts of the claim process.

Here’s how a public adjuster can immediately turn the tables on a stubborn insurer:

- They perform their own forensic-level damage assessment, documenting all the damage the company adjuster conveniently “missed.”

- They take over all communication. No more frustrating phone calls or ignored emails. Your public adjuster deals with the insurance company so you don’t have to.

- They know the insurer’s playbook. Public adjusters understand the tricky policy language, complex building codes, and negotiation tactics insurers use to deny and underpay claims.

Hiring a public adjuster sends a clear message: you’re not giving up, you know your rights, and you will not be intimidated. If you’re hitting a wall with a denied claim, understanding what a public adjuster is and how they fight for you is your most critical next step.

Putting the Insurer Under Official Review

If your insurer is ignoring you or is clearly acting in bad faith, you can take the fight to a higher authority: your state’s Department of Insurance (DOI). This is the government agency that regulates insurance companies and protects consumers like you.

Filing a complaint with the DOI doesn’t cost you a dime, but it puts your insurer’s behavior under an official microscope. Once you file, the DOI opens an inquiry and demands a formal, written response from your insurance company, forcing them to justify their denial to a regulator.

A complaint to the Department of Insurance turns your private fight into a public record. It forces the insurer to answer for their actions to a government body with the power to fine them or even pull their license.

While the DOI usually won’t order an insurer to pay a specific amount, the pressure of a state investigation is often enough to make a stubborn claims department reconsider and come back to the table with a fair offer.

Understanding Your Other Options: Appraisal, Mediation, and Litigation

When an internal appeal and a DOI complaint don’t break the stalemate, you still have several powerful options left.

- Appraisal: This is for when the dispute is strictly about the cost of repairs, not about whether the damage is covered. Your policy likely has an appraisal clause. You and the insurer each hire an independent appraiser, and they agree on a neutral third party (an umpire). A decision from any two of the three is binding.

- Mediation: Think of this as a structured negotiation. A neutral mediator helps you and the insurance company try to find common ground and reach a settlement. The mediator doesn’t make a decision but works to get a deal done, which is a great option if communication has completely broken down.

- Litigation: Filing a lawsuit is the last resort. If the insurance company has breached its contract or acted in bad faith, this may be the only way to hold them accountable. It’s a longer and more expensive road, but sometimes it’s the only one that leads to justice.

The sad truth is that insurance companies deny valid claims all the time because they know most people won’t fight back. It’s a business model built on you giving up. Don’t fall for it.

Got Questions About Fighting a Denied Claim? We Have Answers.

When you get that denial letter in the mail, your head starts spinning with questions. It’s a confusing and frustrating place to be, but you’re not alone. Here are some of the most common questions we get from homeowners and business owners who are learning how to fight back.

How Long Do I Have to Appeal a Denied Property Claim?

This is the single most important detail, and the insurance companies are betting you’ll miss it. There’s no single, universal deadline; it’s hidden in the fine print of your specific insurance policy. That window to fight back could be as short as 60 days or stretch out to a full year from the date on your denial letter. In NC the state statute is 3 years from the date of loss.

Your very first move after getting a denial should be to hunt down that deadline in your policy documents. If you miss it by even one day, the insurer can legally toss your appeal in the trash without a second glance. They build these procedural traps hoping you’ll step right into them.

Can My Insurance Company Drop Me for Appealing?

Absolutely not. It is illegal for an insurance company to cancel your policy or refuse to renew it just because you filed a legitimate claim or appealed their bad decision. That’s called illegal retaliation, and there are laws to protect you from it.

If you even suspect your policy was dropped because you pushed back on a lowball offer or a denial, don’t wait. File a formal complaint with your state’s Department of Insurance immediately. This puts a spotlight on their actions and protects your rights as a policyholder.

What if the Insurer Blames Pre-Existing Damage?

This is a classic move, especially from the big carriers like Allstate and State Farm. Their adjuster will hire an “expert” engineer or contractor who—big surprise—writes a report blaming everything on “wear and tear,” “faulty maintenance,” or some other pre-existing issue.

You do not have to accept the word of an expert who is paid by the same company that wants to deny your claim. It’s a massive conflict of interest.

The best way to shut this argument down is to bring your own facts to the fight. Hire your own independent public adjuster to perform a separate, unbiased assessment. Their report becomes your most powerful weapon, directly contradicting the insurance company’s hired gun.

An independent report systematically tears their flimsy arguments apart and gives your appeal the rock-solid foundation it needs to win.

Do I Need a Lawyer to Appeal a Denied Claim?

You can often handle the first round—the internal appeal—on your own by following the steps we’ve outlined. But if you want to bring in real firepower from the start, hiring a public adjuster is an even better move. A public adjuster takes the entire fight off your shoulders.

You should only start thinking about a lawyer if you’ve gone through the internal appeal and the insurance company is still stonewalling you or clearly acting in bad faith. At that point, an attorney specializing in property insurance law can take legal action, which is the final step when the standard appeals process fails.

Q2: What essential evidence do I need to gather to successfully appeal a property claim denial?

A: You need evidence that directly contradicts the insurer's reason for denial. This often includes: detailed photographs/videos of the damage, independent contractor/engineer reports on the cause and scope of damage, professional estimates that support a higher value, and detailed records of all your communication with the insurer.

Q3: What is the 'Internal Appeal' process and is it mandatory to challenge a denial?

A: The Internal Appeal is the first formal step where you ask the insurance company to review its own decision. It is the required step before moving to external reviews or legal action. You must submit a detailed letter with new or overlooked evidence within the insurer's specified deadline.

Q4: What happens if my internal appeal is also denied, and what is the next level of appeal?

A: If the internal appeal fails, the next level is often an External Review or Filing a Complaint with your state's Department of Insurance (DOI). The DOI can mediate the dispute and ensure the insurer followed proper claims handling procedures.

Q5: How can a policyholder successfully challenge a denial based on a policy exclusion?

A: To challenge a policy exclusion, you must often demonstrate that the dominant cause of loss is covered (not excluded), or that the exclusion was vaguely defined or improperly applied. Expert policy interpretation and a compelling legal argument, usually built by a Public Adjuster or attorney, is required.

Q6: Can a Public Adjuster overturn a denied property insurance claim, and how do they help?

A: Yes, a Public Adjuster specializes in overturning denials. They help by conducting an expert reassessment of the loss, building a robust, professional file of documentation and estimates, and negotiating directly with the insurer's adjusters and management from a position of authority. Contact For The Public Adjusters, Inc. to have all your claim questions answered at NO COST! (567) 888-HELP

Q7: Is it too late to hire a Public Adjuster if my claim has already been denied?

A: No, it is not too late. Many policyholders hire a Public Adjuster specifically after a denial or severe underpayment. A Public Adjuster is often the best resource for gathering the necessary counter-evidence and navigating the formal appeals process.

Q8: When does a denied claim become a 'Bad Faith' issue that requires an attorney?

A: A denial may involve Bad Faith if the insurer denies the claim without a reasonable basis, fails to conduct a thorough and prompt investigation, or uses misleading tactics. While a Public Adjuster can often resolve the claim, an attorney is necessary to pursue a formal Bad Faith lawsuit.

Q9: Can I use the Appraisal clause in my policy to appeal a claim denial?

A: No, Appraisal is generally used to dispute the amount of loss (valuation), not the coverage decision (denial). If the insurer denies that a loss is covered at all, the claim must be appealed through internal/external review or litigation, not Appraisal.

Q10: Are there deadlines I must meet when appealing an insurance claim denial?

A: Absolutely. The denial letter will specify strict deadlines (often 60, 90, or 180 days) for filing an internal appeal. Missing this deadline can permanently void your right to appeal and receive payment, making timely action critical.

RELATED:

Fight Claim Denial

When your insurance company cares more about its bottom line than your recovery, you need an expert in your corner. For The Public Adjusters, Inc. fights for policyholders—not the insurance giants. If you’re dealing with a denied, delayed, or underpaid claim in North Carolina or Virginia, contact us for a no-cost claim review and find out how we can get you the full settlement you’re owed.

Trackbacks/Pingbacks