When disaster strikes your home, the first thing on your mind is getting your family to safety. But in the hours and days that follow, a new, crushing reality sets in: Where are you going to live?

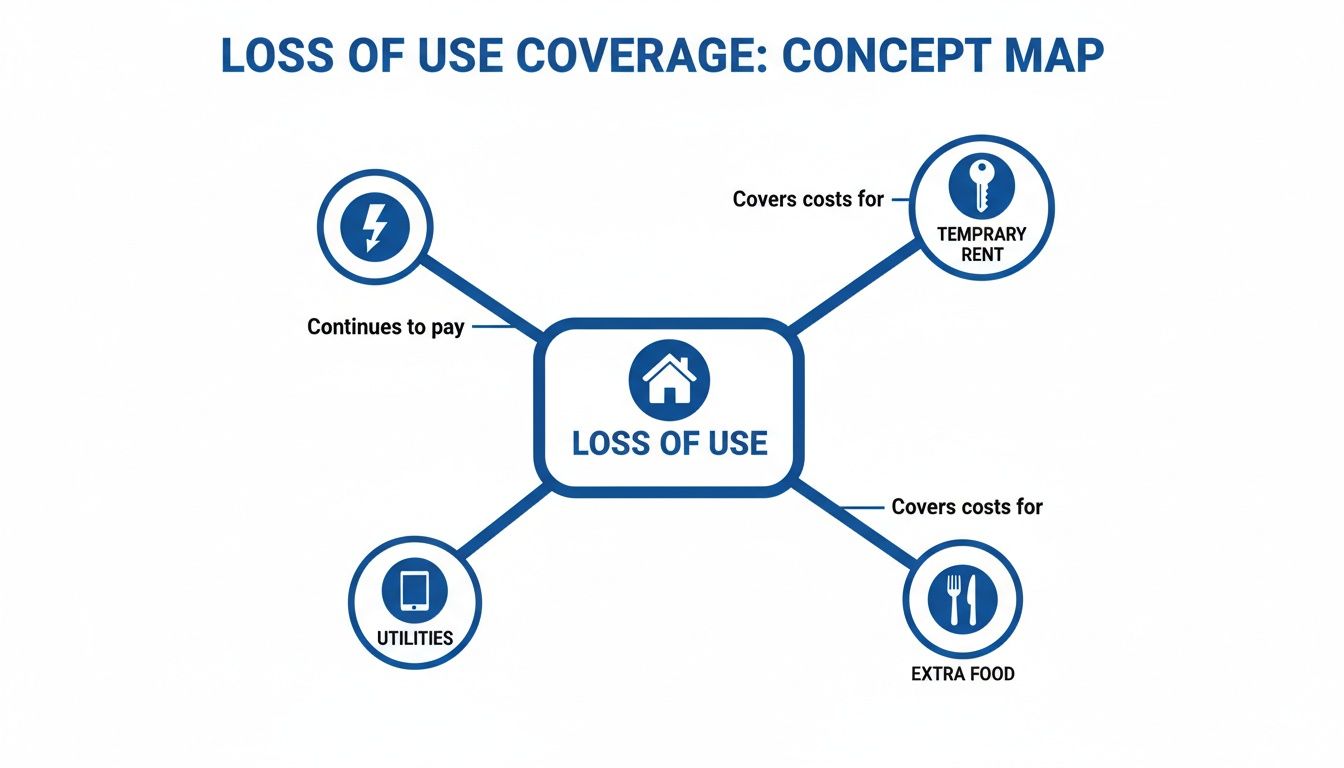

This is where your Loss of Use coverage, sometimes called Additional Living Expenses (ALE), is supposed to kick in. It’s the part of your homeowners insurance policy designed to be a financial lifeline, covering the extra costs of temporary rent, food, and other necessities so you can maintain your family's life while your home is being rebuilt.

But here’s the hard truth: this coverage, meant to provide peace of mind, often becomes a major battleground with insurance companies like State Farm and Allstate, who are notorious for delaying and denying valid claims.

What Is Loss of Use Coverage And Why It Is A Battleground

After a fire, hurricane, or major pipe burst wrecks your North Carolina or Virginia home, your insurer’s promise is that they’ll cover the financial burden of being displaced. This critical protection, found under “Coverage D” in most policies, is meant to pay for the increase in your living expenses—the difference between what you normally spend and what you’re forced to spend now.

It sounds simple enough. But we see major insurance carriers turn this promise into a prolonged fight every single day.

Instead of providing the support you’ve paid for, their adjusters use vague policy language and aggressive tactics to limit what they pay you. They’ll question whether your temporary rental is “comparable,” scrutinize every single meal receipt, or prematurely declare your damaged house “livable” just to cut off your benefits. This isn't about fairness; it's about protecting their profits.

The Growing Need For ALE Coverage

Let’s be clear: the need for strong Loss of Use coverage has never been more critical.

When a sudden catastrophe like a pipe burst makes your home unlivable, this coverage becomes your only way to keep your family stable. Of course, taking the right immediate steps to minimize damage after a pipe burst can shorten how long you're out of the house, but you're still going to need a place to live.

This is what your ALE coverage is supposed to handle.

As you can see, it’s not just about a roof over your head. It’s about covering all the extra costs that come with displacement, from higher food bills to utility setup fees, so your life isn't completely upended.

Unfortunately, the gap between what your policy promises and what insurers actually pay is getting wider. Repair and construction costs jumped about 45% between 2020 and 2023 alone. Families are blowing through their ALE policy limits long before their homes are ready.

This is exactly what the insurance companies are counting on. They know the numbers, and they use these trends to their advantage, leaving you to cover tens of thousands in out-of-pocket expenses unless you’re prepared to fight. That’s why you have to know every detail of your policy—something we break down in our guide to understanding homeowners insurance coverage.

Decoding the Hidden Traps in Your ALE Policy

Insurance policies are designed to be confusing, and big carriers like State Farm and Allstate have weaponized that confusion against you. It's a system that’s rigged from the start, especially when it comes to your Additional Living Expenses (ALE), also known as homeowners insurance loss of use coverage.

The game is stacked against you because your ALE limit is almost always just a percentage of your dwelling coverage. So if your home’s structure is undervalued—which is terrifyingly common—it kicks off a domino effect that guarantees you get shortchanged on both the rebuild and your temporary housing.

The Underinsurance Domino Effect

This underinsurance trap is exactly why so many families in North Carolina and Virginia blow through their ALE benefits long before the repairs are even close to being done. It's a nationwide crisis. One analysis found that roughly two-thirds of U.S. homes are underinsured against climate-related disasters, leaving homeowners with a massive financial hole when they need help the most.

When your policy only covers 50–60% of what it actually costs to rebuild in today’s market, the ALE limit tied to that bogus number will never be enough. You can learn more about this problem from the Consumer Federation of America’s full report on homeowners insurance gaps.

This isn't an accident; it's a calculated strategy. Insurers know that an undervalued dwelling limit puts a low ceiling on your loss of use benefits. They’re setting you up to run out of money before your home is livable again.

This financial pressure is designed to force your hand, making you accept a lowball settlement offer just to get back home. It's a deliberate squeeze play meant to save the insurance company money at your expense.

Vague Language Adjusters Exploit

Beyond lowballing your home's value, insurers lay traps right in the policy's fine print. These aren't innocent mistakes. They are intentionally vague clauses that give the company adjuster all the power to deny legitimate expenses.

Here are two of the most abused clauses we see every day:

- Restrictive Time Limits: Your policy probably says ALE is covered for the "shortest time required to repair or replace the damage." The insurer will then pull an impossibly optimistic timeline out of thin air, arguing repairs should take six months when material shortages and booked contractors mean it will really take over a year.

- The 'Reasonable and Necessary' Clause: This is the insurance adjuster’s favorite weapon. They get to be the judge and jury of what’s "reasonable," claiming your temporary rental is too fancy or your meal receipts are excessive. Their goal is to bully you into substandard housing and nickel-and-dime every single receipt, all while you’re just trying to hold your life together.

How to Document Every Expense to Build an Ironclad Claim

If you want to win a fight over your homeowners insurance loss of use coverage, a shoebox full of receipts isn't going to cut it. You need to build a mountain of evidence so overwhelming that the insurance adjuster has no choice but to pay what you're owed. Don't think of yourself as a victim asking for help; you need to be a prosecutor building an airtight case against an insurer who is programmed to lowball you.

Your most powerful weapon here is meticulous, almost obsessive, documentation. It’s not just about saving receipts—it's about creating a detailed log that clearly proves the increase in your spending. This means you have to know what your normal, pre-disaster costs were and then compare them, line-by-line, to your new, post-disaster expenses.

Creating an Undeniable Expense Log

First, figure out your baseline budget for a typical month before the disaster wrecked your life. Then, track every single new expense you’re forced to pay because you can no longer live in your home.

Your log should have columns for things like:

- Date: When you spent the money.

- Expense Category: Think Temporary Rent, Groceries, Restaurant Meals, Extra Mileage.

- Amount: The exact dollar figure.

- Proof: Make a note of the documentation—receipt, invoice, bank statement.

- Justification: A quick note explaining why this was a necessary additional expense.

Let's say your normal monthly grocery bill was $800. But now, because your temporary apartment has no real kitchen, you're spending $1,200 a month on groceries and restaurant meals. That $400 difference is your claimable Additional Living Expense.

Every single dollar you document chips away at the insurance company's power to fight your claim. An organized log like this transforms a messy pile of receipts into a powerful story of your financial hardship, making it that much harder for them to justify an unfair settlement.

The Essential Documentation Checklist

Your goal is to leave absolutely no room for doubt. Gather and organize everything, keeping both digital and physical copies. A complete, organized file is your best defense against an adjuster’s nitpicking and is a crucial part of a formal Proof of Loss statement.

Your documentation arsenal needs to include:

- Housing: Signed rental agreements for your temporary place, hotel bills, and any receipts for security deposits.

- Utilities: Every invoice for setting up new services like electricity, internet, or gas at your temporary home.

- Food: All grocery and restaurant receipts. Keep them separate so you can easily show the increase over your normal food budget.

- Storage: Invoices from storage facilities. And don't forget the costs associated with finding temporary storage units for whatever belongings you could salvage.

- Transportation: Keep a mileage log showing the extra miles you're now driving to work or to get the kids to school. Add in receipts for gas, parking, or public transit.

- Other Services: Receipts for anything else you wouldn't have paid for if you were still in your home—think pet boarding, laundry services, and so on.

This level of detailed record-keeping is not optional. It’s the very foundation you need to build a successful fight against a stubborn insurance company.

Fighting Back Against Common Insurer Excuses

When you file for homeowners insurance loss of use coverage, you expect help. What you often get is a fight. Insurance adjusters from major carriers like Allstate and State Farm are trained to minimize payouts, and they have a standard playbook of excuses they use to deny and underpay your Additional Living Expenses (ALE) claim.

Their goal is brutally simple: wear you down until you accept a settlement that saves them money.

Recognizing their tactics is the first step to beating them at their own game. An adjuster’s excuse isn’t a final decision; it’s an opening jab in a negotiation you need to be ready to win.

![]()

Dismantling Their Favorite Excuses

The insurance company's adjuster is banking on you not knowing the true power of your own policy. They'll throw out vague rejections, hoping you won't push back. Here are the most common excuses we see every day and how to tear their arguments apart:

- Excuse 1: "Your rental isn't comparable to your home's value." They're trying to shove you into a smaller, cheaper, or less convenient property to save a buck. Your counterargument is that "comparable" means maintaining your standard of living. That includes size, quality, and location—and it absolutely includes keeping your kids in their school district.

- Excuse 2: "You could have found a cheaper hotel." This is a classic lowball tactic. Your defense is to prove the hotel you chose was the most reasonable and available option at the time of the disaster, when your choices were likely few and far between.

- Excuse 3: "The repairs should be done by now." Insurers love to invent unrealistic timelines to cut off your benefits. The reality is that contractor shortages and supply chain delays are the norm, not the exception. A public adjuster crushes this excuse by providing documented proof from your contractors and suppliers showing the actual timeline, not the insurer's fantasy version.

Case Study: Defeating an Unreasonable Denial

A family in North Carolina we represented faced this exact battle after a fire. Their insurer, a major national carrier, flatly refused to cover their temporary rental home, claiming it was "too luxurious" and not necessary. The adjuster’s brilliant alternative? A cramped apartment 45 minutes away from their children's school.

This wasn't about luxury; it was about giving a family in crisis a shred of stability. The insurer’s offer would have forced the kids to change schools or endure a three-hour commute every single day. It was a clear-cut, bad-faith attempt to save money at our client’s expense.

We didn't just argue with them—we buried them in undeniable evidence. Our team at For The Public Adjusters, Inc. conducted a complete market survey of every available rental property inside the family's school district. We proved their chosen rental was not only reasonably priced for that specific area but was one of the only properties available that met their needs without destroying their children's lives.

Faced with cold, hard proof, the insurance company had nowhere to hide. They reversed their denial and paid the full rental cost for the entire time it took to rebuild the home.

How a Public Adjuster Puts You Back in Control

When a disaster makes your home unlivable, the last person you want to trust is the insurance company's adjuster. Let's be blunt: their job isn't to help you. Their job is to protect their employer’s profits. That’s a massive conflict of interest that leaves you stressed, vulnerable, and at risk of getting a lowball offer for your homeowners insurance loss of use coverage.

Hiring a public adjuster from For The Public Adjusters, Inc. completely flips that power dynamic. We work for you and only you, the policyholder. We are your advocate, your expert, and your shield against the insurance company’s classic delay-and-deny tactics.

Taking Command of Your ALE Claim

From the moment we step in, we take control of the entire process. We don't sit back and wait for the company adjuster to dictate the terms. We immediately launch our own investigation, making sure every single detail is documented to get you the maximum recovery you're entitled to.

Here’s how we do it:

- A Complete Policy Analysis: We tear through the fine print of your policy to find every ounce of coverage you’ve paid for, often uncovering benefits the company adjuster would conveniently forget to mention.

- An Independent Damage Assessment: We conduct our own hands-on, thorough inspection of the damage. This allows us to build a detailed scope of loss that shows what it will actually take to make you whole again.

- Forecasting Your ALE Needs: We create a realistic, long-term forecast of your Additional Living Expenses. We account for everything from temporary housing to increased food bills and transportation costs.

- Handling All Negotiations: We take over all communication with the insurance company. No more stressful phone calls or intimidating emails for you. We fight the battles so you can focus on your family.

To get a better handle on our role, you can dig into our detailed guide on what a public adjuster does and how we go to bat for homeowners like you.

Success Story: A Five-Fold Increase for a North Carolina Family

A family in North Carolina lost almost everything in a house fire. Their insurer—a huge, national corporation—came in fast with a tiny ALE settlement. It wouldn't have even covered two months of rent in their area. They were devastated and felt completely powerless.

That's when they called us.

Our team at For The Public Adjusters, Inc. immediately reopened the claim and went to work. We meticulously documented thousands of dollars in expenses the insurance company had just dismissed out of hand—things like laundry services, extra mileage to get to work from the temporary rental, and even fees for boarding their pets.

We built an ironclad case proving the insurer’s offer wasn't just low—it was an act of bad faith. After some intense negotiations, we secured a final payout that was five times the original offer. This gave the family the financial security to live comfortably while their home was rebuilt, turning an absolute nightmare into a manageable recovery.

This is the control a public adjuster gives you. We level the playing field, making sure you get the full and fair settlement you are owed under your policy. Period.

Answering Your Questions About Loss of Use Disputes

When your life gets turned upside down by a disaster, the last thing you need is your insurance company playing games with your homeowners insurance loss of use coverage. When they start pushing back, you’re bound to have urgent questions.

Here are the straightforward answers to the most common disputes we see homeowners in North Carolina and Virginia get dragged into—and how to fight back.

My Insurer Cut Off My ALE Payments, but My Home Is Still Unlivable. What Can I Do?

This is a classic pressure tactic, plain and simple. The insurance company invents an arbitrary timeline for repairs, conveniently ignoring the real-world delays they often create themselves—like lowballing the scope of work so badly that no reputable contractor will touch the job.

This isn't just unfair; it's a strategy designed to back you into a financial corner, hoping you’ll give up and accept less.

Your first move is to formally dispute their decision in writing. Better yet, have a public adjuster take over the fight. We build an undeniable case using detailed contractor schedules, supply chain documents, and expert reports to prove the home remains uninhabitable. We force them to turn the payments back on, just like the policy says they have to.

The Adjuster Says My Restaurant Bills Are Too High. How Do I Prove They Are Reasonable?

Your policy isn't there so you can live on ramen noodles for six months. It’s there to help you maintain your normal standard of living. If your temporary rental doesn't have a kitchen, eating out isn't a luxury—it’s a necessity created by the disaster.

The company adjuster is betting you won’t have the records to prove your costs are legitimate.

We shut that down by building a clear financial picture. We help you document your pre-loss spending on groceries and dining out, then stack it up against your current food bills. When you present them with organized, hard data, it becomes nearly impossible for them to claim the increase is "unreasonable."

Can I Hire a Public Adjuster After My Claim Was Already Underpaid or Denied?

Yes, absolutely. A huge number of our clients come to us after their insurance company has already made a terrible, unfair decision. It is never too late to fight for what you are rightfully owed. We are experts at reopening and fixing poorly handled claims.

We dive in and find the critical evidence their adjuster conveniently ignored, re-evaluate the entire loss from scratch, and negotiate a supplemental payment for the full amount you should have gotten from day one. An initial denial or lowball offer is just the start of the fight, not the end.

An insurer’s denial is not a final verdict. It is an opening offer in a negotiation you were never prepared for. A public adjuster levels the playing field, ensuring you have an expert fighting for your interests, not the insurance company's bottom line.

My Insurer Offered a Hotel Far From My Kids' School. Do I Have to Accept It?

No, you do not. Your ALE coverage is for a "comparable" standard of living, and that absolutely includes the location. Forcing your family into a terrible commute that disrupts your kids' schooling is a classic bad-faith tactic.

Their goal is to make your temporary life so miserable that you'll accept a quick, cheap settlement just to get back into your half-repaired home.

A public adjuster will immediately reject their nonsense offer. We find appropriate housing that actually meets your family’s needs and then bill the full, proper cost back to the insurer.

If you're facing a dispute over your loss of use coverage in North Carolina or Virginia, you don't have to fight the insurance company alone. At For The Public Adjusters, Inc., we handle the entire claims process, from documentation to negotiation, to secure the fair settlement you deserve. Contact us today for a no-cost claim review.