Trying to get your head around a homeowners insurance policy can feel like you’re reading a foreign language. But once you strip away the jargon, it’s really just a promise: a promise from an insurance company to help you get back on your feet after a disaster.

It’s your financial backstop for when things go sideways. Let’s get an understanding homeowners insurance coverage.

Your Homeowners Policy Explained in Simple Terms

Forget the dense legal contract for a second. Think of your homeowners policy as a financial shield for the biggest investment you’ll likely ever make. Sure, your mortgage lender probably made you buy it, but that’s not its real job. Its real job is to give you peace of mind and keep a bad day from turning into a financial catastrophe.

Getting a handle on the basics is everything. It’s what gives you the confidence to deal with the chaos, whether it’s a kitchen fire that gets out of hand, a storm that drops a tree on your roof, or a guest who takes a nasty spill on your front steps. The right coverage is the line between a manageable problem and a life-altering setback.

The Core Purpose of Homeowners Insurance

At its most basic level, your policy is a simple trade. You pay a regular fee, which is called a premium, and in exchange, the insurance company agrees to pay for covered damages if something unexpected happens. In the insurance world, these “unexpected events” are called perils.

A lot of people think homeowners insurance covers absolutely everything that could go wrong. It doesn’t. It only covers the specific risks listed in your policy, which is why you have to know what’s in and what’s out.

The whole point is to put you back in the same financial spot you were in before the loss. It’s a way of spreading out the risk, so one homeowner doesn’t have to shoulder the entire cost of a disaster alone.

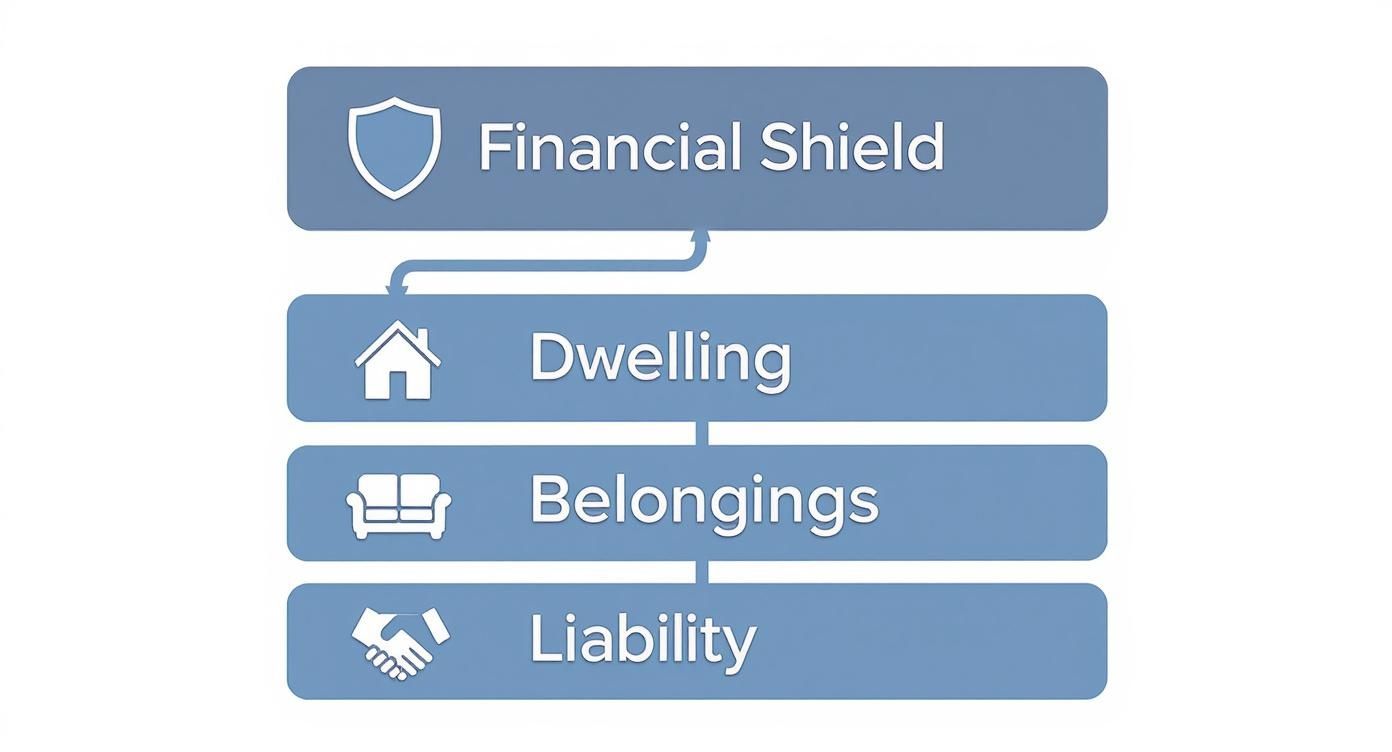

What Your Policy Generally Protects – Understanding Homeowners Insurance Coverage

A standard homeowners policy isn’t one single thing; it’s actually a bundle of different coverages rolled into one package. Each part has a specific job to do. We’ll get into the nitty-gritty later, but for now, just know that your policy protects three main areas:

- Your Home’s Structure: This is the house itself—the foundation, the walls, the roof. It also includes things that are attached, like your plumbing and electrical systems. This is officially known as dwelling coverage.

- Your Personal Belongings: This is all your stuff inside the house. Think furniture, clothes, electronics, and pots and pans. Basically, anything that isn’t nailed down. This part is called personal property coverage.

- Your Personal Liability: This is your financial protection if you’re found legally responsible for injuring someone or damaging their property. A classic example is a visitor slipping on your icy walkway and suing you.

When you see it broken down like this, the policy starts to make a lot more sense. It’s not just one confusing document; it’s a collection of specific protections working together to keep you safe. This is the foundation you need to really understand what you’re paying for.

Decoding the Six Core Components of Your Coverage

When you look at your homeowners insurance policy, it’s easy to see it as one big, complicated safety net. But that’s not quite right. It’s actually a package of six different types of coverage, all bundled together, with each one designed to protect a specific part of your world.

Think of it like a first-aid kit. You have different supplies for different injuries—bandages for a cut, ice packs for a sprain. Your policy works the same way, using different “tools” (labeled Coverage A through F) for different disasters. Once you understand what each part does, the policy stops being confusing and starts looking like what it is: your financial recovery plan.

The infographic below gives you a bird’s-eye view of how these pieces fit together, protecting your home, your stuff, and you for understanding homeowners insurance coverage.

As you can see, it all boils down to three main jobs: protecting the building, protecting your belongings, and protecting you from getting sued.

Coverage A: Dwelling Protection

This is the big one—the absolute heart of your policy. Dwelling Coverage, or Coverage A, protects the physical structure of your house. We’re talking about the roof, the walls, the foundation, and anything permanently bolted down, like your plumbing, electrical system, and built-in appliances.

If a nasty hailstorm punches holes in your roof and siding, the money to repair that damage comes from your Dwelling Coverage. This coverage is based on your home’s replacement cost value (RCV), which is what it would cost to rebuild your home from scratch today, not what you could sell it for.

Coverage B: Other Structures

Got a shed out back? A detached garage? A fence? That’s where Other Structures Coverage, or Coverage B, steps in. It’s specifically for any structure on your property that isn’t physically attached to the main house.

Let’s say a heavy snow load causes your detached garage to collapse. The cost to rebuild it would be covered here. As a rule of thumb, this coverage is usually set at 10% of your main Dwelling Coverage. So, if your house is insured for $400,000, you’ll have about $40,000 to cover your other structures.

Coverage C: Personal Property

Now we get to your stuff. Personal Property Coverage (Coverage C) is for everything you own inside the house. The easiest way to think about it is this: if you could flip your house upside down and shake it, everything that falls out is your personal property.

This includes your furniture, clothes, electronics, and pots and pans. It even covers your belongings when they’re not at home, like if your laptop gets stolen from your car.

One of the biggest mistakes people make while understanding homeowners insurance coverage is guessing how much their stuff is worth. Take the time to create a home inventory. It’s the single best way to prove what you lost and make sure you have enough coverage to replace it all.

This coverage is typically 50% to 70% of your Dwelling Coverage. Just be aware that policies have special, lower limits on high-value items like jewelry, firearms, or art. If you own expensive pieces, you’ll need to add a special endorsement to insure them for what they’re actually worth.

Coverage D: Loss of Use

A disaster doesn’t just damage your home; it can kick you out of it. If your house becomes unlivable during repairs, where do you go? That’s the problem Loss of Use Coverage—often called Additional Living Expenses (ALE)—is meant to solve.

This part of your policy pays for the extra costs you rack up while you can’t live at home. This can include:

- A hotel room or a short-term rental.

- The cost of eating out if you don’t have a kitchen.

- Laundry services, storage unit fees, or even pet boarding.

The key here is that it helps you maintain your normal standard of living. If a pipe bursts and floods your first floor, forcing you into a hotel for two weeks, Loss of Use keeps that unexpected expense from turning into a financial catastrophe.

To give you a clearer picture of understanding homeowners insurance coverage, here’s a quick summary of the main coverage types we’ve discussed so far, plus the two that protect you from liability.

Standard Homeowners Insurance Coverage At a Glance

| Coverage Type | What It Protects | Common Example |

|---|---|---|

| A: Dwelling | The physical structure of your house. | A fire damages your kitchen and roof. |

| B: Other Structures | Detached structures like garages, sheds, or fences. | A tree falls and crushes your garden shed. |

| C: Personal Property | Your belongings, like furniture and electronics. | A burglar steals your TV and computers. |

| D: Loss of Use | Extra living expenses if your home is uninhabitable. | Paying for a hotel while your home is repaired. |

| E: Personal Liability | Your assets if you’re sued for injury or property damage. | A visitor slips on your icy steps and sues you. |

| F: Medical Payments | Minor medical bills for guests injured on your property. | A neighbor’s child gets a cut and needs stitches. |

This table shows how each piece of the puzzle works together to provide complete protection. Now let’s dive into the last two critical components.

Coverage E: Personal Liability

Your responsibility doesn’t end at your front door. Personal Liability Coverage, or Coverage E, is your financial shield if you or a family member accidentally hurt someone or damage their property. It protects your assets from being wiped out by a lawsuit.

For instance, if your dog gets loose and bites the mail carrier, who then sues you for their medical bills and pain and suffering, your liability coverage is what pays for your legal defense and any settlement. Most standard policies offer $100,000 to $300,000 of protection, but it’s often smart to consider more, especially with an umbrella policy.

Coverage F: Medical Payments to Others

Think of this one as “goodwill” coverage. Medical Payments to Others (Coverage F) is a small pot of money set aside to cover minor medical bills if a guest is injured at your home, no matter who was at fault.

If a friend trips on a rug in your living room and sprains their ankle, this coverage can pay for their visit to urgent care. The limits are usually low, around $1,000 to $5,000, but the goal is to resolve small incidents quickly and amicably, hopefully preventing them from escalating into a bigger liability claim.

How Policy Limits, Deductibles, and Premiums Work

The best way to understanding homeowners insurance coverage is to think of your homeowners insurance policy as a balancing act, a financial seesaw with three key parts. On one end, you have your premium—that’s the regular payment you make to keep the policy active. On the other end are your deductible and your coverage limits.

These three pieces are constantly working together. Tweak one, and the others almost always shift in response. Nailing this balance is everything. It’s the difference between paying for coverage you don’t need and finding yourself dangerously underinsured when a crisis hits.

The Balancing Act of Premiums and Deductibles

Your deductible is simply the amount of money you agree to pay out-of-pocket for a claim before your insurance company steps in. It’s your skin in the game.

Let’s say a storm blows through and causes $10,000 in roof damage. If your policy has a $1,000 deductible, you pay that first $1,000, and the insurance company covers the remaining $9,000.

This is where the trade-off happens. If you’re willing to take on more of the initial risk with a higher deductible, your insurer rewards you with a lower premium.

- Higher Deductible: You pay less every month (lower premium), but you’ll have a bigger bill to pay yourself if you ever need to file a claim.

- Lower Deductible: You pay more every month (higher premium), but your out-of-pocket costs will be much smaller when you need to use your insurance.

Choosing the right deductible really comes down to your personal financial situation. A good rule of thumb is to pick the highest deductible you could comfortably pay tomorrow without it causing a major financial strain.

Understanding Your Coverage Limits

While your deductible is what you pay first, the coverage limit is the absolute maximum amount your insurance company will pay out for a specific loss. Every part of your policy—Dwelling, Personal Property, Liability—has its own limit.

For the structure of your house (Dwelling Coverage), this limit needs to be based on its replacement cost value (RCV). This is a critical point.

Replacement cost is what it would take to rebuild your home from the ground up with similar materials at today’s prices. It has nothing to do with your home’s market value (what you could sell it for) or its actual cash value (which subtracts depreciation). To really dig into this, check out our guide on why ACV vs. RCV matters for your claim.

If your dwelling coverage is too low, you could face a huge financial gap after a total loss. Insurance companies have software to estimate this, but you should always double-check that it accounts for local construction costs and any major upgrades you’ve made.

Different Types of Deductibles

Not all deductibles are created equal. Your policy can have a few different types, and you need to know which ones apply to you before a disaster strikes. Understanding homeowners insurance coverage deductibles will help you determine if it’s worth filing a claim or not.

- Standard Dollar Amount: This is the most common kind—a fixed amount like $1,000 or $2,500 that applies to typical claims like fire or theft.

- Percentage-Based Deductibles: These are a different beast entirely. They’re common for specific events like hurricanes, wind, or hail, and they are calculated as a percentage of your home’s total insured value (usually 1% to 5%).

For example, if your home is insured for $400,000 and has a 2% hurricane deductible, you’d be on the hook for the first $8,000 of any hurricane claim. That can be a nasty surprise if you’re not prepared. Always read your policy’s declarations page to see exactly what you’re dealing with.

Common Exclusions: What Your Policy Will Not Cover

There’s nothing worse than filing an insurance claim, fully expecting a check, only to find out the damage isn’t covered. A standard homeowners policy is a powerful tool, but it’s not a magic shield against every possible disaster. So, understanding homeowners insurance coverage is key.

Understanding what your policy intentionally leaves out—the exclusions—is just as crucial as knowing what it includes. Think of it this way: your policy is a list of promises, and the exclusions section is the rulebook that sets the boundaries.

Uncovered Perils You Need to Know

Most standard homeowners policies are built to cover sudden and accidental damage. But certain large-scale or preventable events are almost always left out and require you to buy separate, specialized insurance.

Here are the big ones to watch out for:

- Floods: This is the most common shocker for homeowners. Damage from rising water—whether from a storm surge, overflowing river, or torrential rain—is not covered. You absolutely need a separate flood insurance policy, which you can often get through the National Flood Insurance Program (NFIP).

- Earthquakes: Ground movement, including tremors, landslides, and sinkholes, is another standard exclusion. If you live in a seismically active area, you’ll need to purchase a standalone earthquake policy to be protected.

- Sewer Backup: The damage from water backing up through your sewers or drains is a messy and expensive surprise. While some policies might offer a tiny bit of coverage, most require you to add a specific endorsement (an add-on) for any real protection.

Knowing these gaps exist is the first step toward building a real safety net for your home.

Why Maintenance Issues Are Your Responsibility

Your insurance policy is there for unexpected disasters, not to pay for the routine costs of being a homeowner. This is a critical distinction. Any damage that results from a lack of maintenance or general wear and tear will be consistently excluded.

An insurance policy isn’t a home warranty. It won’t pay to fix a leaky faucet that has been dripping for months, but it will cover the sudden and accidental water damage if that faucet abruptly bursts.

Insurance companies expect you to keep your home in good working order to prevent problems before they start. If your 25-year-old roof fails simply due to age, the repair costs are on you. The same goes for damage from pests like termites, mold that grows over time due to poor ventilation, or a foundation that cracks from gradual settling. These are all considered maintenance issues.

Filling the Gaps with Endorsements

The good news? You’re not completely powerless against these exclusions. You can customize your policy by adding endorsements, also known as riders, to fill specific coverage gaps. These are small, add-on policies that broaden your protection for an extra premium.

Some of the most common endorsements to consider are:

- Water Backup and Sump Pump Overflow: This adds coverage for that nasty damage caused by backed-up sewers, drains, or a failed sump pump.

- Scheduled Personal Property: If you own expensive jewelry, art, or firearms, this provides higher, specific coverage that goes way beyond your standard policy limits.

- Identity Theft Protection: This helps cover the costs of restoring your identity after a theft, including legal fees and even lost wages.

Taking the time to review what’s not covered is one of the smartest things you can do as a homeowner. For a deeper dive into one of the most common issues, you can learn more about how homeowners insurance covers water damage and the key differences between various types of water-related claims. This knowledge lets you get ahead of your home’s unique risks and make sure you’re truly protected.

How Climate and Economic Forces Shape Your Rates

You’ve been the perfect policyholder. You pay on time, every time, and have never filed a claim. So why in the world did your homeowners insurance rate just spike at renewal?

It’s a totally valid and frustrating question. The answer, however, often has less to do with you and everything to do with massive forces completely outside your control.

Your premium isn’t just a number based on your personal risk. It’s deeply connected to huge, tangled systems of climate and economics that are shaking the entire insurance industry. When those systems get volatile, homeowners everywhere feel the aftershocks in their wallets.

The Growing Impact of Climate Risk

One of the biggest culprits driving up insurance costs is the brutal one-two punch of more frequent and more severe natural disasters. It’s not just your imagination; climate change is fueling stronger weather events, from hurricanes battering the coasts to wildfires tearing through areas once considered safe.

These catastrophes trigger staggering losses for insurance companies. When an insurer pays out billions in claims after a major storm, they have to replenish those funds to be ready for the next one. They do this by re-evaluating risk across their entire portfolio and adjusting premiums for everyone—not just the people who were hit.

This new reality is creating a tough market. For instance, many homeowners who bought insurance just a few years ago saw their premiums jump by nearly 70% at their recent renewal. These kinds of hikes are a direct result of these market-wide ripple effects. Globally, extreme weather caused over $2 trillion in economic losses in the last decade alone. If you want to dive deeper, the 2025 personal lines insurance market outlook offers more insight into how these factors are connected.

Think of it like this: insurance works because everyone chips into a giant pool of money. When a massive disaster drains a huge chunk of that pool, everyone has to contribute a little more to fill it back up. You’re not just paying for your own risk; you’re paying to keep the whole system afloat so it can handle widespread disasters.

Economic Pressures on Rebuilding Costs

At the exact same time, the global economy is throwing fuel on the fire. The cost to actually rebuild a house after it’s been damaged has gone through the roof, thanks to two main issues: inflation and supply chain nightmares.

These economic problems hit your “replacement cost” value—the foundation of your Dwelling Coverage—right where it hurts. Here’s how it works:

- Skyrocketing Material Costs: The price of basics like lumber, roofing materials, and even copper wiring has become wildly unpredictable and far more expensive.

- Skilled Labor Shortages: Finding qualified construction workers is harder and costs more than ever, which drives up the total price tag for any repair or rebuild project.

When it costs more to rebuild a home, the potential payout for the insurer also goes up. To cover that bigger financial risk, they have no choice but to raise premiums. In the end, your rate is a direct reflection of what it would cost to put your home back together in today’s economy.

You might think your homeowners insurance is just a deal between you and a local agent, but that’s only a tiny piece of the picture. The truth is, your policy is tied into a massive, planet-spanning system where a disaster on the other side of the world can make your premium go up.

It’s all connected. Think of it like one giant, global pool of money set aside for disasters. When historic wildfires scorch California or a super typhoon slams into Asia, the financial hit is enormous. Those losses create ripples that spread across the entire system, eventually reaching your wallet—even if your own home was perfectly safe.

How “Insurance for Insurers” Hits Your Bottom Line

So, how does this actually happen? The main driver is a system called reinsurance. You can think of it as insurance for your insurance company. Your local provider buys a reinsurance policy to protect itself from a catastrophic event, making sure it has enough cash to pay everyone’s claims after a disaster without going belly up.

These reinsurance companies are global giants, covering claims from floods, hurricanes, and earthquakes everywhere. When they have to pay out billions for a disaster in one corner of the world, they have to raise their own prices to rebuild their funds. That means your local insurer suddenly has to pay more for its own protection, and you can bet that extra cost gets passed right down to you as a higher premium.

It sounds strange, but a major hurricane hitting Florida can directly cause a premium hike for a homeowner in a quiet, landlocked state. It all flows through the global reinsurance market, which balances risk across the entire planet to keep the system from collapsing.

Why Your Zip Code Is Under a Microscope

Global events are one thing, but regional risks are where things get personal. Insurers use incredibly sophisticated models to predict the odds of a disaster hitting your specific area, and those predictions dictate what they’ll cover and how much they’ll charge. The North American hurricane season, for example, is something underwriters watch like a hawk every single year.

If forecasters predict an active season, insurers don’t wait for a storm to form. They start tightening their rules, raising deductibles, and increasing premiums for coastal homeowners immediately. This is why someone in a hurricane-prone part of North Carolina sees a totally different insurance bill than someone living in the mountains. For instance, the hurricane season, which runs from June 1 to November 30, is a massive factor in pricing. We’re also seeing trends where U.S. casualty insurance rates jumped by 8%, driven by the rising cost of claims, even as global property rates dipped slightly. You can discover more about these global market trends to see how it all connects.

This really gets to the core of understanding homeowners insurance coverage: your personal situation is just one part of a much larger, more complicated puzzle. Global financial markets and regional disaster models are the invisible forces shaping the policy you buy and the price you pay.

Homeowners Coverage Questions We Hear All The Time

Even when you’ve got the basics down, homeowners insurance can still throw a few curveballs. Certain questions just seem to pop up again and again when people are trying to figure out their policies.

Let’s walk through some of the most common ones to clear the air and give you some real-world clarity.

What Is The Difference Between RCV and ACV?

This is one of the big ones, and getting it wrong can cost you thousands. The difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV) is huge.

Think of it this way: RCV is the money you need to go out and buy a brand-new replacement for what you lost. ACV, on the other hand, is what your stuff was worth the second before it was destroyed, after years of wear and tear.

Let’s say a fire takes out your five-year-old couch.

- RCV gives you the money to buy a new, similar couch at today’s prices.

- ACV gives you the cash value of a used, five-year-old couch.

You can see why most homeowners want RCV coverage. It’s the policy that actually gives you enough money to rebuild your life without having to dig deep into your own pockets.

Does My Policy Cover a Home-Based Business?

Probably not. And this is a trap a lot of people fall into. Your standard homeowners policy is designed for personal living, not for commerce.

It might offer a tiny sliver of coverage for business equipment, often capped at a mere $2,500. But when it comes to the big risks—like someone getting hurt in your home office (liability) or covering your lost income—it offers next to nothing.

If you’re running a business out of your house, you absolutely need to look into a separate business policy or add a special endorsement to your current plan. Don’t assume you’re protected.

How Do Home Improvements Affect My Insurance?

Putting in a new kitchen or building a deck is great for your home’s value, but it also instantly makes your house more expensive to rebuild. This means your old insurance limit might not be high enough anymore.

It is absolutely critical to call your insurance agent after any major upgrade. They’ll need to bump up your dwelling coverage to match the new, higher value of your home. If you skip this step, you could find yourself dangerously underinsured after a total loss.

When the stakes are high after a major upgrade and a claim, it can be a smart move to see what a public insurance adjuster can do for you to make sure every detail is accounted for correctly.

At For The Public Adjusters, Inc., our job is to dive deep into your policy and fight for the full, fair settlement you’re owed. If you’re dealing with a property damage claim in North Carolina or Virginia, visit us at https://forthepublicadjusters.com for a no-cost claim review.

Trackbacks/Pingbacks