Yes—a public adjuster’s name can go on your insurance check, but it depends on the situation.

When is public Adjuster on check?

- You signed a contract with the public adjuster

- The contract allows them to be listed as a payee

- They want to ensure their agreed fee (percentage of the claim) is paid

In this case, the insurance company may issue the check to You + Public Adjuster, or You + Mortgage Company + Public Adjuster

What it means for you – If they’re on the check, you’ll need their endorsement/signature to deposit it. They’ll receive only their percentage, not control the full payout.

It’s understandable why that rattles people. You’ve got a damaged home or business, contractors waiting, bills stacking up, and an insurance company that already dragged its feet. Now they’ve added another obstacle between you and your money. If you’re staring at a public adjuster on check issue right now, the important thing is this: don’t panic, and don’t sign blindly. The way this check is structured can either protect your claim or help the carrier shut it down early.

The Check Arrived But The Fight Isn’t Over

The check is in your hand, but that doesn’t mean the insurance company has suddenly become reasonable.

For homeowners and business owners, the worst moment often isn’t the day of the loss. It’s the day the carrier sends a payment that looks official, feels urgent, and introduces a new problem. You need repair money now. The insurer knows that. They also know confusion makes people sign fast.

What throws people off

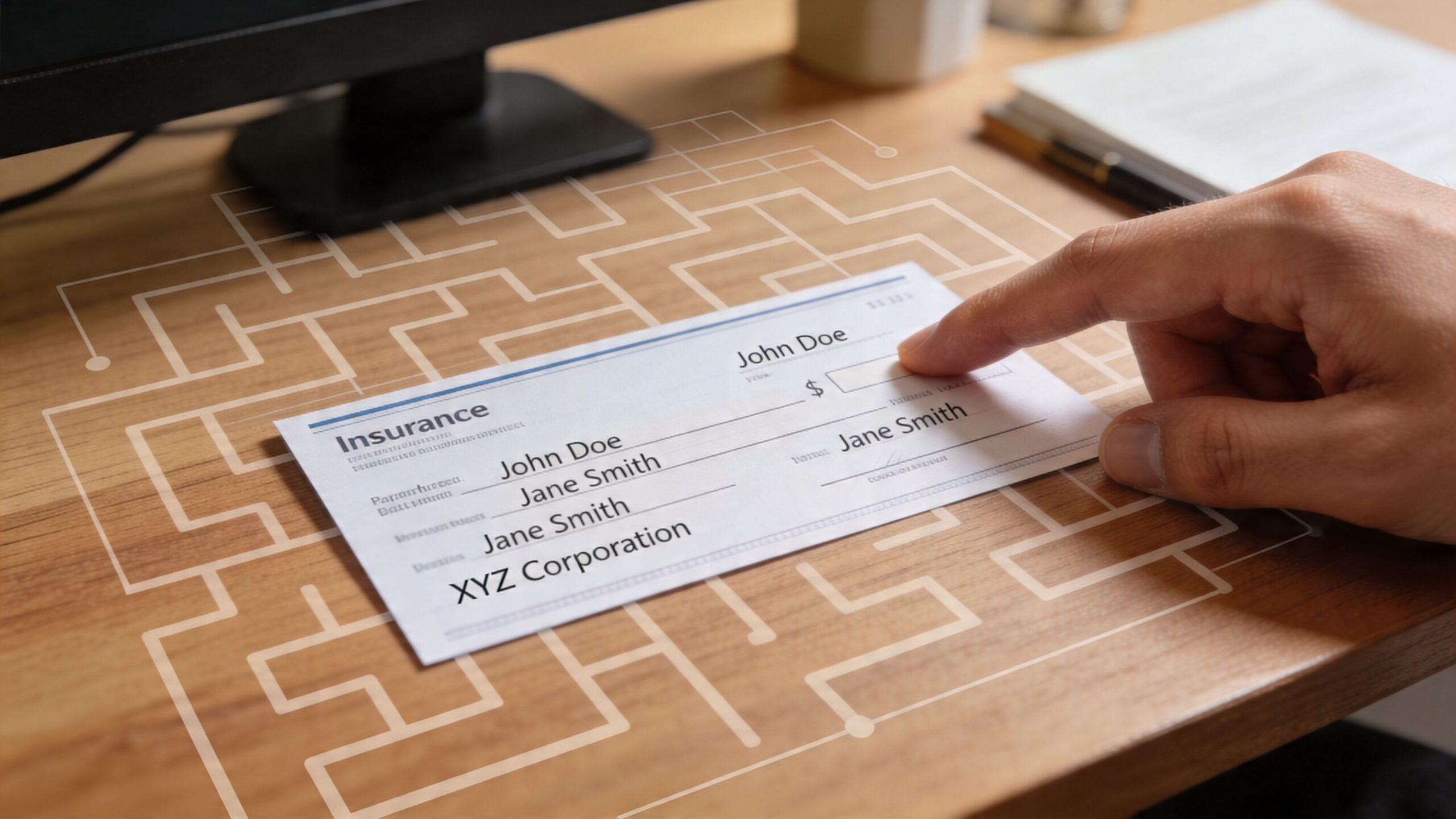

A joint check raises immediate questions:

- Can I deposit this alone: Usually not, if multiple payees are listed.

- Why is my public adjuster on my check: Because the payment process is tied to the representation agreement and the claim work that got the money released.

- Does “final payment” mean I’m done: Not always, and treating it that way can cost you.

That last point matters. A lot of policyholders think cashing a check ends only that payment. In practice, carriers often use payment language to pressure you into accepting a smaller claim resolution than the damage supports.

Why this feels like a control move

It is a control move.

Insurance companies like State Farm and Allstate don’t mind making the process look messy if that mess helps them close the file. A joint-payee check slows access to funds. A “final” notation creates doubt. A vague cover letter shifts risk onto you. None of that helps you rebuild faster.

Practical rule: A check is not just money. It’s a negotiation document.

This aspect is commonly overlooked. The check itself can hold considerable sway. If the amount is low, if damage is still unresolved, or if the carrier is trying to box you into closure, the payment has to be reviewed as carefully as the estimate.

When a public adjuster on check appears, don’t treat it like an error. Treat it like a pressure point in an active claim dispute.

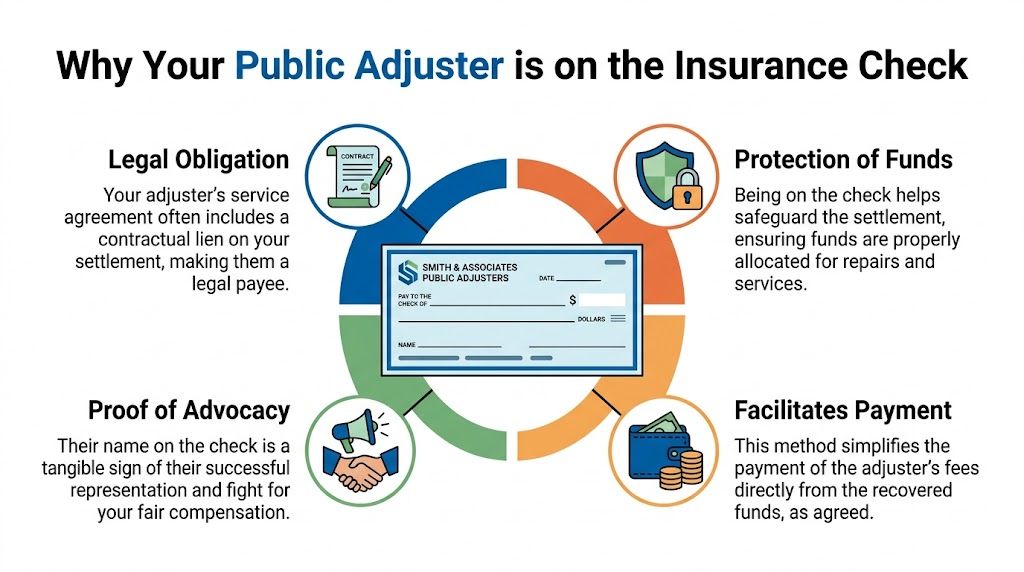

Why Your Public Adjuster Is On The Insurance Check

You fought through inspections, estimates, delays, and excuses. Then the check shows up with your name and your public adjuster’s name on it. That is not clerical noise. It is the insurance company acknowledging that you have representation and that they cannot shut your adjuster out at the money stage.

That matters because the payment stage is where control shifts. If the carrier sends funds only to you, it gets one more chance to pressure, confuse, or rush you into accepting less than the claim is worth. Putting your public adjuster on the check keeps your advocate in the room when the carrier would rather deal with you alone.

The legal and contractual reason

A public adjuster gets named on the check because the carrier has notice of your representation agreement and the fee arrangement tied to the claim. In North Carolina, the Department of Insurance explains that joint payment is common in these claims and is tied to how public adjusters are paid under their contracts with policyholders (North Carolina Department of Insurance guidance on claims and adjuster information).

The point is straightforward. Your adjuster does not get named because the insurer is doing them a favor. The adjuster is on the check because the insurer knows someone is watching the numbers, the wording, and the release language.

If you need the basic role spelled out, this guide on what a public adjuster does covers the claim work behind that representation.

Why this protects your position

A joint check protects your position in a live claim dispute. It keeps the carrier from trying to separate the payment from the advocacy that got the payment issued in the first place.

That protection shows up in a few practical ways:

- It keeps your adjuster involved at the money stage. The carrier cannot quietly send funds and hope you cash them without questions.

- It reduces the chance of side deals. Once you have representation, the insurer should not be trying to work around it with direct pressure.

- It ties payment to the written agreement. That cuts down on later fights over what your adjuster earned and when.

This is about control. The insurer wants a clean path to close its file. You want a fair path to collect what the policy owes. Those goals are not the same.

What it does not mean

Your public adjuster being on the check does not mean the adjuster owns the settlement funds. It means the payment has to be handled according to the representation agreement and endorsed correctly.

A good adjuster explains that process in plain English. Who signs. Where the check is deposited. How the fee is calculated. What happens if the amount is still disputed. If you are getting vague answers, press for specifics immediately.

The smart read on a joint check is simple. It is a protection device in a contested payment process, and it gives the policyholder more strength against insurer lowball tactics than a direct check ever would.

How Insurers Weaponize The Payment Process

You finally get the check. You think the carrier is done fighting. Then you read the letter, see the payee line, and realize the insurer is still trying to control the claim through the payment itself.

That is not an accident. It is a claims tactic.

The carrier uses friction as a tool against you

A payment should be simple. Insurers make it messy when mess helps them.

They know you need money now. You may be out of your house, trying to keep a business open, or paying mitigation invoices while the claim is still underpaid. So they add delay, confusion, and pressure at the exact moment you are most likely to sign first and ask questions later.

That usually shows up in a few predictable ways:

- Staged payments that break the claim into pieces: This makes it harder to see what has been paid and what is still missing.

- “Final payment” language in letters or check stubs: The carrier wants to frame the dispute as over, even when obvious items remain unresolved.

- Complicated payee lines: More names mean more chances for delay, mistakes, and finger-pointing.

- Silence on open issues: Code upgrades, matching, hidden damage, lost business property, and depreciation often get pushed aside while the insurer pushes the draft in front of you.

This is a control move. The insurer wants the transaction to feel administrative. It is not. The payment stage is part of the negotiation, and if you treat it like routine paperwork, the carrier gains ground.

Lowball first, then rush the close

A weak payment is often paired with a fast-close strategy.

The first draft is commonly the number the carrier hopes you will accept because you are tired, under pressure, and ready to move on. Then comes the wording that suggests the matter is wrapped up, even though the scope is still disputed. That is why a check can be more dangerous than a denial letter. A denial gets your attention. A check lowers your guard.

Public adjusters see this pattern every day. Carriers understate repair scope, ignore line items that cost real money, and then use the payment process to make that shortfall harder to challenge. If your file also includes reservation-of-rights language or shifting coverage positions, read this explanation of a non-waiver agreement in insurance. That kind of letter often shows the carrier is trying to keep its options open while limiting yours.

Read the payment like a negotiation document

Do not treat the check as a simple transfer of funds.

Treat it like a claim document with consequences. Read the check stub, every enclosure, and every notation. Compare the amount to the current estimate, the known damage, and the unresolved items. If the insurer is still disputing moisture, code compliance, matching, contents, ALE, or business interruption, any wording that suggests full settlement should stop you cold.

Here’s a short explainer worth watching before you endorse anything:

If the carrier wants your signature faster than it wants to answer your questions, the payment is serving the insurer, not you.

That is the core issue in a public adjuster on check situation. The draft is not just money. It is a pressure point, and the carrier will use it to steer the outcome if you let it.

Your Action Plan For Endorsing A Joint Check

Don’t rush. A joint check needs a process, not a guess.

The right move is boring and methodical. That’s good. Insurance carriers count on chaos. You beat that by slowing the transaction down and checking every detail before a signature hits the back of the check.

Step one through three

-

Photograph the front and back of the check

Keep a clean record before anyone endorses anything. Save the envelope and every letter that came with it. -

Read every word that came with the payment

Look for “final payment,” “full settlement,” release language, or anything that suggests the carrier is trying to close the claim. -

Send the check copy to your public adjuster immediately

Don’t summarize it by phone only. Send images or scans so the wording, amount, claim number, and payee line can be verified.

What your adjuster should confirm

A competent public adjuster should compare the check against the actual settlement status.

They should answer questions like:

- Is the amount consistent with the latest agreed scope?

- Is the payment partial, supplemental, or allegedly final?

- Are there still open items such as hidden damage, code issues, or depreciation?

- Is a mortgage company also on the draft, and if so, what endorsement sequence applies?

The safest ways to handle endorsement

Not every claim needs the exact same payment flow. Good firms adapt the process, but the process should still be transparent.

A safe approach often looks like this:

| Situation | Best move |

|---|---|

| You want maximum visibility | Endorse at the bank with all parties present if possible |

| The adjuster uses a client-trust process | Get a written breakdown of fee, net funds, and timing |

| The check says “final payment” but damage remains | Hold endorsement until the language and claim status are reviewed |

| The mortgage company is on the check | Confirm lender requirements before anyone assumes quick deposit is possible |

What not to do

Don’t sign first and ask questions later.

Don’t hand the check over without a receipt or written acknowledgment. Don’t let a contractor pressure you to use the payment before the claim issues are sorted out. And don’t assume “final” means untouchable if the carrier still owes for damage it left out.

Bottom line: Endorsement is the last administrative step in a claim stage. It is not a substitute for claim review.

If you’re uneasy, that’s normal. The cure is documentation and clear instructions, not blind trust in the insurer’s paperwork.

Navigating Public Adjuster Rules In North Carolina And Virginia

You open the mail, see the insurance check, and then spot your public adjuster’s name on it. Now the carrier still controls the tempo unless you understand the rules in your state and force the process onto solid ground.

North Carolina and Virginia policyholders need to stop relying on rumors, Facebook advice, and whatever the insurer’s desk adjuster says on a quick phone call. Payment control matters. If a public adjuster is on the check, that is tied to the contract you signed, state licensing rules, and the fee arrangement that governs who gets paid and how.

What matters in North Carolina

North Carolina requires the fee agreement to be in writing. That is the starting point. If your public adjuster expects to be protected on the draft, the contract needs to say so clearly.

That matters because a check is not just money. It is control.

Insurers know many homeowners relax once payment shows up. That is when sloppy contracts, vague fee language, and rushed endorsements create problems the carrier can use to its advantage. If the paperwork is clear, the insurer has less room to play dumb, delay release, or stir up conflict between you and your adjuster.

If you want straight answers on representation, fees, and claim handling, review these public adjuster FAQs.

What NC and VA policyholders should demand

Do not treat state rules like trivia. Use them.

- A clear written contract: The fee percentage, when it applies, and how payment is handled should be spelled out in plain English.

- An active state license: Verify the public adjuster is licensed for North Carolina or Virginia before you sign anything or endorse a check.

- Written fund-handling instructions: You should know who endorses, who deposits, what gets deducted, and when you receive your net funds.

- No carrier-driven pressure: If the insurer is pushing you to sign fast, ask why. Pressure usually shows up when the carrier wants closure before the full scope and payment issues are settled.

The practical takeaway

A joint check in North Carolina or Virginia is not automatically a red flag. Poor documentation is. Weak communication is. An insurer that uses the payment stage to box you into a cheap resolution is.

Handle this like a business dispute, because that is what it is. Read the contract. Verify the license. Get the payment instructions in writing. If any part of that chain is unclear, stop the endorsement process until it is fixed. That is how you protect your claim and keep control of your money.

Success Story A Homeowner’s Fight Against A Lowball Offer

A water loss claim can turn ugly fast.

One homeowner dealing with major interior water damage got the usual insurer routine. The carrier focused on visible damage, minimized the scope, and pushed a payment that didn’t come close to putting the property back the way it should’ve been. Drying, tear-out, hidden moisture, and finish work were all being handled like they were somebody else’s problem.

What changed the claim

The turning point wasn’t the insurer “doing the right thing.” It was proper representation and pressure.

Once the loss was documented correctly, the missing pieces became harder for the carrier to ignore. Moisture concerns behind walls and in adjacent materials had to be addressed. The estimate had to reflect restoration reality, not a desk-adjusted fantasy. And when payment came through, the check itself still had to be reviewed before anyone treated it like the end of the claim.

That sequence matters. A bad estimate often leads to a bad check. A bad check, signed too fast, can lock in a bad result.

Why flood claims are even tougher

NFIP flood claims are even less forgiving than standard homeowners claims.

After Hurricane Idalia made landfall on August 30, 2023, at 7:45 AM EDT near Keaton Beach, Florida, affected policyholders faced a strict 60-day Proof of Loss deadline, which fell on October 29, 2023. Public adjusters help prevent denials by making sure that Proof of Loss submission is timely and accurate under federal flood rules (Hurricane Idalia flood claim deadline and Proof of Loss guidance).

That is where people lose claims they should have been able to pursue. Not because the damage wasn’t real, but because the paperwork standard is brutal.

What real clients notice

When policyholders finally get someone in their corner, the first thing they usually mention isn’t jargon. It’s relief.

The lesson is straightforward. A lowball offer rarely fixes itself. Neither does a confusing payment. When the carrier under-scopes the damage and then sends a restrictive check, you need someone reading every line like your recovery depends on it. Because it does.

Red Flags And Best Practices For Your Protection

The check shows up. Your contractor wants payment. Your family wants repairs started. Then your public adjuster says, “Do not sign anything yet.”

That moment tells you who is protecting your claim and who is trying to control it.

A public adjuster whose name appears on the check holds real influence over how and when money moves. That can protect you from a carrier trying to close the file cheap. It can also create a mess if the adjuster is sloppy, greedy, or evasive. Treat this as a control issue, not a paperwork issue.

Red flags to avoid

Watch for conduct that puts your money at risk:

- Doorstep pressure after a loss: Serious professionals do not rush signatures while you are still in shock, displaced, or cleaning up.

- Murky fee terms: Fee limits can apply in declared emergencies, and the contract should spell out the percentage, what the fee applies to, and when it is earned. If you need a state-specific reference point, review the public adjuster fee and licensing rules published by the North Carolina Department of Insurance.

- No proof of licensing: If they cannot show an active license for the state where the loss happened, stop there.

- Vague answers about the check: You should know who will endorse it, where it will be deposited, what gets paid first, and whether any disputed amount is still being fought.

- Side deals with contractors or vendors: If your adjuster is steering work to a preferred company without full disclosure, your claim can turn into someone else’s payday.

What good representation looks like

A strong public adjuster keeps control where it belongs. With the policyholder.

| Bad actor | Professional advocate |

|---|---|

| Pushes a contract before explaining rights | Walks through the agreement line by line |

| Talks around the fee | Puts every fee term in writing |

| Treats a joint check like a formality | Checks release language and claim status before endorsement |

| Controls communication | Copies you and documents decisions |

| Gets defensive when questioned | Answers clearly and keeps records |

One habit matters more than people realize. Good adjusters leave a paper trail. If a dispute breaks out over the check, the fee, or the scope of loss, written records stop games fast.

Use outside tools when needed

If the claim file is turning into a document pile, get organized before someone uses that confusion against you. Tools like AI legal assistants can help you sort letters, track deadlines, compare contract language, and prepare questions for your adjuster or attorney.

Use tools to stay sharp. Do not use them as a substitute for licensed claim representation.

Your money is too hard-won for blind trust.

Take Control Of Your Claim And Your Check

A public adjuster on check is not the problem. Instead, the problem is an insurance company that wants to control your recovery from start to finish.

When the carrier puts your adjuster on the check, it confirms one thing. You aren’t standing alone while the insurer tries to lowball, delay, or close the claim too early. That joint-payee structure can feel inconvenient, but inconvenience is manageable. An underpaid claim is harder to fix once you sign the wrong document and the file gets pushed toward closure.

If your dispute keeps escalating beyond payment issues, it also helps to understand how post-judgment collection works in the broader legal world. This guide on how to collect on a judgment is useful context for understanding that winning on paper and securing money are not always the same thing.

The point is simple. Review the check. Review the wording. Confirm the claim status. Don’t let the carrier turn urgency into surrender.

If your homeowner or commercial property claim in North Carolina or Virginia has been delayed, denied, or low-balled, get a no-cost review from For The Public Adjusters, Inc.. They represent policyholders, not insurance companies, and they help homeowners and business owners fight for the full amount owed on fire, water, wind, hail, hurricane, tornado, and flood-related property damage claims.