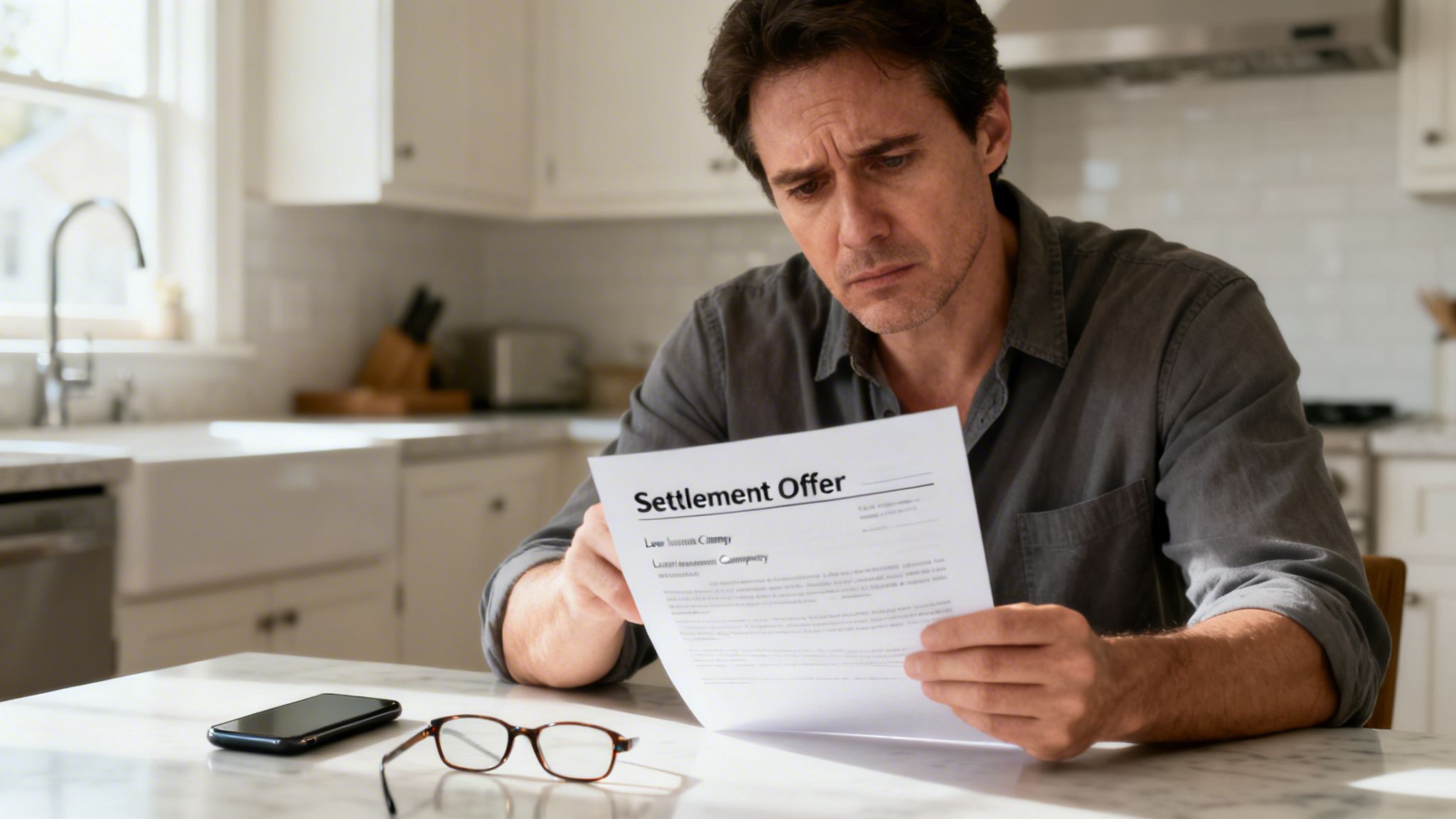

When you file a claim, you're counting on your insurance company to come through for you. But what happens when their settlement offer wouldn't even cover the paint, let alone the repairs? Or when they deny your claim with a flimsy, confusing excuse?

That's not just bad luck. It’s a massive red flag signaling it's time to find homeowners insurance claim lawyers or a public adjuster to step in and fight for the payout you're actually owed.

Recognizing When Your Insurer Is Not On Your Side

After a fire, flood, or hurricane turns your life upside down, the absolute last thing you need is a fight with the very company you've paid thousands to protect your home.

But the hard truth is, for-profit insurance giants like State Farm and Allstate are businesses first. Their primary goal is protecting their bottom line, and that often means minimizing what they pay out to policyholders like you. Their business model thrives on delaying, denying, and low-balling legitimate claims.

Spotting their tactics is the first step to taking back control. You aren't just filing paperwork; you're often walking into a dispute where you need a professional in your corner to level the playing field.

Common Tactics of a Bad Faith Insurer

Insurance companies send out their own adjusters who are trained to look for reasons to deny, delay, or underpay your claim. Learning to recognize their playbook is critical.

Here are the key red flags to watch for:

- Unreasonable Delays: The company goes silent, dragging its feet for weeks or even months without a real explanation. They’re hoping you’ll get frustrated and just give up. If you're stuck waiting, you need to know how to handle it when your insurance company is not responding to your claim.

- Low-Ball Offers: You get a settlement offer that is insultingly low. It doesn't even come close to covering the estimates you’ve gotten from trusted local contractors.

- Misrepresenting Your Policy: The adjuster starts throwing around confusing jargon or citing obscure clauses in your policy to justify a denial. They're banking on the fact that you haven't memorized all 100+ pages of fine print.

- Pressure to Settle Quickly: They push you to sign off on a low offer fast, before you’ve had a chance to get a second opinion or uncover the full scope of the damage.

This experience from Robert Jones highlights a common story. The difference professional representation can make is staggering. When an insurer’s offer feels off, trust your gut—it probably is.

Their adjuster might dismiss your contractor's report, claim some damage was "pre-existing," or bury you in endless, unnecessary paperwork. These aren't the actions of a company doing a thorough job. They are the hallmarks of an insurer actively working against your best interests.

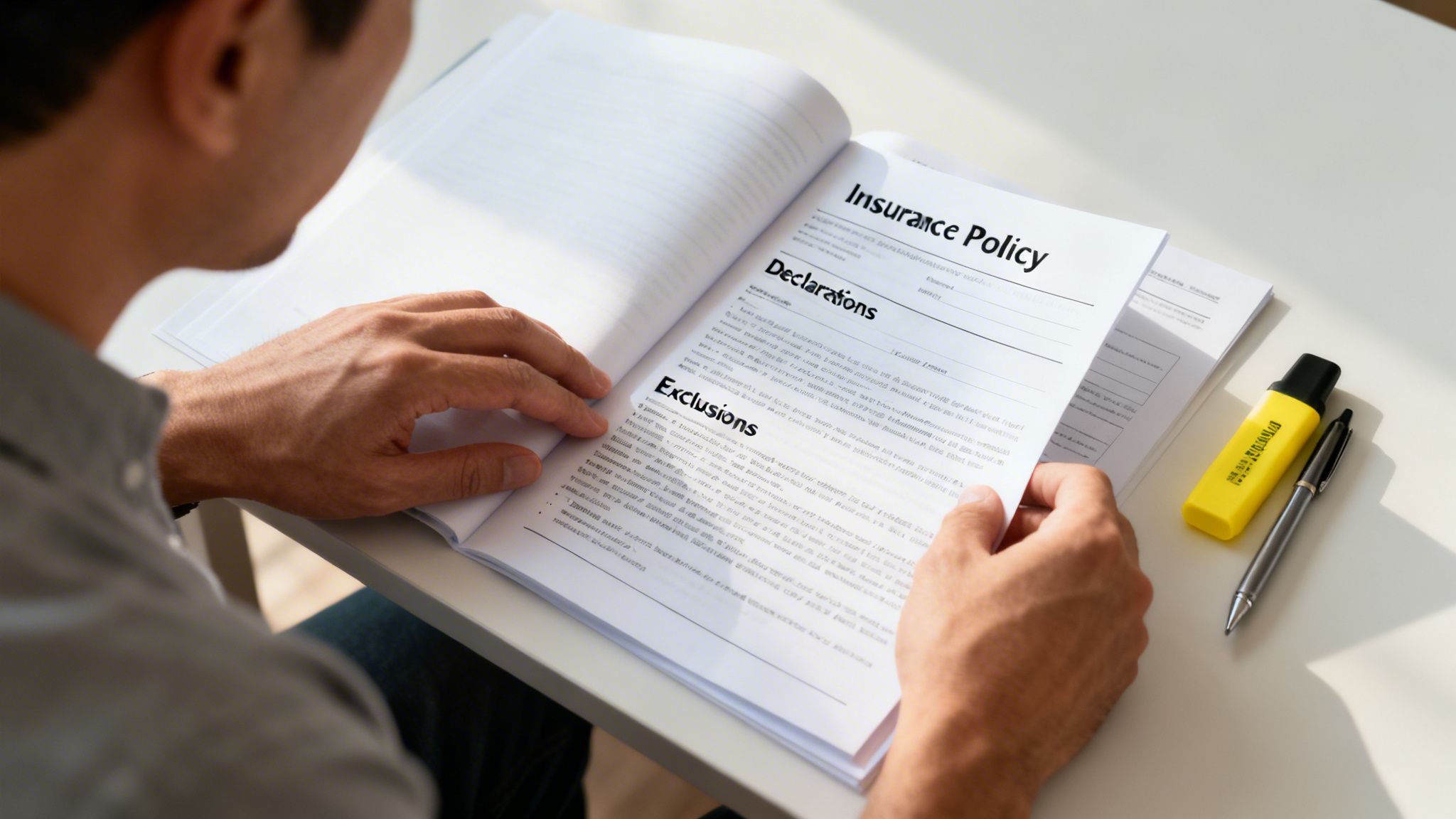

Decoding Your Policy To Fight A Claim Dispute

When you’re staring at a claim denial, your insurance policy—the very thing you bought for protection—suddenly feels like a weapon aimed directly at you. It’s no accident. Companies like State Farm and Allstate have teams of lawyers who spend their days crafting these dense, jargon-filled documents full of loopholes designed to protect their bottom line.

To fight back, you have to turn their weapon into your own. It means digging into that policy, getting past the confusing legal language, and finding the exact phrases and clauses that support your claim. It’s a tough read, but this is where the battle against a low-ball offer begins.

Key Sections To Scrutinize

Forget reading your policy from start to finish like a book. You need to go on a targeted hunt for the sections that really matter in a dispute.

Here’s where to look first:

- The Declarations Page: This is your policy’s one-page summary. It lays out the basics: your name, address, policy number, and most importantly, your coverage limits for the structure and your personal belongings, plus your deductible.

- Coverages: This section gets into the nitty-gritty of what your insurer is supposed to pay for. Pinpoint Coverage A (Dwelling) and Coverage C (Personal Property). This is also where you’ll find the terms for Additional Living Expenses (ALE) if the damage forces you out of your home.

- Exclusions: Pay close attention here—this is the insurance company’s favorite part of the contract. It's a laundry list of everything they won’t cover, and adjusters love to use vague exclusions to justify a denial.

- Conditions: Think of this as your to-do list after a disaster. It outlines your duties, like protecting your property from further damage and providing all the necessary documents. If you miss a step, they can use it as grounds to deny the whole claim.

The real fight often comes down to the definitions of specific words. Insurers are masters at twisting policy language to their advantage. For instance, they might offer a payout based on Actual Cash Value (ACV), which is the value of your damaged property after they subtract for age and wear-and-tear. It leaves you with pennies on the dollar.

But your policy might actually require them to pay Replacement Cost Value (RCV), which covers the full cost to replace what you lost with brand-new materials today.

An insurer might offer you the depreciated ACV for your 10-year-old roof, knowing full well that your policy allows for the full RCV required to install a brand-new one. This single "interpretation" can short you by tens of thousands of dollars.

This is exactly why having an expert in your corner can completely change the outcome. A seasoned public adjuster or one of the specialized homeowners insurance claim lawyers knows how to tear this language apart. They can spot hidden coverages and call out the insurer's self-serving interpretations.

They take the very document the insurance company is using against you and turn it into your most powerful tool for getting the settlement you deserve.

Key Policy Terms Your Insurer Might Use Against You

Insurance companies have a whole dictionary of terms they use to minimize payouts. They count on you not knowing the difference. Here’s a look at how they spin these terms versus what they actually mean when you have an advocate on your side.

| Insurance Term | Insurer's Typical Interpretation (To Limit Payout) | Policyholder Advocate's Interpretation (To Maximize Claim) |

|---|---|---|

| Actual Cash Value (ACV) | "The value of your 15-year-old roof, minus depreciation. Here's a check for a fraction of what a new roof costs." | "This is just the first payment. The policy also owes for the recoverable depreciation once the work is done, bringing you to full replacement cost." |

| Matching | "We only owe to replace the few shingles damaged by hail. It doesn't matter if the new ones don't match the rest of your roof." | "The policy requires restoring the property to its pre-loss condition. Mismatched materials create a visible, ongoing loss, so the entire slope (or roof) must be replaced for a uniform appearance." |

| Sudden & Accidental | "That water damage looks like it happened over time from a slow leak, so it's a maintenance issue we don't cover." | "The leak began from a specific, accidental event on a certain date. Any resulting damage is a direct loss covered by the policy, not a pre-existing maintenance problem." |

| Cosmetic Damage | "The dents in your siding from the hailstorm are just cosmetic. Since the siding still functions, we don't owe for it." | "This 'cosmetic' damage has diminished the property's value and lifespan. The policy covers direct physical loss, and these dents qualify. It must be repaired or replaced." |

Understanding these distinctions is critical. The gap between their interpretation and the correct one can mean the difference between a few thousand dollars and a settlement that truly allows you to rebuild.

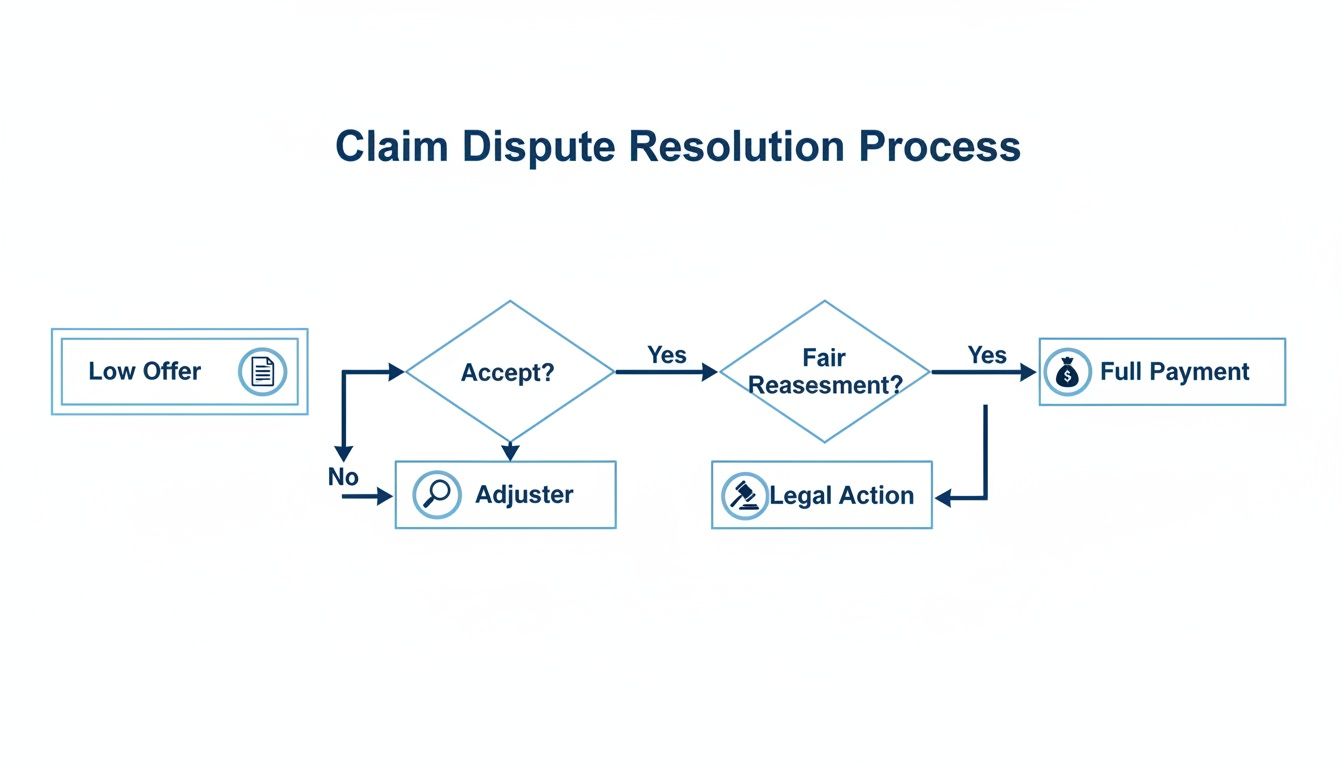

How A Public Adjuster Can Win Your Fight Without A Lawsuit

Before you jump into hiring a homeowners insurance claim lawyer—a process that can be incredibly long and stressful—there’s another powerful option. You can often resolve the dispute faster and without ever seeing a courtroom by bringing in a licensed public adjuster.

Think of a public adjuster as your frontline advocate. They're an expert in the nitty-gritty of policy language and damage assessment who works only for you, not the insurance company. Their entire job is to level a playing field that's heavily tilted in the insurer's favor, meticulously documenting every single detail of your loss to force the carrier to honor the policy you’ve been paying for.

In many cases, just getting a public adjuster involved is enough to turn a denial or a ridiculous low-ball offer into a fair settlement.

A Public Adjuster Success Story

Let’s look at a case handled for a homeowner in Raleigh. A nasty hailstorm blew through and chewed up their roof, siding, and windows. Their insurance company, one of the huge national carriers, sent out an adjuster who did a quick 20-minute walk-around.

The result? An offer for just $8,500. It was barely enough to cover a small part of the roof and completely ignored the siding damage, which the company adjuster brushed off as "cosmetic."

Feeling frustrated and completely powerless, the homeowner called us at For The Public Adjusters, Inc. We sent one of our certified adjusters to their home right away to conduct a real, comprehensive inspection from the ground up.

Here’s how we flipped the script on their claim:

- We Found What Their Adjuster 'Missed': Our team spent hours on-site, using specialized equipment to document every single dent, crack, and point of failure. We uncovered massive hail damage to the siding that the company adjuster conveniently dismissed. We even found interior water stains that were clearly linked back to the compromised roof.

- We Built an Ironclad Evidence Package: We didn't just ask for more money. We built a professional claim file that included a detailed report with hundreds of photos, an independent contractor's estimate for a full replacement, and a line-by-line breakdown of their policy. We even highlighted the "matching" clause that required the insurer to replace all the siding, not just a few random pieces.

- We Negotiated from a Position of Strength: Armed with undeniable proof, we reopened negotiations. We presented a case that proved their initial assessment wasn't just wrong—it was negligent and incomplete.

Faced with an evidence package they simply couldn't argue with, the insurer's desk adjuster reversed the initial low-ball offer.

The final settlement was over $62,000—more than seven times the original amount.

This family got their home fully restored to its proper value and safety without ever having to speak with a lawyer. That's the power of having a real expert in your corner. A public adjuster’s deep knowledge can force an insurer to pay what they actually owe, saving you the time, money, and stress of a lawsuit.

If you want to learn more about this role, check out our guide on what a public claims adjuster does and how they can help you win your fight.

Knowing When To Escalate And Hire A Lawyer

While a skilled public adjuster can win most battles, some insurance companies just dig in their heels and refuse to do the right thing. This is when the fight escalates. It’s the point where you need the legal hammer that only a homeowners insurance claim lawyer can bring to the table.

Knowing when to make that call is everything.

If your insurer has gone silent, sent you a final denial letter without a legitimate reason, or just won't negotiate in good faith—even after your public adjuster laid out an airtight case—it's time to bring in the legal firepower.

Recognizing Bad Faith

One of the loudest alarm bells telling you to hire an attorney is when you suspect bad faith. This isn't just a simple disagreement over the cost of a new roof. It’s when your insurance company deliberately misinterprets your policy, refuses to conduct a proper investigation, or uses intimidation tactics to bully you into accepting a lowball settlement.

These aren't just shady tactics; they're often illegal. An experienced lawyer knows exactly how to spot these moves and can hold your insurer accountable for breaking the law. That can lead to damages far beyond what your original claim was even worth. In a landmark case, State Farm Mut. Auto. Ins. Co. v. Campbell, the U.S. Supreme Court upheld a verdict against the insurer for bad faith, confirming that insurance companies can face substantial punitive damages for their egregious behavior.

As you can see, negotiation is always the goal. But legal escalation is the necessary final step when insurance companies won't cooperate.

We’re seeing this happen more and more. The number of homeowners insurance lawsuits is skyrocketing, signaling a deep and growing distrust in how insurers handle claims. Over 3,500 suits were filed in U.S. federal courts in a single year—the highest number we've seen since at least 2009.

A huge chunk of those lawsuits involved storms, rain, and wind, which hits close to home for property owners in North Carolina and Virginia where tornadoes and hail are a constant threat.

The Power Of A Contingency Fee

A lot of homeowners get nervous about the cost of hiring a lawyer, but here's the good news: most reputable insurance claim lawyers work on a contingency fee basis. This completely changes the game.

You pay absolutely nothing upfront. The lawyer only gets paid if they win a settlement for you, and their fee is just a percentage of the money they recover.

This setup makes legal help available to anyone, no matter their financial situation. It also means your lawyer is 100% motivated to get you the biggest settlement possible.

When your insurance company won’t listen to reason, hiring a lawyer on contingency is a risk-free way to force them to listen in a courtroom. If you're stuck with a stubborn denial, our guide explains how to appeal a denied insurance claim and lays out when it's time to call in the pros.

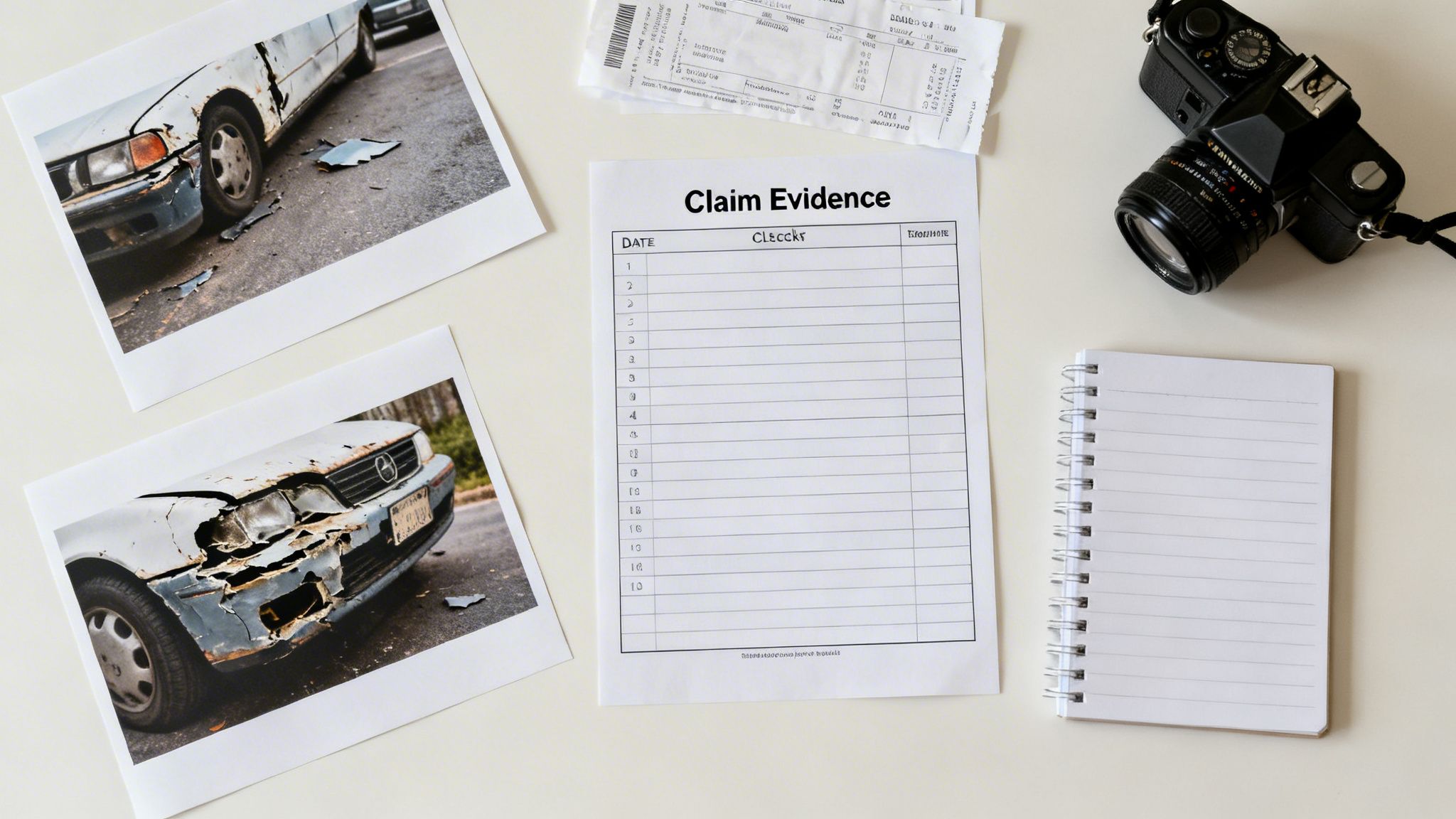

Building An Unbeatable Case Against Your Insurer

Whether you’re working with a public adjuster or bringing in a lawyer, winning a dispute boils down to one thing: irrefutable proof.

Your insurer has a whole team looking for reasons to underpay your claim. Your job is to build a case so tight and so well-documented that they have nowhere to hide. This isn't just about snapping a few photos after the damage. It's about creating an evidence locker that turns the chaos of your situation into an organized, powerful argument.

This is exactly how you turn the tables on them.

Your Essential Evidence Checklist

Every single piece of evidence you collect chips away at the insurance company’s position and strengthens yours. Get started on this immediately.

- Go Overboard with Photos and Videos: Don't just take a few pictures. Take hundreds. Record a slow video walkthrough of your entire property, talking about what you’re seeing. Get close-ups of serial numbers on appliances, zoom in on the damage, and then pull back for wide shots that show the full scope of the disaster.

- Keep a Detailed Communication Log: Grab a notebook or start a spreadsheet dedicated only to this claim. Log every single interaction—every phone call, email, and letter. Note the date, time, the name of the person you spoke with, and what was said. This log becomes gold when you need to prove delays or contradictory statements.

- Hoard Receipts for Every Related Expense: Did you have to run to the hardware store for tarps? Was your family forced into a hotel? Save every single receipt for temporary repairs and additional living expenses. This is money you’re entitled to get back.

Countering Their Skewed Numbers

The adjuster your insurance company sends out will come up with their own repair estimate, and it's almost guaranteed to be low. They use outdated pricing, "overlook" damage, and do everything they can to shrink the number.

Your most powerful weapon against this is to get your own independent estimates from at least two reputable, local contractors.

These quotes reflect the real-world cost of repairs in your area and directly challenge the insurer's low-ball offer. When a lawyer or public adjuster presents these competing bids, it forces the company to either pay up or try to justify its ridiculous numbers in writing.

Documenting your loss is non-negotiable. To really drive home the extent of your losses and build an unbreakable claim, a complete home inventory for insurance claims is essential. A detailed list of your belongings, with photos and purchase dates, can mean the difference between a fair settlement and a devastating financial blow.

This becomes even more critical in states where insurance fights are common. In Florida, for example, the property insurance market saw over 60,000 litigated claims in a single year—a shocking 8% litigation rate for homeowners. That trend is a serious warning for property owners in other storm-prone areas like North Carolina and Virginia.

The bottom line is that an organized, evidence-based approach is how you win.

Fighting Flood Claim Denials From FEMA And The NFIP

Think battling your homeowners insurance company is a tough fight? That’s nothing. When you’re dealing with flood damage, you’re stepping into a whole different ring, one run by the federal government—and believe me, the rules are designed to work against you.

Your standard homeowners policy won’t touch flood damage. This forces you into the bureaucratic maze of the National Flood Insurance Program (NFIP). It doesn’t matter if you’re dealing with FEMA directly or a "Write Your Own" (WYO) carrier like Allstate that just administers the policy; their goal is almost always the same: pay as little as possible.

The Unique Hell of NFIP Claims

NFIP claims are governed by a brutal set of federal regulations. They are completely unforgiving. Miss one deadline, make a single error on the required "Proof of Loss" form, and your entire claim can be tossed out on a technicality. It happens all the time.

The adjusters they send out are trained to follow a painfully strict interpretation of what’s covered, which means legitimate damages get denied left and right. They know this system inside and out and use that knowledge to their full advantage.

Just imagine your North Carolina home gets devastated by a storm, and you’re left with a denied or criminally low-balled offer. This nightmare is a reality for too many, especially when you consider the average home insurance claim payout is just $15,100. To get a better sense of how policyholders are forced to fight back, you can discover more insights on Insurify.com.

Make no mistake: the NFIP isn’t your neighborhood insurance agent. You are fighting a branch of the federal government, and they have a thick playbook designed specifically to limit their financial payout after a major disaster.

This is why getting specialized help isn’t just a good idea—it’s a necessity. A lawyer who understands the ins and outs of federal regulations is one route. But often, a more effective first step is bringing in a public adjuster who has deep, firsthand experience with NFIP claims. They know the unique paperwork, the rigid appeal process, and how to build an ironclad case that forces the government to pay what it actually owes.

Got Questions About Your Insurance Dispute? We've Got Answers.

When your claim gets denied or the offer is ridiculously low, a million questions start racing through your mind. It’s confusing and overwhelming. Let's cut through the noise and get you some straight answers to the questions we hear every single day.

Should I Start With a Public Adjuster or a Lawyer?

For almost every property damage dispute we see, calling a licensed public adjuster first is the smartest move you can make.

Think of it this way: public adjusters are the frontline experts in policy language and damage valuation. Their entire job is to build an iron-clad case for your claim and negotiate with the insurance company. More often than not, they can get the job done without ever stepping foot in a courtroom, which saves you a ton of time and money.

If the insurance company digs in its heels, acts in bad faith, or just flat-out refuses to be reasonable, that’s when your public adjuster will bring in the legal firepower and connect you with experienced homeowners insurance claim lawyers.

I Can't Afford a Lawyer. What Now?

You absolutely can. This is a common myth that insurance companies love.

The vast majority of reputable insurance claim lawyers work on a contingency fee basis. In plain English, that means you pay them nothing upfront. Zero. They only get paid a percentage of the money they win for you after they secure your settlement. If they don't win, you don't pay. This levels the playing field and gives every homeowner access to the legal help they need.

What Does "Bad Faith" Actually Mean?

Bad faith isn't just a mistake or a disagreement over numbers. It’s when your insurance company actively tries to dodge its legal and contractual responsibilities to you, the policyholder.

It’s a deliberate strategy to protect their profits at your expense.

Some classic examples of bad faith include:

- Twisting the words in your policy to deny a valid claim.

- Refusing to conduct a proper, thorough investigation.

- Using stall tactics and endless delays to wear you down.

- Making lowball offers and using intimidation to get you to accept.

If your gut is telling you something is off, you’re probably right. For more background on the claims process, you can find some helpful general insurance claims information here. Suspecting bad faith is a major red flag that means it's time to get a professional in your corner, immediately.

Is your insurance company giving you the runaround? The team at For The Public Adjusters, Inc. can help you fight back. Get a no-cost claim review and learn how to get the settlement you are owed. Visit us to get the help you need today: https://forthepublicadjusters.com