When your insurance company is not responding to your claim, it's almost never an accident. It's a strategy. Your first move is to build an undeniable paper trail of every single communication attempt while knowing the legal deadlines your insurer is supposed to meet. That documentation is the ammunition you need to fight back and force them to act.

The Deliberate Silence Insurers Use To Delay And Low-Ball Your Claim

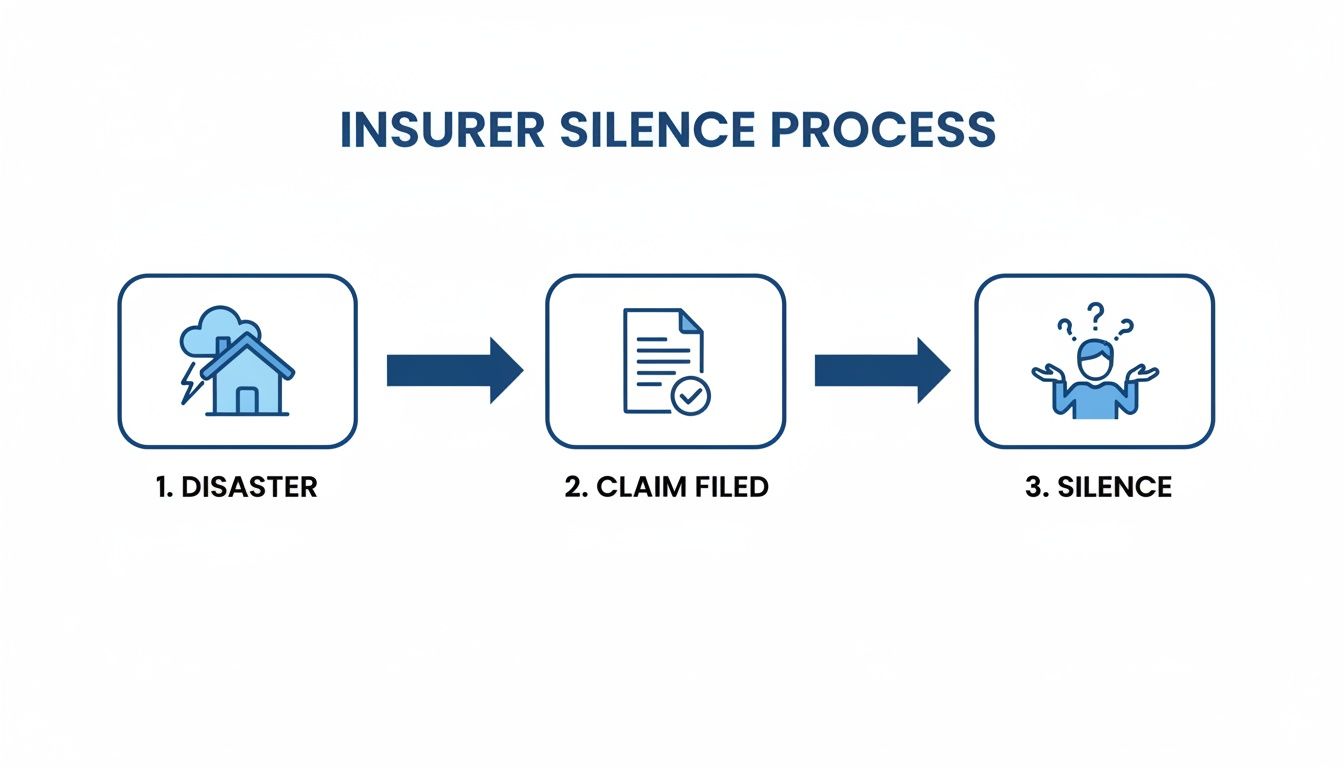

The shock of a fire, hurricane, or major water damage to your home or business is bad enough. But the deafening silence from your insurance company afterward? That can feel like a second disaster.

You’ve paid your premiums on time, year after year, expecting them to be there when you need them most. Instead, you're met with unanswered calls and emails that disappear into a void. Let’s be clear: this isn't just bad customer service. For major carriers like State Farm and Allstate, it’s often a calculated strategy designed to wear you down and protect their profits.

They’ll blame overwhelming caseloads after a storm, but more often than not, these delays are intentional. The longer they hold onto your money, the more interest they earn. The more frustrated and exhausted you get, the more likely you are to accept a low-ball settlement just to make it all stop. This silence is a battle tactic.

Why Your Insurer Hopes You'll Give Up

Imagine a hurricane tears through your North Carolina home, and for weeks—even months—you hear nothing but crickets from your insurance company. This isn't some rare nightmare scenario; it's a harsh reality for countless homeowners and business owners.

For property owners in storm-prone states like NC and VA, where wind, hail, and water damage claims spike after every major weather event, these delays are devastating. Mold starts to spread, damaged roofs begin to cave in, and families are left in limbo.

This non-responsiveness often comes from the top down. The company's own adjusters are trained to protect the bottom line, which creates a massive conflict of interest. While claim denials are a known issue across the board, the impact on property owners is immediate and severe. You can see for yourself how common this tactic is and get more insights on claim denial rates.

Your insurance company's silence is not a sign of them being busy. It is a calculated delay tactic. They are betting on your frustration, hoping you will abandon your claim or accept a fraction of what you are owed.

This passive-aggressive approach puts the entire burden on you. Every day they ignore you is another day your property deteriorates and your stress level skyrockets. Understanding how long an insurance claim should rightfully take is the first step in knowing when you're being taken for a ride.

They are banking on you not knowing your rights. They're counting on you not knowing the steps to hold them accountable. But you don't have to play their game. The key is to shift the power back to your side by proving their negligence and demanding the attention your homeowner or business claim deserves.

Build An Undeniable Paper Trail To Force A Response

When your insurance company goes radio silent, sitting by the phone is the worst thing you can do. It's exactly what they're banking on. Instead, it’s time to pivot from passively waiting to actively building a rock-solid case that documents their negligence.

Every unanswered call, every ignored email, becomes a brick in the wall of evidence you’re constructing.

This isn’t about being confrontational. It’s about being professional, persistent, and methodical. The goal is to create a paper trail so airtight that ignoring you becomes a bigger headache for the insurer than just handling your claim properly. This record is your leverage. It proves you’ve done everything right while they’ve dropped the ball.

Start Logging Every Single Interaction

Your memory isn’t a legal document. From this point forward, every single time you try to communicate with your insurer, you need to log it. Whether you leave a voicemail for the adjuster or fire off a quick email, write it down immediately.

This simple act of tracking your attempts paints a clear, undeniable picture of their silence.

This kind of communication log is your first and best tool for holding them accountable. We’ve even created a simple template to get you started.

| Date | Time | Contact Method (Call/Email/Letter) | Insurer Representative | Summary of Conversation | Follow-Up Action Needed |

|---|---|---|---|---|---|

Start filling this out today. Every blank row that should contain their response is another piece of proof that they’re not meeting their obligations.

On top of this, you absolutely must document every penny you spend related to the damage. This means costs for temporary repairs, extra living expenses if you’re displaced from your home, or business interruption costs. It’s a good idea to organize your receipts with a modern digital system to make sure nothing gets lost.

Escalate and Formalize Your Communication

Once your log shows a clear pattern of being ignored, it’s time to change tactics. Stop leaving the tenth voicemail for an adjuster who clearly has no intention of calling you back.

Instead, take these deliberate, more forceful steps:

- Go Up the Ladder. It’s time to find the adjuster’s boss. A quick search online or a call to the company's main number can usually get you the name and contact info for a claims supervisor or manager. A polite but firm email to that supervisor, with your original adjuster CC’d, signals that you’re not going to be brushed aside.

- Send a Certified Letter. This is a critical step. Move your communication from digital to physical by sending a formal "Letter of Inquiry" via certified mail with a return receipt. This creates a legal record proving they received your message. Keep it professional. State the facts: your policy number, claim number, date of loss, and a timeline of your unanswered attempts to get an update.

A well-crafted letter can work wonders. In fact, if the situation requires you to submit an official Proof of Loss form, your meticulous records will be the foundation of that document. The paper trail you’ve built will be invaluable. You can learn more about the critical importance of a Proof of Loss here, but just know it’s a powerful tool that can turn the tide in a stalled claim.

Your methodical paper trail forces the insurance company into a corner: either respond or risk creating a clear record of bad faith conduct.

Know Your Rights And The Insurer's Legal Obligations

When your insurance company goes silent on your property claim, they aren't just giving you the runaround—they may actually be breaking the law. That policy you have isn't just a suggestion; it's a legally binding contract. Your insurer has a list of duties they have to fulfill, and understanding them is the first step to getting the upper hand.

Their silence isn't just bad customer service; it can be a direct violation of their contractual duties and state law. Here in North Carolina and Virginia, there are specific regulations designed to protect homeowners and business owners from these exact delay tactics.

Insurers don't get to take forever. They are legally required to act in good faith, which means they have to investigate and process your claim fairly and with reasonable speed.

The Power Of The Unfair Claim Settlement Practices Act

Most states, including North Carolina and Virginia, have adopted some form of the Unfair Claim Settlement Practices Act. This is the rulebook that spells out exactly what insurance companies can't do, and it's a powerful piece of legislation for policyholders.

This act makes it illegal for an insurer to do things like:

- Fail to acknowledge and act reasonably promptly on your calls, emails, and letters about a claim.

- Refuse to try, in good faith, to settle claims quickly and fairly once it's clear they owe you.

- Force you to file a lawsuit just to get what you're owed by offering a ridiculously low-ball settlement.

So when a big carrier like Allstate or State Farm ignores your calls for weeks on end, they are very likely violating these statutes. Their non-responsiveness isn't just frustrating; it can be legally classified as acting in bad faith.

Bad faith is more than just a buzzword. It's the legal term for when an insurer tries to dodge their obligations to you. Deliberate delays and ignoring your attempts to communicate are classic examples, and they can give you a solid legal foundation to fight back.

Legal Timelines And Precedent Are On Your Side

State laws put insurers on a clock. For example, many states require an insurance company to acknowledge they’ve received your claim within 10-15 business days. After that, another countdown starts for them to investigate the damage and tell you if your claim is accepted or denied.

When they blow past these deadlines without giving you a legitimate reason in writing, they are in breach of their legal duties. This is exactly why that paper trail you're keeping is so crucial—it becomes your weapon.

Courts have sided with policyholders against insurance giants for these very tactics time and time again. In the notable case Vaughan v. Nationwide Mut. Ins. Co., a jury found Nationwide acted in bad faith for delaying and denying a homeowner's claim. The court's decision sent a clear message: insurance companies can be held financially accountable for intentionally dragging their feet and failing their policyholders.

Knowing your rights changes the entire game. You’re no longer just a frustrated customer hoping for a call back. You are a policyholder whose contractual and legal rights are being violated, and you have the power to do something about it.

When It’s Time to Stop Asking and Start Demanding: Hire a Public Adjuster

If your documented calls and emails have been met with a wall of silence, it’s time to stop pleading for a response. You've done your part. Now, it's time to bring in a professional who not only speaks the insurance company's language but is someone they absolutely cannot ignore.

This is the exact moment a public adjuster becomes your most powerful asset.

Let's get one thing straight: the adjuster your insurance company sends to your property works for them. Their loyalty is to their employer’s bottom line, which often means minimizing what they pay you.

A public adjuster, on the other hand, is licensed by the state and works exclusively for you, the policyholder. Their only objective is to fight for the maximum, fair settlement you're entitled to under your policy.

An Advocate Who Forces the Insurer to the Table

Imagine this real-world scenario: your North Carolina business is devastated by a fire. You file the claim, expecting the support you’ve paid for, but weeks bleed into months with no word. The company adjuster won’t return your calls, your business is shut down, and the financial pressure is becoming unbearable.

This isn’t just a hypothetical; it’s a situation we see business owners get forced into all the time.

Bringing in a public adjuster changes the entire dynamic. Instead of you chasing the insurer, a seasoned expert takes command. They perform their own independent, detailed investigation, documenting every bit of structural damage, smoke contamination, and business interruption loss—often uncovering things the company adjuster conveniently “missed.”

They then package this mountain of evidence into a rock-solid claim and force the insurer to the negotiating table. The silent treatment stops cold. Suddenly, the insurance company is on the defensive, dealing with a professional who knows the policy backward and forward and won't fall for their usual delay tactics.

When you hire a public adjuster, you’re no longer a frustrated policyholder begging for a phone call. You are a client with professional representation, and the insurance company is legally required to respond.

Success Story: Turning Radio Silence into a Real Settlement

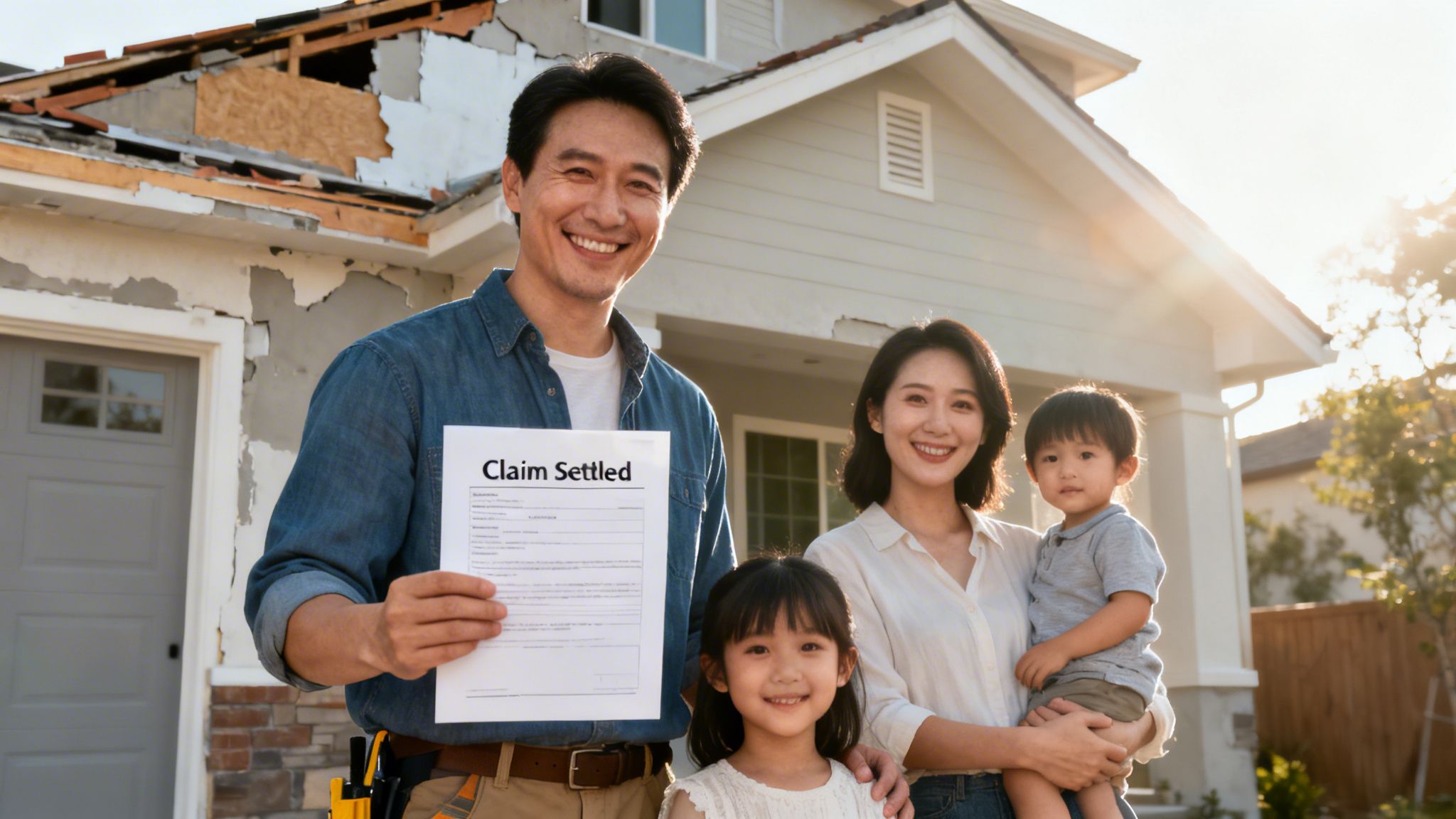

A homeowner in North Carolina suffered significant water damage from a failed plumbing line. Their insurance company, a major national brand, sent out an adjuster who offered a shockingly low settlement of just $15,000, nowhere near enough to cover the extensive repairs. When the homeowner tried to dispute it, they were met with silence. Calls and emails went unanswered for weeks.

Frustrated and on the verge of giving up, they hired a public adjuster. Our team immediately conducted a thorough inspection, identifying widespread damage the company adjuster had ignored. We documented everything and presented a new, comprehensive claim package. The insurer's delay tactics stopped. Faced with undeniable evidence, they came to the table and settled the claim for over $95,000—more than six times their original offer. This is the power of expert advocacy.

Across North Carolina and Virginia, this work has turned outright denials and low-ball offers into fair, paid claims. With claim denial rates on the rise, homeowners and businesses can't afford to just accept silence as an answer. You have to demand a response, and the single most effective way to do that is with a pro in your corner.

Having an expert on your side completely levels the playing field. To see exactly how they take the fight to your unresponsive insurer, check out our guide on what a public claims adjuster does.

From Frustration To Full Recovery: A Real Client Story

Sometimes, the best way to see the light at the end of the tunnel is to hear from someone who has already made it through. When your insurance company is not responding to your claim, that feeling of being completely ignored and powerless can be crushing. But it's a battle that can absolutely be won.

The endless waiting, the mounting stress, the financial pressure—this isn't an accident. It's often a deliberate strategy. Some insurance carriers count on you getting exhausted and just giving up.

Bringing in a professional advocate flips the script entirely. It transforms what feels like a hopeless situation into a story of successful recovery.

From Radio Silence To A Check In Hand

Don't just take our word for it. Hearing from a homeowner who was in your exact shoes—stuck, frustrated, and getting nowhere—is the best proof there is. Their experience is a powerful reminder that you don't have to put up with the silent treatment from your insurer.

Here’s a real review from a client who was at their breaking point before they got the right help on their side.

"My insurance company was giving me the run around when I tried to file a water damage claim. For months I argued with them and got no where. I finally decided to seek professional assistance and came across FOR THE PUBLIC ADJUSTERS. A representative was out to my home within a few days. They handled my claim from start to finish. All I had to do was show them the damage, provide them with my insurance documentation and they took it from there. I was awarded a lot more than I anticipated. I would have still been fighting with my insurance company had it not been for the help of FOR THE PUBLIC ADJUSTERS. They are a professional and honest company that I would not hesitate to do business with again." – Crystal H., Client Review

This client's story is a perfect, real-world example of what happens when you bring in a public adjuster. The insurance company's stonewalling tactics were immediately met with professional persistence and deep industry knowledge. It forced them to stop playing games, engage with the claim, and ultimately pay what was fair.

This isn't just about getting a check. It’s about the incredible relief that comes from handing that fight over to an expert who knows the playbook. It's about taking back control from an insurance company that is banking on you walking away.

Your Questions Answered: Dealing with a Silent Insurance Company

When your insurance company goes dark, it's easy to feel powerless and confused. You're not alone in this, and you definitely have questions. Let's tackle some of the most common ones we hear from homeowners and business owners who are getting the silent treatment.

How Long Is Too Long to Wait For a Response?

This is the big one. While there can be some slight variations, states like North Carolina and Virginia have laws on the books to stop insurers from dragging their feet indefinitely. As a general rule, an insurance company should acknowledge your claim within 10-15 business days.

If it's been weeks and all you've got to show for it is an automated email receipt, that's a massive red flag. This isn't just bad customer service. Deliberate, prolonged silence can be a direct violation of the Unfair Claim Settlement Practices Act. When this happens, the time for waiting is over. It’s time to escalate, with all your documented communications in hand.

Will Hiring a Public Adjuster Get My Policy Canceled?

Let me be crystal clear: absolutely not. It is illegal for your insurance company to cancel your policy, raise your rates, or retaliate against you in any way for hiring professional help. Your right to hire a licensed public adjuster to represent your interests is protected.

Frankly, hiring a public adjuster does the opposite of what you might fear. It sends a powerful signal to the carrier that you know your rights and you won't be pushed around, ignored, or low-balled. It forces them to stop the delay games and deal with your claim by the book—your policy's book.

Hiring a public adjuster doesn’t create a problem; it solves the one the insurance company created with their silence. It levels the playing field and puts an expert in your corner who works only for you.

Can I File a Complaint with the State?

Yes, and you absolutely should think of this as a key tool in your arsenal. Every state has a Department of Insurance (DOI) that’s supposed to police the industry and look into consumer complaints.

Filing a formal complaint about a non-responsive insurer can light a fire under them. It often triggers an official inquiry that pressures the company to finally respond and justify their actions (or lack thereof). Just know the DOI's limits. Their job is regulatory—making sure the insurance company isn't breaking the law. They typically won't step in to argue the value of your damaged roof or fight for a fair settlement. For that, a public adjuster is still your strongest advocate.

What's the Difference Between a Public Adjuster and an Attorney?

This is a critical distinction, and getting it right can save you a lot of time and money.

A public adjuster is a licensed specialist in property loss and insurance policy. Our job is to get in the trenches—assessing the full scope of your damage, documenting every last detail, and negotiating directly with the insurance company to get you a fair and just settlement based on your policy.

An attorney is your go-to for legal action, like suing an insurer for acting in "bad faith." While a lawsuit is sometimes the only option left, bringing in a public adjuster is almost always the best first move. We can often break the logjam, build an ironclad claim file, and get you paid properly without ever seeing the inside of a courtroom. And if the insurer still won't budge? The incredibly detailed claim file we've built becomes the perfect foundation for an attorney to launch a powerful bad faith case.

When your insurance company ignores you, it's a clear sign you need an expert to take over the fight. The team at For The Public Adjusters, Inc. specializes in forcing unresponsive insurers to the table and securing the maximum settlement you are owed. Don't let their silence cost you another dollar—contact us for a free, no-obligation claim review today.

This is an important reminder of how critical documentation and financial organization become during stressful claim situations. Many people don’t realize that keeping a clear record of communications, expenses, and timelines can significantly strengthen their position when dealing with delayed responses.

From a digital services perspective, we often see families — especially those managing finances remotely for loved ones — struggle during emergencies because payments, records, and essential documents are scattered across different platforms. Having secure digital access to financial transactions, bills, and communication history can make situations like insurance claims far more manageable and transparent.

Awareness around policyholder rights and proactive record-keeping is key. Content like this helps individuals stay informed and better prepared when unexpected challenges arise.

Well said!