You opened a home insurance claim because your house was damaged and you expected help. Instead, you got a thin estimate, a vague denial, or a string of calls and emails that go nowhere. The contractor says the insurer's number won't even start the job. The adjuster acts friendly, then sends language that reads like it was designed to confuse you.

That's the moment many homeowners realize they're not in a customer service process anymore. They're in a dispute. And if you treat it like routine paperwork, the insurance company usually keeps control.

Table of Contents

- When Your Home Insurance Claim Becomes a Fight

- Decoding Insurer Tactics That Deny and Low-Ball Claims

- Building Your Counter-Offensive Documentation Is Ammunition

- The NFIP Flood Claim A Different Kind of Fight

- Calling for Backup How a Public Adjuster Wins Your Fight

- Take Back Control and Get the Payout You Deserve

When Your Home Insurance Claim Becomes a Fight

You paid premiums for years. Then the storm hits, the pipe bursts, the fire tears through part of the house, and you do what any reasonable homeowner would do. You report the loss and expect the carrier to step in. Then the letter arrives. It says the damage is partially excluded, not sudden enough, not caused the way you described, or somehow worth far less than the contractors say.

That shock is real. It's also common.

In 2024, the five largest U.S. home insurance groups did not pay out on more than 44% of resolved homeowner claims, with some states seeing nonpayment rates over 40% due to claim complexities and exclusions, according to U.S. News reporting on unpaid homeowner claims. If you feel blindsided, you're not being dramatic. You're running into a system that often protects the carrier's balance sheet first.

The adjuster isn't your advocate

This is the part homeowners need to accept quickly. The insurance company's adjuster works for the insurance company. That doesn't make every adjuster dishonest. It does mean their job is tied to the carrier's process, the carrier's estimate, the carrier's interpretation of the policy, and the carrier's claim file.

That changes how you should respond.

Practical rule: The first low offer or denial isn't the end of the claim. It's the start of the real negotiation.

A lot of people freeze after the first denial letter because it looks official. Others accept a low settlement because they need cash fast and assume the insurer must know better. Both reactions are understandable. Both can cost you.

Stop acting like a claimant and start acting like opposition

Once the insurer disputes scope, price, cause, or coverage, you need a new posture. You need written explanations. You need your own numbers. You need your own experts if the facts require them. And you need a record that shows exactly where the carrier's position falls apart.

If you're already stuck in that cycle, this guide on how to dispute an insurance claim is a useful next read. The key point is simple. Polite cooperation matters, but passive trust won't win a disputed home insurance claim.

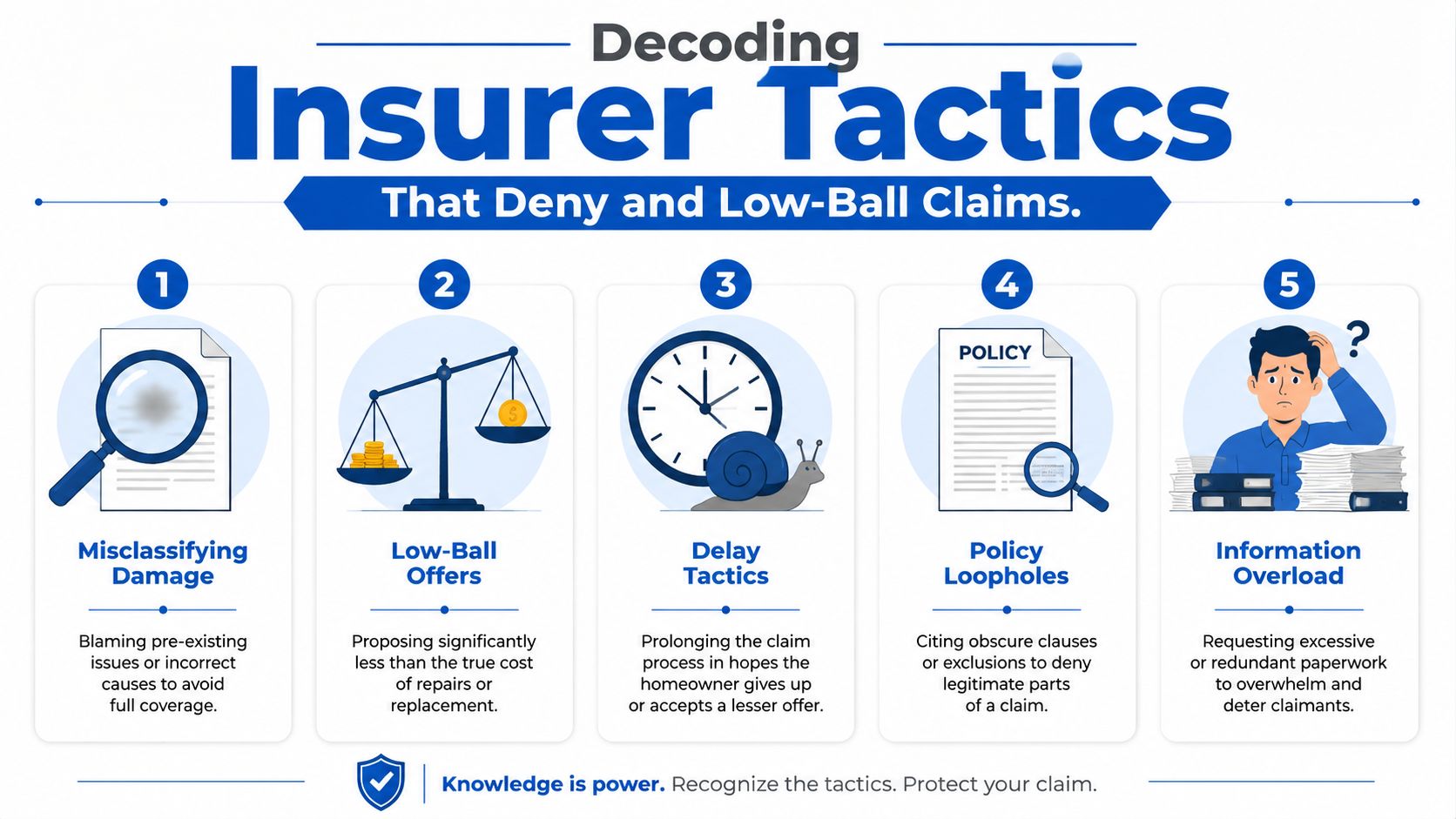

Decoding Insurer Tactics That Deny and Low-Ball Claims

Most bad claim outcomes don't start with a dramatic accusation. They start with small framing moves. The carrier narrows the scope. Labels damage the wrong way. Breaks one loss into covered and uncovered pieces. Requests more paperwork than the file needs. Then it presents the result as objective.

That's the playbook.

Misclassification is one of the oldest tricks in the book

A common tactic is to re-label the cause of damage so the policy pays less or not at all. As explained in this discussion of homeowners claim denial tactics, insurers may blame recent wind damage on pre-existing wear to deny coverage. That matters because cause drives coverage. If they win the cause argument, they often win the money argument too.

A roof opening after a storm becomes “long-term deterioration.” Water intrusion after a sudden event becomes “repeated seepage.” Interior damage caused by a covered event gets pushed into maintenance language. Homeowners hear those labels and assume the carrier has already settled the issue. It hasn't. It has stated a position.

If the insurer controls the story of causation, it controls the payout.

Low-ball estimates look technical on purpose

Homeowners get intimidated by line-item estimates because they appear precise. But precision isn't the same as accuracy. A low estimate can come from omitted rooms, missing trades, unrealistic labor assumptions, ignored code items, or pricing that doesn't reflect what qualified contractors will charge.

One place homeowners get tripped up is valuation itself. If your settlement is being reduced under depreciation or limited valuation language, read up on actual cash value in insurance before you agree to anything. Many disputes that feel like “bad math” are in fact valuation disputes buried inside policy language.

Delay wears people down

Some carriers don't need to deny right away. They can slow the file until the homeowner is exhausted. More documents. Another inspection. A different desk adjuster. A request you already answered. A promise to call back next week.

That strategy works because damage doesn't wait. Roof leaks spread. Cabinets swell. Temporary repairs become permanent stress. Families need to move forward, and insurers know that pressure changes behavior.

Here are common red flags:

- Repeated requests for the same records: The file may already contain what they're asking for.

- Shifting explanations: One week it's coverage, the next week it's pricing, then causation.

- Oral statements without follow-through: If it isn't in writing, treat it as unfinished.

- Preferred vendor pressure: The carrier's preferred contractor isn't your boss and shouldn't define your loss.

Policy language gets used as a weapon

Policies are contracts, but carriers often present them like puzzles only they can solve. They quote exclusions broadly and ignore endorsements, exceptions, or factual details that cut the other way. Homeowners then argue emotion while the insurer argues text.

That's a losing setup. Fight them with documents, not frustration.

Building Your Counter-Offensive Documentation Is Ammunition

If the insurer has built a weak version of your claim, your job is to build a stronger one. Not a louder one. Not a more emotional one. A stronger one. Every disputed home insurance claim turns on proof.

Get independent proof before the file hardens against you

If the insurer says damage is old, minor, excluded, or cheaper than your contractor says, don't argue in circles. Build evidence that answers the exact point in dispute. As noted by Keating Wagner on fighting back against denied home insurance claims, policyholders should obtain expert opinions from licensed contractors or engineers to document the true cause of damage and demand a written explanation citing the exact policy language used for the denial.

That's not optional in a serious dispute. It's the backbone of your response.

What to collect right now

Use this checklist like you're preparing for a contested hearing.

- A complete policy set: Get the declarations page, endorsements, exclusions, and any renewals. Don't rely on a summary.

- A written denial or written explanation of underpayment: Force the carrier to commit to a reason and policy wording.

- Detailed contractor estimates: Not a one-page number. You want line items, scope, materials, labor, and code-related work where applicable.

- Expert reports when causation is disputed: Engineers, roof consultants, moisture specialists, or fire investigators can separate sudden damage from old conditions.

- A communication log: Dates, names, titles, what was said, and what was promised.

- Photos and videos: Wide shots, close-ups, and progression over time.

Field advice: If an insurer keeps talking in generalities, pin them down in writing. Ask what exact policy language applies and what exact facts they rely on.

Separate maintenance from sudden damage

Homeowners often lose ground at this stage. The insurance company may lump everything together so it can call the whole loss wear and tear. Your evidence has to do the opposite. It must isolate the covered event and show what changed because of it.

A licensed contractor or engineer can be especially useful here. They can distinguish old staining from fresh water pathways, storm-created openings from ordinary aging, or structural movement from cosmetic cracking. That technical separation matters.

A practical complement to claim documentation is prevention records. If you've kept service invoices, roof inspections, or seasonal maintenance notes, they can help rebut lazy “poor maintenance” arguments. A solid resource for staying organized going forward is this 2025 home maintenance guide from Bulls Eye Repair.

Don't send a pile of papers. Send a theory of the claim

This is the difference between documentation and persuasion. Your package should tell a clean story:

| Issue | Insurer says | Your response |

|---|---|---|

| Cause of loss | Wear and tear | Independent expert ties damage to covered event |

| Scope | Limited repairs | Contractor estimate shows full affected areas and needed trades |

| Price | Carrier estimate is enough | Market-based estimate reflects actual repair requirements |

| Coverage | Exclusion applies | Policy wording and facts support coverage |

The stronger your file, the harder it is for the carrier to hide behind vague conclusions.

The NFIP Flood Claim A Different Kind of Fight

Flood changes the entire dispute. If the damage came from floodwater, you're usually not dealing with a standard homeowners policy problem. You're dealing with FEMA and NFIP flood coverage, often administered through the National Flood Insurance Program or through a Write Your Own company handling an NFIP claim under federal rules.

That distinction matters because the tactics, deadlines, paperwork, and decision-makers are different.

NFIP claims don't behave like normal homeowners claims

Homeowners often make a costly assumption after a hurricane or major storm. They think one claim process covers all water damage. It doesn't. Wind, rain entering through storm-created openings, and flood can trigger different paths. If rising water caused the loss, the NFIP framework may control, not your regular homeowners carrier.

That creates a different fight. NFIP adjusters and WYO carriers work inside a rigid federal system. Proof requirements are stricter. Policy wording is specialized. Small mistakes can turn into underpayment or denial arguments fast.

Why flood disputes are so difficult

A standard home insurance claim dispute often leaves room for negotiation about scope, causation, and pricing. NFIP disputes are tighter and more technical. The file usually rises or falls on whether the insured can document the covered flood damage in the required form and within the required claim process.

Common trouble spots include:

- Proof of loss issues: Missing support, incomplete descriptions, or weak documentation can wreck the file.

- Damage allocation fights: The insurer may separate building damage, contents damage, and excluded items in ways that shrink payment.

- Causation confusion after storms: Wind and flood may hit the same property, but they are not handled the same way.

- WYO administration: Even when a private company name is on the paperwork, the claim may still be governed by NFIP rules.

Flood claims punish assumptions. If you treat an NFIP dispute like a regular homeowners dispute, you can lose rights before you realize it.

Get specialized help early

This is one area where homeowners should stop improvising. NFIP flood coverage disputes require someone who understands how federal flood claims are documented, how WYO carriers process them, and how to separate flood damage from other concurrent losses.

In coastal North Carolina and Virginia, that issue comes up constantly after hurricanes and tropical systems. If your insurer is using flood rules against you, or if the adjuster keeps narrowing what counts as covered flood damage, bring in a public adjuster with flood claim experience before the record hardens.

Calling for Backup How a Public Adjuster Wins Your Fight

Most homeowners don't call a public adjuster at the beginning. They call after the insurer has stalled, underpaid, or denied the claim. That's usually the right moment. Once the dispute turns technical, you need someone who knows how to read the policy, inspect the damage, build the estimate, challenge causation, and negotiate from evidence instead of frustration.

The money at stake is often larger than homeowners think. The average homeowners insurance settlement for property damage is around $13,804, while fire claims can average over $77,340, as discussed in Storm Law Partners' review of home insurance adjuster tactics. When an insurer low-balls a serious loss, the gap can be life-changing.

What a public adjuster actually does

A public adjuster is licensed to represent the policyholder, not the insurance company. That matters because every major claim dispute has two fights inside it. One is factual. What was damaged, what caused it, what does it cost to fix. The other is contractual. What does the policy cover and how should the carrier apply it.

A qualified public adjuster works both sides of that problem.

If you want a plain-English breakdown of the role, read what a public adjuster does. The short version is this: they document the loss, challenge weak carrier assumptions, prepare or review estimates, organize evidence, and negotiate directly with the insurer.

When calling for backup makes sense

Not every claim needs outside help. These usually do:

- Denied claims: Especially when the denial leans on causation, exclusions, or alleged pre-existing damage.

- Low offers: If the number won't perform the repairs, something in the scope, pricing, or valuation is wrong.

- Complex losses: Fire, storm, large water, business owner claims, and mixed-cause losses get messy fast.

- Communication breakdowns: If the carrier keeps changing adjusters or won't commit in writing, the file needs pressure.

Here's a closer look at how the process works in practice.

A realistic success story, minus the fairy tale

I'm not going to invent a dramatic case study just to sell you hope. What I will tell you is what experienced public adjusters do in real disputed claims. They re-inspect the property. They compare contractor scopes to the carrier estimate. They identify omitted line items, misclassified damage, and valuation errors. They demand clarity on policy application. Then they negotiate with a complete file.

That's the work.

For homeowners and business owners in North Carolina dealing with fire, smoke, water, wind, hail, hurricane, tornado, theft, or vandalism losses, For The Public Adjusters, Inc. is one option for that type of representation. The firm handles inspection, documentation, estimate preparation, coverage-related claim support, and direct carrier communication for disputed property claims.

The right help doesn't just “assist” your claim. It changes who controls the facts in the file.

As for reviews, the pattern that matters most is simple. Clients value clear communication, documentation that matches the damage, and someone who pushes back when the insurer's story doesn't fit the property. That's what homeowners remember when the carrier has spent weeks doing the opposite.

Take Back Control and Get the Payout You Deserve

You do not have to accept a bad claim decision just because it arrived on company letterhead. A denial is not the final word. A low offer is not a fair offer just because it came from an adjuster. In a disputed home insurance claim, the carrier's first position is often just that. A position.

Your response should be disciplined.

Appeal with evidence, not outrage

If your claim is denied, you must file a formal written appeal within the timeframe specified in the denial letter, typically 30 to 90 days, and include all relevant evidence like photos, expert reports, and contractor estimates, as outlined by CMS Law Group's guidance on disputing a homeowners insurance claim. Miss that window and you can lose a crucial advantage you may never get back.

Keep the appeal focused. State what decision you are disputing. Identify the damage and cause. Attach the records that support your position. Demand a written reconsideration based on the full file.

Use a simple escalation framework

When a claim goes sideways, move in this order:

- Lock down the insurer's position in writing. Verbal explanations are weak and easy to shift.

- Answer the dispute with independent evidence. Contractor estimates and expert reports matter more than angry phone calls.

- Organize the record. Send a clean, indexed package, not scattered attachments.

- Escalate when needed. If the claim remains delayed, denied, or underpaid, bring in a public adjuster or coverage counsel appropriate to the dispute.

Your policy is a contract. The carrier doesn't get to rewrite it after the loss.

Don't let exhaustion decide the claim

Insurance companies know that claimants are dealing with damaged property, family disruption, missed work, and financial strain at the same time. Delay is powerful because life gets in the way. That's why structure matters. Keep the file moving. Keep your documentation tight. Keep forcing the dispute back to facts, scope, price, and policy wording.

You don't need to become an insurance expert overnight. You do need to stop assuming the insurer will correct itself if you just wait long enough. Fight smart, document hard, and get help when the claim turns into a contest.

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your homeowners, dwelling, or business owner property claim has been delayed, denied, or underpaid, For The Public Adjusters, Inc. can review the damage, organize the documentation, and help you challenge the insurance company's position. They represent policyholders in North Carolina, not insurers, and assist with fire, smoke, water, wind, hail, hurricane, tornado, theft, and vandalism claims.