After a fire rips through your home or business, that insurance policy you’ve been paying for is supposed to be your lifeline. But let’s be blunt: fighting for a fair fire damage claim settlement often turns into a bare-knuckle brawl against the very company you paid to protect you.

That first settlement offer they slide across the table? It’s not a helping hand. It’s the opening shot in a negotiation designed to protect their profits, not rebuild your life.

Your Fire Damage Claim Is A Battleground

When you’re reeling from the shock of a fire, dealing with smoke and water damage, you are at your most vulnerable. Insurance giants like State Farm and Allstate know this. They bank on it.

They use this chaos to their advantage, deploying tactics designed to make you fold and accept a fraction of what you’re actually owed. This isn’t just one bad adjuster—it’s a business model. Delaying, denying, and underpaying claims is baked into their system to boost their bottom line.

Expect an Uphill Fight

The insurance adjuster your provider sends out works for one person: their boss. Their loyalty is to the insurance company’s shareholders, not to you.

They are trained to find loopholes in your policy and twist the language to limit the payout. They might call catastrophic damage a “partial loss,” arguing that your smoke-saturated furniture and electronics just need a good “cleaning” instead of a full replacement. This tactic alone can save their company tens of thousands of dollars at your expense.

The first offer is never the best offer. It’s a test to see if you’ll just take the money and go away. Without an expert on your side, you’re walking into an ambush.

This is where the fight really begins. Your insurer is betting on your exhaustion, your grief, and your lack of deep policy knowledge to get you to sign off on a lowball offer. They have zero obligation to hunt for hidden damages or point out every bit of coverage you’re entitled to. That job falls on you.

Leveling the Playing Field

To get the money you are contractually owed, you have to stop thinking of your claim as a request for help and start treating it as a demand for payment. This means shifting your mindset from victim to fighter. You have to document everything, challenge every undervalued item, and refuse to be bullied by jargon and delays.

But you don’t have to do it alone. A public adjuster is a state-licensed claims expert who works only for you, the policyholder. They are your hired gun in this fight.

Here’s what they do:

- Investigate and document every last bit of damage, both seen and unseen.

- Dissect your policy to uncover every dime of coverage you are entitled to claim.

- Build an independent, detailed estimate of what it will actually cost to rebuild and replace everything.

- Go to war with the insurance company on your behalf, negotiating directly to force a maximum settlement.

Hiring a public adjuster from the start sends a powerful message to your insurer: you will not be a pushover. It completely changes the power dynamic, putting a seasoned professional between you and the company trying to underpay you.

Recognizing Bad Faith Insurance Tactics

After a fire guts your home, you call your insurance company expecting a lifeline. Instead, you get a fight. It can feel like they’re actively working against you, and let’s be clear: you’re not imagining things. This is a cold, calculated business strategy designed to minimize what they pay out on your fire damage claim.

To defend yourself, you have to understand their playbook. Corporate giants like State Farm and Allstate don’t make billions in profit by generously paying claims. They profit by using tactics designed to wear you down, confuse you, and ultimately force you to accept a lowball offer.

The Delay Game

One of the oldest tricks in the book is the strategic delay. They know you’re not in your own bed. They know you’re stressed, desperate, and just want to start rebuilding your life. They use that desperation as a weapon.

Those unreturned calls, “lost” documents, and endless requests for the same paperwork aren’t just administrative errors. They are deliberate moves meant to bleed you dry emotionally and financially. The goal is simple: make you so tired of fighting that you’ll take any offer they throw at you just to make it stop.

“Bad faith” isn’t just a fancy term for bad service. It’s when an insurer breaks its legal duty to treat you fairly and honestly. Unreasonable delays in investigating or paying a valid claim are a classic sign of this.

This isn’t a process; it’s a war of attrition. The longer they can drag it out, the more pressure builds on you to settle for pennies on the dollar.

Under-Scoping and Lowball Offers

When the insurance company finally sends their adjuster, that person’s job isn’t to find everything wrong with your property. Their job is to find the least amount of damage they can get away with paying for. It’s common for them to send a junior-level adjuster who completely misses things like hidden smoke damage inside your walls or the compromised structural integrity of your home.

This “inspection” leads directly to a ridiculously low settlement offer. They’ll re-categorize major problems as minor cleanup jobs. You’ll see things like:

- Soot-covered walls: They’ll offer a budget for cleaning and a coat of paint. They deliberately ignore that toxic soot and stubborn odors have soaked into the drywall, meaning it all needs to be torn out and replaced.

- Smoke-damaged electronics: They’ll suggest a “specialized cleaning,” knowing full well that corrosive soot gets into the circuitry and will cause your TV or computer to fail a few months from now.

- Water-damaged kitchen cabinets: They’ll offer to dry and repaint them, even when the underlying particle board has swelled up and warped, destroying their structural integrity for good.

Their first offer isn’t a fair assessment. It’s an opening bid in a negotiation they hope you’re too exhausted to even start.

Using Policy Language Against You

Your insurance policy is a dense, legal document designed to be confusing. Insurers use this complexity to their advantage, twisting definitions and citing obscure clauses to deny or underpay your claim. They’ll lean on vague terms like “like kind and quality” to justify replacing your solid wood cabinets with cheap pressboard junk from a big-box store.

They might even deny a huge part of your smoke damage claim by arguing it wasn’t caused by “direct flame”—a deceptive reading of your policy. Getting a better understanding why an insurance company might refuse to pay a claim is critical to anticipating and fighting back against these dirty tricks.

You have to see these strategies for what they are: a corporate game plan to protect their profits at your expense. The company adjuster isn’t on your team. In fact, they’re the other team’s star player. To get a fair settlement for your fire damage claim, you have to be ready to counter every single one of their moves.

How to Build an Unshakeable Fire Damage Claim

Let’s be blunt: to win the fight against your insurance company, you can’t just trust their adjuster’s assessment. You have to build a fortress of proof they simply can’t tear down. A truly unshakeable fire damage claim isn’t a simple list of things you lost; it’s a meticulously documented case that gives your insurer zero room to lowball or deny what they legally owe you.

Think of it this way: the insurance company’s adjuster is the opposing counsel, and you’re preparing for court. Their job is to find holes in your story and systematically devalue your losses. Your job is to hit them with such overwhelming evidence that they have no choice but to pay you fairly. This means going way beyond a quick walkthrough and creating a powerful, detailed record of every single thing that was damaged or destroyed.

Document Everything Like a Forensic Investigator

Your smartphone is your single most powerful weapon right after a fire. As soon as it’s safe to re-enter the property, start recording everything. Don’t just snap a few wide shots of a burned room; you have to get granular.

- Capture the Obvious: Get clear photos of all charred structures, burned furniture, melted appliances, and anything else with visible fire damage.

- Focus on the Hidden: This is where adjusters try to cut corners. Record the smoke stains creeping up the inside of your kitchen cabinets. Get video of the soot inside your HVAC vents. Document the warped baseboards and swollen drywall from the water used to fight the fire.

- Narrate Your Videos: As you walk through, talk to your phone. Describe what you’re seeing and what used to be in each space. “This was where the antique grandfather clock stood… this entire wall of books is now a total loss.” This verbal record is priceless later on.

This kind of detailed visual evidence is your frontline defense against an adjuster trying to dismiss severe smoke and water damage as a simple “cleanup job.”

Create an Itemized Inventory of Your Life

Your insurance company is going to demand a list of your personal property. Do not rush this. This document is where they make millions by undervaluing everything from your socks to your sofa. You must build a comprehensive inventory, going room by room, drawer by drawer.

A vague list gives your insurer the power to assign insultingly low values to your belongings. A detailed, evidence-backed inventory forces them to acknowledge the true cost of making you whole again.

For every single item, you need to document the following:

- Item Description: Be specific. Not just “toaster,” but “Breville 4-Slice Smart Toaster, Model BTA840XL.”

- Age and Condition: Be honest about how old it was and what shape it was in before the fire.

- Original Cost: Dig up receipts, bank statements, or credit card records if you can.

- Replacement Cost: This is crucial. Research what it would cost to buy that exact item brand new today.

Yes, this process is tedious and emotionally draining, but it is absolutely non-negotiable. The principles of meticulous documentation are universal in property claims, which is why resources like this complete guide to a wind-damaged roof insurance claim are so valuable—the fight is the same, just the cause is different.

Control the Narrative and the Numbers

Never, ever rely on the contractors and “experts” your insurance company sends out. Their loyalty is to the insurer who gives them a steady stream of work, and they are almost always pushed to keep repair estimates as low as possible.

You must get your own independent estimates from trusted, local contractors who work for you. This creates a competing bid and instantly exposes how low the insurance company’s offer really is.

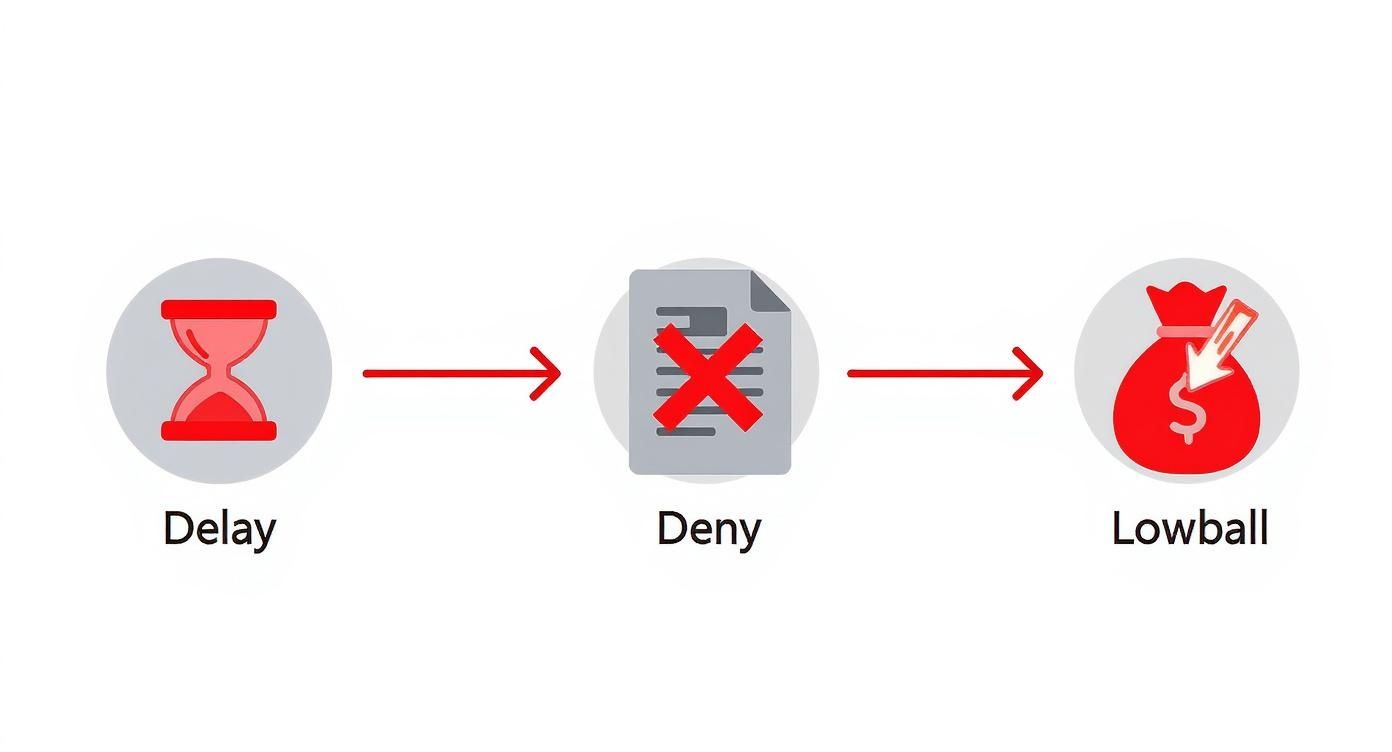

The infographic below shows the playbook insurers use to wear you down and cheat you out of a fair settlement.

This isn’t random—it’s a deliberate strategy. They delay, they deny, and they offer pennies on the dollar, hoping you’re too exhausted to fight back.

Just look at a case study involving a North Carolina family whose home was devastated by fire and smoke. Their insurer, one of the biggest names in the business, came in with an initial offer of $150,000. Their logic? Most of the family’s possessions could simply be “professionally cleaned.”

Feeling completely defeated, they hired a public adjuster. The first thing the PA did was bring in an industrial hygienist who tested the “cleanable” furniture. The results showed it was contaminated with toxic carcinogens, making it a total loss. Armed with this proof, a painstaking inventory with real-world replacement costs, and independent repair bids, they went back to the insurer.

The final settlement was over $400,000. That’s the power of building an unshakeable case with irrefutable proof.

Your Evidence Toolkit for Disputing a Lowball Offer

When your insurer comes back with an insulting offer, you can’t just say, “That’s not enough.” You have to prove it. This table breaks down the essential evidence you’ll need to build your case and force their hand.

| Evidence Category | What to Collect | Why It’s Critical |

|---|---|---|

| Visual Proof | Dated photos & videos of all damage (structural, smoke, water) | Counters claims that damage is minor or pre-existing. Establishes the full scope of the loss. |

| Personal Property Inventory | Detailed, itemized spreadsheet with descriptions, age, and replacement costs | Prevents the insurer from assigning generic, low-ball values. This is often the largest part of a claim. |

| Proof of Value | Receipts, credit card statements, and original purchase records | Substantiates the original cost and quality of your items, making it harder for them to depreciate heavily. |

| Independent Estimates | Repair/rebuild bids from 2-3 trusted, local contractors | Creates a direct apples-to-apples comparison that exposes the insurer’s low estimate. |

| Expert Reports | Evaluations from specialists (engineers, industrial hygienists) | Provides third-party, scientific proof of hidden damages like structural issues or toxic contamination. |

| Communication Log | A record of every call, email, and letter with your insurer | Documents delays, contradictions, and bad faith tactics, creating a timeline of their behavior. |

Think of this toolkit as your ammunition. Without it, you’re walking into a gunfight with nothing but harsh words. With it, you have the power to dismantle their arguments and demand the settlement you deserve.

The High-Stakes Economics of Modern Fire Claims

If that first lowball offer for your fire damage claim feels more like a corporate smackdown than a good-faith negotiation, you’re not just being sensitive. It’s not personal. It’s a cold, hard business decision driven by the massive financial pressure cooker the insurance industry now lives in.

Once you understand this economic reality, you’ll see exactly why you need a professional advocate in your corner.

The entire landscape of fire risk has been turned on its head. Insurers aren’t just dealing with the occasional kitchen fire anymore. They’re getting hammered by catastrophic wildfires that can erase entire towns from the map in a single afternoon. These disasters trigger staggering, industry-wide losses, forcing giants like State Farm and Allstate to clamp down on every single claim they pay out. And that includes yours.

The New Reality of Catastrophic Losses

We’re living in an era of unprecedented natural disasters, and the price tag is astronomical. In just the first half of 2025, global insured losses from natural catastrophes exploded to $80 billion. A massive slice of that came from California wildfires, which racked up an estimated $40 billion in claims—the single most expensive insured wildfire event in history. As you can learn more about these catastrophic fire damage claim statistics, these numbers reveal a terrifying new normal.

When an insurance carrier has to pay out billions for a single event, they don’t just quietly absorb it. They go on the defensive, aggressively managing costs everywhere else. This means every claim, from a small kitchen flare-up in North Carolina to a total loss in a wildfire zone, gets put under a microscope with one goal: minimize the payout.

Your individual fire damage claim isn’t just a line item on some local adjuster’s report. It’s a tiny cog in a multi-billion-dollar corporate machine designed to offset catastrophic losses by systematically underpaying every policyholder they possibly can.

That immense pressure rolls downhill, right onto the company adjuster they send to your home. They are trained, incentivized, and graded on their ability to save the company money. That saving comes directly out of your settlement check.

How This Affects Your Settlement

This high-stakes game means insurers are more willing than ever to play hardball. They’ll insist that smoke-damaged furniture just needs a “good cleaning,” knowing full well that toxic soot and acidic residue have ruined it. They’ll push hard for an Actual Cash Value (ACV) settlement, a depreciated figure that leaves you with pennies on the dollar compared to what it actually costs to rebuild or replace. Understanding the difference is non-negotiable, and our guide on why ACV vs RCV matters in your claim breaks it down clearly.

Because insurers are playing a numbers game on a colossal scale, your claim isn’t seen as a promise to be kept. It’s an expense to be managed and controlled.

This is exactly why fighting back is no longer an option—it’s a necessity. You’re not up against one difficult adjuster; you’re up against a systemic business practice. Knowing that should reinforce the absolute need for an expert who lives in this world and knows how to force the insurance company to honor the policy you paid for.

Why a Public Adjuster Is Your Strongest Ally

After a fire, your insurance company will send their adjuster to your property. They’ll be polite and use reassuring language, but don’t be fooled for a second: their job is to protect their employer’s bottom line.

They are a trained employee of a massive corporation, and their primary goal is to minimize your fire damage claim payout. You would never go to court against a powerful legal team without your own lawyer. Why would you face their financial expert without your own?

This is where a public adjuster becomes your most critical asset. A public adjuster is a state-licensed insurance professional who works exclusively for you, the policyholder. They have zero loyalty to the insurance company. Their only mission is to level the playing field and force the insurer to pay the maximum settlement you are owed under your policy.

A Fundamentally Different Mission

The difference between the company adjuster and your public adjuster isn’t just about who signs their paycheck—it’s a massive conflict of interest. The company adjuster is paid to find ways to limit your claim. Your public adjuster is motivated to find every ounce of damage and all applicable coverage to maximize it.

Think about the stark contrast in how they operate:

- The Company Adjuster: Shows up for a quick, surface-level walk-through. They’ll suggest that smoke-damaged walls just need a fresh coat of paint or that soot-covered appliances can be simply “cleaned,” conveniently ignoring the corrosive long-term damage.

- The Public Adjuster: Conducts a forensic-level investigation. They get into the attic, pull back drywall, and bring in specialists like industrial hygienists to test for the hidden toxins and carcinogens left behind by smoke—the kind of damage the company adjuster hopes you never find.

This evidence-based approach completely flips the script on the negotiation. It’s no longer about what the insurance company wants to pay; it’s about what they are contractually obligated to pay.

Decoding Your Policy and Documenting Your Loss

Insurance policies are dense legal contracts written by teams of lawyers to protect the insurer, not you. A public adjuster speaks this language fluently. They dig into every line of your policy to uncover coverages you probably don’t even know exist, like additional living expenses, code upgrade requirements, or business interruption losses. You can find out more about the vital role of a public claim adjuster in our detailed guide.

From there, they build an ironclad case on your behalf. This means creating a meticulous, room-by-room inventory of every single item you lost, complete with accurate, real-world replacement costs. They photograph, video, and document every square inch of damage, leaving the insurance company no room to argue or lowball your loss.

A public adjuster doesn’t just argue with your insurer; they hit them with a mountain of undeniable proof that makes a lowball offer indefensible.

This professional documentation and aggressive negotiation are the difference between winning and losing. Without an expert advocate, policyholders are often left to fight a losing battle, worn down by delays and confusing jargon until they give up and accept a fraction of what their claim is truly worth.

A Case Study in Getting What You Deserve

Take the story of a Raleigh business owner whose commercial kitchen was hit by a severe electrical fire. The initial assessment from their carrier—a big national insurer—came back with a settlement offer of $200,000. The company adjuster argued that most of the structural damage was minor and the smoke-damaged equipment could be salvaged with some specialized cleaning.

Feeling completely overwhelmed and undervalued, the owner hired For The Public Adjusters. The PA immediately brought in a structural engineer and an industrial hygienist. The engineer found that the fire had critically weakened key roof trusses—damage the company adjuster either missed or ignored. The hygienist’s tests confirmed the “salvageable” stainless steel equipment was contaminated with carcinogenic compounds, making it a total loss.

Armed with expert reports and a detailed business interruption analysis, the public adjuster reopened the fight. They systematically dismantled the insurer’s flimsy initial assessment, proving it was built on incomplete and faulty information.

The final settlement was over $750,000—more than three times the original offer. This is the real, life-altering difference a dedicated advocate makes when you’re fighting a corporate giant for your financial survival.

Holding Insurers Accountable with Legal Action

When the endless delays, insulting lowball offers, and flat-out denials cross the line, you are not out of options. You don’t have to just take it. The law gives you a final, powerful way to fight back against an insurance company that handles your fire damage claim in bad faith.

Taking legal action is the last stand. It’s how you hold a corporate giant accountable for breaking the simple promise they made to you.

https://www.youtube.com/embed/ws2aC6uMPvM

When your insurer deliberately fails to uphold their duty to treat you fairly and honestly, that’s not just bad business—it’s an act of bad faith. This isn’t a simple customer service hiccup; it’s a legal violation. It opens the door for you to sue not just for every penny you’re owed on your claim, but for additional punitive damages as well.

Landmark Cases and Precedents

Let’s be clear: courts all over the country have hammered insurance giants for putting profits ahead of people. These major legal victories are a stark warning to the industry that dishonest, systemic games will not be tolerated.

One of the most famous examples is Campbell v. State Farm, where the U.S. Supreme Court upheld a massive punitive damages award against the insurer for its nationwide scheme to cap payouts and systematically deny valid claims. Evidence revealed a corporate culture that rewarded adjusters for meeting arbitrary payment targets, regardless of the claim’s actual value.

When a court determines an insurer’s behavior wasn’t just a mistake but a calculated, company-wide pattern of bad faith, the financial penalties are designed to hurt. This is how the legal system punishes and deters this kind of corporate greed.

These lawsuits expose a very ugly truth. Sometimes, the only language a massive corporation like State Farm or Allstate truly understands is a court order.

When to Consider Legal Action

Suing your insurance company is a huge step, and it’s usually the final move after everything else has failed. If you’ve laid out undeniable proof, filed formal appeals, and are still hitting a brick wall of denial or getting offers that are just plain offensive, it’s probably time to talk to an attorney who specializes in bad faith insurance law.

This is the nuclear option, often taken after your public adjuster has hit a dead end in negotiations. The mountain of evidence your PA has built for your claim now becomes the bedrock of your legal case, providing the hard proof needed to show the insurer acted unreasonably. If you’re not there yet, our guide explains how to appeal a denied insurance claim and can help you get organized for the earlier stages of the fight.

Filing a lawsuit sends the loudest possible message: you will not be bullied. You will not be scared into accepting a fraction of what your policy guarantees. It forces the insurer to finally take your fire damage claim seriously and face real consequences for their actions.

Common Questions in a Disputed Fire Claim Fight

When your insurance company decides to play hardball with your fire damage claim, the confusion can be paralyzing. Here are some blunt answers to the questions we hear every single day from homeowners and business owners just like you.

Why Is My Insurer Calling This a “Partial Loss”? It Looks Destroyed.

Insurance carriers like State Farm and Allstate love the term “partial loss” because it’s a license to lowball you. Calling catastrophic damage “partial” is a deliberate strategy to justify cheap, corner-cutting repairs instead of the full replacement you actually need.

They’ll push for quick fixes like “ozone treatments” or “specialized cleaning” for materials saturated with toxic smoke and soot. They know full well that a proper restoration often requires tearing everything down to the studs, but the “partial loss” label gives them the excuse they need to offer you pennies on the dollar.

Do I Have to Use the Contractor My Insurance Company Sent?

Absolutely not. You are never required to use your insurer’s “preferred” contractor. Think about it: who does that contractor really work for? The company that feeds them a steady stream of jobs, or you? Their loyalty is to the insurer, and their goal is to keep repair costs as low as possible.

You have the right to hire your own independent contractor—someone who answers only to you. A good public adjuster will have a network of vetted, aggressive contractors who provide honest, detailed estimates that expose just how inadequate the insurance company’s initial offer really is.

My Adjuster Says They Can “Clean” My Soot-Damaged Belongings. Should I Let Them?

Letting an insurer “clean” items exposed to a modern fire is a massive gamble with your family’s health. The soot and smoke from today’s fires aren’t just messy; they’re a toxic cocktail of chemicals and carcinogens that seep deep into porous materials like furniture, clothing, and even electronics.

A simple “smell test” is completely meaningless. The only way to know if your home and belongings are safe is through scientific testing by a certified industrial hygienist.

Insurers push for “cleaning” because it’s exponentially cheaper than replacing your property. A public adjuster will immediately demand that the insurance company pay for an industrial hygienist to test everything. When the results prove toxic contamination, the insurer is forced to declare those items a total loss and pay you to replace them. It’s a non-negotiable step to protect your family’s future.

How does a Public Adjuster document hidden structural damage caused by fire, heat, and firefighting efforts?

We use structural engineers and forensic thermal imaging to assess integrity loss not visible to the naked eye. We also document water damage from the fire department's suppression efforts, ensuring the insurer pays for secondary losses like mold remediation and complex drying protocols.

How is a Fire Claim's Additional Living Expenses (ALE) correctly maximized when I cannot return home?

A Public Adjuster ensures your ALE covers not just rent, but the full difference between your pre-loss lifestyle and your temporary one, including utilities, pet boarding, increased mileage, and food costs, and negotiates for adequate duration (often 12+ months) for a complete rebuild.

What specific policy endorsement is essential to ensure I can rebuild my fire-damaged property up to current building code?

You must have the Ordinance or Law coverage endorsement. This benefit pays for the increased costs associated with meeting new municipal building codes (e.g., modern wiring, stricter foundations) that were not required when your home was first built. Your Public Adjuster ensures this is utilized.

How do you accurately calculate the true Replacement Cost Value (RCV) for highly custom home components lost in a fire?

We utilize expert appraisals and specialized Xactimate line items for custom cabinetry, historical millwork, or unique finishes. We reject generic valuations and force the insurer to price "like kind and quality" replacements from specialty, high-end vendors, not low-cost suppliers.

What is a "Contents Inventory Specialist," and why is one essential for a complex fire claim?

For total loss or severe damage, a Public Adjuster employs a Contents Specialist to create a line-by-line, room-by-room inventory that documents not just the item, but its age, original cost, brand, and RCV. This prevents the insurer from minimizing the value of thousands of items with a simple lump-sum estimate.

How is the intangible and persistent issue of smoke and soot damage fully quantified and paid for?

Smoke and soot cause microscopic, acidic damage that requires specialized HVAC system cleaning, ozone treatment, and complex air scrubbing. Your Public Adjuster ensures the estimate includes professional remediation companies, not basic cleaning, to guarantee the property is medically safe and odor-free.

Can the insurance company force me to accept cash-out instead of paying for the full repair or rebuild?

No. If your policy is Replacement Cost Value (RCV), the insurer is required to pay the full cost to return your home to its pre-loss condition, up to the policy limits. A Public Adjuster ensures that any "cash-out" option is based on a full, fair RCV estimate, not a lowball compromise.

What evidence is used to successfully overturn a fire damage claim denial based on suspicion of misrepresentation or arson?

A Public Adjuster can help guide you through the process the carrier is taking against you via a separate fire investigation or by assisting with your Examination Under Oath (EUO). The carrier will usually require these along with personal financial documents. PAs can assist in gathering such documents requested by the carrier to disprove any motive and defending the policyholder's integrity.

- You can obtain your own independent, certified fire investigator (CFI) to produce an origin and cause report that directly refutes the insurer's findings.

- An Examination Under Oath (EUO) is a formal, legal procedure where the insurance company's representative (often an attorney) takes a recorded statement and questions the policyholder. The insurance company uses this to get detailed information about the claim and to check for any inconsistencies or signs of fraud. A public adjuster can prepare you for the EUO by explaining the process and anticipating the types of questions you will be asked and help you secure an attorney for this process if needed.

If the insurance company delays payment or processing of my fire claim, what financial penalty can I impose?

A Public Adjuster leverages state Fair Claims Settlement Practices Acts, which mandate specific timelines. Unreasonable delays can lead to the insurer being liable for interest on the delayed payment and potential exposure to a bad faith lawsuit if the delays are prolonged or malicious.

How does the Public Adjuster coordinate the RCV recovery process after the initial ACV payment for a fire loss?

The Public Adjuster works with the contractor, tracking repair milestones and receipts. They submit periodic supplemental requests for the depreciation holdbacks, ensuring the policyholder receives the full RCV funds necessary to complete the rebuild without being forced to pay out-of-pocket first.

How does a Public Adjuster manage the involvement of the mortgage company on the fire settlement check?

For substantial fire losses, the mortgage company is listed as a payee because of the Mortgage Clause in most policies. The Public Adjuster can assist and guide you, providing the bank with the approved scope of work and contractor details, helping establish a draw schedule to ensure funds are released in stages as repairs are certified complete.

When your insurance company is playing games, you can’t afford to fight alone. You need a professional gladiator on your side. The team at For The Public Adjusters, Inc. works exclusively for policyholders like you to force insurers to pay what you’re actually owed under your policy. Don’t let them intimidate you into accepting a weak settlement. Get a no-cost claim review and show them the fight is on. Visit us at https://forthepublicadjusters.com and get the expert help you deserve.