The water may be gone, but your fight usually starts when the flood adjuster shows up.

You're standing in a house or business that still smells like silt, sewage, and wet drywall. Floors are buckled. Appliances are shot. The lower cabinets are swollen. The adjuster walks through quickly, takes a few notes, and acts like the loss is smaller than what you're staring at. Then the estimate comes in low, key items are missing, and suddenly the primary stress isn't just the damage from a flood. It's the claim dispute.

That frustration is justified. Flood claims under FEMA's National Flood Insurance Program are notorious for strict rules, technical traps, and low-ball handling through NFIP and Write Your Own carriers. If you already filed and now you're stuck with delays, denials, or a weak estimate, you need a fight plan, not another generic article about reporting a loss.

Table of Contents

- The Second Disaster Your NFIP Adjuster Brings

- Why Your Flood Claim Is Not a Normal Insurance Claim

- Decoding the Four Types of Flood Damage Adjusters Undervalue

- Your Evidence Checklist to Fight a Low-Ball Estimate

- The Proof of Loss The Most Important Document in Your Fight

- Why a Public Adjuster Is Your Best Weapon Against NFIP

- Get Expert Claim Help Do Not Fight the Insurance Company Alone

The Second Disaster Your NFIP Adjuster Brings

After a flood, many expect the hard part to be the cleanup. It isn't. The hard part is realizing the person sent to “adjust” your claim often approaches your loss like a cost-control exercise.

That's why so many homeowners and business owners feel blindsided twice. First by the water. Then by the estimate.

A typical scene looks like this. The adjuster notes visible flood lines, takes a few room measurements, and focuses on what can be cleaned instead of what should be removed and replaced. Damaged drywall becomes a “minor repair.” A compromised cabinet run gets treated like partial salvage. Mechanical systems get a quick look, not a serious evaluation. Then you get a low number and a lot of silence.

That pattern hits people outside mapped flood zones especially hard. According to research on underestimated U.S. flood damage risk, FEMA's 100-year flood plain maps only 221,000 square miles, while recent computer modeling shows a high probability of flood damage across 1.01 million square miles of U.S. land. That's over 4.5 times more territory at risk than many property owners assume. The same source states that just one inch of flooding can cost an average of $25,000.

The adjuster is not your recovery coach

NFIP and WYO adjusters may be polite. That doesn't make them your advocate.

Their estimate is not the final word. Their scope is often incomplete. Their first pass regularly misses the full damage from a flood because they're looking for what they can limit, not what you need to restore the property properly.

Practical rule: If you're talking to a flood adjuster, don't treat the conversation casually. The things you say about pre-loss condition, cleanup, prior issues, and what “looks okay” can all be used to shrink the claim.

If you need to tighten up how you communicate once the claim turns adversarial, read these mistakes to avoid when speaking with a water claim adjuster.

Low-ball flood handling usually starts with scope

The first estimate often sets the tone for the whole fight. If the carrier under-scopes demolition, omits contaminated materials, ignores hidden moisture, or treats damaged systems as reusable without proper support, you end up arguing uphill from day one.

That's why you need to stop thinking, “They've seen this before, so they'll do the right thing.”

You need to think, “I have to prove every dollar.”

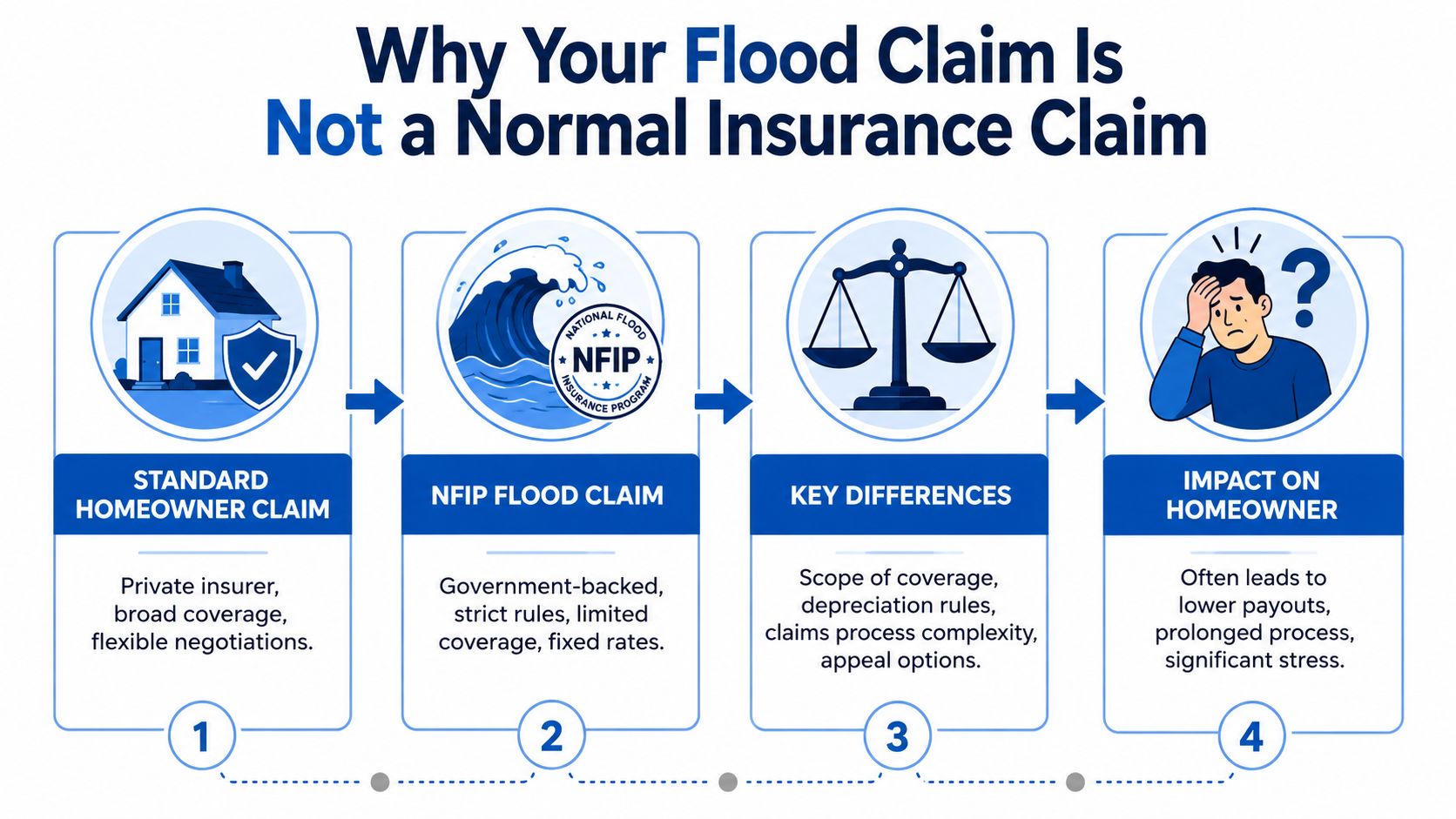

Why Your Flood Claim Is Not a Normal Insurance Claim

A standard homeowners carrier dispute is one thing. An NFIP flood claim is a different animal.

Flood insurance under FEMA and the NFIP runs on rigid federal rules. Even when a private insurer name appears on the paperwork through a WYO arrangement, the claim process doesn't behave like a normal dwelling or business owner property dispute. The deadlines are tighter, the wording is stricter, and your margin for error is smaller.

Federal rules change everything

The biggest mistake I see is homeowners assuming flood claims work like ordinary property claims. They don't. People think the adjuster's estimate starts a negotiation. In NFIP claims, the paperwork and proof requirements can decide the outcome long before anyone talks settlement in a meaningful way.

That's why weak documentation becomes expensive fast. The adjuster can miss line items, skip categories of damage, or undervalue repair needs, and the policyholder is left trying to undo that damage under a system that doesn't give much room for sloppy submissions.

To understand how carriers and adjusters frame these claims, this video is worth watching before you push back:

Why delays and disputes keep happening

This isn't paranoia. The dispute history is there.

Empirical legal analysis of NFIP disputes after Hurricanes Katrina and Rita found that over 165,000 flood insurance claims were submitted after those storms, with systemic delays and unresolved disputes showing how inadequate the process has been for policyholders. If you're dealing with a low-ball estimate, repeated requests, or a denial dressed up as “insufficient documentation,” you are not dealing with a rare exception.

The system puts the burden on the property owner to be precise, organized, and aggressive. If you wait for the carrier to build your case for you, you lose leverage.

Here's the plain-English comparison:

| Claim issue | Standard property dispute | NFIP flood dispute |

|---|---|---|

| Rules | Usually policy and state-based | Federal policy language controls |

| Adjuster role | Company-focused | Company-focused under stricter federal framework |

| Missing items | Often negotiable later | Can become a serious proof problem |

| Deadlines | Important | Ruthless |

That's why damage from a flood needs to be treated as a documentation war. Not a customer service problem. Not a misunderstanding. A documentation war.

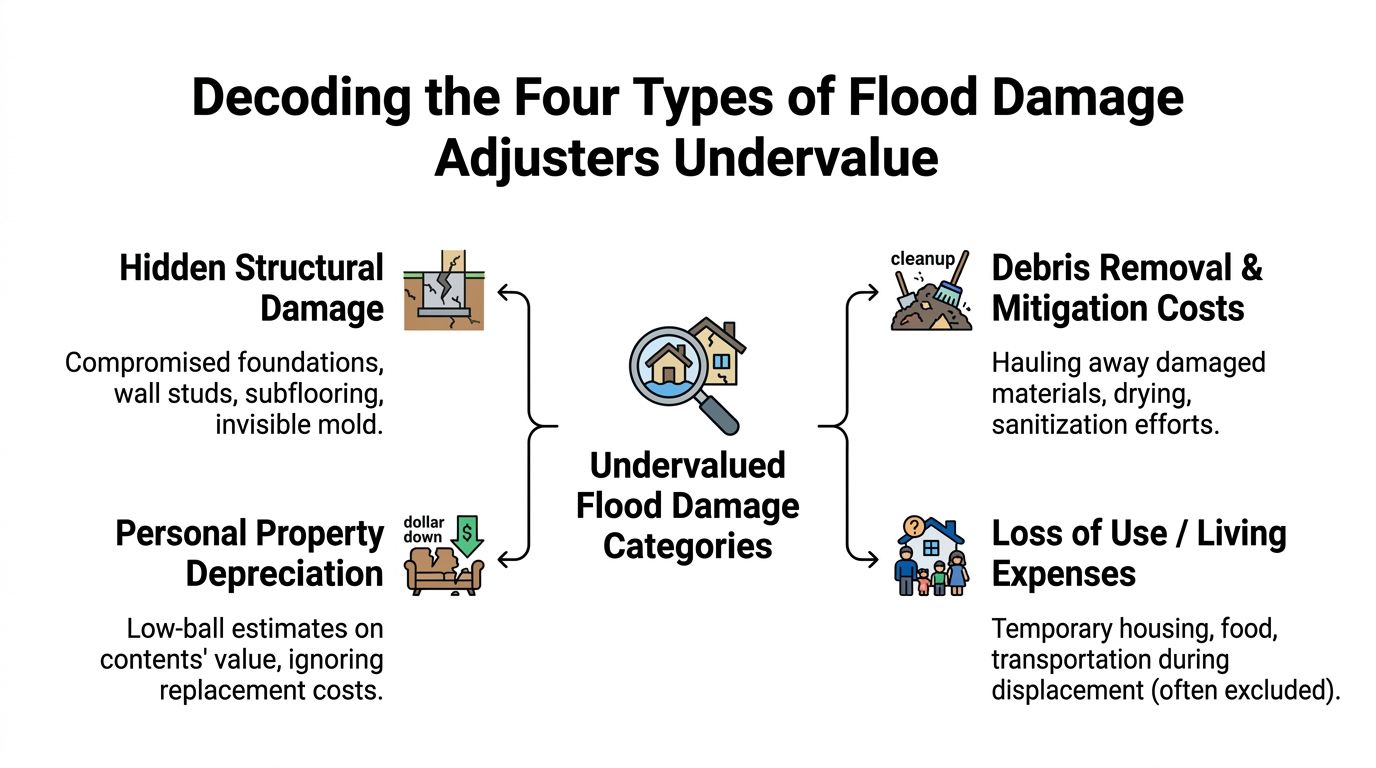

Decoding the Four Types of Flood Damage Adjusters Undervalue

The flood line on the wall is only the beginning. What gets missed or minimized is usually where the money disappears.

Structural damage that gets treated like cosmetic damage

Flood adjusters often reduce structural damage into simple cleanup language. That's a serious problem.

Technical flood-damage modeling uses vulnerability functions and fragility functions to connect inundation level and flow velocity with actual building damage, and the modeling shows that structural damage is not linear. Higher flow velocity increases the probability of severe failure, as described in research on structural flood damage assessment. In plain language, the same water depth can produce very different structural outcomes depending on force, building type, and material condition.

Watch for these common under-scoped items:

- Wall systems: Adjusters may price a lower cut or spot replacement when the wall cavity, insulation, studs, and fasteners were all exposed to flood conditions.

- Subfloors and framing: A floor that “looks dry now” can still be compromised.

- Foundations and supports: Cracking, shifting, erosion, and settlement don't always announce themselves during a quick walk-through.

Systems contents and contamination that get shortchanged

Flood losses don't stop at drywall and flooring. The expensive fights usually involve what's behind walls, under cabinets, and inside equipment.

Mechanical and electrical systems are frequent targets for underpayment. HVAC components, wiring, outlets, plumbing connections, and appliances may get written as clean-and-test items when replacement or deeper repair is more reasonable. If floodwater reached areas where plumbing components were affected, practical guidance like MG Drain Services LLC's pipe repair tips can help you distinguish between a minor issue and the kind of system damage that needs a licensed evaluation.

Then there's contents. Carriers often depreciate aggressively, overlook full item groups, or ignore how flood contamination affects usability. Furniture, inventory, electronics, textiles, tools, and stored materials may be written down to almost nothing unless you itemize them carefully.

Flood claims get smaller every time a damaged item is described loosely. “Bedroom contents” is weak. A room-by-room inventory with model names, photos, and replacement support is stronger.

The fourth category is contamination, including mud, sewage residue, and microbial growth concerns. Carriers love to frame this as ordinary cleanup. Property owners are the ones left paying when sanitation, removal, and proper rebuild standards aren't included.

Here's the short version of where adjusters cut corners most often:

- Hidden structural compromise

- Mechanical and electrical components

- Contents valuation

- Contamination and remediation scope

If those four categories aren't fully developed, your flood estimate is probably incomplete.

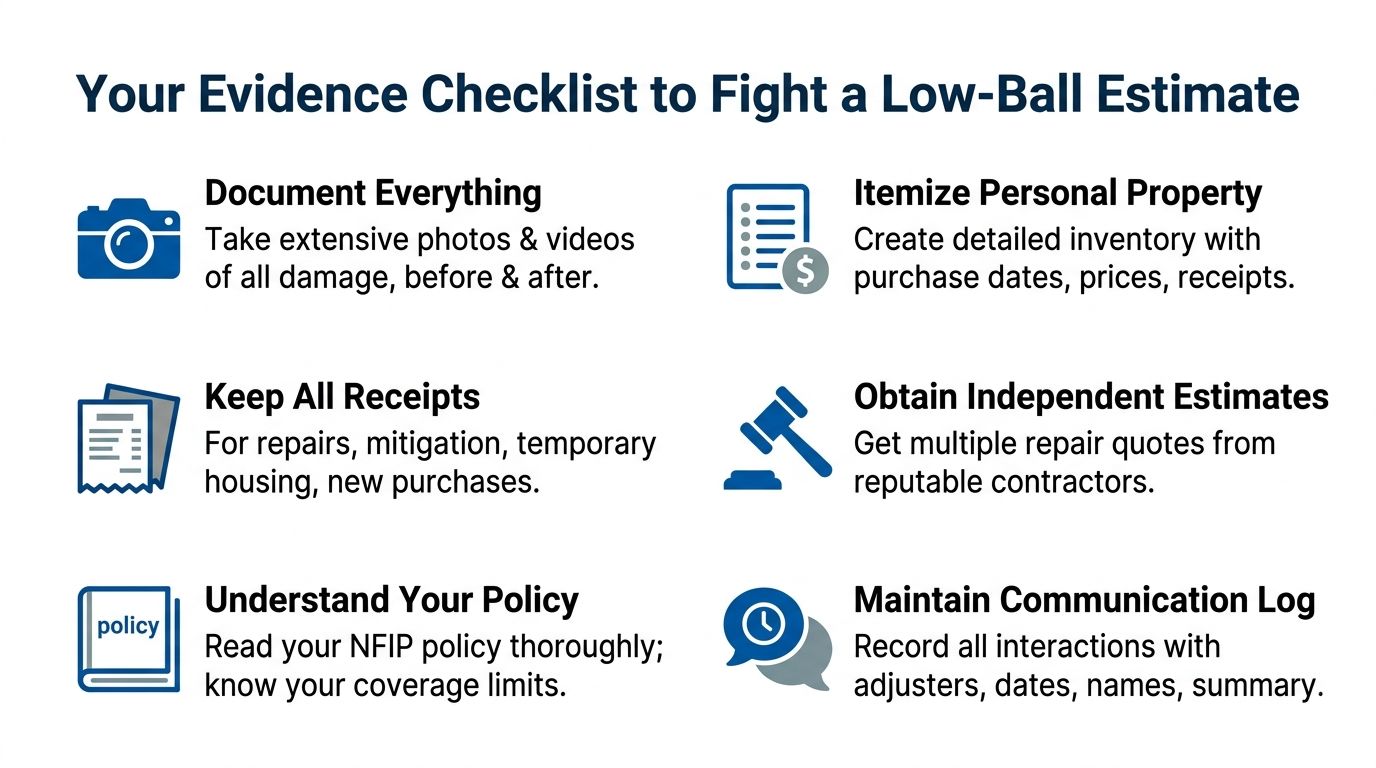

Your Evidence Checklist to Fight a Low-Ball Estimate

You don't win a flood claim dispute by saying the estimate feels unfair. You win by building a file that's harder to dismiss than the carrier's version of the loss.

What FEMA says you need to document

FEMA's Office of the Flood Insurance Advocate says claimants should document all damages with photos, videos, high-water line measurements, appliance serial numbers, and receipts before repairs begin, and it emphasizes that payments are based on documented evidence and that the adjuster's estimate is not final if items were missed, as explained in this Flood Insurance Advocate guidance video.

That instruction matters because many people make the same mistake. They assume the adjuster saw enough. He didn't.

Your evidence file should include:

- Wide photos first: Show every affected room from multiple corners so no one can later argue the layout or extent was unclear.

- Tight photos second: Get close shots of baseboards, buckled floors, swollen trim, stained wall cavities, rust marks, damaged panels, and mud lines.

- Video walkthroughs: Narrate what room you're in, what the water touched, what was removed, and what still smells, stains, warps, or malfunctions.

- Water line proof: Mark and measure high-water lines before they disappear during cleanup.

- Appliance data plates: Serial and model information helps identify what was there and supports replacement arguments.

- Receipt preservation: Keep mitigation, cleanup, temporary repair, and emergency purchase records together.

How to build a file the carrier can't ignore

Don't throw damaged property away until it's fully documented. That includes cabinets, flooring, cut drywall, damaged inventory, soaked furniture, detached trim, and affected equipment. If disposal becomes necessary, photograph it in place, during removal, and in the debris pile.

Get your own contractor and specialist opinions. Not vague verbal comments. Written estimates. Written scopes. Written notes about why materials need removal, why systems failed, and what code or practical repair realities affect the rebuild.

Use a simple evidence structure:

| Evidence type | What to capture | Why it matters |

|---|---|---|

| Photos | Every room, every elevation, every damaged component | Prevents “not observed” arguments |

| Video | Walkthrough with narration | Captures condition before changes |

| Estimates | Independent repair and replacement scopes | Counters the carrier's low scope |

| Contents list | Item description, brand, model, age, cost support | Stops blanket depreciation games |

| Communications log | Date, person, summary, next step | Exposes delays and contradictions |

A strong contents list should be room-by-room, not random. Kitchen first. Living area next. Bedrooms after that. Then utility spaces, storage, office, and exterior structures if covered. Include photos, receipts if available, owner notes if receipts are gone, and replacement references where possible.

Field advice: If you repaired or cleaned something because you had no choice, document what it looked like before, during, and after. Emergency action doesn't erase flood damage. Poor documentation does.

Keep a claim diary. Write down every call, email, inspection, promise, request, and missed callback. Names matter. Dates matter. Contradictions matter. When the dispute sharpens, a detailed communication log becomes an advantage.

The goal isn't to overwhelm the carrier with paper. The goal is to leave them with fewer excuses.

The Proof of Loss The Most Important Document in Your Fight

If you remember one thing from this article, remember this. The Proof of Loss is where many flood claims are won or lost.

Under the Standard Flood Insurance Policy, policyholders must submit a signed, sworn, and itemized Proof of Loss within 60 days of the flood event to claim more than the insurer's initial offer. If you fail to submit a complete Proof of Loss with a specific loss amount, the result is automatic denial, as explained in this breakdown of the SFIP Proof of Loss requirement.

That deadline isn't a suggestion. It's a trap door.

Why the adjuster's number is not your number

A lot of policyholders make a costly mistake. They assume the adjuster's estimate is the amount that belongs on the Proof of Loss. That can box them into the carrier's version of the claim.

If the estimate is low, incomplete, or flat-out wrong, your Proof of Loss should reflect your documented amount, not the number that makes the insurer comfortable.

That means you need support for the figure. NFIP-related damage estimation guidelines use staged damage concepts and direct-plus-indirect damage thinking. The Federal Flood Damage Estimation Guidelines describe direct residential flood damage by estimating costs for each 300 mm of water depth and define total damages as Direct Damages + Indirect Damages, with indirect costs including evacuation expenses and business interruption. The same guidance also calls for locally developed or regionally adjusted stage-damage functions by building class.

For homeowners and business owners in a dispute, the lesson is simple. Flood damage valuation is supposed to be systematic and property-specific. A quick generic estimate that ignores real building conditions deserves to be challenged.

What makes a Proof of Loss strong

A strong Proof of Loss isn't just a form with a higher number typed in. It's a supported demand package.

Build it like this:

State a specific amount

Use an exact claimed amount based on your evidence. Never leave it undetermined.Attach itemization

Break down building damage, contents, and other documented covered categories clearly.Include support

Add contractor estimates, photographs, inventories, invoices, measurements, expert notes, and anything else that backs the number.Sign and swear to it

This is a formal claim statement. Treat it that way.Meet the deadline

A great package sent too late is still a losing package.

If you need a deeper understanding of how this document works in real disputes, review this guide on the flood claim Proof of Loss process.

Your Proof of Loss is your formal rejection of a low-ball position. If you don't put your real number in play correctly and on time, the carrier's number controls the fight.

Don't let the insurer turn your silence, confusion, or delay into a denial.

Why a Public Adjuster Is Your Best Weapon Against NFIP

Flood claims become dangerous when the carrier has experts and the policyholder has hope. Hope doesn't document a building. Hope doesn't write a better scope. Hope doesn't catch what the adjuster omitted.

A public adjuster works for the policyholder. That difference is everything.

The loyalty problem nobody should ignore

The NFIP or WYO adjuster may say he's there to inspect the loss fairly. Fine. But he still doesn't represent you. He represents the claim process from the insurer side.

When the dispute turns on omitted materials, underestimated quantities, damaged systems, or unsupported depreciation, you need someone whose job is to expand the scope to match the actual damage from a flood. Not defend the first estimate. Not smooth things over. Not tell you to wait.

That's the core reason expert representation matters. The flood claim system is technical, deadline-driven, and unforgiving. The side that organizes the evidence and presents the loss correctly has the advantage.

What professional representation actually changes

A good public adjuster doesn't just argue. They inspect, measure, document, itemize, compare, challenge, and negotiate.

That changes the fight in practical ways:

- Scope gets corrected: Missed rooms, hidden components, and underpriced work get pushed back into the claim.

- Paperwork gets stronger: Supporting records are assembled in the format disputes require.

- Deadlines are managed: The claim doesn't die because a key submission was late or incomplete.

- Pressure shifts: The carrier has to answer a documented position, not a frustrated phone call.

There's also a human side to this. Flooded homeowners and business owners are exhausted. They're cleaning, relocating, paying out of pocket, and trying to decipher policy language at the same time. Professional help gives them a way to stop reacting and start controlling the claim.

You do not need to be an expert in flood insurance. You do need one on your side when the insurer starts acting like your loss is smaller than it is.

If you want to understand what a policyholder advocate does during a property claim dispute, this overview of a public adjuster's role is a good place to start.

Get Expert Claim Help Do Not Fight the Insurance Company Alone

Flood claims under FEMA, NFIP, and WYO handling are built on strict rules and narrow tolerances. That's why so many legitimate claims get underpaid, delayed, or denied after the initial filing is already done.

The practical takeaway is straightforward. Document everything. Challenge missing scope. Take the Proof of Loss seriously. Don't confuse the insurer's adjuster with your advocate.

Property owners who get strong help during a claim dispute usually say the same things in reviews. They appreciated clear communication, fast responses, thorough documentation, and someone who pushed back when the carrier didn't. That's what people remember when they've been ignored or low-balled for weeks.

For The Public Adjusters, Inc. Client Reviews

| Client Name | Review Snippet |

|---|---|

| Homeowner client | Clear communication and strong support during a difficult property claim dispute. |

| Business owner client | Thorough documentation and steady follow-up helped keep pressure on the carrier. |

| Residential policyholder | Professional guidance made the claim process easier to understand and challenge. |

If your payment doesn't match the actual damage from a flood, stop waiting for the insurer to fix its own mistake. Get help and force the claim onto documented ground.

For homeowners and business owners dealing with denied, delayed, or low-balled flood claims, For The Public Adjusters, Inc. represents policyholders, not insurance companies. They help inspect damage, document losses, interpret coverage, and fight for the full amount owed under the policy. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!