When disaster rips you from your home, the last thing you should be worried about is where you’ll live or how you’ll pay for it. That’s what your loss of use coverage is for. It’s a promise baked into your homeowner’s policy, designed to cover your extra living costs so you can keep your life as normal as possible while your home is being rebuilt. Loss of Use coverage, often referred to as Additional Living Expenses (ALE), is the financial safety net that allows you to maintain your standard of living while your home is uninhabitable due to a covered loss. Insurance carriers frequently attempt to restrict the duration and limit the scope of these benefits.

But let’s be clear: it’s a promise your insurance company will often try to twist, downplay, or break entirely.

Don’t Let Them Take Away Your Right to Normalcy

Loss of Use coverage, often called Additional Living Expenses (ALE) or Coverage D, isn’t some luxury add-on. It’s a fundamental part of the policy you pay for every single month. When a covered disaster like a fire, hurricane, or major water leak makes your home uninhabitable, this is the coverage that’s supposed to kick in immediately.

Its whole purpose is to cover the increase in your living expenses—the amount you’re spending above and beyond your normal monthly budget.

This is where the fight usually starts. Insurance giants like State Farm and Allstate have one primary mission: protect their profits. And that means paying you as little as legally possible. They’ll scrutinize every receipt and challenge every expense, hoping to wear you down until you accept a fraction of what you’re owed.

The Insurance Company’s Playbook: Delay, Deny, Defend

You have to understand the dynamic from day one: the company adjuster is not your friend. They are not on your side. Their job is to limit the insurer’s financial payout, which puts them in direct opposition to you. Every dollar they save the company is a dollar out of your pocket.

This coverage is meant to be comprehensive, bridging the huge financial gap created when you’re forced out of your home. It’s much more than just a cheap hotel room.

- Temporary Housing: This should cover a rental home, apartment, or hotel that is comparable to your damaged home in size and quality.

- Increased Food Costs: If your temporary place doesn’t have a kitchen, ALE covers the difference between your normal grocery spending and the much higher cost of eating out.

- Storage Fees: You need a place to put your belongings while repairs are underway. This coverage pays for moving and storing them safely. It’s critical to know the best tips for insuring items in storage to make sure your things are fully protected.

- Extra Transportation Costs: If your rental is farther from work or your kids’ school, the increased gas and mileage costs are covered.

- Other Essential Costs: This can include things like laundry services if you don’t have a washer/dryer, pet boarding fees, and other necessary expenses you only have because you’re displaced.

Below is a breakdown of what your Loss of Use coverage is supposed to do versus the common tactics insurers use to underpay you.

What Your Loss of Use Coverage Should Pay vs How Insurers Deny It

| Covered Expense Category | What It Should Cover For You | Common Insurer Pushback or Lowball Tactic |

|---|---|---|

| Temporary Housing | A rental comparable in size, quality, and location to your damaged home. | Offering a cramped, low-budget hotel room or an apartment in an inconvenient area to save money. |

| Increased Food Costs | The full difference between your normal grocery budget and the cost of restaurant meals if you have no kitchen. | Arguing that you should be cooking in a hotel kitchenette or offering a flat, insufficient per diem rate. |

| Utility & Moving Costs | Costs to set up utilities at your rental, plus the expense of moving and storing your belongings. | Refusing to pay for professional movers or questioning the need for climate-controlled storage for sensitive items. |

| Transportation Expenses | The extra gas and mileage you spend commuting from a temporary location that’s farther away. | Claiming your new commute is not “significantly” longer or refusing to reimburse at the proper mileage rate. |

| Miscellaneous Costs | Pet boarding, laundry services, and other daily expenses you wouldn’t have at home. | Calling these expenses “unnecessary” or “luxury” costs and refusing to cover them. |

This table exposes the game: your policy promises to make you whole, but the insurer’s internal playbook is designed to chip away at that promise, one denied expense at a time.

The reality is that while about 90% of U.S. homeowners policies included this coverage in 2023, the limits are often way too low for a long-term displacement, especially after a major catastrophe. It’s a dangerous gap between what people think they have and what they actually need.

Knowing every protection your policy provides is your first line of defense. Get a head start by understanding the basics of what homeowners insurance covers. When you know your rights, you’re much harder to push around.

Building an Undeniable Record of Your Expenses

When you’re fighting for your coverage loss of use, your greatest weapon isn’t anger or frustration—it’s meticulous, undeniable documentation. Let’s be clear: insurance companies like Allstate and State Farm often count on policyholders being overwhelmed and disorganized. They use missing receipts or poorly justified expenses as leverage to lowball your claim, turning a bureaucratic process into a war of attrition.

To win, you have to build a financial record so solid that their adjuster has no room to argue.

This isn’t just about stuffing receipts in a shoebox. It’s about creating a strategic, detailed expense log that preemptively shuts down every potential denial. You need to think like the adjuster who will scrutinize every dollar and prove that each expense was both necessary and a direct result of being forced from your home.

This flowchart shows the typical, and often frustrating, path homeowners are forced down when filing a loss of use claim.

As you can see, what starts as a disaster can quickly escalate into a conflict with your insurer. Organized documentation is your best defense.

Categorizing Every Single Cost

Your first step is to track your spending in distinct categories. This structure makes it easy to present your costs and a lot harder for the insurer to dismiss them. Get a spreadsheet going or use a dedicated app to log everything.

Break it down like this:

- Temporary Housing: Document every hotel bill, rental agreement, and payment. If you pay a security deposit, log that too.

- Increased Food Costs: Track every restaurant meal, takeout order, and even groceries if your temporary kitchen is less equipped. You’ll need to calculate the difference between this and your normal food budget.

- Transportation: Log every extra mile you drive from a longer commute. Keep gas receipts and note the date, mileage, and purpose of each trip.

- Utilities and Setup Fees: Include any costs to connect electricity, internet, or other services at your temporary place.

- Moving and Storage: Keep invoices from moving companies and the monthly receipts for your storage unit.

- Pet Boarding: If your temporary rental doesn’t allow pets, the cost of boarding them is a legitimate expense.

- Laundry Services: Without a washer and dryer, laundromat or dry-cleaning costs are covered.

For every single entry in your log, you must attach a digital copy of the receipt. This creates a powerful, self-contained record that leaves no doubt about where the money went.

Justifying Expenses to Maintain Your Standard of Living

The most common battleground is the concept of “normal standard of living.” The insurer will argue that your choices were extravagant, even when they were simply necessary. Your documentation is what proves them wrong.

Your policy does not require you to live in the cheapest possible conditions; it requires the insurer to fund a lifestyle comparable to the one you lost. Your detailed records are the evidence that proves your expenses were reasonable, not luxurious.

For example, if the insurer questions your choice of a three-bedroom rental home, your documentation should include a copy of your original home’s floor plan and photos showing its size and features. This proves you needed a similar space. To make sure your records are foolproof, learn about effective strategies to organize your receipts, much like you would for tax purposes. It makes your claim undeniable.

This level of detailed record-keeping is crucial not just for your ALE claim but for formalizing your entire case against the insurer. In many disputes, the insurance company will require you to submit a sworn statement. For a deeper dive into this critical step, review our guide on how to properly complete a Proof of Loss form. Your organized expense log will be the backbone of that document, making your claim almost impossible to dispute.

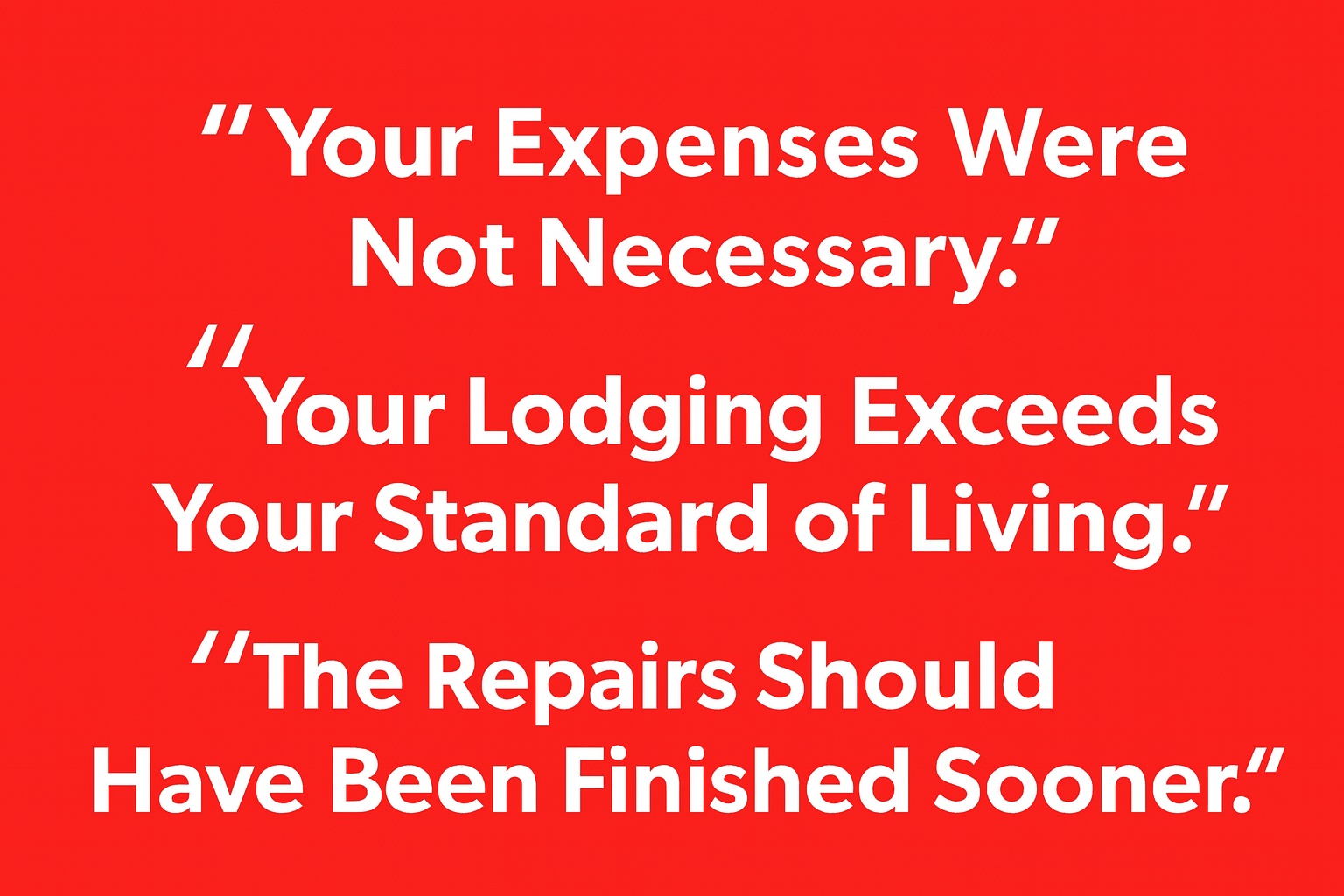

Common Excuses Insurers Use to Deny Your Claim

After a disaster, you expect your insurance company to come through. You’ve paid your premiums, and now you need them to honor their end of the deal. Instead, you’re often thrown onto a battlefield where every receipt is questioned and every decision is second-guessed. Insurance giants have a predictable playbook of excuses they use to deny, delay, and lowball your coverage loss of use claim—all to protect their profits.

Understanding these bad-faith tactics is the first move in fighting back. Let’s be clear: they aren’t just being difficult. They’re running a strategy designed to wear you down until you give up and accept far less than you’re owed. Don’t fall for it.

“Your Expenses Were Not Necessary”

This is one of the most insulting and common excuses you’ll hear from an adjuster. They’ll go through your receipts with a fine-toothed comb, flagging things like a slightly nicer dinner or a specific brand of shampoo, labeling them “luxuries” instead of necessities.

The rebuttal is simple and written right into your policy: coverage is meant to maintain your normal standard of living. If your family ate fresh, healthy meals before the fire, you aren’t suddenly required to live on ramen noodles just because it’s cheaper. Proving your pre-loss lifestyle is the key to shutting down this ridiculous argument.

This isn’t just about your claim; it’s a huge, systemic problem. Between 2016 and 2023, nearly 70% of global losses from natural disasters were uninsured. As insurers feel the heat from rising losses, they get even more aggressive about denying claims like Loss of Use, making the gap between what your policy promises and what they actually pay even wider. You can read more about the global insurance protection gap from the United Nations Development Programme to see just how big this issue is.

“Your Lodging Exceeds Your Standard of Living”

Get ready for the insurer to push you into subpar temporary housing. They might offer a single, cramped hotel room for your family of four or an apartment clear across town in a different school district, all while calling it “reasonable.”

But your policy gives you a powerful word: comparable. You are entitled to a comparable living situation.

- Size and Layout: If you lived in a three-bedroom house with a backyard for the kids, you are entitled to rent a three-bedroom house with a yard.

- Location: The temporary home should be reasonably close to your work, your kids’ schools, and your community.

- Amenities: Did your home have a two-car garage or a dedicated home office? Your temporary place should offer the same.

You are not obligated to downgrade your entire life just to save the insurance company a few bucks. The photos, floor plans, and property records of your original home are the proof you need to force them to approve a genuinely comparable place.

“The Repairs Should Have Been Finished Sooner”

This tactic is particularly dishonest. The insurance company’s adjuster will invent an impossibly short timeline for repairs and then threaten to cut off your ALE benefits on that arbitrary date—whether the work is done or not. They are essentially blaming you for delays often caused by post-disaster contractor shortages or, ironically, their own slow claims handling.

Case Study: Fighting Back and Winning

A Raleigh, NC, family lost their home in a fire. Their insurer, Allstate, tried to give them a measly three months of ALE, claiming repairs would be fast. But with supply chain nightmares and no available contractors, the realistic timeline was closer to nine months. The family was about to be financially ruined.They hired For The Public Adjusters who immediately established a realistic scope of work and repair schedule. Armed with this expert evidence, the public adjuster proved Allstate’s timeline was made up and in bad faith. The family’s coverage loss of use settlement was tripled, covering their entire nine-month displacement.

This story makes one thing crystal clear: the insurance company’s timeline is not law. It’s an opening offer in a negotiation—one you can and absolutely should fight with credible evidence from real construction professionals. When you see these excuses for what they are, you can dismantle their arguments and demand the full and fair settlement you’re owed.

Navigating Flood Damage and NFIP Claim Disputes

When a flood rips through your property, you’re thrown into a completely different, often hostile, insurance world. Flood claims aren’t handled like a standard homeowner’s claim. They fall under the rigid, bureaucratic thumb of the **National Flood Insurance Program (NFIP)**—a system that feels like it’s stacked against you from day one.

The first, and most brutal, shock for many flood victims is discovering a devastating hole in their policy. Standard NFIP policies DO NOT include Loss of Use coverage.

That’s right. While your home is unlivable, there is no automatic coverage for your hotel bills, a temporary rental, or any other extra living expenses. This intentional gap leaves families financially stranded at the worst possible moment.

The Bureaucratic Nightmare of FEMA Aid

With no Loss of Use benefits, your only option is often to turn to FEMA for assistance. But let’s be clear: this is not an insurance payout. You aren’t getting what you’re owed under a policy; you’re applying for limited federal aid that is notoriously slow, insufficient, and wrapped in endless red tape.

You’re no longer a policyholder making a claim. You’re a disaster victim navigating a complex bureaucracy. This process can drag on for weeks or even months, forcing you to pay out-of-pocket while you wait for help that might not be enough to keep you afloat.

Fighting the NFIP and Its Carriers

Beyond the lack of living expense coverage, getting the NFIP or its designated “Write Your Own” (WYO) carriers to pay fairly for the actual flood damage is an uphill battle. The adjusters they send are known for their aggressive, penny-pinching tactics.

- Systematic Lowballing: They are notorious for undervaluing repair costs, offering bottom-dollar estimates that don’t come close to what it actually costs to rebuild.

- Rigid Rules: They hide behind strict federal guidelines, leaving zero room for negotiation or common-sense adjustments based on real-world conditions.

- Delay, Deny, Defend: The entire process is often bogged down by intentional delays and overwhelming documentation requests designed to wear you down until you give up.

It’s no secret that insured losses from natural catastrophes are skyrocketing, with global insured losses topping USD 100 billion in the first half of 2025 alone. As you can learn more about these global insurance market trends, you’ll see how this pressure makes carriers even tougher on claims.

Because loss of use coverage is off the table and the dwelling damage is almost always undervalued, your only path forward is to fight for a fair settlement on your structural claim. This is where getting an expert is non-negotiable.

A public adjuster who specializes in NFIP claims knows the federal rulebook inside and out. They know how to counter the tactics of WYO adjusters, meticulously document your damage, and build an undeniable case to force the maximum possible payout for your home—which is often the only money you’ll ever see.

Why a Public Adjuster Is Your Strongest Ally

Let’s get one thing straight: when you’re going up against a billion-dollar insurance company, it’s not a fair fight. You’re reeling from the trauma of losing your home, trying to hold your life together. They have entire teams of adjusters and lawyers whose sole purpose is to pay you as little as possible. It’s a brutal, uphill battle, but you don’t have to fight it alone.

Hiring a public adjuster is the single most powerful move you can make to level that playing field.

The difference is simple but critical. The insurance company’s adjuster works for them—their loyalty is to the insurer’s profits. A public adjuster works exclusively for you, the policyholder. Their only mission is to fight for the maximum, fairest settlement you are entitled to under your policy.

Taking Command of Your Claim

A good public adjuster isn’t just an advisor; they are your expert advocate who takes command of the entire claims process. They become your shield against the insurer’s classic delay-and-deny tactics, managing the mountain of paperwork, the strict deadlines, and the tense negotiations. This frees you up to focus on what matters most: your family.

From day one, they get to work:

- They conduct a deep-dive policy review to uncover every penny of coverage you’re owed, especially the fine print in your coverage loss of use.

- They meticulously document every single expense, building an ironclad file of receipts and justifications that the insurer can’t argue with.

- They calculate the true, real-world value of your claim, making sure your Additional Living Expenses reflect your actual standard of living—not some cheap motel the insurer wants to stick you in.

- They handle all communication and lead the negotiations with the insurance company, using their industry expertise to crush unfair denials and lowball offers.

Hiring a public adjuster isn’t giving up; it’s arming yourself with the same professional firepower the insurance company is using against you. To see just how they can turn the tables, you can learn more about what a public adjuster does and how they champion the rights of policyholders.

A Success Story From the Trenches

The impact of a public adjuster isn’t just theoretical—it’s measured in tens of thousands of dollars. We saw this firsthand with a Wendell, NC homeowner whose house was devastated by major water damage. Their insurer, State Farm, threw a pathetic $5,000 at them for ALE, insisting it was enough for a brief stay in a budget motel.

The family was crushed and felt completely hopeless. That’s when they looked up online for a Public Adjuster Wendell, and hired us.

Our public adjuster immediately went to work. He built a detailed report proving the family’s pre-loss standard of living, found comparable local rental homes, and got a realistic repair timeline backed by contractor estimates. Armed with undeniable evidence, he proved State Farm’s offer wasn’t just low—it was a bad-faith tactic.

After a tough negotiation, the final settlement for their coverage loss of use was increased to over $40,000.

That wasn’t luck. It was expertise, strategy, and relentless advocacy. It’s proof that with the right ally in your corner, you can force the insurance company to honor the promise they made when they cashed your premium checks.

Frequently Asked Questions About Loss of Use Disputes

When you’re fighting for your loss of use coverage, you’re going to have questions. Here are straight answers to the most common roadblocks policyholders hit when their insurer starts playing hardball. Let’s get one thing straight: you have a right to a fair and just settlement.

How Long Can I Claim My Additional Living Expenses?

You can claim ALE for the shortest time required to either repair or replace your home, or for your family to permanently move somewhere else. But here’s the catch: insurers will almost always try to pressure you with an absurdly short timeline to save themselves money. They’ll invent a fantasy repair schedule that no contractor in the real world could ever meet.

A public adjuster calls their bluff. We get realistic repair schedules from trusted, local contractors and use that documentation to force the insurance company to cover you for the entire time you are actually out of your home—not just for the self-serving timeframe they made up.

What if My Insurer Says My Temporary Housing Is Too Expensive?

This is a classic move designed to slash their payout. Your policy says you are entitled to maintain your “normal standard of living,” a phrase they love to ignore. If you have a three-bedroom home with a yard for your kids and pets, you do not have to accept a cramped two-bedroom apartment an hour away from your life.

A public adjuster shuts this down immediately. We build a powerful, evidence-based case comparing your original home’s size, quality, location, and amenities to your temporary housing options. We use that evidence to compel the insurer to approve a truly comparable living situation, ensuring your family isn’t downgraded just to save them a few dollars.

Can I Fight a Loss of Use Denial Without Help?

You can try, but you’ll be at a massive disadvantage. Insurance companies have entire teams of adjusters, lawyers, and experts dedicated to underpaying and denying claims. They know the confusing policy language inside and out and use frustrating delay tactics designed to wear you down until you finally give up and accept a lowball offer.

A public adjuster is the expert who levels the playing field. We take over the entire fight, using our experience to anticipate and counter the insurer’s strategies. We consistently secure substantially higher settlements for policyholders than they can ever get on their own.

How can a Public Adjuster prevent the insurance company from prematurely terminating my ALE benefits?

Carriers often try to terminate ALE based on a short, initial repair estimate (e.g., 6 months). A Public Adjuster immediately challenges this by submitting an updated, expert Scope of Work that accounts for realistic repair timelines, permitting delays, contractor availability in a catastrophe area, and mandatory code upgrade time. We argue that benefits must continue until the home is truly "restored to a state of reasonable habitability."

Does my Loss of Use coverage have a hard dollar limit, a time limit, or both, and how do I verify this?

Most policies (HO-3) place a dollar limit on ALE, often calculated as a percentage (e.g., 20% to 30%) of your Dwelling Coverage (Coverage A). However, some policies also contain a time limit (e.g., 12 or 24 months). A Public Adjuster meticulously reviews your Declarations Page and Policy Form to ensure you utilize the most favorable limit—often the dollar amount limit—before any time restriction applies.

What essential expenses, often missed by policyholders, can a Public Adjuster ensure are included in the ALE claim?

Beyond rent and utilities, we ensure the inclusion of necessary and reasonable "hidden" costs: Increased mileage/gas for driving children to school or work, furniture rental for temporary housing, storage fees for contents, non-refundable pet boarding costs, utility setup/transfer fees, and temporary internet/cable setup charges at the rental location.

Can my ALE cover the cost of a temporary rental that is significantly more expensive than my pre-loss mortgage payment?

Yes. ALE is not tied to your mortgage payment; it is tied to your pre-loss standard of living. If your temporary housing requires a similar size, school district, amenities, and commute time, we argue that the increased cost is necessary and reasonable to maintain your lifestyle. A Public Adjuster presents market comps of comparable temporary rentals to justify the higher expense.

If my contractor delays the repair or rebuild of my home, can the insurance company legally stop my ALE benefits?

The carrier may argue that delays caused by the policyholder or contractor's negligence are not covered. We counter this by placing the blame squarely on systemic delays (permitting, supply chain, market conditions) and demanding documentation from the carrier proving the contractor's "unreasonable" negligence. A Public Adjuster ensures a formal paper trail is created to protect your ongoing right to benefits.

What non-covered expenses must I continue to pay out of pocket while claiming ALE?

You must continue to pay your baseline, normal expenses. This includes your mortgage payment, normal monthly costs for utilities at the damaged residence (if they were $150/month), and your normal grocery and personal item expenses (if they were $1,000/month). The ALE only covers the portion above these baseline costs.

How does a Public Adjuster handle the financial strain of paying ALE expenses upfront for months at a time?

We work to negotiate direct billing (where the insurer pays the rental company directly) or request a large upfront cash advance from the insurer specifically designated for ALE. This ensures you are not forced to deplete savings or rely on credit cards while waiting for slow expense reimbursements.

How is "Loss of Use" calculated for my rental or investment property that became uninhabitable?

For rental properties, the coverage is called Fair Rental Value (FRV) or Loss of Rents. A Public Adjuster calculates this by documenting the tenant's current lease and, if the property was vacant, using local market comparable properties to establish the monthly rental income you reasonably could have collected during the repair period.

In a total loss scenario, how long does ALE coverage last while I rebuild or purchase a replacement home?

For total losses, ALE typically extends for the necessary time required to rebuild or, if you purchase a replacement, the time required to settle on the new home. This period often extends well beyond 12 months, depending on permitting and construction realities. A Public Adjuster provides realistic timelines to the carrier, preventing a premature cut-off before you are settled.

Are the costs of moving, utility deposits, and security deposits for the temporary rental covered by ALE?

Moving costs and utility connection fees are typically covered as they are necessary and additional expenses resulting from the loss. However, security deposits are generally not covered because they are fully refundable and therefore not an expense unless they are forfeited by the temporary lease agreement.

If the insurance company denies a specific ALE expense (e.g., increased food costs), how does a PA dispute the rejection?

We dispute the rejection by submitting robust evidence and arguing the Reasonable and Necessary standard. For food costs, we provide receipts demonstrating the inability to prepare meals in temporary housing and compare the temporary restaurant bill directly against the pre-loss grocery average, forcing the insurer to justify why the expense was unreasonable given the circumstances.

Don’t let your insurance company dictate the terms of your recovery. The team at For The Public Adjusters, Inc. fights exclusively for homeowners and business owners in North Carolina and Virginia, making sure you get the full settlement you are owed.

Contact us for a no-cost claim review and let us handle the fight for you. https://forthepublicadjusters.com