You opened the letter expecting help. Instead, you got a denial, a partial payment that won't cover the work, or another request for documents you already sent. The kitchen still smells like water damage, the tarp is still on the roof, and the carrier's estimate reads like they inspected a different house.

That's the point where most homeowners start searching for an attorney for a home insurance claim. The question is fair, but it's often asked too late or framed the wrong way. In many disputed property claims, the smartest path isn't public adjuster or attorney. It's public adjuster first, attorney when the insurer forces legal escalation.

A strong claim dispute usually relies on effective tactics. First, somebody has to document the damage correctly, read the policy carefully, challenge bad scoping, and put a real number on the loss. If the carrier still delays, low-balls, misreads the policy, or refuses to negotiate fairly, then legal pressure changes the file in a different way. That's where an attorney steps in.

Table of Contents

- Your Claim Was Denied or Low-Balled Now What

- The True Role of an Attorney in a Home Insurance Dispute

- Red Flags That Signal You Need to Hire an Attorney

- Public Adjuster vs Attorney Understanding Your Allies

- The Typical Claim Dispute and Litigation Timeline

- Special Claim Dispute Rules in North Carolina and Virginia

- Your Next Steps and Frequently Asked Questions

Your Claim Was Denied or Low-Balled Now What

A lot of claim disputes start the same way. The insurance company sends a letter that sounds final. The tone is polished, the wording is technical, and the money offered doesn't line up with what your contractor says it takes to restore the property.

That doesn't mean the carrier is right.

In practice, I see homeowners make two costly mistakes at this stage. First, they assume the insurer's estimate is objective because it came from an adjuster. Second, they wait too long to challenge the scope, pricing, or coverage position because they're exhausted and hoping the company will “do the right thing” on the next call.

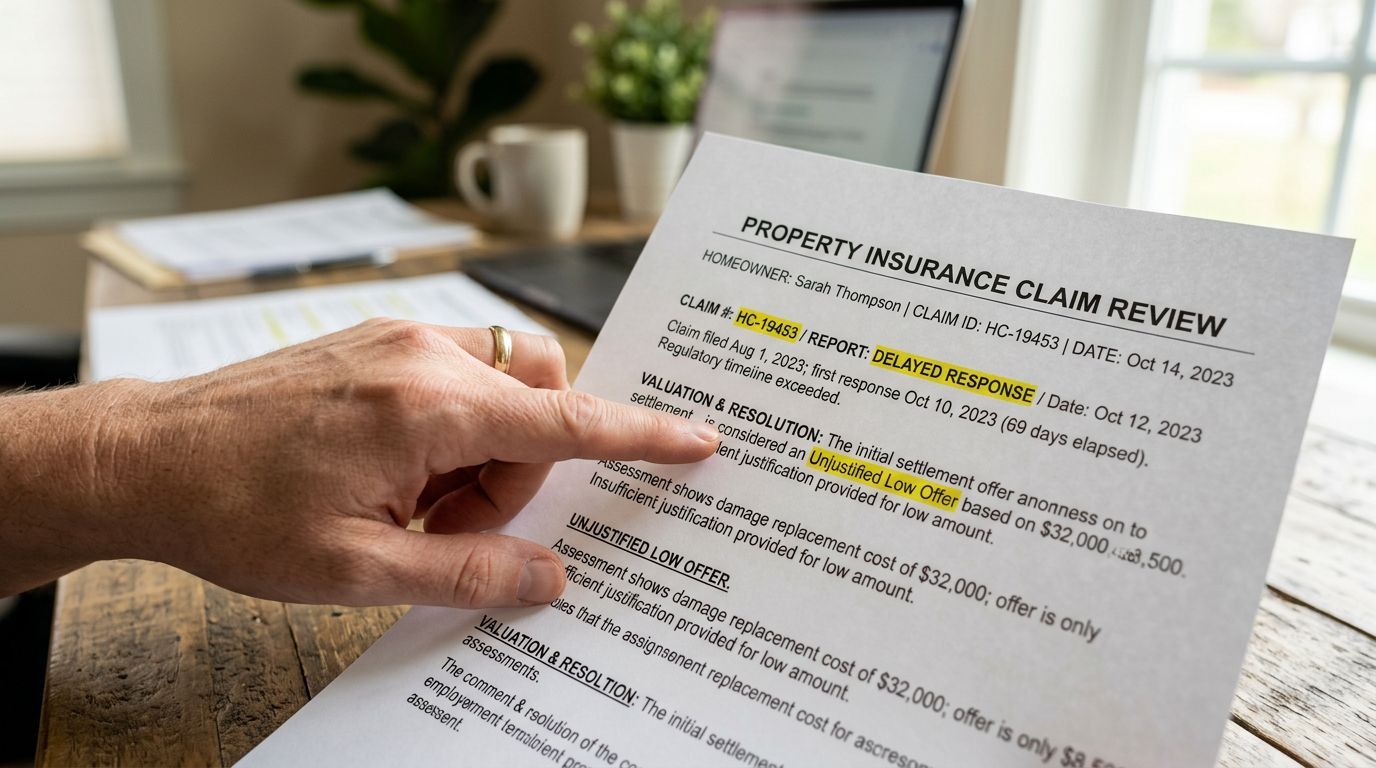

Sometimes the dispute is obvious. The carrier denies roof damage after a storm. Sometimes it's subtler. The claim gets approved, but key line items are missing, repairs are under-scoped, or the estimate prices work in a way no qualified local contractor would accept. The result is the same. You're left with a shortfall.

Practical rule: A denial letter or low settlement offer is the start of the dispute process, not the end of it.

At that point, homeowners need to think in terms of escalation strategy. A public adjuster can re-inspect, document, estimate, and negotiate the value of the loss. If the insurer keeps dragging its feet or takes a legally weak position, an attorney can evaluate the denial, the policy language, and whether the carrier's conduct has crossed into bad-faith territory.

If you're already staring at a denial or low-ball payment, it helps to understand the appeal path before you say the wrong thing or sign the wrong document. A practical starting point is this guide on how to appeal an insurance claim.

The True Role of an Attorney in a Home Insurance Dispute

Most homeowners think hiring an attorney means filing a lawsuit immediately. Sometimes litigation happens. Often, though, the first legal value is more disciplined than dramatic. A good attorney reviews the policy language, the claim file, the denial basis, the carrier's communications, and the evidence that supports coverage and damages.

What an attorney actually changes

One of the most technical jobs an attorney handles is preserving the proof-of-loss record. In property claims, that record matters because the insurer typically assigns an adjuster first to inspect damage and determine coverage. If the file is thin, disorganized, or incomplete, the carrier gets a head start on causation and scope arguments. That's why attorneys often push policyholders to preserve photos, video, repair estimates, and the relevant policy language so the file can support coverage arguments and damages valuation during review and negotiation, as discussed in Merlin Law Group's overview of a property insurance claim lawyer.

That work becomes even more important in larger or disputed claims. An attorney may help coordinate engineers, fire experts, meteorologists, industrial hygienists, contractors, public adjusters, or other specialists when the cause, extent, or pricing of damage is contested. That matters because the carrier's estimate isn't the only estimate that counts, and insurer pricing guidelines don't always match what it costs to perform proper repairs in the market.

Here's the simple version of what legal counsel can do when a file has gone sideways:

- Interpret policy language: Attorneys read the actual coverage grant, exclusions, conditions, and endorsement wording that drives the dispute.

- Challenge legal positions: If the denial is based on a strained reading of the policy, counsel can attack that position directly.

- Create pressure: A lawyer changes the tone of communication. Demand letters, formal notices, and litigation readiness usually get handled differently than ordinary claim emails.

- Pursue formal remedies: If the insurer's conduct justifies it, attorneys can move into breach-of-contract or bad-faith claims.

Where legal work overlaps with technical claim work

Legal strength still depends on factual strength. That's why the best disputed claims are built, not argued into existence. Photos need dates. Damaged materials need to be identified. Repair scopes need to match what the property needs. Communications should be saved in writing.

For firms that handle a high volume of incoming claim issues, even the intake process matters. Homeowners who are trying to preserve voicemails, inspection notes, and call summaries often benefit when claim teams use systems that automate claims intake so the timeline and communications don't get lost in the shuffle.

The attorney's leverage is strongest when the homeowner's file is already organized, supported, and hard to dismiss.

An attorney for a home insurance claim is not a replacement for damage documentation. Legal help is what you bring in when policy interpretation, carrier conduct, or litigation risk becomes part of the fight.

Red Flags That Signal You Need to Hire an Attorney

Not every underpaid claim needs a lawsuit. Some can still be corrected with better documentation, stronger estimating, and tougher negotiation. But some files start showing patterns that tell you the dispute has moved beyond ordinary adjustment.

The insurer behaviors that matter most

A major reason homeowners should pay attention early is that legal help doesn't just matter after a final denial. It can change the timeline, evidence burden, and negotiation strategy while the dispute is still developing. Merlin Law Group notes that attorneys review policy language, assess whether a denial was legally justified, and pursue bad-faith remedies, while common dispute triggers include delayed acknowledgment, inadequate investigation, biased experts, and excessive documentation requests in its discussion of when to involve an insurance attorney.

The strongest warning signs usually look like this:

- A weak denial explanation: The letter quotes policy language but doesn't connect it clearly to the actual damage.

- A carrier that keeps moving the target: Every time you submit what they asked for, they ask for something else.

- An investigation that feels one-sided: The insurer relies on a consultant or engineer whose conclusions ignore visible damage or obvious chronology.

- A serious underpayment dispute: The carrier pays something, but the scope is stripped down so aggressively that meaningful repair isn't possible.

- A communication freeze: Calls aren't returned, emails go unanswered, and no one will explain what's happening in plain language.

- Fraud insinuations or examination pressure: Once the carrier starts hinting at concealment, misrepresentation, or demanding unusually heavy documentation, legal risk rises quickly.

If the insurer is no longer adjusting the claim fairly and is instead building a defense file, you need to recognize that shift.

Why early legal review sometimes makes sense

A lot of consumer content frames lawyers as a post-denial option only. That's too narrow. Some homeowners should get legal review before accepting the first estimate, especially when the problem is underpayment rather than outright denial.

That's because accepting the carrier's framing of the loss can lock you into the wrong argument. If the estimate leaves out categories of damage, prices repairs unrealistically, or narrows the cause of loss too early, the dispute becomes harder to unwind later. An attorney can spot whether the issue is just a valuation fight or whether the insurer is positioning the claim for a more formal denial down the line.

Public adjusters are often the right first move when the main battle is scope and pricing. But once the insurer's conduct shows these red flags, delay becomes expensive. That's when legal counsel stops being optional and starts being protective.

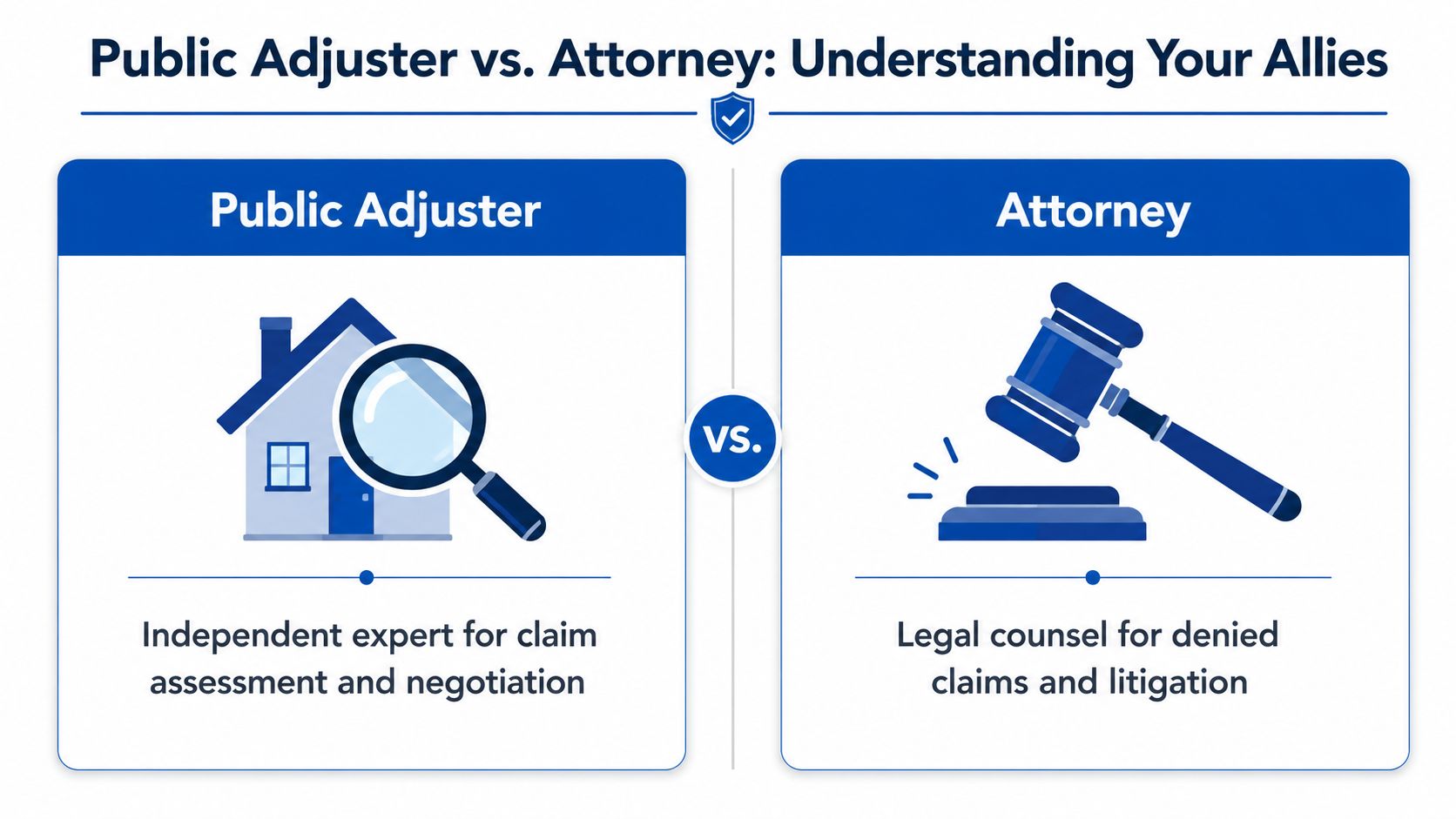

Public Adjuster vs Attorney Understanding Your Allies

Homeowners often ask which professional they need, as if they have to choose one side. In real claim disputes, that's usually the wrong question. A public adjuster and an attorney solve different problems.

They do different jobs

A public adjuster works the claim itself. That means inspecting damage, documenting the loss, preparing estimates, reviewing policy language from a claim-handling standpoint, and negotiating with the insurance company over scope and value. This is field-level advocacy. It's about getting the property damage understood and priced correctly.

An attorney works the legal dispute. That means analyzing whether the denial is justified, whether the policy was misapplied, whether the insurer's conduct supports legal claims, and whether a lawsuit, formal demand, or other legal pressure is necessary.

Those roles often complement each other. In many tough property claims, the cleanest sequence is this:

- Build the claim first. Get the scope, photos, estimate, and supporting documents in order.

- Negotiate from evidence. Push for correction while the claim is still adjustable.

- Escalate legally if needed. Bring in counsel when the insurer won't move, misapplies the policy, or shifts into defense mode.

A quick explainer on that escalation path is also covered in this discussion of homeowners insurance claim lawyers in North Carolina.

Here's the comparison at a glance.

Public Adjuster vs. Insurance Attorney Key Differences

| Factor | Public Adjuster | Attorney |

|---|---|---|

| Primary role | Evaluates, documents, and negotiates the property damage claim | Handles legal analysis, formal disputes, and litigation strategy |

| Main focus | Scope of loss, estimating, evidence presentation, negotiation | Coverage disputes, denial analysis, bad-faith issues, court process |

| Best time to call | When the insurer under-scopes, underprices, delays, or mishandles adjustment | When denial, severe delay, legal threats, or bad-faith conduct appears |

| Type of leverage | Stronger documentation and better claim valuation | Legal pressure, formal demand, lawsuit capability |

| Relationship to insurer | Negotiates within the claim process | Escalates beyond ordinary claim handling when necessary |

| Ideal use | Maximize and support the claim before it hardens into a legal dispute | Force legal accountability when ordinary negotiation fails |

The video below helps visualize why these roles shouldn't be treated as interchangeable.

One practical observation matters here. The claims that resolve best usually don't jump to litigation as the first move. They get built thoroughly first. When a public adjuster assembles a credible, documented, well-supported package, the insurer has to answer the actual damage. If the carrier still refuses to deal fairly, the attorney inherits a cleaner record and a stronger dispute posture.

A public adjuster helps prove the claim. An attorney helps enforce the rights attached to it.

The Typical Claim Dispute and Litigation Timeline

Many homeowners call a lawyer because they want the insurer to move faster. That's understandable, but litigation is rarely fast. Once a property claim leaves ordinary adjustment and enters legal escalation, the process becomes more structured and more demanding.

How the dispute usually unfolds

A typical path looks something like this:

- Pre-suit review: The attorney studies the policy, denial letters, estimates, photos, correspondence, and any expert reports already in the file.

- Demand and response: Counsel may send a formal demand or position letter and give the insurer a chance to reconsider.

- Suit gets filed: If the carrier doesn't correct course, the attorney files a complaint.

- Discovery begins: Both sides exchange documents, request records, and take testimony.

- Mediation or settlement talks: Many cases intensify here because each side has seen more of the evidence.

- Trial preparation: If no agreement is reached, the dispute moves toward court.

That sequence matters because every stage requires records, consistency, and patience. Casual statements made early in the claim can show up later in discovery. Missing photos and missing invoices can hurt. So can changing explanations about when the damage was first noticed or what temporary repairs were done.

Why homeowners get frustrated with the timeline

The hard truth is that legal escalation often takes many months and can continue much longer depending on the dispute. That's one reason strong claim preparation matters so much before a case hardens into litigation. If the issue can be corrected through better scoping, stronger valuation support, and disciplined negotiation, that's often more efficient than fighting every point in court.

A few practical expectations help:

- You'll need to stay organized: Save every email, estimate, invoice, photograph, and inspection note.

- You may need experts: Cause-of-loss disputes and pricing disputes often require technical support.

- Settlement can happen late: Carriers sometimes become more reasonable only after legal deadlines start carrying consequences.

Litigation is a pressure tool, not a magic reset button.

If you hire an attorney for a home insurance claim, do it with clear eyes. Legal pressure can be necessary and effective. It also demands a longer runway than most policyholders expect.

Special Claim Dispute Rules in North Carolina and Virginia

North Carolina and Virginia homeowners deal with the same core claim problems seen elsewhere. Delays, underpayments, and disputed storm losses. But there's a practical issue in these states that deserves more attention, especially in hurricane-exposed areas. Flood losses and mixed wind-water losses don't fit neatly inside the standard homeowners claim playbook.

Flood claims are not standard homeowners claims

That distinction matters because many articles lump all storm damage together. They shouldn't. Sullivan Galleshaw's discussion of bad-faith insurance issues highlights an important gap in consumer guidance. Flood-related losses, especially in NFIP-backed claims and mixed wind-water cases, often involve different coverage rules and documentation standards than ordinary homeowners claims.

That means a homeowner may be dealing with three separate tracks:

- A private homeowners policy claim

- A bad-faith or legal dispute over claim handling

- A federally backed flood claim with its own rules

Those are not interchangeable. The professionals who help on one track may not be solving the same problem on the other. If the loss includes flood, wind-driven rain, storm-created openings, surge, or rising water, the first question isn't just “Do I need an attorney?” It's “What type of claim do I have?”

For homeowners trying to sort that out, this guide on how to dispute a property insurance claim is a useful starting point.

Mixed wind and water losses need early claim framing

In North Carolina and Virginia, storm seasons often create mixed-cause disputes. Part of the damage may be argued as wind. Another part may be characterized as flood. How the file is framed early can affect how the loss gets classified and which rules apply.

That's why documentation needs to separate causes as clearly as possible. Exterior openings, roof damage, interior moisture paths, waterlines, debris patterns, timestamps on photos, and repair chronology all become more important when the carrier may split the loss into covered and excluded components.

This is one area where homeowners often wait too long for help because they assume “storm damage is storm damage.” It isn't. If flood is involved, or may be involved, the dispute can get technical fast. A public adjuster can help develop the damage presentation and claim framing. An attorney may be needed if the wrong coverage path is being forced or the claim handling turns adversarial.

Your Next Steps and Frequently Asked Questions

The most practical way to think about an attorney for a home insurance claim is this. Use a public adjuster to build, document, and negotiate the strongest possible property damage case first. Use an attorney when the insurer's conduct turns the claim dispute into a legal dispute.

A practical order of operations

Start with the file. Get the damage documented thoroughly. Compare the insurer's estimate to an independent scope. Preserve every communication. Don't assume a partial payment means the carrier got it right, and don't assume a denial is the final word.

If the claim is still in the negotiation stage, a public adjuster can often gain an advantage where the insurer expected compliance. If the carrier keeps delaying, misapplies the policy, relies on one-sided experts, or makes the dispute about legal defenses instead of damage, that's when counsel becomes necessary.

Homeowners also want to know whether the company they call will communicate and advocate. Positive client feedback tends to focus on responsiveness, clear explanations, and persistence during tough negotiations. Those aren't small things. In property claims, steady communication often determines whether a homeowner stays organized enough to fight effectively.

Frequently asked questions

How much does an insurance attorney cost?

It depends on the lawyer and the posture of the dispute. Some work on contingency, some don't, and some use mixed fee structures. Ask for the fee agreement in writing and make sure you understand costs related to experts, filing, and litigation support.

Can I hire a public adjuster and an attorney on the same claim?

Yes, in some disputes that combination makes sense. They do different work. One focuses on building and valuing the claim. The other handles legal rights and litigation pressure.

What if I already cashed the insurance check?

You may still have options, depending on what documents you signed and how the payment was issued. The key question is whether you released further rights. Have someone review the claim paperwork before assuming the matter is closed.

Should I call an attorney first for flood damage?

If flood is part of the loss, don't treat it like a standard homeowners claim. The first priority is identifying whether you're dealing with private coverage, federal flood coverage, or both.

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your insurer denied, delayed, or low-balled your property damage claim, For The Public Adjusters, Inc. helps homeowners and business owners in North Carolina and Virginia assess the damage, document the loss, and push back with a stronger claim file before legal escalation becomes necessary. When the dispute calls for it, that groundwork also puts an attorney in a much stronger position to act.