You open the front door after the hurricane and your stomach drops. Ceiling stains spread overnight. Shingles are gone. The living room floor is wet, and the carrier’s adjuster is already talking about “possible flood involvement” before anyone has traced where the water entered.

That is how many hurricane claims go sideways.

So, does homeowners insurance cover hurricane damage? Yes, for many wind-driven losses. No, for flood damage unless you carry separate flood coverage. And in North Carolina and Virginia, that gap is exactly where carriers push hardest. They know stressed homeowners miss deadlines, trust the first inspection, and accept vague denial letters that hide weak reasoning behind policy jargon.

Do not make that mistake.

If your payment is too low or your claim was denied, treat it as the start of a dispute, not the final word. A carrier adjuster works for the insurance company, not for you. Your job is to force the claim back onto facts: what damaged the property first, how the water entered, what the policy covers, and where the insurer is stretching exclusions past their limits. If you need a practical starting point, review these steps after hurricane property damage and insurance claim mistakes.

The pressure gets worse when the storm drops trees across the house or blocks access to the property. Before you pay for cleanup out of pocket, read this key information on tree removal policies. That expense is often mishandled too.

I have seen carriers slice one loss into pieces, label part of it “flood,” discount the repair scope, and then act like the file is settled. It is not settled if the facts support more coverage. It is a fight, and homeowners who document early, challenge bad causation calls, and bring in a public adjuster when needed put themselves in a far stronger position.

Table of Contents

- The Aftermath Is Just the Beginning of Your Fight

- Wind vs Flood The Coverage Trap Insurers Use to Deny Claims

- How Hurricane Deductibles Erase Your Settlement

- Dispute Your Denial Exposing The Concurring Causation Lie

- Build Your Case Documenting Damage to Defeat the Adjuster

- From Low-Balled to Rebuilt A Public Adjuster Success Story

- Do Not Accept a Denial Your Hurricane Claim Fight Is Winnable

The Aftermath Is Just the Beginning of Your Fight

You walk back into your house after the storm. The roof is torn up, insulation is hanging down, the living room smells like wet drywall, and water has reached places you have not even inspected yet. You call the claim in expecting help. What often comes back is a stripped-down estimate, a delay, or a denial dressed up in policy language.

I have seen this play out across North Carolina and Virginia for years. Carriers know homeowners are exhausted, displaced, and under pressure to clean up fast. That is when they push the same playbook. Keep the inspection narrow. Miss the full repair scope. Blame part of the loss on water, wear, or a lack of proof. Then wait and see if the homeowner gives up.

The first inspection is where a lot of claims get boxed in. One adjuster spends a short time on site, takes selective photos, and writes an estimate that leaves out the hard parts of the loss. Once that number is in the file, every later conversation starts from a low anchor.

Here is what that usually looks like:

- Roof damage gets chopped down to a patch: The estimate includes a few shingles and ignores underlayment, flashing, decking, ridge components, and the full path of water entry.

- Interior repairs are broken into pieces: The carrier pays for a ceiling stain and skips demolition, drying, insulation replacement, testing, texture match, and repainting continuous surfaces.

- Tree and debris damage gets narrowed fast: If a tree hit the structure or debris removal is being limited, review key information on tree removal policies before you sign off on a partial payment.

- Emergency work gets second-guessed: Tarps, board-up, water extraction, and mitigation invoices are questioned after the house was already exposed and you had no real choice but to act.

Treat the first estimate as the carrier’s opening position. Do not treat it as the truth.

Homeowners who are already getting stonewalled need more than claim filing tips. They need a dispute plan built around evidence, policy language, and scope. If that is where your claim stands, read this guide on hurricane insurance claim disputes.

The denial pattern is real. As noted earlier, post-storm claim denials have been high enough to make one point obvious. Carriers do not give hurricane losses the benefit of the doubt. They look for pressure points they can use against you.

So build your file from day one. Photograph every room, every elevation, every broken component, and every temporary repair. Save invoices, moisture logs, mitigation records, contractor notes, and text messages. Keep a written timeline of every call with the insurer, including dates, names, and what was promised.

That paper trail matters because the carrier is building a story about your loss too. If you do not document aggressively, their version becomes the claim file. And once that happens, reversing a denial or low-ball offer gets harder and more expensive.

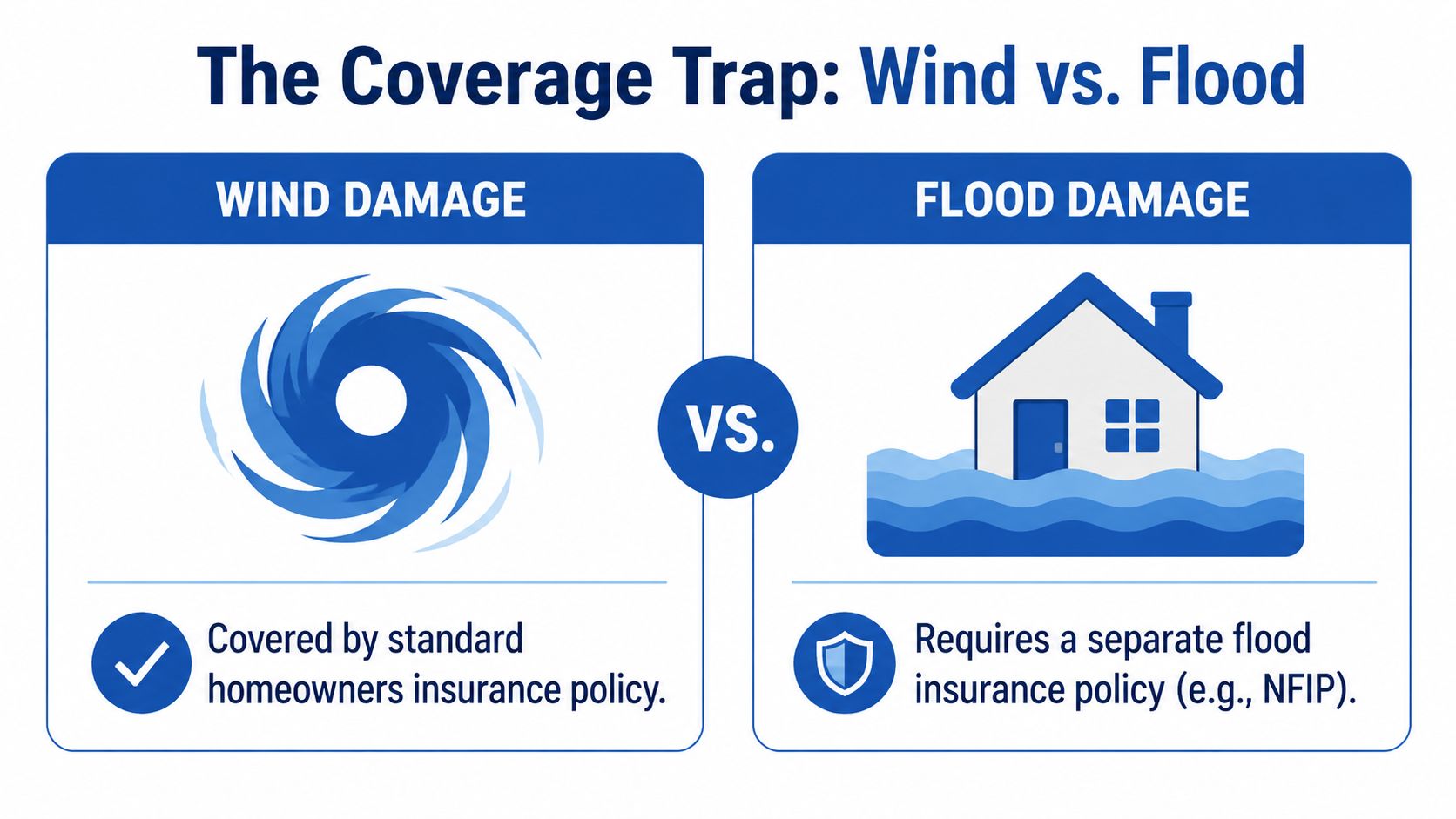

Wind vs Flood The Coverage Trap Insurers Use to Deny Claims

This is the trap that catches homeowners every hurricane season. They know the storm damaged their home, but they don’t yet know which part of the storm the insurer wants to pay for and which part it wants to exclude.

That distinction decides the claim.

The line insurers lean on

Standard homeowners policies typically cover wind damage and wind-driven debris. They do not cover flood damage. That’s the starting point.

The most important technical distinction is this. If hurricane winds damage the roof and rain enters afterward, the interior damage is covered under homeowners insurance. If water rises from external flooding or storm surge, that same water damage requires separate flood coverage, as explained in this breakdown of hurricane wind and flood coverage.

That sounds simple until the insurance company starts stretching the word “flood.”

Hurricane damage coverage comparison

| Type of Damage | Standard Homeowners Policy (Wind) | NFIP Flood Policy (Water) | Common Insurer Dispute Tactic |

|---|---|---|---|

| Wind tears shingles off roof | Usually covered | Not the policy that applies | Says damage was old or cosmetic |

| Broken window lets rain into home | Usually covered | Not the policy that applies | Says there was no storm-created opening |

| Tree or debris strikes structure during storm | Usually covered if caused by wind | Not the policy that applies | Limits scope to visible exterior only |

| Storm surge enters from outside and rises into home | Excluded | Typically addressed under flood coverage | Tries to push all water-related loss into flood category |

| Rising water from ground saturation or overflow | Excluded | Typically addressed under flood coverage | Uses exclusion broadly to deny mixed losses |

If your loss involves rising water, you’re in a separate world. That usually means the National Flood Insurance Program (NFIP) or a Write Your Own carrier handling a federal flood policy. Those claims are their own dispute process, and they’re often rigid, paperwork-heavy, and unforgiving.

If the carrier is calling your damage “flood,” read this guide on flood damage insurance claim disputes before you answer their position.

If water came in after wind opened the building envelope, don’t let the carrier lazily label the whole loss “flood.”

Why NFIP disputes become their own battle

Flood claims aren’t normal homeowners claims. The policy language is different. The adjuster may be working under NFIP rules even if the paperwork came through a private insurer’s brand. That distinction matters because homeowners often think they’re still arguing under their regular home policy when they’re not.

What I tell clients is straightforward:

- Separate the damage by cause: Don’t mix wind-created openings with rising-water loss in the same description.

- Use room-by-room proof: Show where the opening occurred and what damage followed from that path.

- Challenge broad labels early: “Water damage” is not specific enough. The source matters.

- Don’t assume the carrier categorized it correctly: They often choose the category that saves them money.

A hurricane claim can involve covered wind loss, excluded flood loss, and disputed overlap in the same house. That’s exactly why insurers use this trap so effectively. Confused homeowners accept the carrier’s version before anyone has proved the cause of each item of damage.

How Hurricane Deductibles Erase Your Settlement

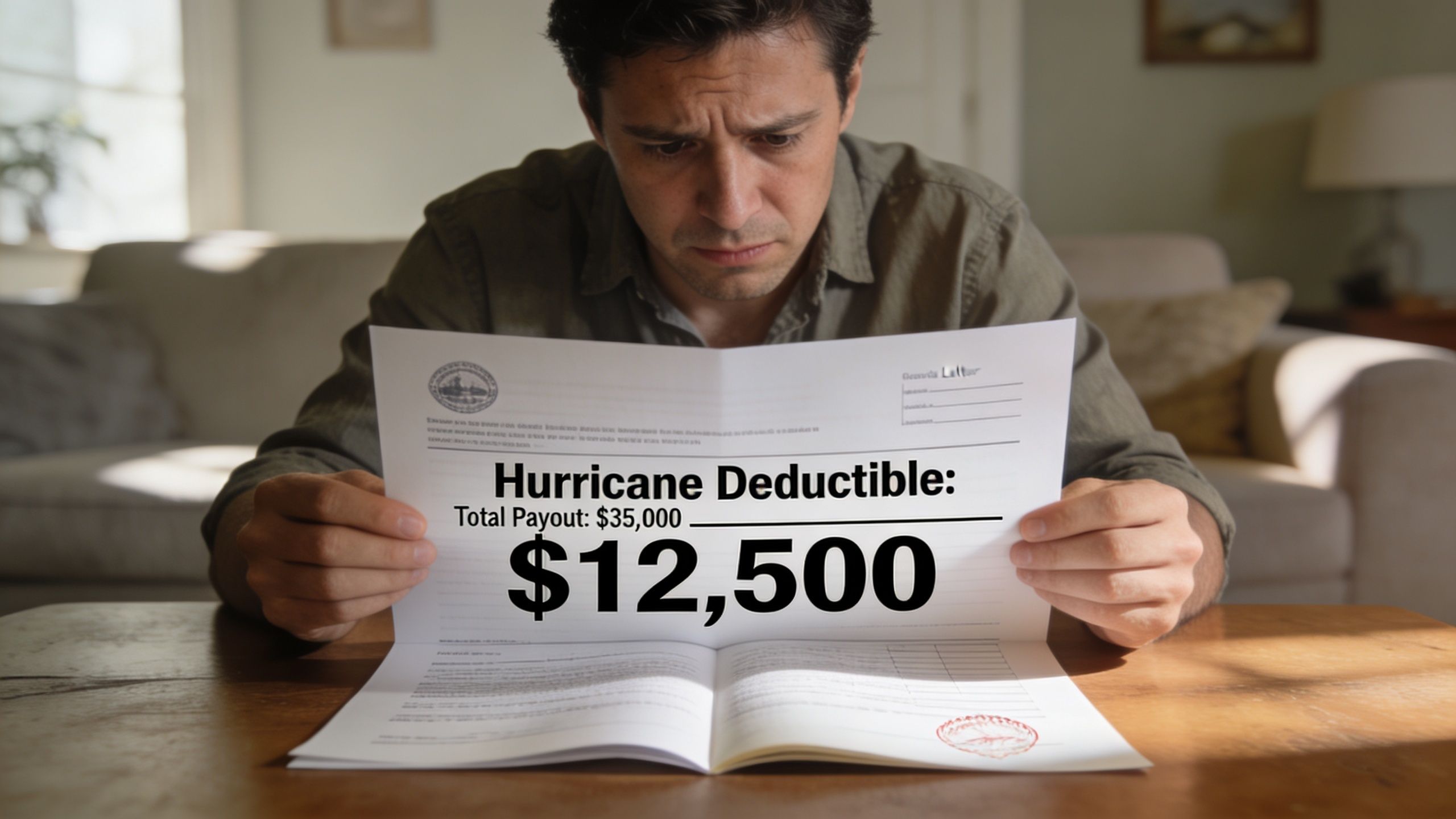

Many homeowners don’t get blindsided by coverage first. They get blindsided by the deductible.

They see a major storm, obvious damage, and a repair estimate that feels substantial. Then the carrier explains the hurricane deductible and the claim suddenly shrinks or disappears.

Why the deductible shocks people

A hurricane deductible usually isn’t a flat amount. It’s a percentage of your dwelling coverage. That’s why it hits so hard.

For example, a home insured at $250,000 with a 5% hurricane deductible leaves the homeowner paying the first $12,500 out of pocket, according to this explanation of hurricane deductibles. That same source notes a 39% denial rate for residential claims after Hurricane Milton, which tells you homeowners were dealing with both a steep deductible and aggressive claim resistance.

Another example makes the danger even clearer. Hurricane deductibles commonly range from 1% to 5% of dwelling coverage, and a homeowner with $400,000 in dwelling coverage and a 5% hurricane deductible would owe $20,000 before insurance pays anything, as described in this guide to how hurricane deductibles are triggered.

How low estimates help the carrier

The company adjuster’s estimate then becomes a weapon.

If your actual covered damage is significant but the carrier writes an artificially thin scope, they can keep the claim value near or below the deductible threshold. They don’t need to issue a dramatic denial. They can say the covered damage doesn’t exceed your deductible by much, or at all.

That’s a quiet underpayment strategy. It works because percentage deductibles give the carrier room to shave line items without appearing to deny the whole loss.

Watch for these patterns:

- Partial roof replacement logic: They pay for a patch when the damage pattern supports a broader repair scope.

- Interior repairs stripped down: Paint only, no tear-out, no texture match, no insulation, no flooring transitions.

- Detached structures overlooked: Other structures can be covered, but they’re often missed or undervalued.

- Contents under-scoped: Wet personal property gets minimized or omitted.

The math matters. A deductible doesn’t excuse a bad estimate. It just means the estimate has to be accurate before anyone can know what the insurer really owes.

A quick explainer can help if the policy language is giving you trouble:

Bottom line: If the carrier’s estimate lands suspiciously close to your hurricane deductible, challenge the scope before you accept the number.

Ask for the full estimate. Read every line. Compare it to what your contractor sees, not what the insurer prefers to count. If they left out code-driven work, hidden moisture damage, interior finishes, or attached structural components, the settlement figure is fiction.

Dispute Your Denial Exposing The Concurring Causation Lie

Some denials are blunt. Others are dressed up to sound elaborate. Concurrent causation is one of the carrier’s favorite ways to make a broad denial sound legitimate.

Here’s what it means in practice. Wind is covered. Flood is excluded. Both happened during the same storm. The insurer argues that because excluded flood contributed in some way, it can deny all or most of the claim.

That argument is often overused.

How the denial is framed

The denial letter usually won’t say, “We’re looking for a way out.” It will sound technical. The carrier points to mixed causes and claims the excluded peril controls. Homeowners read that and assume the issue is settled.

It isn’t.

According to this discussion of concurrent causation in hurricane claims, insurers often deny entire claims when flood contributes alongside wind, while public adjusters fight back by proving wind was the efficient proximate cause, a strategy that has overturned 30% to 50% of initial denials in post-hurricane disputes.

That matters because mixed-peril hurricane losses are common. A roof fails first. Rain pours in. Later, water rises outside. The carrier tries to sweep all interior damage into the flood exclusion. That’s not analysis. That’s a tactic.

How you attack that argument

The right counter is usually efficient proximate cause. In plain English, you identify the main initiating cause of the damage you’re claiming.

Take a common example. Wind breaks a window on the windward side of the house. Rain enters for hours and damages flooring, drywall, trim, and contents in that area. Later, floodwater enters another part of the structure. The insurer says flood was involved, so the interior claim is excluded.

That’s where a serious dispute file changes the outcome.

You need evidence that separates causes, such as:

- Exterior opening proof: Broken window, torn flashing, lifted roofing, punctured siding.

- Directional water pattern: Staining and saturation beginning near the storm-created opening.

- Timeline evidence: Photos, video, weather timing, and witness observations showing wind damage happened first.

- Room-specific analysis: One room may support covered wind-driven rain while another supports excluded rising water.

The carrier wants one bucket labeled “water.” You need two buckets. Covered wind-driven intrusion and excluded rising water.

A bad denial thrives on blur. A good dispute file creates separation.

This is also where homeowners get hurt by waiting. The longer damaged materials sit, the easier it becomes for the insurer to say no one can tell what happened first. If the company already denied your claim based on mixed causes, demand the basis for each item they excluded. Make them identify what they say was caused by flood, what they say was caused by wind, and what evidence they relied on.

If they can’t break it down cleanly, their denial is probably broader than the facts support.

Build Your Case Documenting Damage to Defeat the Adjuster

By the time the adjuster starts narrowing your loss, you need more than photos for the file. You need evidence arranged like a case presentation.

That means documenting cause, scope, and cost. Most homeowners only document scope. That’s not enough when the carrier is looking for ways to deny or discount.

Create proof of cause not just proof of damage

Don’t just photograph wet drywall. Photograph the path that explains why it became wet.

Use a sequence like this:

- Start outside. Photograph lifted shingles, missing ridge cap, bent flashing, broken windows, damaged doors, impact points, and debris direction.

- Move inward logically. If the roof was compromised above a bedroom, document the ceiling stain, insulation saturation, wall moisture, and damaged flooring in that same area.

- Repeat over time. Take photos on day one, during mitigation, and after demolition exposes hidden damage.

- Keep all emergency invoices. Tarps, board-up work, water extraction, and drying records all help prove the loss developed from a storm event.

- Log every conversation. Name, date, time, and what the adjuster said. Adjusters “forget” things that hurt the carrier’s position.

If you’re already dealing with a difficult company representative, this guide on dealing with an insurance adjuster after property damage can help you stay disciplined in every interaction.

Treat ALE like a separate dispute file

Additional Living Expenses (ALE) are underpaid all the time. Carriers know homeowners are exhausted, displaced, and spending money fast. That’s exactly when sloppy documentation costs you.

According to this discussion of hurricane insurance gaps and ALE limits, ALE is often capped at 20% of dwelling value or 12 months, and insurers underpay these claims by 35% on average, which is why every expense has to be documented carefully.

Build an ALE file with:

- Housing records: Lease, hotel folios, rental agreements, and payment confirmations.

- Meal receipts: Especially when your displaced living situation increased food costs.

- Laundry and commuting: If displacement created new routine expenses, track them.

- Utility overlap: Temporary housing can produce duplicate utility costs.

- Move-in and move-out costs: Storage, moving supplies, and related charges may matter.

Keep one folder for structural damage and a second folder for ALE. When homeowners mix them together, carriers use the confusion against them.

Also, don’t rush into the insurer’s preferred contractor network just because the adjuster suggests it. The carrier wants alignment. You need independence. Get your own contractor opinions, your own moisture findings, and your own repair scope before you sign any release or cash any final settlement without review.

From Low-Balled to Rebuilt A Public Adjuster Success Story

Two weeks after the storm, the homeowner had a check that would not cover the roof, the wet insulation, the ruined drywall, or the contractor’s real repair scope. The carrier called it a limited loss. The house said otherwise.

I have seen that play in both North Carolina and Virginia. The insurer writes a cramped estimate, labels obvious storm damage as old wear, ignores connected building components, and bets the homeowner is too tired, too displaced, or too cash-strapped to fight. That bet pays off for the carrier when nobody rebuilds the claim file.

One North Carolina claim turned because the homeowner stopped arguing in circles and started forcing proof. The original payment treated the loss like a simple patch job. The actual damage included roof failure, interior water intrusion, damaged finishes, and repair items the carrier left off completely. Once the file was rebuilt with independent photos, contractor input, moisture documentation, and a line-by-line challenge to exclusions, the insurer had to answer the missing scope instead of hiding behind a thin estimate.

That is what a public adjuster changes. The carrier’s adjuster protects the carrier’s money. A public adjuster documents the loss for the policyholder, ties the damage back to covered causes, and attacks weak denial language before it hardens into the insurer’s final position. In NC and VA, that often means tearing apart the company estimate and rebuilding it from zero.

One option homeowners use in these disputes is For The Public Adjusters, Inc., a licensed public adjusting firm that represents policyholders in assessing, documenting, and negotiating property damage claims.

What a real turnaround looks like

A real turnaround is not about getting the insurer to “be fair.” It is about making their shortcuts expensive to defend.

That usually means:

- Replacing the carrier’s estimate with a full repair scope that accounts for all affected materials and connected work.

- Matching damage to policy coverage so the insurer cannot wave it off with vague exclusion language.

- Attacking bad causation arguments when the company tries to blur wind, rain, and excluded water to cut payment.

- Building a negotiation file with photos, contractor estimates, invoices, moisture findings, and written rebuttals the carrier cannot easily dismiss.

Homeowners rebuilding after a hurricane should also make better construction choices while the walls are open and the roof is being replaced. If you are planning major repairs, review this guide on designing hurricane-proof residences before locking in final plans.

Actual client review for For The Public Adjusters Inc

| Review source | What stands out |

|---|---|

| Raleigh Google business review screenshot shown above | The review reflects what homeowners usually need after a hurricane claim goes sideways: clear explanation, accurate damage scoping, and pressure on the insurer when the first number is nowhere near enough. |

You do not need to know policy language like an adjuster. You need someone who does, and who does not work for the insurance company.

Do Not Accept a Denial Your Hurricane Claim Fight Is Winnable

So, does homeowners insurance cover hurricane damage?

Yes, for covered wind-related loss. No, for flood loss under a standard homeowners policy. And in practice, the bigger issue is this: insurance companies exploit that distinction, apply punishing hurricane deductibles, and use mixed-cause arguments to shrink or deny valid claims.

A denial letter is not the truth. It’s the carrier’s position.

A low estimate is not the value of your loss. It’s what the insurer hopes you’ll accept before you understand your rights.

If your roof was opened by wind, if rain entered through storm-created damage, if the adjuster ignored obvious scope, if ALE was cut down without explanation, or if the company lumped everything into “flood” to avoid paying, push back. Demand the estimate. Demand the policy basis. Demand itemized reasoning for every reduction and every denial.

A hurricane claim is won with evidence, pressure, and policy language. Not with trust.

You’re not asking for a favor. You paid for coverage. If the carrier is delaying, low-balling, or hiding behind technical language, treat that as the opening move it is. Then answer it with a stronger file, better documentation, and an advocate who works for you instead of the insurer.

If your hurricane claim was denied, delayed, or underpaid, For The Public Adjusters, Inc. can review the damage, the policy language, and the insurer’s estimate so you can understand what’s covered, what’s being missed, and how to challenge the carrier’s position.