When you file a homeowner's or business insurance claim, you’re not just documenting damage—you’re stepping into a high-stakes negotiation against a corporate giant. Your mindset has to be strategic from the get-go.

You have to understand the insurance adjuster's one and only goal: to minimize your payout for the benefit of their employer, whether it's State Farm, Allstate, or another major carrier. It’s not about making you whole; it’s about protecting their company’s bottom line. That means every conversation, every email, and every meeting needs to be handled professionally but with your guard up.

Success comes down to presenting undeniable proof of your loss and never, ever accepting their first offer as final. This is a fight, and you need to be prepared to dispute their findings.

The Hidden Conflict Behind Every Adjuster's Visit

When your home or business gets hit, the adjuster sent by your insurance company—whether it’s State Farm, Allstate, or another big carrier—will probably show up with a friendly face and a reassuring tone. They’ll present themselves as your partner, there to help you get back on your feet.

But you need to see through that from the very first handshake. There's a fundamental conflict of interest baked into their job.

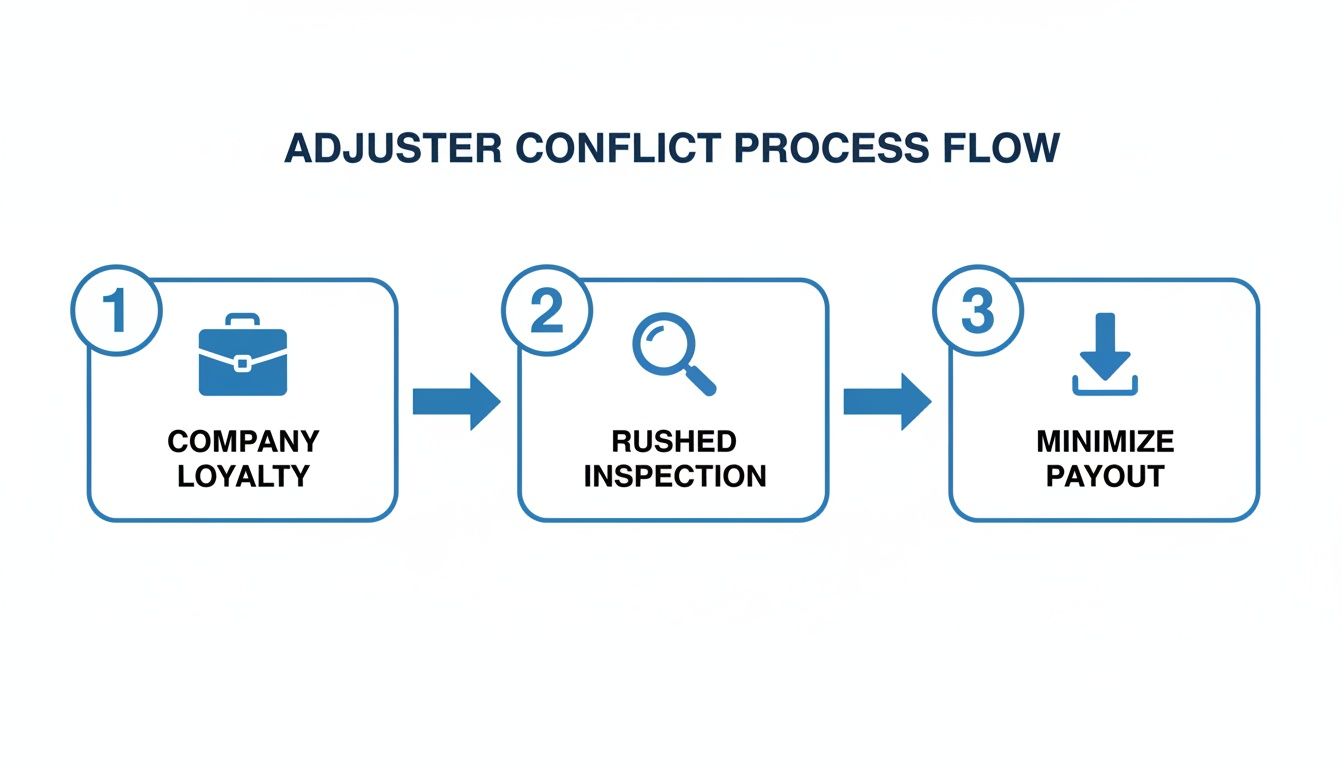

Their real loyalty isn't to you, the policyholder who's been faithfully paying premiums. It's to the insurance company's profits. These are trained professionals, and their performance is often measured by how quickly and cheaply they can close claims. This sets up an adversarial dynamic right away, even if it’s buried under a layer of polite conversation. These companies are notorious for lowballing and delaying claims, putting their financial interests far ahead of your recovery.

The Pressure Cooker Environment

Make no mistake, insurance is a massive business. The U.S. Claims Adjusting industry has ballooned into a $14.6 billion powerhouse, largely thanks to the explosion of catastrophe claims from hurricanes, floods, and wildfires. You can dig into the claims adjusting industry market research report to see just how big it's gotten.

Inside this high-pressure world, staff adjusters are completely overwhelmed. It’s not uncommon for them to be juggling 150 to 200 claims at once. This crushing workload forces them to sprint through inspections, spending as little time as possible at each property.

This is exactly where homeowners and business owners lose.

The adjuster’s rushed inspection means they miss the critical but less obvious damage. Things like hidden water damage seeping behind your drywall, subtle smoke contamination in the attic, or wind-lifted shingles that have secretly compromised your entire roof system. Their goal is simple: document the most glaring damage, plug it into their company’s pricing software, and move on to the next file in their stack.

Key Takeaway: An overworked adjuster is not your advocate. Their insane caseload practically guarantees a superficial inspection, leaving you on a path to a settlement that's 20-30% less than what you actually need to recover.

Who Is Really on Your Side?

The difference between the adjuster your insurer sends and a public adjuster you can hire isn't just a minor detail—it's the single most important factor that will determine your claim's outcome. One works to protect the insurance company’s profits. The other works exclusively to protect you.

It helps to think about it this way: would you ever show up in court and let the other side’s lawyer represent you? Of course not. An insurance claim is no different. The company adjuster is the opposition's representative, and their job is to limit their liability. Going in without your own expert puts you at a massive disadvantage from the very start.

This table cuts through the noise and shows you what’s really going on.

Who Is Really on Your Side?

| Role | Insurance Company Adjuster | Public Adjuster |

|---|---|---|

| Loyalty | The Insurance Company | You, the Policyholder |

| Goal | Minimize claim payout and close the file quickly | Maximize your settlement based on policy coverage |

| Assessment | Often a surface-level inspection under pressure | A detailed, forensic investigation of all damages |

Once you truly grasp this conflict, everything changes. It shifts your perspective from seeing the adjuster as a helper to seeing them for what they are: a negotiator for the opposing side. That’s the mindset you need to arm yourself with the caution and preparedness for every single phone call, email, and meeting that lies ahead.

Navigating Your First Meeting with the Adjuster

That first in-person meeting with the insurance adjuster is a make-or-break moment. This isn't some friendly walkthrough; it’s a critical inspection where every observation they make is calculated to justify the lowest possible payout for their employer. If you want to protect your financial recovery, you have to walk into this meeting with a game plan.

Before that adjuster ever rings your doorbell, your job is to create an overwhelming amount of evidence. This part is non-negotiable. Grab your smartphone and take hundreds—yes, hundreds—of photos and videos. Get wide shots of every damaged room, then get close-ups of the water stains creeping across the ceiling, the cracked drywall behind the sofa, the warped floorboards under the rug.

Open every cabinet. Pull back carpets. Get into the closets. Document everything. As you record video, narrate what you're seeing and how it was caused. This isn't just taking pictures; it's building the foundation of your entire claim.

Here’s your pre-meeting checklist:

- Your Policy: Have a complete copy of your insurance policy printed out and ready to go.

- Proof of Value: Gather any receipts, invoices, or appraisals you have for high-value items that were damaged—think appliances, custom cabinets, furniture, or expensive electronics.

- Your Questions: Write down a list of specific questions you need the adjuster to answer. Don't try to remember them in the heat of the moment. You'll want to ask about timelines, next steps, and exactly how they intend to value certain types of damage.

- Don't Touch Anything: Whatever you do, don't throw away damaged items or start making permanent repairs. That's called spoliation of evidence, and it can sink your claim before it even starts.

Guiding the Inspection Without Starting a Fight

When the adjuster arrives, you’re not a passive bystander—you’re the tour guide. You need to walk them through every single inch of the damage. Because you've done your homework, you can point out things they would absolutely miss in their rush to get to the next appointment.

Stick to the facts. Instead of saying, “The roof is leaking,” you guide their attention: “You can see right here where the wind-driven rain pushed under this flashing. That’s what caused this ceiling stain, which continues down the wall and damaged the baseboard.” You are directing their focus and demonstrating that you know exactly what happened. For more in-depth tactics on handling this conversation, our guide on how to negotiate with an insurance adjuster is a must-read.

Remember, the adjuster is operating on a simple, company-first playbook.

This process is built on a fundamental conflict of interest. Their job is to get from inspection to a minimal payout as fast as humanly possible.

What to Do the Second They Leave

Your work isn't done when the adjuster's car pulls away. The follow-up is just as important.

Right after they leave, send a follow-up email. Be polite but firm. This creates a written record of what was said and seen.

Key Takeaway: In that email, summarize the main points you discussed, list the specific damages you pointed out to them, and confirm the timeline they gave you for their official report and estimate. This paper trail is your best defense when—not if—a dispute comes up later.

And under no circumstances should you ever feel pressured to sign a release or accept a settlement on the spot. An adjuster pushing you for an immediate signature is a massive red flag. They know that a quick, lowball payment is a huge win for their side. Just tell them politely that you need time to review their official written report before making any decisions. That simple sentence protects your rights and buys you the time you need to make sure their offer is actually fair.

The "Delay, Deny, and Underpay" Playbook Exposed

Big insurance carriers like State Farm and Allstate didn't become corporate giants by writing big checks. They built their empires on a calculated, time-tested strategy designed to wear you down and protect their bottom line. It isn't some backroom conspiracy; it's just business. And in our world, it’s known as the "Delay, Deny, Underpay" playbook.

When you're reeling from a devastating property loss, understanding these tactics is your first line of defense. The insurance company is banking on your exhaustion, confusion, and financial desperation. They want to push you into accepting a fraction of what you're truly owed under your policy.

The 'Delay' Tactic

This is almost always the opening move. Insurance companies know that the longer they can drag out your claim, the more financial pressure you'll feel. Suddenly, the adjuster goes quiet. They might claim to have "lost" your paperwork or keep asking for the same documentation you’ve already sent three times.

It's a war of attrition. Every day they hold onto your money is another day it's earning interest for their shareholders, not for you. The bet is simple: you'll eventually get so frustrated and desperate for any money to start repairs that you’ll grab whatever unfair offer they throw at you just to make it stop.

The 'Deny' Tactic

Here, the adjuster becomes a master of misdirection. They will comb through your policy, searching for any obscure loophole or vague exclusion they can twist to their advantage and reject parts of your claim.

You'll hear all the classic excuses:

- The damage was caused by "pre-existing issues" or "poor maintenance."

- The specific cause of the loss isn't a "covered peril."

- Their interpretation of the policy language limits coverage for things like code upgrades or matching materials.

This tactic is designed to intimidate and overwhelm you. They wield complex insurance jargon like a weapon, hoping to make their decision sound final and unchallengeable. They count on you not having the energy or the expertise to fight back.

The 'Underpay' Tactic

This is the most common strategy of all: the lowball settlement. The adjuster's first estimate will almost always be miles below the actual cost of getting your life back together.

How do they get the numbers so low? For starters, they often rely on generic pricing software that has no clue about real-world labor and material costs in your specific town. Then, they conveniently "overlook" hidden damages—the smoke contamination that seeped into your attic from a kitchen fire, or the compromised underlayment beneath your wind-damaged roof. It's a systematic process.

This problem is only getting worse as the industry leans more on technology and less on thorough, boots-on-the-ground inspections. This tech-first shift means adjusters spend less time at your property, making it even easier to miss critical damage. For homeowners in North Carolina and Virginia who are constantly getting battered by storms, this trend is a serious threat. You can see more about these claims industry statistics on blog.talli.ai.

We saw this firsthand with a North Carolina family after a devastating house fire. Their insurance company's adjuster did a quick walkthrough and came back with a settlement offer of $50,000. The family knew instantly it wouldn't even cover the smoke and soot damage, let alone the structural repairs.

This is where a good public adjuster changes the entire game.

Feeling completely defeated, the family hired us. We conducted a forensic-level investigation, bringing in our own experts to test for hidden smoke damage. We documented the full scope of structural repairs needed and built a detailed, line-by-line estimate based on current, local costs.

Armed with irrefutable proof, we went back to the insurance company and exposed every single line item their adjuster had "missed." The result? The final settlement came in at $350,000—a staggering seven times their original insulting offer. This wasn't magic. It was simply leveling the playing field and forcing the insurer to pay what the policy promised. This case shows exactly why you need an expert fighting exclusively for your interests.

When to Hire a Public Adjuster in NC and VA

Dealing with an insurance adjuster can feel like you’re trapped in a slow-moving nightmare. If you’ve been stonewalled with unexplained delays, insulted with lowball offers, or hit with a wall of silence, you've reached a breaking point.

This is the moment when you realize you're in a fight you probably can't win on your own. And that's exactly what your insurance company is banking on.

It’s time to stop pleading and start preparing to fight back. Hiring a public adjuster isn’t admitting defeat; it’s a strategic move to bring a professional advocate to your side of the table. They work for you—and only you—to level a playing field that was designed from the start to be uneven.

Recognizing the Red Flags

So, how do you know when it’s time to call in the professionals? The signs are usually crystal clear and incredibly frustrating. If you're running into any of these issues, it’s a good sign you need help.

- The Lowball Offer: You get a settlement offer that doesn't come close to covering the estimates from your own trusted contractors.

- Unexplained Delays: The adjuster suddenly stops returning your calls and emails, leaving your claim stuck in limbo for weeks or months without a good reason.

- Complex Policy Jargon: You’re getting hit with obscure policy exclusions and confusing language to justify denying or underpaying parts of your claim.

- Pressure to Settle: You feel intense pressure to sign on the dotted line and accept a check just to get some money, even when you know it’s not nearly enough.

Make no mistake, these aren't just minor hiccups; they are calculated tactics. The insurance industry is a massive business, and recent trends show just how crucial it is to have an expert on your side. While the Claims Adjusting sector is on track to hit $10.8 billion in revenue, the number of adjusting businesses is shrinking, consolidating power with the large insurers.

With catastrophe-driven claims predicted to jump by 30% by 2030, company adjusters are more overwhelmed than ever, making it that much easier for them to underpay and move on. The data doesn't lie: public adjusters can boost recoveries by staggering amounts—in some cases by an average of 574% on disputed commercial claims. You can see more on the evolving claims adjusting industry on IBISWorld.com.

How a Public Adjuster Changes the Game

Hiring a public adjuster immediately shifts the power dynamic of your claim. They become your exclusive representative, taking over every single communication with the insurance company. This alone relieves you of the immense stress and frustration of trying to fight a corporate giant by yourself.

Most reputable firms, like ours, will start with a no-cost claim review. We’ll dig into your policy, inspect the damages with our own expert eyes, and tear apart the insurer’s estimate to pinpoint exactly where they went wrong. There is no upfront fee for this.

Public adjusters work on a contingency fee basis. That means we only get paid if we successfully increase your settlement. Our fee is a small, agreed-upon percentage of the additional money we recover for you. If we don’t get you more money, you don’t owe us a dime.

This structure guarantees our goals are perfectly aligned with yours: to get you every single dollar you are rightfully owed.

Furthermore, when you're dealing with complex fire or water damage, hiring a firm with IICRC (Institute of Inspection, Cleaning and Restoration Certification) credentials gives you a massive advantage. This specialized training means we understand the science behind the damage and can document the hidden issues that company adjusters almost always miss.

You can take a deeper dive into the role of a public claims adjuster on our blog to really understand the value we bring. For policyholders in North Carolina and Virginia, hiring a public adjuster isn’t just an option—it’s the most powerful tool you have to force your insurer to honor the promise they made when they cashed your premium checks.

Escalating a Dispute When the Adjuster Says No

So you’ve done everything right. You handed over overwhelming evidence, documented every single conversation, and laid out a clear, fact-based argument for why their settlement offer is just insulting. And the insurance adjuster still says no.

This is the moment so many homeowners and business owners throw in the towel. It's exactly what the insurance company is banking on. They assume their denial or lowball offer is the final word, but I’m here to tell you it absolutely is not. You have powerful rights and several strategic ways to fight back and demand the fair payment you're owed.

When you hit a brick wall with a difficult adjuster, it’s time to shift your mindset from negotiation to escalation. This means moving past the cycle of polite phone calls and emails and into formal processes that force the insurance company to take your dispute seriously.

Invoking the Appraisal Clause

Buried deep in the fine print of most homeowner and business owner policies is a powerful tool called the appraisal clause. This is your contractual right to resolve disputes over the amount of loss, and it’s one of the most effective ways to break a stalemate without jumping straight into a lawsuit.

Here’s the rundown on how it typically works:

- You hire your own appraiser. This is an independent, impartial expert who assesses the damage and calculates the true cost of repairs.

- The insurance company hires their appraiser. They’ll pick their own expert to do the same thing.

- The two appraisers negotiate. They review all the evidence and try to come to an agreement on a fair settlement amount.

- An umpire steps in if needed. If the two appraisers can’t agree, they will jointly select a neutral third party, known as an umpire, to make a binding decision.

Invoking appraisal takes the decision out of the adjuster's hands and gives it to impartial experts. It’s a formal process that forces the insurer to defend its cheap estimate against a qualified professional who isn't on their payroll.

Filing a Formal Complaint

If the problem goes beyond just the dollar amount and involves shady behavior—like endless delays, ignoring your calls, or misrepresenting your policy—it’s time to get the state involved. Both North Carolina and Virginia have a Department of Insurance (DOI) that regulates insurance companies and protects consumers.

Filing a complaint is free and puts your insurer on official notice. Once the DOI opens an investigation, the insurance company is legally required to respond and justify its actions. Believe me, this external pressure is often all it takes to make a stubborn adjuster suddenly become much more reasonable.

Key Takeaway: A complaint to the Department of Insurance creates an official paper trail of the insurer's conduct. Even if it doesn't solve your claim overnight, it adds a serious layer of accountability and can be critical evidence if you end up having to pursue legal action.

The Last Resort: Litigation and Bad Faith

When all other avenues fail, a lawsuit may be your only remaining option. It’s a big step, but sometimes it’s the only way to hold an insurance company accountable for the promises they made in your policy.

In some cases, an insurer's conduct is so outrageous that it crosses the line into what the law calls bad faith. This isn't just about disagreeing on the value of a claim; it’s about an insurer completely failing to uphold its basic duties of fair dealing.

Courts have sided with policyholders in these situations time and time again. For instance, in State Farm Lloyds v. Nicolau, a Texas jury found that State Farm had knowingly engaged in unfair and deceptive practices related to a foundation damage claim. The court awarded the homeowners not only the full repair costs but also significant damages for mental anguish and bad faith, sending a clear message to the insurer. While every case is unique, these legal precedents prove you have powerful rights, and the courts can and will force an insurer to pay for breaking its promise.

You can find more details on what steps to take in our complete guide on how to dispute an insurance claim.

Frequently Asked Questions About Insurance Claims

After your property gets hit, the last thing you want is more confusion. But when you're dealing with an insurance adjuster whose job is to pay out as little as possible, questions are going to come up fast.

Here are some of the most common ones we hear from homeowners and business owners—and the straight answers you need.

Should I Accept the First Settlement Offer from My Adjuster?

Let’s make this simple: almost never.

That first number isn't a final offer; it's the opening shot in a negotiation. Major carriers like State Farm or Allstate have this down to a science. Their initial offer is a carefully calculated lowball, the absolute minimum they think you might be desperate enough to accept just to make the nightmare end.

It’s a tactic. They’re banking on your exhaustion and your urgent need for cash to start repairs. They want you to take the quick, low payment and disappear. Don't fall for it. Always take a deep breath, review their offer line by line, and get your own estimates from trusted contractors. Be ready to push back.

Can I Reopen a Claim After I Have Cashed the Check?

This is a critical point, and it all comes down to what you signed.

If the insurance adjuster pushed you to sign a “full and final release of all claims” to get that check, you’ve probably signed away your right to any more money for that loss. This is exactly why you should never sign release forms on the spot.

But if you just cashed an initial check for what the insurer calls the "undisputed" portion of the damage and didn't sign a final release, the door is still open. You absolutely can—and should—file a supplemental claim for damages you discover later or for things the adjuster conveniently missed the first time around.

What Is Considered Insurance Bad Faith?

"Bad faith" isn't just a disagreement over the cost of a new roof. It’s a legal term for when an insurance company deliberately fails to hold up its end of the bargain—your policy. They are actively trying to duck their clear responsibilities.

Common examples of bad faith include:

- Intentionally twisting your policy language to deny a valid claim.

- Dragging their feet and refusing to conduct a prompt, thorough investigation.

- Using deceptive or coercive tactics to bully you into a lowball settlement.

- Failing to give you a reasonable, written explanation for a denial.

If you even suspect your insurer is acting in bad faith, documentation becomes your best friend. Log every call, save every email, and send all important communication in writing. That paper trail is the evidence you'll need.

For policyholders, having a solid grasp of insurance, including understanding your insurance coverage and costs, is the first step in knowing when you're being wronged. But proving bad faith is tough, which is why getting professional advice from a public adjuster is crucial if you think your insurer is breaking the rules. They know how to build a case and force the company to play fair.

When you're fighting a difficult insurance adjuster, you don't have to go it alone. The team at For The Public Adjusters, Inc. provides no-cost claim reviews to help homeowners and businesses in North Carolina and Virginia understand their rights and secure the full settlement they are owed. Contact us today to level the playing field. https://forthepublicadjusters.com