When the immediate chaos of a burst pipe finally subsides, a different kind of battle often begins—the one with your insurance company. The shock of the water damage is one thing, but dealing with an insurance company that seems determined to underpay your claim can feel like a second disaster.

Let's be blunt: when you file a pipe burst water damage claim, your insurer's primary goal isn't necessarily to make you whole again. Their business model is built on minimizing payouts to protect their bottom line. It's a harsh reality that can turn a deeply stressful event into a prolonged fight for the compensation you deserve.

The Insurance Fight After a Pipe Burst

The moment you report the damage, your insurance company—whether it's a giant like Allstate or State Farm—assigns an adjuster to your case. It's absolutely critical to remember who this person works for. They are on the insurance company's payroll, not yours.

Their job is to assess the damage through the lens of limiting the company's financial liability. This creates an immediate conflict of interest that sits at the very heart of why so many homeowners find the claims process so difficult. The adjuster's initial assessment is almost never a comprehensive, good-faith effort to catalog every bit of damage. Think of it as a strategic opening move in a negotiation, designed to undervalue your claim from the get-go.

Common Tactics Used to Undervalue Your Claim

Insurance companies have a well-worn playbook for minimizing what they pay out. These tactics are designed to exhaust you, creating financial and emotional pressure that might push you to accept a low-ball offer that won't come close to covering the actual cost of repairs.

You can expect to run into a few common strategies:

- Intentional Delays: They might drag the process out for weeks, or even months. The longer you wait, the more likely you are to feel desperate enough to take any settlement offered, just to get the process over with. This is a common tactic used by large insurers who know that a homeowner's financial resources are limited.

- Confusing Policy Language: Adjusters often lean on complex jargon and point to obscure policy exclusions to deny portions of your claim. This is a tactic meant to make you feel powerless and confused, as if you have no choice but to accept their interpretation.

- Low-Ball Estimates: The estimate you receive will likely be far too low. It often conveniently overlooks hidden water damage, fails to account for the cost of matching existing materials (like flooring or cabinetry), and relies on outdated pricing for labor and supplies.

"A recent Arkansas court case revealed how State Farm argues for claim denials based on fine-print exclusions—like slow leaks, corrosion, or water seeping through a foundation—that are never mentioned in their consumer-friendly advertising. This shows a stark contrast between their 'good neighbor' marketing and their aggressive courtroom tactics."

Their first offer is just that—an offer. It's not a final, take-it-or-leave-it number. It’s the starting point for a negotiation you might not have realized you were entering. You have every right to dispute their assessment and fight for what your policy actually entitles you to. The key is to see their strategy for what it is and be prepared to counter it.

When you find a burst pipe, the scene is pure chaos. But the steps you take in those first few hours will absolutely define the outcome of your insurance claim dispute. You're fighting a battle on two fronts: stopping the damage from getting worse while simultaneously building a rock-solid case for your claim.

This isn't just about mopping up water. It's about creating irrefutable proof of the pipe burst water damage before a single thing is moved or thrown away. The evidence you gather right now is the most powerful tool you'll have in your fight against a low-ball offer.

Document the Scene Before You Touch Anything

The insurance adjuster won't be there to see water cascading through your ceiling or pooling across your new floors. They only see the aftermath, which never tells the whole story. Your job is to paint them a vivid picture of the disaster at its peak.

- Start with a video walkthrough. As soon as it's safe, hit record on your phone. Move through every affected area, describing what you're seeing out loud. Capture the sound of the leak, pan across the submerged furniture, and show how high the water has climbed. This raw footage is incredibly compelling evidence.

- Then, switch to photos—and take a ton of them. After the video, get detailed snapshots. I’m talking about close-ups of the warped baseboards, the drenched drywall, the ruined rug, and the electronics sitting in water. If you can safely see the source of the burst pipe, get multiple pictures of it from different angles.

- Show the high-water mark. This is a pro tip: Grab a tape measure or a ruler and hold it up against the wall, a sofa leg, or a kitchen cabinet to show exactly how deep the water was. These lines on the wall are hard evidence that can be difficult for an insurer to argue against later.

To really get a handle on this, the Melbourne Homeowners Emergency Guide for burst water pipes offers a great rundown of similar immediate actions that can significantly strengthen your claim from the get-go.

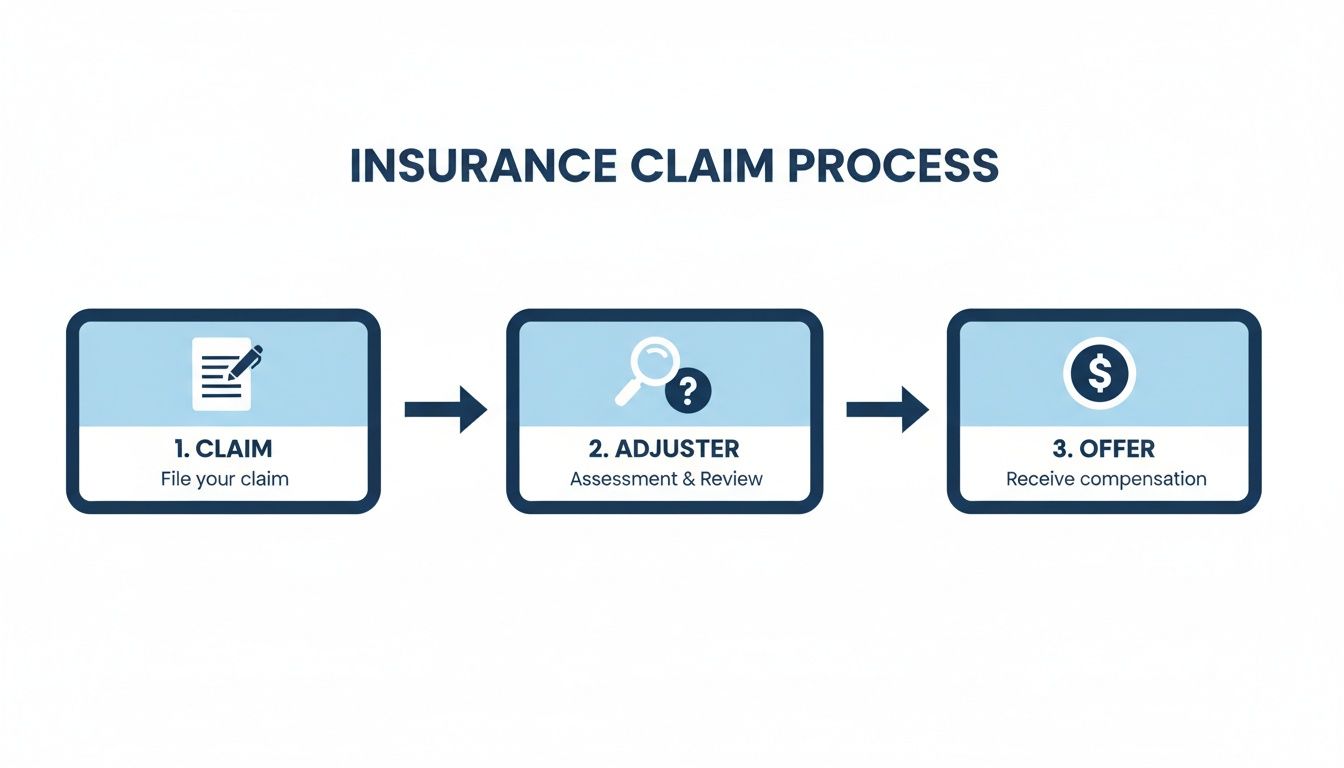

Insurance companies often present the claims process as a simple three-step affair, which can be dangerously misleading.

While it looks easy on paper, the "Adjuster Review" and "Receive Compensation" stages are precisely where your claim can be chipped away. This is where they find reasons to pay you less than you deserve, turning a straightforward process into a fight.

Your Initial Evidence Documentation Checklist

Use this checklist to capture critical photo and video evidence immediately after a pipe burst. This builds a powerful foundation for your claim dispute.

| Item to Document | Why It's Critical For Your Claim Dispute |

|---|---|

| Wide-angle video tour of all affected rooms | Captures the full scope of the disaster and proves the initial chaos and water volume. |

| The source of the leak (the burst pipe itself) | Establishes the cause of loss as a "sudden and accidental" event, which is key for coverage. |

| High-water marks on walls and furniture (with a ruler) | Provides undeniable proof of the flood's depth, preventing the insurer from downplaying its severity. |

| Damaged personal belongings (electronics, furniture, clothes) | Creates an inventory of what was destroyed before it gets moved or discarded during cleanup. |

| Damage to structural elements (drywall, flooring, ceilings) | Shows the immediate impact on the home's structure, justifying costs for tear-out and replacement. |

| Photos of room layouts before moving items | Proves where expensive items were located and how they were impacted by the water flow. |

Having this visual evidence organized and ready makes it much harder for an adjuster to question the extent of your losses.

Stop the Bleeding and Make the Official Call

Once you have that initial evidence locked down, you have to pivot to damage control. Your policy requires you to take reasonable steps to prevent the problem from getting worse.

First, shut off the main water valve to your house—no exceptions. Then, your next call should be to a professional water mitigation company. Getting experts on-site to start extracting water is crucial. If you're not sure where to start, you can learn how to find a reliable water damage restoration service in our guide.

Finally, it's time to notify your insurance carrier. When you call, just stick to the facts: "I've had a pipe burst, and my home has significant water damage." Don't guess about the cause, don't downplay anything, and absolutely do not agree to give a recorded statement right away. You need time to think clearly. At this stage, your only job is to get the claim number and put them on notice that a loss has occurred.

Don't Fall for the Insurance Company's First Offer

When the insurance adjuster finally shows up after a pipe burst, it's easy to feel a sense of relief. They seem professional, they inspect the damage, and they hand you a detailed repair estimate. But here's the hard truth from someone who sees this every day: that first estimate is almost never a fair offer.

Think of it as their opening bid in a negotiation. It’s a carefully crafted number designed to minimize their payout and pressure you into settling for far less than you need to truly recover.

How They Undervalue Your Claim

Insurance companies rely on complex software to create these estimates, but the output is only as accurate as the information someone puts into it. The company adjuster, who works for the insurer, not you, has a knack for leaving out crucial details.

Here are a few of the most common tricks of the trade:

- Overlooking Hidden Water: They'll write up the obvious damage you can see, but what about the water that seeped behind your drywall or soaked the insulation under the floor? That hidden moisture is a ticking time bomb for mold and rot, and they often "forget" to look for it.

- Creating Patchwork Repairs: They might budget to replace just the three kitchen cabinets that got wet, ignoring the fact that you can't buy a perfect match for your 10-year-old cabinetry. A proper repair means making the whole room look seamless again, not just patching the damage.

- Using Out-of-Date Pricing: The cost databases they use are frequently loaded with bulk-rate, low-ball prices for labor and materials that don't reflect what a real, local contractor would charge for a quality job.

This isn't just an occasional problem; it's how the game is often played. With aging pipes failing more often—the American Society of Civil Engineers reports over 6 billion gallons of water lost daily from bad systems—the risk of damage is high. That's a big reason why the average water damage claim hits $11,605, a figure insurers are always trying to push down.

Why Our Estimate Is Different

This is exactly where a public adjuster levels the playing field. We work for you and only you. We bring in our own tools, like thermal imaging cameras and moisture meters, to uncover every last bit of damage, especially the hidden stuff.

Our estimate isn't based on a generic database. It's built from the ground up, reflecting the actual, local costs to restore your home to the condition it was in moments before that pipe let go. We factor in everything the insurance company conveniently ignores—from the cost of specialized drying equipment to the price of hiring a craftsman who can perfectly match your custom trim. We've seen all the tactics, and we know how to counter them when dealing with an insurance adjuster.

Your insurer’s estimate is a starting point for a negotiation you didn’t ask for. A public adjuster’s estimate is a comprehensive demand for what you are rightfully owed under your policy.

When we submit our detailed scope of work, the power dynamic shifts. We're not just asking for more money; we're presenting undeniable proof. This forces them to defend their low-ball numbers against our expert-backed report, making it incredibly difficult for them to get away with underpaying your claim.

How A Public Adjuster Turned A $20k Offer Into $100k

It’s easy to talk about insurance company tactics in theory, but seeing them play out in real life is something else entirely. A recent case with a homeowner in Apex, NC, perfectly captures the massive gap between an insurer’s first offer and what a family truly needs to recover from a burst pipe.

After a pipe burst and flooded their home, their insurance company sent out its own adjuster. After a quick look around, the adjuster handed the family a check for $20,000, telling them it was more than enough to cover the repairs. But as they stood in their water-damaged home, they knew that number wasn't just low—it was impossible. It wouldn’t even scratch the surface.

Feeling completely overwhelmed and disrespected, they decided to call us at For The Public Adjusters, Inc. for a second opinion. That’s when everything changed.

The Power of an Independent Investigation

The first thing we did was launch our own investigation, and I mean a real investigation. We weren’t just looking at the obvious damage like stained carpets and buckled floors. We brought in specialized equipment, including thermal imaging cameras and moisture meters, to uncover what the insurance company’s adjuster either missed or chose to ignore.

What we found was staggering.

- Hidden Moisture: Our thermal scans lit up with signs of extensive water saturation trapped behind the walls and deep within the subflooring. This was a critical find because leaving that moisture untreated is a guaranteed path to widespread mold and structural rot.

- Detailed Scope of Loss: We then built a line-by-line scope of work that accounted for everything. This included professional mold remediation, replacing entire sections of drywall, and the cost to match their unique custom cabinetry—a detail the insurer's estimate conveniently left out.

Armed with this mountain of indisputable proof, we went back to the insurance company. Suddenly, their $20,000 offer didn't look so solid. Faced with our detailed documentation and expert reports, they had no choice but to come back to the table. In the end, we secured a final settlement for that family of over $100,000.

This isn't just a success story; it's a cautionary tale. Without an advocate on their side, this family would have been stuck with a payout that was 80% less than what they rightfully deserved. That’s the real-world difference a public adjuster can make.

Understanding the Insurance Company's Playbook on Water Damage Claims

Your homeowner's insurance policy isn't exactly light reading. It's a dense legal contract, written by the insurance company's lawyers to protect their bottom line. When it comes to something as destructive as pipe burst water damage, their first move is often to find a way to limit what they have to pay.

When you file that claim, the insurance adjuster assigned to your case will immediately start looking for reasons to reduce or deny it. They know your policy inside and out—and they're experts at using its confusing language to their advantage.

The "Sudden and Accidental" Loophole

You'll hear the phrase "sudden and accidental" a lot. This is the key that unlocks coverage. A pipe freezing solid and then bursting is a perfect example of a "sudden and accidental" event, and it should be covered.

But here’s the twist insurers often use. They'll try to reframe the event as "gradual" damage. They might suggest a tiny, slow leak was happening for weeks, causing wear and tear, and that your lack of maintenance is the real culprit. Since gradual damage is almost always excluded from policies, this one word change can be enough for them to deny the entire claim.

This isn't just a rare trick; it's a common strategy. The money involved is huge. In the UK, just one insurer paid out £20 million for only 345 frozen pipe claims, with one catastrophic incident costing £566,000. You can see why they fight so hard when you explore more about these significant pipe burst payouts.

Using Mold Exclusions Against You

Another favorite tool in the adjuster's arsenal is the mold exclusion. Almost every homeowner's policy has one, and it either strictly limits or completely denies coverage for any mold-related issues. The problem is, mold can start growing within 24 to 48 hours after a pipe lets loose.

Here's how it plays out: The adjuster might agree to pay for the initial water removal but then draw a line in the sand when it comes to mold. They’ll point to that exclusion clause and treat the mold as a separate, non-covered event.

This is a classic case of misdirection. The mold wouldn't exist without the covered water damage in the first place—it’s a direct result of the initial incident. To win this fight, you have to prove that the burst pipe was the sole cause of the mold. It's a tough battle to win on your own, and many homeowners end up paying for expensive remediation themselves just to make their homes safe again.

When You Need A Public Adjuster To Fight For You

It’s a terrible feeling to realize the insurance company you’ve dutifully paid for years isn't really on your side. After a pipe bursts and floods your home, you expect a helping hand, not an uphill battle. Knowing when to call in professional backup is often the single most important decision you can make to protect your financial recovery.

If you're already getting the runaround with delays, ridiculously low settlement offers, or a flat-out denial of your claim, it's time to act. These aren't just minor frustrations; they are often deliberate strategies used by insurance carriers to wear you down and get you to accept far less than you deserve.

Red Flags That Signal You Need Help

I've seen it countless times—homeowners getting overwhelmed by the process. Recognizing the warning signs early can save you thousands of dollars and an incredible amount of stress.

Here are the classic signals that your insurer isn't playing fair:

- Delay Tactics: Suddenly, your adjuster is impossible to reach. Calls go to voicemail, emails go unanswered, and weeks pass with no real progress. This isn't just poor customer service; it's a strategy to make you more desperate and likely to accept a low offer.

- Pressure to Sign: You're being rushed to sign documents or accept a settlement "on the spot." Never, ever sign anything under pressure. This is a huge red flag.

- An Unrealistic Offer: The settlement offer comes in, and it wouldn't even cover half of the estimates you're getting from reputable contractors. This is the definition of a low-ball offer.

- Outright Denial: Your claim gets denied for a confusing reason, often citing policy exclusions like "gradual damage" or blaming a pre-existing issue you had no idea even existed.

This isn't just a one-off problem. It's tied to a massive infrastructure crisis. A 2023 study revealed that aging pipes in the U.S. and Canada cause an estimated 260,000 water main breaks every year. You can read more about the staggering scale of water main breaks to understand why insurers are so prepared to minimize these costly claims.

The Critical Difference An Advocate Makes

Let’s be perfectly clear: the adjuster sent by your insurance company works for them. Their job is to protect their employer’s bottom line, not yours.

A public adjuster, on the other hand, is the only type of insurance adjuster licensed by the state to work exclusively for you, the policyholder. We are your advocate.

We step in to level the playing field. A good public adjuster handles all communication with the insurance company, meticulously documents every detail of your pipe burst water damage, and negotiates from a position of strength. We speak their language and use hard evidence to fight for you. To see exactly what we do, you can learn what a public adjuster does in our detailed guide.

Ultimately, our goal is to make sure you get every penny you are entitled to under your policy, not just what the insurance company wants to pay.

Real Client Review: Fighting a Low-Ball Offer

Don't just take our word for it. Here's what a real client had to say after their insurance company tried to underpay their claim:

"When we had a main line burst, our insurance company tried to low ball us and sent a check that wouldn't have even paid for a fourth of the damages. Once we hired For the Public Adjusters everything became easy. Zack took care of everything and worked with the insurance company and our mortgage company to get everything handled and paid for. Very much worth hiring them to get the maximum for your damages. Would 100% recommend to anyone making a claim."

– Adam B., Google Review

This experience is incredibly common. Insurers count on policyholders not knowing the true cost of repairs, making it easy for them to offer a fraction of what is needed. Hiring an advocate changes that dynamic completely.

Don’t let your insurance company bully you into accepting less than you deserve. If your pipe burst claim has been denied, delayed, or drastically underpaid, reach out to the team at For The Public Adjusters, Inc. We offer a free, no-pressure claim review to see how we can help. Let us take on the fight for you. Find out more at https://forthepublicadjusters.com.