Ordinance or Law coverage is a policy add-on that pays the extra costs to rebuild your property to meet current building codes after a disaster. Your standard homeowner's or business owner's policy is designed to do one thing: pay to restore your property to its previous condition. Insurance companies like State Farm and Allstate deliberately exploit this to create a massive, often six-figure gap between what they pay and what it actually costs to legally rebuild.

The Rebuilding Cost Your Insurance Company Hides

Let’s say a hurricane tears through your neighborhood and wrecks your home. You file a claim, assuming the policy you've been paying for years has you covered. But then the local building inspector delivers some shocking news: your home can't just be patched up. It must be rebuilt to meet dozens of new, expensive codes that didn't exist when it was first constructed.

Suddenly, your insurance company—maybe a big name like Allstate or State Farm—informs you they will only pay to rebuild the home as it was. Their adjuster will deny payment for the mandatory storm-resistant windows, updated wiring, stronger structural supports, or new plumbing required by law. This is a common tactic to lowball your claim, leaving you with a crippling bill to bridge the gap between what their policy pays and what it legally costs to rebuild.

The Hidden Threat in Your Policy

This isn't a rare "what if" scenario; it's a hidden threat lurking in millions of property insurance policies. Insurance companies profit by minimizing payouts, and they often downplay or completely leave out adequate Ordinance or Law coverage from standard policies. This protection is specifically designed to pay for these legally required—and expensive—upgrades that your basic dwelling coverage will not touch. As you consider these significant financial risks, a broader understanding of how to prepare can be invaluable. This Your Guide to Risk Mitigation Planning offers some great insights.

This coverage isn't a luxury; it's a financial shield against a common tactic used by insurers to underpay claims. Without it, you are exposed to immense out-of-pocket expenses just to comply with local laws.

This vital coverage is typically broken down into three crucial parts, often labeled Coverage A, B, and C. Each part addresses a specific financial blow that the insurance company's adjuster is trained to ignore.

Let's break down exactly what these three parts do and why each one is so critical in your fight against the insurance company.

Ordinance Or Law Coverage at a Glance

This table explains the three crucial components of this coverage and the rebuilding risks they address.

| Coverage Part | What It Covers | Real-World Problem It Solves |

|---|---|---|

| Coverage A: Loss to the Undamaged Portion | Pays for the value of the undamaged parts of your property that must be torn down to comply with local building ordinances. | Your town's law says if 50% of a structure is damaged, the entire structure must be demolished and rebuilt to code. Your insurer's adjuster will only offer to pay for the damaged 50%, leaving you with a total loss on the other half. This coverage forces them to pay that gap. |

| Coverage B: Demolition Cost | Covers the expense of tearing down and hauling away the undamaged portion of the building. | The cost to demolish and remove the "good" part of your house can run into the tens of thousands. Your standard policy doesn't cover this, forcing you to pay out of pocket before rebuilding can even begin. |

| C: Increased Cost of Construction | Pays for the additional expenses required to rebuild your property to meet current, stricter building codes. | This is the big one. It covers mandatory upgrades like hurricane-straps, modern electrical systems, and updated plumbing that your original policy won't touch, even though they are legally required. |

Understanding how these components work together is the first step in fighting back and making sure you have the protection you actually need. You can dive deeper into this topic and learn more about why building code upgrade coverage is so important for homeowners.

Breaking Down the Three Pillars of Your Coverage

To fight back against a lowball offer, you first have to understand the language your insurer uses to confuse and underpay you. Ordinance or Law coverage isn’t some vague, single safety net; it’s a strategic defense system made up of three distinct parts. Each one is built to counter a specific financial gut-punch your insurance company hopes you'll take on the chin.

Think of it as a three-legged stool. If one leg is missing or too short, the whole thing collapses, leaving you to crash to the ground. Let's pull back the curtain on these three pillars so you know exactly what your insurer owes you.

To make this clearer, let's break down how these three critical parts work together.

Ordinance Or Law Coverage Breakdown

| Coverage Part | What It Covers | Example Scenario |

|---|---|---|

| A: Undamaged Portion | Pays for the value of the part of your property that wasn't directly damaged but must be torn down by law. | A fire destroys 60% of your business. A local ordinance requires a full demolition if damage exceeds 50%. This covers the loss of the "good" 40% that the insurance company will refuse to pay for. |

| B: Demolition Cost | Pays the actual cost to tear down and haul away the undamaged portion of the structure that the law requires to be removed. | Following the fire, this covers the $10,000+ bill to bring in a wrecking crew to demolish that undamaged 40% and clear the lot—a cost the adjuster will leave out of their estimate. |

| C: Increased Construction Cost | Pays the extra expense to rebuild your property to meet current, stricter building codes that weren't in place when it was first built. | Your new building must have a modern sprinkler system to meet new fire codes, a $100,000+ expense your basic policy won't touch. |

Each part plugs a specific, and often devastating, financial hole that your standard policy is designed to ignore. Now, let’s look closer at each one.

Pillar 1: Coverage A – Loss to the Undamaged Portion of the Building

This is where the insurance games really get started. Imagine a fire tears through 60% of your North Carolina home. The damage is severe, but 40% of the house—maybe a couple of bedrooms and the garage—is completely untouched by the flames.

You might think your insurance company will just pay to repair the burnt section. But then the county inspector shows up and drops a bomb: because more than half the home is damaged, a local ordinance demands the entire structure be demolished for safety.

Your standard dwelling policy only pays for the 60% that actually burned. The adjuster will coolly tell you they don't owe a dime for the remaining 40% because it wasn't damaged by a covered peril. This is the trap. Coverage A is what pays you for the value of this "undamaged" portion that the law says has to be destroyed. Without it, you’ve just suffered a total financial loss on nearly half your home.

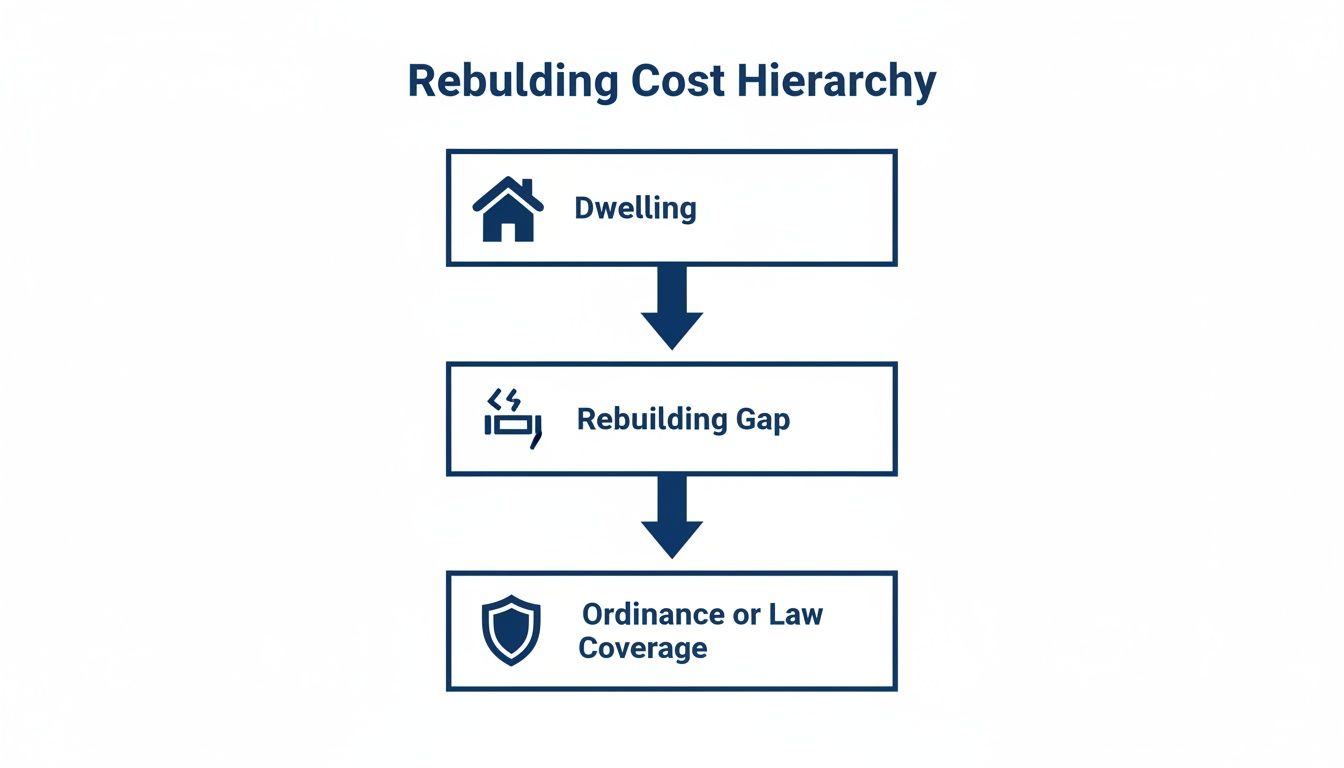

This diagram shows exactly how Ordinance or Law coverage is meant to bridge the gap left by your standard dwelling policy.

As you can see, this coverage is the shield that protects you from the massive rebuilding gap that insurers create by only offering to pay for partial repairs.

Pillar 2: Coverage B – Demolition Cost

So, you’ve just lost the value of the "good" part of your house. But the financial pain is about to get a lot worse. The city has ordered you to tear it all down, and that costs money—a lot of it.

Your standard policy might cover the cost of removing debris from the damaged part of your property. But who pays to demolish and haul away the undamaged 40%? That’s another bill your insurance company will refuse to pay without this specific coverage.

This is where Coverage B steps in. It’s designed to pay the real-world costs to bring in the heavy machinery needed to tear down and remove the rest of your home. Without it, you could be staring down a bill for $10,000, $20,000, or even more just to clear your lot before you can even think about rebuilding. It’s an out-of-pocket gut punch that can drain your savings and stop your recovery dead in its tracks.

Pillar 3: Coverage C – Increased Cost of Construction

This is the real powerhouse of Ordinance or Law coverage, and it's the part that insurers fight tooth and nail to avoid paying. Building codes are constantly being updated. A home built just ten years ago is almost certainly non-compliant with dozens of today’s stricter safety and energy regulations.

After a major loss, you can’t just rebuild your property "as it was." The local building department is going to require you to meet every single current code. This often involves jaw-droppingly expensive mandates like:

- Upgraded Electrical Systems: Tearing out old wiring and installing modern, grounded circuits to prevent fires.

- Modern Plumbing: Replacing old pipes with new materials to meet current health and safety standards.

- Hurricane Straps and Bracing: In coastal areas of North Carolina and Virginia, this is now mandatory to protect against wind damage.

- Elevating the Structure: In flood-prone zones, you may be forced to raise your entire home several feet—a project that can easily cost over $100,000.

Your standard policy will not pay one red cent for these legally required upgrades. An adjuster from a big carrier will just say their job is to restore your property to its pre-loss condition. Coverage C is the hammer that forces them to pay the increased cost to rebuild your home legally and safely. It's the difference between getting a modern, compliant home and a settlement that only covers half the job.

The costs associated with being displaced during these long repairs can also be staggering. For a closer look at how your policy should cover those expenses, you can learn more about Loss of Use coverage in our detailed guide. Knowing every part of your policy is absolutely critical to a full recovery.

Why Your Insurer Downplays This Essential Protection

Let's be blunt about a fundamental conflict of interest baked into every insurance policy: your provider makes more money by paying you less. This isn't just business as usual; it's a deliberate financial strategy. Major insurers like Allstate and State Farm have a massive incentive to keep you in the dark about how vital Ordinance or Law coverage really is.

Why? Because selling you a bare-bones policy with little or no ordinance coverage slashes their financial risk after a widespread disaster, like a hurricane barreling into the North Carolina coast. When thousands of homes get damaged at once, the total cost of legally required upgrades can soar into the billions. It’s far more profitable for them to let you foot that bill.

Common Tactics Used by Company Adjusters

The adjuster sent by your insurance company is not your ally. They are a trained employee whose primary job is to protect their company's bottom line—not your financial recovery. When it comes to Ordinance or Law claims, they come armed with a playbook of tactics designed to deny, delay, and underpay.

You can expect to hear arguments like these:

- "That code update is just a recommendation." This is a classic move. They’ll try to paint a mandatory legal requirement as an optional "suggestion," hoping you won’t take the time to check with your local building department.

- "The damage isn't severe enough to trigger the ordinance." Insurers love to misinterpret local laws, especially the "50% rule." They'll argue your damage falls just shy of the threshold that mandates a full demolition and rebuild to current codes.

- "Our estimate covers repairs to how it was." Their first offer will almost certainly ignore the increased cost of construction. They'll hand you a lowball estimate that only covers the pre-loss condition, conveniently sidestepping the tens of thousands of dollars needed for legally required upgrades.

The core strategy for many large insurance carriers is simple: bet on your ignorance of the policy and the law. They’ve built a system that puts you at a severe disadvantage from the moment you pick up the phone to file a claim.

This intentional downplaying of coverage creates a dangerous financial gap for homeowners. To fully understand your protection, it's also helpful to recognize the role of the different types of insurance agencies that might have sold you the policy in the first place.

The Financial Incentive to Underinsure You

The hard truth is that many insurance agents are incentivized to sell cheaper policies to win your business. A policy stripped of robust Ordinance or Law coverage carries a lower premium, which looks like a great deal upfront. But that "savings" vanishes the instant you have a major claim, potentially leaving you with a six-figure deficit to rebuild your home.

This benefits the insurer twice. First, they collect your premiums on a policy that carries far less risk for them. Second, when a disaster does strike, their payout is capped at a much lower amount. It’s a business model built on shifting the biggest financial risks of rebuilding directly onto your shoulders.

This is precisely where a public adjuster becomes your most critical advocate. We don't work for the insurance company; our loyalty is exclusively to you. We use our deep knowledge of policy language, construction costs, and local building codes to dismantle the company adjuster's weak arguments. We force them to acknowledge and pay for every single legally required upgrade, ensuring you get the full settlement you're owed to put your property back together—correctly and safely.

Real-Life Nightmares When Coverage Falls Short

It’s one thing to talk about policy gaps in theory. It's another thing entirely to live through the financial devastation when those gaps become your reality. These stories aren’t rare hypotheticals; they are the predictable, real-world consequences that unfold when insurance companies leave you stranded without the right protection.

Case Study: The Historic Virginia Home Fire

Imagine a family in a gorgeous, century-old home nestled in one of Virginia's historic districts. A kitchen fire gets out of control, tearing through the back half of their house. They file a claim, and the initial offer from their big-name insurance carrier seems fair enough to repair the fire damage.

Then, the nightmare begins.

The local building inspector delivers the crushing news. Because of the home's age and the scale of the damage, local ordinances now demand a complete overhaul of the electrical system, ripping out all the old knob-and-tube wiring. On top of that, a new law requires them to install a modern fire sprinkler system throughout the entire house—something that wasn't even conceived of when the home was built.

The price tag for these legally mandated upgrades? A jaw-dropping $75,000.

When they take this back to their insurance adjuster, he shuts them down. The policy, he says, only covers restoring the home to its pre-fire condition. They’re left holding a settlement that makes it illegal to rebuild, forcing them to choose between draining their life savings or walking away from their home.

In a situation like this, a public adjuster would have seen these code-related costs coming a mile away. We would immediately bring in an electrical engineer and a fire suppression specialist to create an undeniable expert report. This isn't about "optional" upgrades; it's about proving what is legally required to make the home whole again—and forcing the insurer to pay for it.

Case Study: The North Carolina Coastal Storm

Now, let's head to the North Carolina coast. A family’s home gets slammed by a brutal storm, with high winds and storm surge wrecking the foundation and first floor. The insurance company's adjuster shows up, does a quick walk-through, and writes an estimate for the visible damage.

But here’s the catch. Since the last big storm, federal and local authorities have completely redrawn the flood maps in their area. To mitigate future damage, new building codes now mandate that their entire house be elevated eight feet off the ground. This isn't a minor tweak; it's a monumental expense that can easily top $150,000.

Their standard homeowner's policy is useless here. The insurer’s stance is cold and clear: they’ll pay to patch up the floor and foundation right where they are, but not a dime toward lifting the house to comply with the new law. The family is financially shattered, holding a check that's just a fraction of what they actually need.

This exact scenario became a widespread disaster for countless families after major storms. When Hurricane Florence hit the coast in September 2018, it left over $22 billion in damages in its wake. Thousands of homeowners suddenly found that rebuilding meant meeting much stricter flood elevation rules. Without Ordinance or Law coverage, they saw their repair bills jump by 20-50% over the initial estimates, according to post-storm insurance analyses. You can dig into more insurance industry insights about managing these escalating risks.

In both of these all-too-common nightmares, the insurance company's first offer was a calculated lowball. It was designed to cover only the most basic, direct damage while completely ignoring the massive, legally required costs to actually finish the job. This isn't an oversight—it's a business strategy. A public adjuster's job is to dismantle that strategy from day one and build a claim based on what it truly costs to make a family whole again under the law, not on what the insurer wishes they had to pay.

How a Public Adjuster Forces a Fair Payout

When your insurer digs in their heels after a disaster, it's easy to feel powerless. That’s the moment a public adjuster steps in to completely turn the tables. We don’t just "help" with your claim; we take control, becoming your exclusive advocate in a fight against a company that’s actively trying to underpay you.

This isn't about filling out forms. It’s about executing a strategic, expert-driven game plan designed to dismantle the insurer’s lowball tactics and force them to pay what their policy legally obligates them to. The chasm between a company adjuster's quick glance and a settlement that actually makes you whole is night and day.

Uncovering Every Dollar of Available Coverage

The battle starts with a forensic review of your insurance policy, line by line. We dive deep into the dense language, endorsements, and exclusions to find every single ounce of coverage you’re entitled to for your Ordinance or Law claim.

Insurance companies count on you not understanding the critical differences between Coverage A, B, and C. We don’t just point these out; we build our entire strategy around them, leaving the insurer with zero wiggle room to play dumb or twist the meaning of their own contract.

Assembling an Unbeatable Team of Experts

Let's be clear: the adjuster your insurance company sends out is not a building code expert. They're not an engineer or a seasoned contractor. Their job is to write up an estimate based only on what they can see, completely ignoring the legal requirements for rebuilding.

To blow that flimsy approach out of the water, we bring our own team of specialists to the fight.

Our process involves deploying:

- Certified Engineers: They assess the true structural integrity and provide the professional opinion needed to determine when local ordinances trigger a full demolition.

- Building Code Experts: They create a definitive report detailing every mandatory upgrade required by state and local laws—the very things your insurer wants to ignore.

- Experienced Contractors: They deliver real-world, local pricing for these upgrades, exposing the insurer’s lowball, software-generated estimates for the fantasy they are.

This creates an ironclad wall of evidence that turns your claim from a polite request into an undeniable demand for payment.

Building an Evidence-Based Scope of Loss

Armed with reports from our experts and an intimate knowledge of your policy, we create a comprehensive scope of loss. This isn't just another estimate. It’s a documented, undeniable blueprint for what it will actually cost to rebuild your property correctly and, most importantly, legally. It includes every mandatory code upgrade, the full cost of demolition, and the value of any undamaged parts of the property that have to be torn down.

We package this mountain of evidence and present it directly to the insurance company. Suddenly, we're not just asking—we're negotiating from a position of overwhelming strength. They can no longer hide behind vague denials when confronted with indisputable facts from certified professionals.

This expert-driven strategy is a core part of what a public adjuster does to maximize your settlement. We level a playing field that was always tilted in the insurance company's favor.

This proactive approach is crucial, especially when you see the staggering gap between economic and insured losses after major disasters. Between 2014-2023, the Americas suffered $1,297 billion in economic losses, but only $706 billion was covered by insurance—leaving a 46% gap. A huge chunk of that uninsured cost comes from ordinance and law requirements that insurers conveniently "forget" in claims, leaving homeowners to foot the bill. After the 2018 Camp Fire in California destroyed 18,000 buildings, survivors were shocked to learn their policies didn't account for new fire-resistant building codes, which added 15-30% to their rebuilding costs. You can read the full analysis on global insurance trends to see just how widespread this problem is.

Frequently Asked Questions About Ordinance Or Law Claims

Trying to make sense of an insurance claim is tough enough. When you add Ordinance or Law issues into the mix, it can feel downright impossible. We’ve seen countless homeowners get stonewalled by their insurance companies on this, so we’ve put together direct answers to the questions we hear most often. This is the information you need to fight back.

Isn't Ordinance Or Law Coverage Standard in a Homeowners Policy?

This is probably one of the most dangerous myths out there, and insurance companies are more than happy to let you believe it. Most standard policies might throw in a tiny bit of this coverage—often just 10% of your dwelling limit—but that’s almost never enough for a major repair, especially on an older home.

The truth is, getting enough Ordinance or Law protection usually requires an add-on, or what the industry calls an endorsement, that you have to buy separately. Agents for the big carriers like Allstate or State Farm often don't explain how crucial this is, leaving homeowners exposed and severely underinsured. One of the very first things a public adjuster does is a deep dive into your policy to uncover the true limits and start building a case to make the insurer pay them.

My Insurer Says the New Codes Are Just Recommendations. Is That True?

Absolutely not. This is a classic delay-and-deny tactic we see all the time from company adjusters. They use it to weasel out of paying for expensive, legally required upgrades. Building codes aren't polite suggestions; they are laws, and they're enforced by your city or county building department.

If a building inspector tells you that you have to upgrade your wiring, raise your foundation, or install hurricane straps before they'll issue a permit, that’s a legal order. A good public adjuster will immediately get on the phone with local building officials to get that requirement in writing. We then use that official document as cold, hard proof to shut down the insurance company's weak argument and force them to pay what they owe for the increased cost of construction.

An insurance company's opinion does not override the law. When a building department issues an order, it is non-negotiable, and your policy should respond accordingly.

How Do I Know if My Claim Involves Ordinance Or Law Issues?

Here’s a good rule of thumb: if your home or business property is more than a few years old and has significant damage, it's almost a guarantee that Ordinance or Law is a factor. Building codes are updated constantly, sometimes every few years. That means nearly any property that isn't brand new will have parts that are no longer up to code.

The only way to know for sure is to have a public adjuster review your claim from day one. We don’t just look at the obvious damage. We dig into your policy, the age of your property, and the specific local codes for your town to build a proactive and powerful case for these costs—one that your insurer can't just dismiss or ignore.

Can I Fight the Insurance Company for This Coverage on My Own?

You certainly have the right to, but you need to understand what you’re up against. You’re essentially stepping into a game where your opponent created the rules, owns the stadium, and pays the referees. Insurance companies have entire departments of lawyers, engineers, and claims specialists who have one single job: to pay you as little as possible.

Hiring a public adjuster is all about leveling that tilted playing field. We are policy experts and construction specialists who know their entire playbook. We’ve seen their lowball tricks, their stall tactics, and we know exactly how to counter them with undeniable evidence and expert reports. Working with a public adjuster dramatically increases your odds of getting a fair settlement that allows you to rebuild your life the right way.

Don't let your insurance company dictate the terms of your recovery. If you're facing a tough battle over your homeowner or business claim, the experts at For The Public Adjusters, Inc. are here to fight for you. We offer a no-cost claim review to help you understand your rights and secure the settlement you deserve. Contact us today at https://forthepublicadjusters.com.

It’s good to know about ordinance or law coverage, especially since standard policies only cover restoring a property to its *previous* condition.