A pipe bursts over the weekend. Or a small fire rolls smoke through your shop, office, or warehouse. Monday morning starts with panic, then relief. You've got insurance. Then the carrier's adjuster shows up, asks loaded questions, takes a quick look, and acts like the damage is smaller than what you're staring at.

That's when most business owners learn the hard truth. The true challenge doesn't start when the damage happens. It starts after you open the claim.

If you're searching what does commercial property insurance cover, you're probably not doing it out of curiosity. You're doing it because the insurance company is pushing back, narrowing the loss, or waving policy language around like a weapon. That frustration is justified. Commercial property policies can cover a lot, but insurers use complexity, exclusions, coinsurance rules, and documentation demands to cut what they pay.

Table of Contents

- Your Claim Fight Starts After the Damage

- Decoding What Your Policy Actually Covers

- Named Peril vs All Risk Policies

- Exclusions Insurers Use to Deny Your Claim

- Dangerous Gaps in Your Endorsements

- How Insurers Exploit Coinsurance and Documentation

- Your Claim Help Action Plan for NC and VA

Your Claim Fight Starts After the Damage

Most owners expect the hard part to be cleanup. It isn't. The hard part is dealing with an insurance company that already knows your policy better than you do and intends to use that advantage.

A restaurant owner sees water coming through a ceiling after a plumbing failure. The flooring buckles, drywall swells, insulation gets soaked, and the kitchen has to shut down. The carrier's adjuster writes for what's visible, skips what's behind walls, and starts framing parts of the loss as maintenance instead of sudden damage. That's not a mistake. That's a familiar claims strategy.

A warehouse owner gets hit by a storm, then hears the same routine. “We need more documentation.” “This may not be covered.” “We're still investigating cause.” Meanwhile the business is bleeding money, tenants are calling, and the first payment doesn't come close to the cost to repair.

You pay premiums for protection. The carrier protects its balance sheet first.

That's why a plain-language understanding of coverage matters. Not because you want to become an insurance lawyer. Because when the company tries to low-ball or deny your claim, you need to know what they're supposed to pay for and where they typically cheat the scope.

If your dispute is already heading in that direction, start with a practical breakdown of commercial property damage claims and compare it to how your insurer is handling your file.

What the company adjuster is doing right now

They're usually doing some version of this:

- Narrowing the cause: They look for any reason to classify damage under an exclusion or partial exclusion.

- Shrinking the scope: They write for stained drywall but ignore wet insulation, trapped moisture, damaged subfloor, or smoke migration.

- Questioning value: They challenge whether an item belongs to the building, business personal property, equipment, or stock.

- Building a paper trail: They ask questions in ways that help support a later denial, delay, or reduced payment.

That's the fight. Not the brochure version of insurance. It's the actual one.

Decoding What Your Policy Actually Covers

Commercial property insurance is supposed to cover physical damage to business buildings and their contents. Common claims include water damage and burglary, while fire is the costliest claim type with an average cost of $80,000. Many policies also require you to insure at least 80% of the property's replacement value or face coinsurance penalties that reduce claim payouts, according to Construction Coverage's commercial property insurance explanation.

If you financed the property, your lender probably cared a lot about valuation and replacement cost on the front end. That's why business owners reviewing their acquisition or refinance paperwork often benefit from the SBA commercial real estate loan guide. It helps you connect financing assumptions to the insurance values that become a problem later during a claim.

The building is only the start

When owners ask what does commercial property insurance cover, they usually think “the building.” That's only part of it.

The policy declarations and forms can extend to the structure itself, completed additions, permanently installed machinery, and business personal property. That often includes furniture, fixtures, improvements, supplies, tools, and other contents tied to operations. But during a dispute, the insurer doesn't treat those categories as neutral. They use them to carve the claim up.

Here's the practical way to read it:

| Category | What you expect | How carriers try to cut it |

|---|---|---|

| Building | Walls, roof, floors, built-ins, permanent fixtures | They argue parts are pre-existing, cosmetic, or not permanently installed |

| Business personal property | Furniture, computers, office contents, supplies | They depreciate heavily or claim incomplete proof of ownership |

| Equipment | Machinery, trade tools, specialized apparatus | They call damage repairable when replacement is needed |

| Stock or inventory | Raw materials, work in process, finished goods | They challenge quantity, condition, or value |

If you don't know how the insurer is categorizing damaged property, you can't spot the low-ball.

The adjuster's favorite low-ball categories

The easiest way for a carrier to reduce payment is to move property into a bucket with less favorable treatment, then act like that decision is obvious.

A built-in fixture may suddenly become “contents.” Tenant improvements may get treated as somebody else's responsibility. Equipment may be priced like used office furniture instead of specialized business machinery. Inventory may be limited because your records aren't organized the way the carrier wants.

Practical rule: Don't argue the claim in general terms. Force the insurer to identify each damaged item, the category they assigned to it, the value they used, and the policy language behind that treatment.

If you're trying to understand the structure before you push back, read your forms line by line and compare them against this guide on how to read an insurance policy. Most denied and underpaid claims aren't lost because there was no coverage. They're lost because the policyholder never pinned the insurer down on what was covered under each category.

Named Peril vs All Risk Policies

The type of policy form you have changes the whole claim fight. Some owners don't learn this until the denial letter arrives.

Commercial property coverage is built around Cause of Loss forms. Basic form policies cover a specific list of risks such as fire and windstorms, while Special form policies operate as all-risk coverage and cover all perils except those specifically excluded. That structure affects claim settlements, and underinsurance can still reduce what gets paid, as explained by the Florida CFO's commercial property insurance overview.

Why the burden of proof matters

With a named peril policy, you usually have to show that the damage was caused by a peril specifically listed in the form. If the cause doesn't fit neatly into one of those named categories, the carrier has an opening to deny.

With an all-risk or Special Form policy, the starting point is different. The loss is generally covered unless the insurer can point to an exclusion that removes it. That's why adjusters on these claims often spend so much time hunting for policy exclusions, prior damage arguments, or wear-and-tear defenses.

Here's the clean comparison:

- Named peril policy: You prove the loss falls inside the listed causes.

- All-risk policy: The insurer tries to prove the loss falls outside coverage because an exclusion applies.

That distinction matters more than most owners realize. It determines who starts the fight uphill.

A short explainer helps if you want the policy form difference in plain English:

How this changes your dispute strategy

If you've got a named peril form, causation becomes the center of the dispute. You need to tie the damage directly to a listed event and document that connection tightly.

If you've got an all-risk form, don't let the carrier bluff you with broad statements. Ask a direct question: What specific exclusion are you applying, and where is it in the policy? If they can't answer that cleanly, they may be stalling while they look for one.

On an all-risk claim, vague suspicion from the insurer isn't enough. They need a real exclusion, not a shrug and a low offer.

Exclusions Insurers Use to Deny Your Claim

Coverage disputes usually don't die in the main grant of coverage. They die in the exclusions.

That's where carriers try to turn a valid property loss into a maintenance issue, a pre-existing issue, or a cause that the policy doesn't insure. They know most business owners never read the exclusions until after the damage, and by then the insurer has already built its position.

The denial usually starts with one word

That word is often “excluded.”

Not every exclusion is wrong when applied. But many are stretched. A carrier may point to wear and tear when the actual loss involved sudden water release. They may point to deterioration to avoid paying for resulting damage. They may isolate one part of the cause chain and ignore the covered damage that followed.

Watch for these common denial setups:

- Wear and tear framing: The company says the condition developed over time, so they avoid paying for the damage that followed.

- Deferred maintenance accusations: They imply neglect without proving it.

- Unlisted location problems: Owners with multiple sites can get hit hard if a location wasn't specifically scheduled on the policy.

- Code and upgrade limits: The insurer pays for basic repair but resists the additional cost required to rebuild properly.

Another overlooked trap is multi-location coverage. Many owners assume one commercial property policy automatically protects every business site, but standard policies can leave unlisted locations uninsured. That's a structural coverage problem, not a peril issue, and it catches businesses off guard when a claim is already underway.

Flood claims are their own battlefield

Flood damage is a separate mess. Standard commercial property policies routinely exclude it, which means businesses usually need a separate flood policy through the National Flood Insurance Program or a Write Your Own carrier. For commercial properties, NFIP coverage is capped at $500,000 for the building and $100,000 for contents, and claims are often delayed 6 to 12 months because of strict documentation rules and adjuster shortages, according to this analysis of flood claim tactics and NFIP limits.

That's why flood disputes are so brutal for business owners in North Carolina and Virginia. The limits can be too low for the actual exposure, the paperwork burden is heavy, and the timeline can drag while your operation sits damaged or partially shut down.

If your commercial loss involves flood, treat it as a separate federal-style dispute from day one. Don't assume it works like a normal property claim.

And if the adjuster is from NFIP or a WYO company, expect rigid documentation demands, narrow readings of damage, and very little patience for incomplete submissions.

Dangerous Gaps in Your Endorsements

Business owners hear “you added the endorsement” and think that means the problem is solved. It doesn't. Endorsements help, but they also come loaded with sub-limits, narrow triggers, waiting periods, and definitions the insurer will use against you.

Extra coverage still has traps

Take business interruption. Owners assume it will make them whole if operations stop after a covered loss. Then the carrier starts arguing about the period of restoration, the records needed to prove lost income, and whether the shutdown really flowed from covered physical damage.

Ordinance and law coverage creates another fight. Rebuilding after a serious loss often means complying with current code, not yesterday's conditions. The insurer may agree to pay for direct physical damage but resist the added cost of required upgrades.

Equipment breakdown can also disappoint owners who thought all machinery damage was automatically covered. Carriers often separate breakdown issues from other property damage issues, then force you into a technical causation fight over whether the damage came from a covered event or from internal failure.

Here's where owners get trapped:

- Business interruption: The insurer scrutinizes financial records and narrows the shutdown period.

- Ordinance and law: The carrier pays for repair but resists the cost of code-required upgrades.

- Equipment breakdown: The dispute turns into a technical argument over cause, not just damage.

The rebuilding cost gap that blindsides owners

One of the most dangerous gaps sits inside the increased cost of construction endorsement, often called ICC. Policies often cap ICC at 4% or 5%, while construction material costs have risen over 15% in many sectors, creating a major underinsurance problem for businesses trying to rebuild after a large loss, according to Reshield's review of commercial property coverage gaps.

That gap gets ugly fast. The carrier points to the endorsement limit. The contractor points to current pricing. You pay the difference unless the policy was structured better before the loss.

Coverage on paper isn't enough. You need enough coverage at today's rebuild cost, under today's code requirements, with limits that match reality.

That's why a “covered claim” can still leave a business owner with a painful out-of-pocket bill.

How Insurers Exploit Coinsurance and Documentation

Many valid claims get cut down. Not denied entirely. Just shaved, restricted, and underpaid until the owner is too tired to keep fighting.

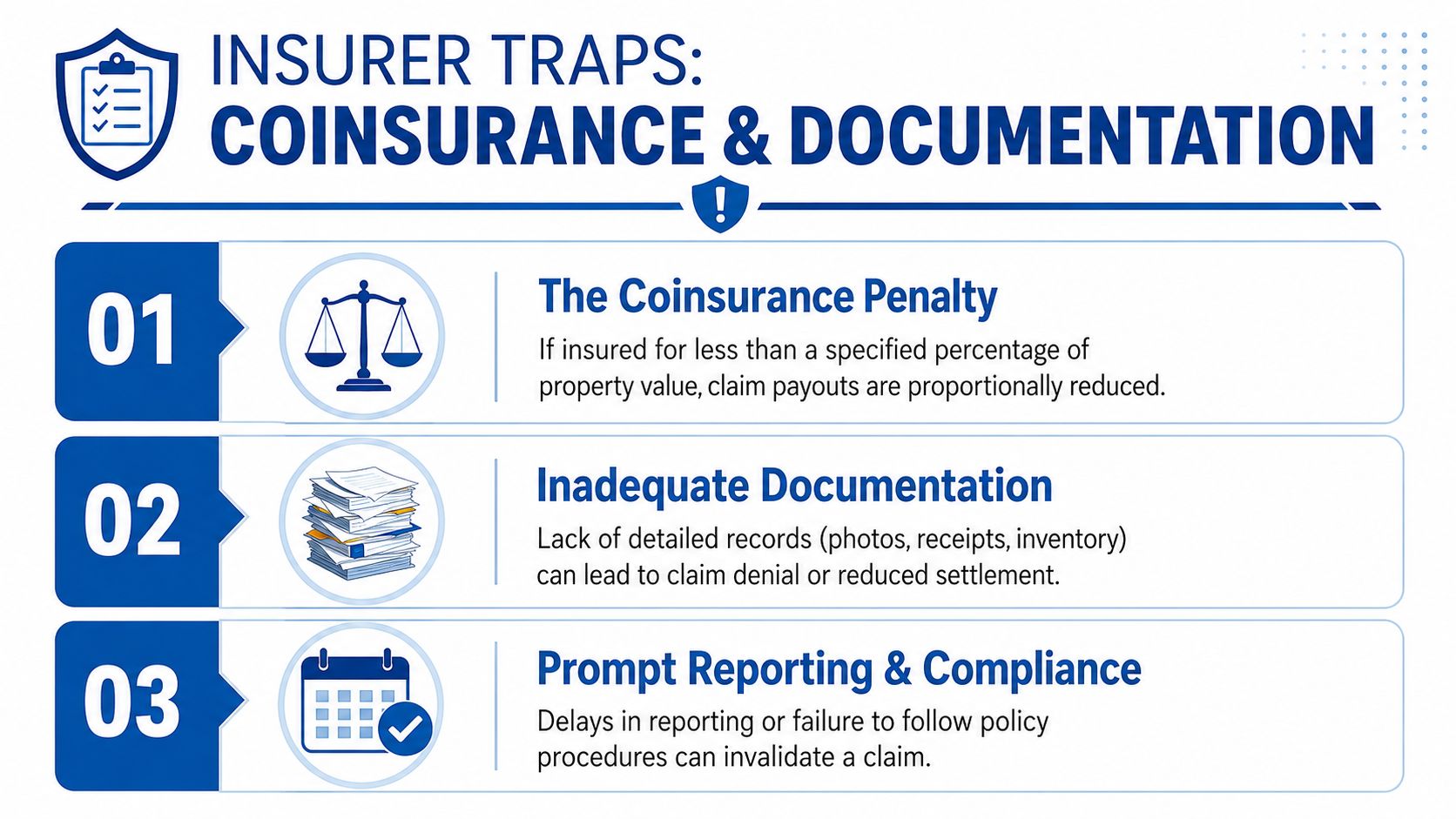

Coinsurance is where valid claims get slashed

Coinsurance sounds technical, but the effect is simple. If the building wasn't insured to the required percentage of value, the insurer can reduce the payment on a partial loss.

Owners hate this because they think, “I had coverage, I paid premiums, and I can afford repairs.” The policy usually doesn't care. If the coinsurance requirement wasn't met, the insurer uses the formula anyway.

That's why it's worth understanding the trap before you're in a dispute. If you need a plain-language breakdown, review this guide on what the coinsurance rule means. It shows why underinsurance becomes a payout problem even when the loss itself is covered.

Documentation is where omitted damage hides

The second trap is documentation. Carriers know most owners don't maintain perfect pre-loss inventories, photo logs, purchase records, and repair histories. They use those gaps to challenge quantities, values, and even the existence of damaged property.

This gets worse with hidden damage. Water behind walls. Moisture under flooring. Smoke in cavities. Damaged materials the field adjuster never opened up or never priced. Under most state rules, policyholders can demand the insurer's full scope-of-loss report and depreciation schedule. When insurers leave out non-visible damage, public adjusters can force revisions by comparing the carrier's scope line by line against contractor estimates, often recovering thousands in omitted damages, as described in this discussion of low-ball claim tactics and omitted damage disputes.

Use this checklist if the carrier's estimate feels light:

- Ask for the full scope: Demand the estimate, line items, depreciation details, and policy provisions they relied on.

- Compare room by room: Don't accept a summary page. Match every damaged area against the insurer's written scope.

- Look for hidden components: Insulation, subfloor, backing materials, contents manipulation, and cleanup often get skipped.

- Get independent estimates: A contractor's detailed scope can expose what the insurer left out.

- Stop talking loosely: Casual phone comments become claim file ammunition.

Claim tactic: When an insurer says, “We've already accounted for that,” ask them to show the exact line item and quantity. If they can't, it probably isn't really in the estimate.

Your Claim Help Action Plan for NC and VA

If you own or manage commercial property in North Carolina or Virginia, the playbook is straightforward. Don't let the carrier define the damage, define the cause, and define the value without a fight.

Start here:

- Read the declarations and cause of loss form. You need to know whether you're dealing with named peril or Special Form coverage.

- Demand the paperwork. Ask for the insurer's estimate, scope notes, depreciation schedule, and any policy language they're using to cut payment.

- Check every category of damage. Building, contents, equipment, and inventory should be evaluated separately and accurately.

- Challenge exclusions in writing. If they say part of the loss is excluded, make them identify the exact exclusion and explain how they applied it.

- Watch endorsements and location issues. Don't assume business interruption, code upgrades, or multiple properties are covered the way you think.

- Bring in professional help early. The right time is when the adjuster starts minimizing damage, delaying decisions, or making an offer that doesn't match reality.

The moment you should stop handling it alone is simple. If the insurer is under-scoping, low-balling, blaming exclusions without specifics, or dragging out the claim while your business suffers, get a licensed public adjuster involved.

Clients consistently value straight answers, detailed inspections, and aggressive documentation when a claim has gone sideways. That matters because most business owners don't need another hotline. They need someone who can read the policy, challenge the estimate, and push the carrier to pay what's owed.

For businesses in North Carolina and Virginia dealing with property damage, For The Public Adjusters, Inc. represents policyholders, not insurance companies. The firm handles business owner, dwelling, and homeowner property claims involving fire, smoke, water, wind, hail, hurricanes, tornadoes, theft, and vandalism. If your commercial property claim has been delayed, denied, or low-balled, their team can inspect the damage, document the loss, interpret the policy, and negotiate directly with the carrier. Clients turn to them for responsive communication, no-cost claim reviews, and real help when the insurance company's numbers don't make sense. Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!