The adjuster was polite. He walked the property, took photos, nodded at the obvious damage, and told you they'd “get this moving.” Then the estimate landed in your inbox and the number was absurd. It didn't match your contractor's scope. It ignored damaged contents. It said little or nothing about downtime. You're sitting there wondering whether this is incompetence or strategy.

It's usually strategy.

Commercial property damage claims don't turn into fights because business owners are unreasonable. They turn into fights because the carrier's first serious move is often to narrow the scope, price the work low, and force you to prove every dollar twice. That pressure is even worse in storm-prone losses. LexisNexis Risk Solutions reported that 46% of personal-lines property claims in 2023 were catastrophic, and wind claims were catastrophic 62% of the time in that dataset, which matters because the same storm systems hit commercial roofs, facades, inventory, and operations too (LexisNexis catastrophic property claims trend).

If you're comparing the carrier's estimate to what a real contractor says it takes to restore the property, get outside input early. For storm-related building work, practical repair context from contractors who handle this every day, such as ZEV Roofing & Construction commercial repairs, can help you spot when the insurer's scope is too thin.

If your loss came from wind, hail, or a major weather event, it also helps to understand the recurring dispute patterns business owners run into on commercial storm damage claims.

Table of Contents

- Introduction The Low-Ball Offer Is Just the Beginning

- Decoding Your Policy as an Insurer's Weapon

- The Insurance Company Playbook for Underpaying Claims

- Building Your Case An Evidence Package They Cannot Ignore

- Winning the Hidden Battles Business Interruption and Depreciation

- When to Call for Backup Hiring a Public Adjuster in NC or VA

- Conclusion Take Control of Your Claim and Your Recovery

Introduction The Low-Ball Offer Is Just the Beginning

That first offer isn't the finish line. It's the insurer testing whether you know how claims get underpaid.

A lot of business owners make the same mistake right here. They treat the carrier's estimate like a neutral evaluation. It isn't. It's a position paper written by a company that keeps more money when the scope stays small, the pricing stays low, and the business owner gets tired.

What the first low offer usually means

When a commercial claim comes in short, one of a few things is happening:

- The scope is incomplete: Roof sections, moisture mapping, hidden interior damage, electrical issues, code-triggered work, or damaged contents were left out.

- The pricing is suppressed: Labor, materials, overhead, specialty trades, access costs, and demolition are priced at levels that don't reflect what it takes to perform the work.

- The loss was split apart: Building damage gets one narrow estimate, contents are pushed off for later, and business interruption gets treated like a separate problem you somehow have to prove from scratch.

- The burden is being shifted to you: The carrier waits for you to assemble the complete case while pretending its own estimate is the default baseline.

The insurer's estimate is not the claim. It's only one version of the claim, and it's often the version cheapest for them.

Why this fight gets ugly fast

Commercial property damage claims sit inside a massive insurance segment. The Insurance Information Institute says commercial lines account for about half of U.S. property/casualty premium, which helps explain why insurers have highly standardized claims systems and demanding proof requirements for business losses (Insurance Information Institute commercial lines facts).

That scale cuts both ways. The insurer has process, forms, internal review layers, vendors, and adjusters trained to control loss costs. If you answer that machine with a few photos and a contractor quote, you're under-armed.

You need a claim file that's stronger than theirs. Not louder. Stronger.

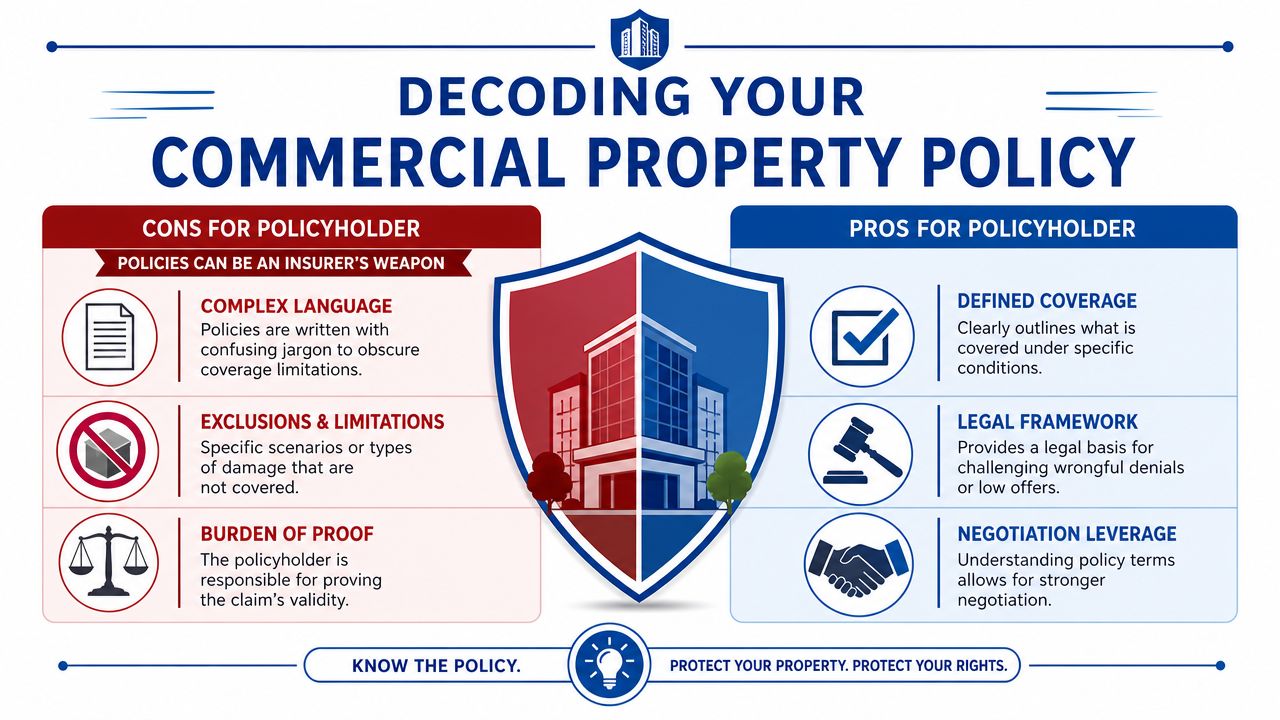

Decoding Your Policy as an Insurer's Weapon

Your policy matters most when the carrier starts using it against you.

A commercial property policy is not written in plain English for your convenience. It's a contract full of valuation rules, limitations, conditions, and exclusions. If you only read the declarations page for the limit and deductible, you're missing the parts the insurer will lean on when it wants to cut your recovery.

Read the declarations page like a defense file

Start with these items before you argue about money:

| Policy area | What you need to find | Why it matters in a dispute |

|---|---|---|

| Coverage type | Building, business personal property, business income, extra expense | Missing or limited categories create blind spots in the insurer's estimate |

| Valuation language | Replacement cost or actual cash value | This affects how much depreciation the carrier will try to take |

| Deductibles | Standard, wind, hail, named storm | A deductible dispute can distort what the carrier says is actually owed |

| Endorsements | Ordinance and law, special limits, protective safeguards | Endorsements often decide whether hidden costs are paid or excluded |

| Conditions | Notice, proof of loss, preservation of property, mitigation duties | These become the carrier's procedural arguments when payment slows down |

The terms that usually get used against you

Actual cash value versus replacement cost.

If the carrier can push payment into actual cash value, it can slash your initial recovery through depreciation. That matters a lot on older roofs, interior finishes, machinery, and tenant improvements. You need to know whether replacement cost is available, what conditions trigger it, and what documentation the policy requires before withheld amounts are paid.

Exclusions and anti-causation arguments.

The insurer will often look for wear and tear, deterioration, prior damage, repeated seepage, maintenance issues, or excluded water pathways. Business owners hear this and panic. Don't. The existence of age or wear does not automatically erase covered storm or accidental damage. But you do need evidence tying the loss to a covered event and showing the condition before the loss.

Coinsurance and valuation traps.

If your policy includes a coinsurance requirement, the carrier may argue the property wasn't insured to value and use that to reduce payment. Consequently, owners are often blindsided. They thought they bought “full coverage.” In truth, their purchase may be a policy with a penalty mechanism buried in the valuation section.

Practical rule: Never dispute a commercial property estimate until you've matched that estimate against the policy's valuation language, conditions, and endorsements.

The legal framework cuts in your favor too, if you understand it. The same contract the insurer uses to limit payment can also define covered property, covered causes of loss, and additional coverages that support a larger claim. Read it like you expect an argument, because one is already underway.

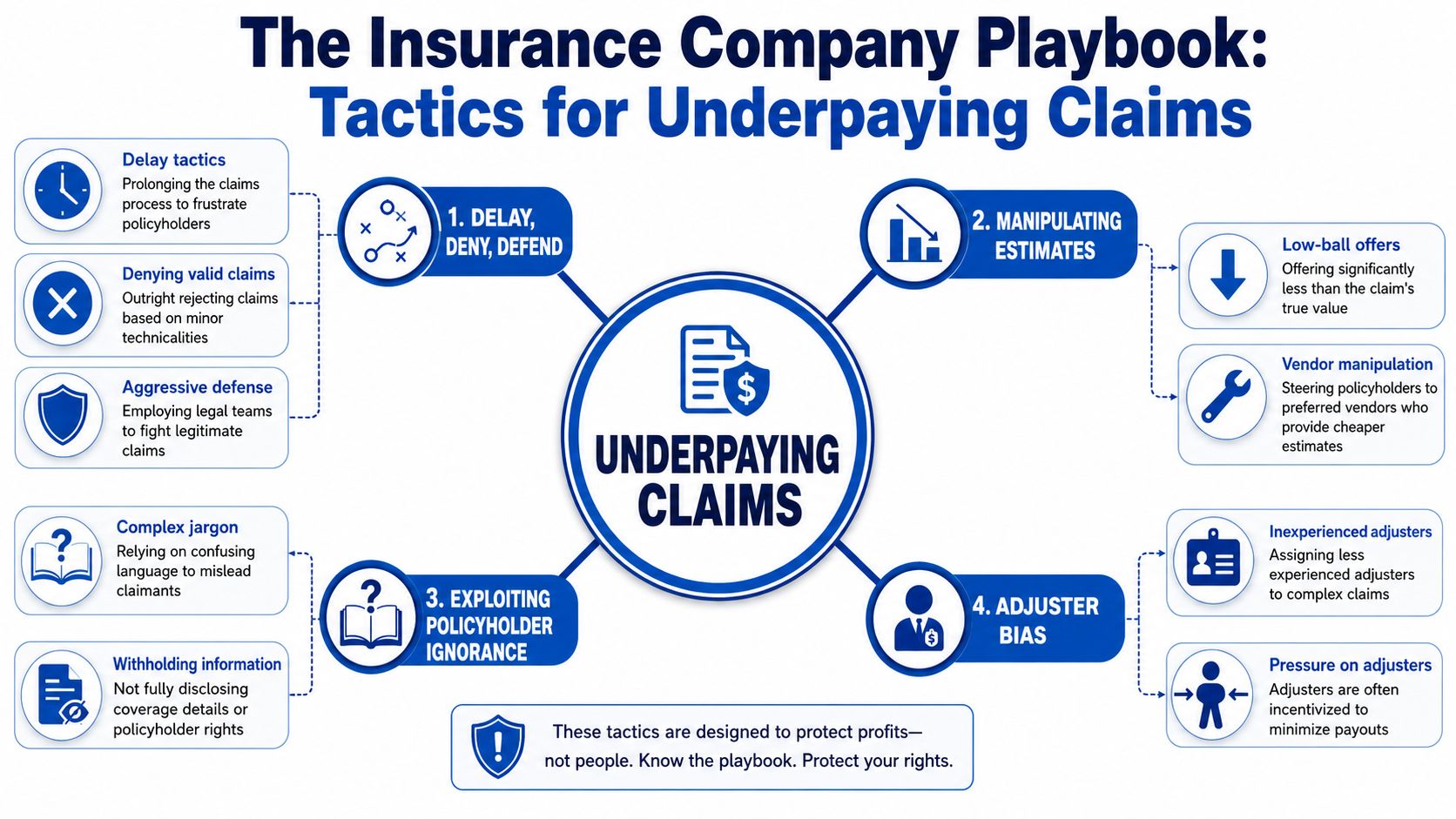

The Insurance Company Playbook for Underpaying Claims

Underpayment usually doesn't arrive as a dramatic denial. It arrives dressed up as cooperation.

The carrier says the loss is covered. It sends an estimate. It asks for “just a few more items.” It switches adjusters. It recommends a vendor. It says your contractor is too high. It says the roof can be repaired, not replaced. It says the downtime should've been shorter. Piece by piece, the claim gets trimmed.

Partial acceptance is where many claims get cut down

One of the most important things business owners need to understand is this: the main fight is often not over whether the claim exists. It's over how small the insurer can make it.

That pattern has been described directly in guidance on underpaid commercial claims. The issue is often partial acceptance, where the insurer agrees there's coverage but underprices the scope, labor, materials, or code-related work, leading to a low settlement position (underpaid commercial property damage claim disputes).

Here's what that looks like in practice:

- They accept roof damage, but only include patching: no full slope replacement, no matching issues, no accessory items, no overlooked penetrations.

- They pay for interior damage, but not the cause-driven repairs: paint without substrate work, spot treatment without full tear-out, limited electrical work without proper testing.

- They recognize building damage, but strip out code work: no upgrades, no compliance items, no related costs that real permits and inspections trigger.

The pressure tactics are usually procedural

Insurers also wear business owners down through process.

Some of the common moves are predictable:

- Redundant document requests that ask for records already submitted.

- Adjuster reassignment that forces you to restart the explanation.

- Preferred vendor steering where the “approved” contractor works to the carrier's budget, not your restoration needs.

- Silence after inspections until your business is desperate enough to take less.

- Narrow estimate software output presented as if it were reality instead of one cost model.

If the dispute moves beyond adjusting and into a broader conflict over obligations, records, or business-side fallout, legal guidance on resolving commercial legal disputes can help frame when the matter has stopped being a normal claim negotiation.

When the carrier keeps saying “we agree there is damage” while refusing to pay the amount required to fix it, you are already in a dispute.

Don't let the insurer define the argument as a minor pricing difference. In commercial property damage claims, underpayment often happens through scope control, not outright rejection.

Building Your Case An Evidence Package They Cannot Ignore

If you want more money, build more proof.

That doesn't mean random photos dumped into a folder. It means a disciplined evidence package that ties cause, scope, ownership, pre-loss condition, current pricing, and financial impact together. Commercial claims are documentation-heavy for a reason. They often require detailed repair estimates, inventory records, financial support, and sworn documentation, and the value of the claim depends on the completeness of that evidentiary chain rather than one quote alone (commercial property claim documentation requirements).

Build evidence by category, not by pile

Organize the loss into separate claim buckets.

Building damage should include photos, annotated diagrams, contractor scopes, permits if available, prior maintenance records, and a repair estimate that explains line items clearly.

Contents and equipment need an itemized inventory. Include description, location, age, original cost if available, vendor or replacement source, condition before the loss, and what physically happened to the item.

Financial loss requires its own lane. Pull tax returns, profit and loss statements, invoices, payroll records, rent obligations, and any records showing interruption to operations.

A short checklist helps:

- Photograph broadly first: Exterior elevations, roof areas, mechanical systems, interior rooms, and product storage.

- Then photograph tightly: Serial numbers, moisture damage, impact points, cracked finishes, detached materials, and damaged stock.

- Get independent estimates: Do not rely only on the insurer's number.

- Preserve damaged material when possible: Don't throw away the evidence before inspection is complete.

- Track emergency spending: Tarping, board-up, water extraction, temporary power, relocation costs.

Create a record that exposes delay and weak estimating

Your communication log matters almost as much as your estimate.

Create a running claim diary with dates, names, titles, phone calls, inspection dates, emails sent, documents submitted, and unanswered requests. If the adjuster changes, your file should make it impossible for the new person to pretend the history doesn't exist.

A comparison table is useful too:

| Disputed item | Carrier position | Your evidence |

|---|---|---|

| Roof scope | Repair only | Independent roofing scope, photos, test cuts, manufacturer issues |

| Interior damage | Cosmetic only | Moisture records, contractor demolition notes, damaged substrate photos |

| Contents value | Limited or undocumented | Inventory spreadsheet, invoices, tax support, vendor pricing |

| Timing | Waiting on insured | Email log showing responses and repeated submissions |

If the insurer claims your contractor pricing is inflated, use practical market references to test reasonableness. Even a general industry discussion like Commercial Roofers on roof pricing can help you ask better questions about what the carrier left out, such as access, tear-off, disposal, or material complexity.

A weak claim file invites a weak offer. A structured claim file forces the adjuster to answer specifics.

Winning the Hidden Battles Business Interruption and Depreciation

A lot of owners fight hard over the walls and roof, then lose badly on the parts that hurt the business most.

That's a mistake. The visible damage gets attention because you can point to it. The hidden damage to operations, cash flow, and valuation often goes underdeveloped, and that's where the claim gets seriously shorted.

Business interruption is often the real financial wound

General claim guidance often notes that business income coverage can reimburse lost revenue during repairs, and one commercial claim guide cites the average commercial property insurance claim cost at about $35,000, while also warning that this figure can understate the true loss once downtime and extra expense are included (common commercial property insurance claims and business interruption).

That gap matters.

If your storefront, restaurant, warehouse, office, or mixed-use property can't operate normally, the biggest hit may not be drywall or flooring. It may be:

- Lost income during repairs

- Continuing payroll you still have to carry

- Temporary relocation costs

- Rent or debt service that doesn't stop

- Extra expense to keep the business functioning in reduced form

The insurer will often try to compress the period of restoration. It may argue that your operations could've resumed earlier, that your slowdown wasn't fully caused by the covered loss, or that some expenses weren't necessary.

That's why the financial proof has to be clean. Monthly sales history, seasonality, vendor interruptions, payroll continuity, canceled contracts, temporary operating changes, and relocation expenses all need support.

Depreciation and code issues are where estimates get shaved

Depreciation is one of the oldest carrier tools in the book. If they can characterize a component as old, lightly maintained, or near the end of useful life, they'll try to reduce payment even when the item was functioning before the loss.

You push back with condition evidence. Maintenance records. Service invoices. Pre-loss photos. Inspection reports. Replacement history. Anything showing the property or item was still serviceable before the damage.

Code work creates a similar fight. The carrier may label code-required items as upgrades or betterment. But if current rebuilding standards trigger additional work, that question should be analyzed against the policy's ordinance and law language, not shrugged off.

If depreciation is eating your estimate alive, read more about how carriers apply and policyholders challenge depreciation on insurance claims.

If you only argue about physical damage and ignore business interruption, code, and depreciation, you're leaving the back door open for the insurer.

When to Call for Backup Hiring a Public Adjuster in NC or VA

Some claim disputes can be pushed forward by an organized owner with a strong contractor and good records. Some can't.

If the damage is broad, the carrier's estimate is badly deficient, or the claim includes business interruption, competing scopes, contents issues, or repeated delay, you need somebody whose job is to build and negotiate claims for policyholders.

The right time to bring in help

Call for backup when any of these are happening:

- The offer doesn't match real repair cost: Your contractor says the scope is incomplete or the pricing won't perform the work.

- The claim has stalled: Weeks pass with repeated requests and no meaningful movement.

- The carrier keeps changing the story: Different adjusters, different explanations, no stable position.

- Downtime is becoming the bigger loss: Business income and extra expense are now central, not secondary.

- You're being pushed into their vendors or their math: That's when independent representation matters most.

If you're comparing options, a public adjuster works for the policyholder, not the insurer. For business owners in North Carolina and Virginia dealing with property losses, public claims adjuster help is worth reviewing before the claim hardens into a bad outcome.

What a public adjuster actually changes

A good public adjuster changes the file, not just the tone.

That means:

| Problem in the claim | What skilled representation can do |

|---|---|

| Thin insurer scope | Reinspect, expand scope, support hidden and consequential damage |

| Low pricing | Present independent estimating and contractor support |

| Missing contents support | Build inventories and valuation records |

| Weak business income presentation | Assemble financial documentation in claim-ready form |

| Communication chaos | Centralize submissions and force written responses |

For The Public Adjusters, Inc. is one example of a state-licensed public adjusting firm that represents policyholders in documenting and negotiating property damage claims in NC and VA.

A quick explainer helps if you want to see how this role works in practice.

You do not need to wait for a total denial to get help. In commercial property damage claims, the worst damage often comes from underpayment wrapped in paperwork.

Conclusion Take Control of Your Claim and Your Recovery

You don't have to accept a bad commercial claim outcome just because the insurer printed it on official letterhead.

The carrier's first offer is often a negotiating position built on a narrow scope, aggressive depreciation, incomplete contents evaluation, or a business interruption analysis that barely scratches the surface. If you treat that first number like a final answer, you relinquish an advantage you may never get back.

Take control by doing three things well.

First, read the policy like it's being used against you, because it probably is. Know the valuation language, the conditions, the endorsements, and the exclusions that the insurer is likely to invoke.

Second, build a claim file that is stronger than the carrier's estimate. Separate building damage, contents, and financial loss. Preserve evidence. Get independent repair input. Keep a clean communication log. Don't let the insurer turn your claim into a stack of disconnected documents.

Third, fight the hidden fronts, not just the visible ones. Business interruption, extra expense, depreciation, and code-related work can swing the value of a commercial loss just as much as the obvious physical damage.

The bottom line is simple. You paid for a policy. You are entitled to insist on the benefits the contract provides. That means you can dispute low-ball scopes, challenge missing line items, question valuation assumptions, and demand written support when the insurer's number doesn't reflect reality.

If the claim has become a grind, get help before more time and money bleed out of the business.

Have your water damage claim questions answered at NO COST. Call 919-400-6440 to speak with a licensed Public Insurance Adjuster or Contact Us here with questions. WE Work For YOU… NOT Your Insurance Company!

If your commercial property damage claim was delayed, underpaid, or buried under a low-ball estimate, For The Public Adjusters, Inc. can help you understand the dispute, document the loss properly, and push the carrier to address the actual scope of damage.